Fertilizers

UREA

|

|

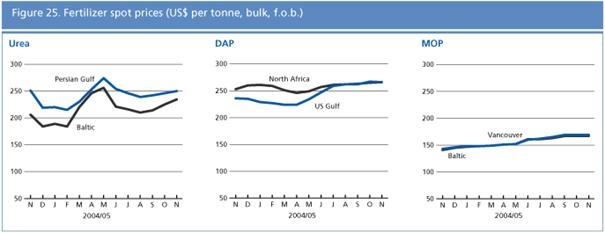

Urea prices are currently close to those at the same time last year: strong demand is expected to support prices in the near future. India and Pakistan are dominating the market, looking for amounts of 250 000 to 300 000 tonnes each: potential suppliers are the Russian Federation and the Persian Gulf. In India, the Department of Fertilizers has given permission to import 100 000 tonnes of urea for manufacturing of complex fertilizers, but no subsidy will be allowed on this urea. Domestic demand in China is slow and about 300 000 tonnes of urea will be available for export for November-December. It is still not clear if China will raise the export tax on urea next January but a 30 percent tax has been predicted, which means a doubling of the present export tax. The market in the United States is slow. Several import cargoes are still expected. Gas prices are still high and the spring season will presumably absorb all the imports.

DAP

|

|

DAP prices remained stable during the last months and are about 5-12 percent higher than a year ago. Prices are expected to remain relatively unchanged in the short term. In Africa, Ethiopia is reportedly importing a significant quantity of DAP form the Baltic Sea. Kenya is in the market for about 12 500 tonnes. Indian DAP production from April to October 2005 is about 1 million tonnes off target. Imports will fill the immediate gap, but the prospects for a sufficiently large inventory for the next season are reportedly not too good. Iraq closed a tender for 100 000 tonnes (shipment from December 2005 through February 2006). There is some small off-season demand from Mexico and Uruguay for December shipment. Brazil announced a joint venture to build a phosphate fertilizer production complex, which is expected to be commissioned in late-2007 to early-2008. It is reported that one of the United States DAP plants is to be shut down permanently. This plant produced about 10 percent of the countries annual average production of around 6.2 million tonnes. There may be some DAP available from the last production runs. Domestic DAP demand is slow but expected to strengthen from December through February.

MOP

|

|

MOP prices are about 20 percent higher than a year ago but are foreseen to remain constant in the near future. Canada is shutting down two mines for inventory purposes for three weeks; this might remove about 300 000 tonnes of MOP from the market. However, as production was up 4.1 percent over the last nine months and export plus domestic demand was down 4.4 percent, inventories have climbed to about 1.45 million tonnes of MOP by end-September (up 35 percent compared to last year). The EU intends to allow imports from CIS countries into the original 15 member countries (not only for the 10 new member countries) and dumping duties will be reduced. However, it is unlikely that this will undercut existing EU prices.

|