![]()

![]()

![]()

ALEX. R. ENTRICAN

Director of Forestry, New Zealand Forest Service

Paper submitted to the Fifth World Forestry Congress.

NEW ZEALAND provides a classic instance of a developing forest economy. It likewise provides a classic instance of the influence of prices on silvicultural practice. If the country's wasteful use of its virgin forest resource was typical of colonial development, its attempted correction by large-scale planting of rapidly growing exotics has been quite abnormal. Instead of plantings of each species being more or less uniformly spread over anticipated rotations, all were compressed into short periods representing from 5 to 20 percent of such rotations. Hardly had establishment been completed when the second world war broke out to create such a shortage of manpower that just when silvicultural treatment was most needed none could be carried out. The same condition continued well into the postwar period.

With the outbreak of war timber came under official price control, and has so continued ever since. It has in fact been under some form of price control for 24 years. As it was clear by 1952 that long continued price control was defeating the purpose of national forest policy, the matter was brought under parliamentary debate by suitable review in the Annual Departmental Report by the Director of Forestry. As a result of both Government and Opposition agreeing that the provision of cheap timber for house building was all important, subordination of forest policy to timber price control became bipartisan in character and still continues so. Peculiar as these conditions are it is nevertheless possible to draw many valuable lessons from the interplay between economic and political factors as they affect the silvicultural management of any country's forest resources, whether they be indigenous or exotic.

The author prepared a paper on " The Influence of Markets on Silviculture " for the seventh British Commonwealth Forestry Conference. It studied the impact of the great depression, the second world war, and the postwar economy upon the management of New Zealand's exotic forest resource. The purpose was to show how the conditions peculiar to these periods were turned to the advantage of the over-all national forest policy both by administrative control of the indigenous resource and development of integrated industries; and how thereby it was possible to alleviate the harmful effects of compressing the establishment of the exotic resource into a very short period. Ostensibly written to explain what had occurred, the paper in fact tended to show the compression of establishment and the lack of silviculture in the most favorable light possible. This paper has been written to highlight the technical and administrative problems created by large-scale exotic forest establishment compressed into a very few years, and the subsequent neglect of silviculture. It thus tends to present New Zealand exotic forestry in its least favorable light.

The decision of the Organizing Committee to distinguish between highly developed and developing forest economies was a wise one and of profound importance to the profession. Most reference works and text books the world over are based upon the concept of a stable forest economy. Much theory and practice proceed on a similar concept even though stable conditions do not exist and there is in fact a developing forest economy.

For the purpose of this paper a developing forest economy is regarded as one in which a country is in process of creating a forest capital, as distinct from a highly developed economy in which a country is already in possession of a forest capital adequate to its foreseeable needs and under sustained yield management for the maintenance of a widely diversified forest products industry.

The history of forestry in New Zealand is probably typical of colonial development in the nineteenth century. Much of the country, both lowland and high country, was under a dense forest cover, a great deal of it comprising a merchantable timber crop, but so remote from the world markets that it was a liability and not an asset to those pioneers who sought land for agricultural and pastoral development. On a conservative estimate not more than 10 percent of the merchantable forest growing on the land cleared for farming development was converted to sawn timber either for local use or for export to Australia - the only market within practicable reach. Exploitation eventually spread from the fertile lowlands to the less attractive hinterland and at such a pace that within a century of the first land settlement it became apparent that only by the establishment of a supplementary capital resource of rapidly growing exotics would the country be able to maintain self-sufficiency in timber supplies.

In 1925 the New Zealand government accepted and implemented a recommendation by its first Director of Forestry, Mr. L. McIntosh Ellis, for the establishment of 300,000 acres (120,000 hectares) of rapidly growing exotics over the following ten years. The purpose was to assist in meeting an expected annual timber requirement of 650 million board feet by 1965, by which time the indigenous forest resource would no longer be capable of wholly meeting such a demand for anything but a short period.

The compression of establishment into a ten-year period, even for such a short rotation species as Pinus radiata, was the result of previous experience in the field of national forest policy. Originally sponsored in 1870, exotic tree planting by the state did not commence until the turn of the century. But with numerous public agitations, a Royal Commission, and repeated departmental urgings, only 40,000 acres (16,000 hectares) had been planted by 1925. Fortunately, the first Director of Forestry conceived it as his duty, not only to alert the country to the seriousness of the situation, but to persuade government to overtake the arrears of forest establishment accumulated through past laissez faire.

A colorful personality with the prestige of overseas experience, Ellis created a wave of popular opinion which has outlived its expected ten years to carry national forestry on its crest ever since. It resulted not only in completion of his original program ahead of schedule, but in the generation of a boom program of private planting which established another 300,000 acres of rapidly growing exotics. Both state and private programs originally envisaged concentration upon the use of Pinus radiata, but only in the case of the private sector were suitable sites available to allow virtual attainment of this objective. In the case of state plantings a significant acreage of P. radiata was established on sites which had to be replanted to more suitable species.

With the development of the great depression of the early thirties the state program was accelerated and completed ahead of schedule, just at the time when public works of all kinds became essential for the relief of unemployment. However, an overseas visit at that time by the author confirmed the growing conviction that P. radiata, because of its vulnerability to a wide variety of insect and fungal pests, was being " over-planted." It was therefore decided that with the availability of unemployed labor at low wage levels this inherent risk should be corrected by extensive planting of the widest possible diversity of other rapidly growing exotic conifers, the limiting factors of course being site and seed supply. Pinus radiata continued to be planted, but only on the most suitable sites. The objective was to produce as rapidly as possible an annual surplus of 50 million cubic feet (1,400,000 cubic meters) of raw forest produce for export in the form of timber, pulp, or paper according-to the manner in which Australia and eastern markets for these commodities-might develop in the interim between planting and maturity.

In retrospect it might appear that much of the low cost unemployment labor available during the great depression could have been more usefully employed on tending some of the earlier planted stands than on planting new ones. The fact is that not only was the supervisory staff so inadequate as to preclude even satisfactory stocking or blanking of many areas, but departmental knowledge and experience of silviculture was so limited that poor value and much damage could well have resulted from any large-scale diversion of planting labor to tending work. Actually there were a few such mistakes.

With the outbreak of the second world war, the Director of Forestry became Timber Controller and as such had the responsibility of conserving manpower in respect not only of forest establishment and tending, but also of logging and milling. In the initial stages before the involvement of the United States, establishment and tending virtually ceased and timber production was curtailed. For the rest of the war manpower was barely sufficient to provide protection services to forestry, but with the United States taking over responsibility for the Southwest Pacific theater of operations, timber production had to be substantially increased, and logging and milling thenceforth commanded a high priority for available manpower.

This gave the forest and timber administration an unexpected opportunity of accelerating the development of the national forest policy - a policy directed toward the rapid substitution of exotic for indigenous timber supplies, thereby rationing and conserving the dwindling indigenous forest resources. The imperative necessity for conserving manpower in timber production thus made it both logical and feasible to integrate a national wartime timber production policy with the national forest policy. As indigenous sawmills exhausted their tributary standing timber supplies they were drifted out of production, and their staffs transferred either to other indigenous sawmills, or preferably to new or existing exotic sawmills. The premise was that consolidation of production nearer to established labor or consuming centers would be more economical, not only of manpower, but of essential supplies and transport. As a result, during the second world war there was a spectacular expansion of exotic sawn timber production which has continued almost without interruption ever since. It would have been even more spectacular had the state owned a larger proportion of the standing indigenous resources.

Since 1952 it has been practicable to continue the wartime policy of withholding new state forest resources from mills cutting out on old state forest locations, but it has not been feasible to persuade owners of Maori indigenous resources to do likewise. Because of this, the production of Maori-owned indigenous timber has increased fourfold since the war. Significantly, however, other private owners of indigenous forest have refrained in most cases from increasing production in order to ration out their resources as long as possible, and in the hope that this would favorably dispose the state to their future claims for indigenous state forest.

All this has been possible only because of a worldwide shortage of timber over both the second world war and its early postwar period. With such limited supplies of indigenous and imported timber available, consumers were then forced to use exotic or go without. In essence there was a sellers' market for 17 years, during which annual exotic production increased from 30 to almost 300 million board feet. Indigenous production remained virtually static at just over 300 million board feet throughout that period. It is extremely doubtful if, in the absence of the peculiar conditions of the second world war and the early postwar years, annual exotic production would have risen even to half its present level.

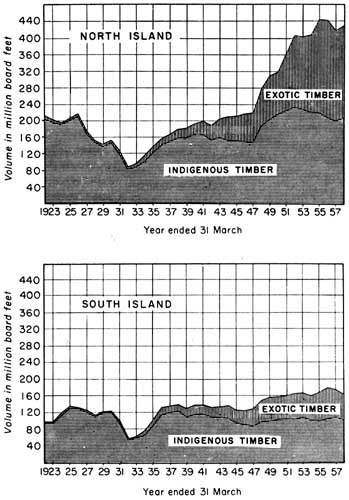

FIGURE 1. - New Zealand: Production of Bough Sawn Timber (indigenous and exotic)

Under such conditions of acute shortage and forced utilization, the sawn exotic product was poorly manufactured, badly graded, and ill seasoned. Naturally enough, not only wood users, but architects, engineers, and specifying and lending authorities tended to resist its substitution for the better manufactured and more valuable indigenous timbers. It was not until a buyers' market developed on both the domestic and the export markets in 1956 that exotic producers were forced to improve both the production and merchandizing of their product. Once this was achieved, the longer length specification of the exotics, combined with their ease of preservative treatment and of working, enabled them to capture some of the markets hitherto dominated by indigenous timbers. In particular they captured the structural framing field in the North Island, while in the cut-up field the factory grade of radiata pine commands a wide market both in New Zealand and in Australia. By improved servicing, the exotic producer is now in a very much more powerful position to compete with the indigenous producer.

Figure 1 demonstrates clearly the trend of both indigenous and exotic production over the period 1923-57, lending force to the claim that New Zealand is a classic instance of a developing forest economy.

Exotic forestry in New Zealand has not been without its insect and fungal troubles, but all have been of a secondary character. Probably only because of its geographical isolation has the country been free of any epidemic attacks of a primary nature.

On the pumice soils of the North Island, many of the pine stands, and particularly those of P. radiata, are characterized by a large proportion of malforms on all sites, the malformation of individual trees increasing with low stocking. Elsewhere on the poor clay sites in the far north and on the shallow gravelly sites in the south the proportion of malforms is lower than on either high quality agricultural loams or pure sandy sites. It is generally true that the poorer sites yield shaplier trees, more lightly branched although smaller, and with considerably less " natural mortality " than is met with on the better soils.

Many parts of New Zealand occasionally experience late spring frosts of great severity. In young P. radiata stands, these cause localized splitting of many leading shoots, thereby allowing infection by Diplodia or Phomopsis. Death of the leader and the subsequent development of double leaders often result. In the original ten-year establishment program a spacing of 8 feet by 8 feet (2.50 × 2.50 meters) was widely used. This gives a nominal stocking of 680 per acre (1,680 per hectare), a number which proved quite inadequate to take possession the site where the young stands suffered any significant mortality from drought or frost and subsequent fungal attack. And because of the pressure under which the program operated, beating-up to replace postplanting mortality was seldom possible. Even the 6 feet by 6 feet (1.85 × 1.85 meters) spacing - 1,210 per acre (3,000 per hectare) - adopted for some areas, often failed to yield a satisfactory final crop of well-formed trees in these circumstances.

Wet and dry periods of several years' duration likewise follow a cycle of about ten years, and a series of dry years favors the build-up of Sirex populations to epidemic proportions. Happily, however, damaging attacks by these wood wasps have so far been limited to trees with weakened sap flow due to the prolonged moisture deficiency. Significantly many of the malforms die, and in untended stands the damage is often spectacular. It is usually worse in the denser 6 feet by 6 feet stands of P. radiata than on the 8 feet by 8 feet stands, some of the former being decimated to the stage where only 30 green trees per acre (75 per hectare) are left at maturity. Some of these trees successfully resisting attack subsequently put on the extraordinary annual diameter growth of 2 inches (5 centimeters) for the next two years.

In essence, the epidemic Sirex attacks have killed virtually all those trees which should have been removed earlier in thinning, an operation rendered impossible by the war. The maximum basal area of Pinus radiata which the pumice sites of the North Island appear to be capable of sustaining against epidemic attacks of Sirex is about 200 square feet (20 square meters), giving at 30 years on Site II quality a growing stock of 7,000 cubic feet (200 cubic meters) to a 6 inch (15 centimeters) top diameter, and a current annual increment of 300 cubic feet per acre (20 cubic meters per hectare).

In view of these experiences it is not altogether surprising that both drill-sown compartments and fire-regenerated stands with stockings up to 10,000 and 500,000 per acre (25,000 and 1,250,000 per hectare) respectively are yielding untended, even on poor sites, more large, lightly lateralled, and better form trees than any other untended stands. To achieve the same result, much genetical research is currently being developed to reduce the high cost of thinning and pruning the 6-foot and 8-foot spaced stands.

As a result of the depression of the early thirties the bottom dropped out of the timber market, with the annual out falling from 300 million to 150 million board feet - most of it sold at well below cost of production. Prices remained at these levels even after the advent of the first Labor Government which, on coming to power at the end of 1935, restored wages to the 1931 award levels. In order to preserve the purchasing power of these wages the government negotiated an agreement with the timber industry whereby any advances in price were strictly limited to proven increased costs arising from both the restoration of wage levels and the increased cost of imported supplies and equipment. The idea was that the increased demand for timber arising from the government's large-scale state house-building activities would make the depression level of prices remunerative to the industry.

This gentlemen's agreement on prices operated until the outbreak of the second world war, when it was replaced by official control under appropriate wartime legislation. Official timber price control has continued ever since. With rare exceptions, the original basis of control has been observed, with increases limited to the covering of costs beyond the control of the industry that is due to increased wages and increased costs of supplies, plant and equipment. As originally adopted by the 1936 gentlemen's agreement the base prices of exotic and indigenous timbers were in no way related to one another. They merely reflected the then fortuitous depression prices for two classes of timber which were at that time being used largely for different purposes, and were not much in competition, with only about 35 million board feet as compared with more like 260 million board feet of indigenous timber.

At that time exotic timbers were being used mostly for the manufacture of the poorer type boxes and crates. The only purpose for which they were used by the building industry was for concrete boxing. Then as now, the exotic timber was knotty as compared with the clear and defect-rare grades of indigenous timbers. The latter therefore dominated not only the building and cut-up fields but virtually every other type of wood use, including manufacture of the better types of boxes and crates. Nevertheless, so great was the oversupply of the indigenous timber that, under the impact of the depression, the prices for indigenous timber were relatively very much more depressed than those for the exotic timbers. Timber price control, therefore, commenced with indigenous timber prices far too low, rather than with the prices of exotic timber too high. Neither was remunerative, even in covering costs of production.

As usual with the maintenance of price control in the face of imperfect coverage and oversupply, not only has it become increasingly ineffective, but there has been a gradual retreat from the original base relationship between the prices of indigenous and exotic timbers. Until recently the basic anomaly arising out of this relationship has been that producers of exotics have been forced to sell much of their production at best only medium quality timber - almost as highly priced as indigenous grades of very much higher quality. Naturally, the consumer has preferred to buy the indigenous product and has done so while supplies have been available.

The few exceptions to the general rule of limiting price rises to proven cost increases have been due to the development of uneconomic conditions in the industry, arising out of the time-lag between the development of increased costs and the approval of increased prices. The cumulative effect of a succession of such time-lags has forced the price control authority to approve from time to time special increases to improve the general economic return to the industry.

Superimposed on the general situation has been the postwar evasion of price control by a realization that legally control was limited to the prices of sawn timber. Just as soon as it became appreciated that there was no price control either over the basic raw material, whether in the form of standing timber or of logs, or over the cost of sawing or over the end-products such as manufactured joinery, and wooden houses, buildings, etc., a revolutionary change in the composition of the timber industry set in. Not only timber merchants but contractors and house builders commenced leapfrogging of sawn-timber price control. In some cases they purchased standing timber and logs and had the material logged and/or sawn to yield the finished product at costs much in excess of approved prices but for which they could compensate themselves by charging the timbers as manufactured joinery and houses at high enough figures to return a handsome profit. In other cases merchants and contractors purchased sawmills outright with the same end result.

In the face of the administrative action by the Forest Service to curtail production from state forest, the immediate effect of this change in the industrial structure was to trigger off large sales of Maori-owned resources in the form both of standing timber and of logs at prices anything from twice to thrice their economic value as related to controlled sawn timber prices. Eventually significant supplies of sawn timber produced via this uncontrolled route became surplus to owner-user requirements and were placed on the open market at higher than approved prices. As such producers were prepared to defend their right to recoup themselves by selling at high enough prices to return a profit on proven costs of production in efficient logging and willing operations, the industry was awarded another economic increase to accommodate the situation.

In the case both of normal and of economic rises the approved increases were invariably larger for indigenous than for exotic timbers. It was therefore only a matter of time before various developments inexorably tended to correct the disregard of economic laws implicit in the whole system of partial price control. With the ever increasing disparity in indigenous and exotic timber prices the competitive power of the exotics increased. Likewise, as the production and costs of indigenous timber from Maori resources increased and extended from a sellers' to a buyers' market, not only did the lower grades of indigenous timber from all sources become much more difficult to sell, but the prices of standing timber and logs from Maori resources have tended to fall quite significantly. Concurrently the prices of standing timber and logs from state forest resources have risen to the new economic levels determined by the increases in approved prim.

The basic cause of all these developments was the operation of the old law of supply and demand. With a surplus in total supply - that is indigenous plus exotic timber - the producers of exotics were forced to service the consuming public sufficiently well to overcome some of its preference for the indigenous timber. The position today is that even on a buoyant domestic market, though still in the buyers' favor, both indigenous and exotic producers are experiencing the same difficulty of quitting their lowest grades. While there is some valid value relationship between alternative grades of the indigenous and exotic timber, nevertheless approved prices continue to hinder optimum integration of the two classes of timber. Similarly, there are remnants of restriction on the use of exotics based upon both prejudice and administrative inertia.

Withal even optimum integration under existing conditions is unlikely to give the exotic grower an adequate return, Due to lack of silviculture his first rotation crop is producing such knotty logs that they are yielding nothing but low and medium grades. Without any significant quantity of highly priced defect-free or defect-rare grades he is unable to realize a remunerative stumpage for sawlog material. It is pertinent to observe, however, that even had no war intervened the compression of establishment of P. radiata into 10 years, instead of being spread over 40 or 50 years, would most likely have precluded intensive silviculture of any but the best stands and would have left the bulk untended. In retrospect there is little doubt that finance, manpower and supervision would have been seriously limiting factors in coping with the corresponding compression of silvicultural work into the short span of years during which tending is practicable in any such short rotation species as P. radiata. Equally important is the point that only interim experience has developed and is still developing correct silvicultural techniques.

There is no doubt that with the removal both of price control and of use restrictions the prices of the clear and defect-rare grades of indigenous would rise somewhat. This would have the twofold effect of restricting their use to essential purposes, and allowing the wider use of exotics for medium grade uses, thus returning higher prices to the exotic producer. Finally, this would return to the forest grower a higher price for his standing timber, which at the present time is so low that even with the high profits returned by paper and/or fibreboard products from integrated plants, it returns only about 3 percent compound interest on the original costs of establishment and maintenance over the last 40 years. Unfortunately these are but a fraction of the cost that it would now take, either to regenerate the crop naturally, or reestablish it de novo and maintain it over the next rotation. This is the essence of the financial problem which faces the New Zealand forest grower.

It is in striking contrast to the position of the Australian exotic forest owner who enjoys the advantage of having the price for his end-product determined by the high cost of landing New Zealand exotic timber in his nearby market. Thereby he secures not only the equivalent of the New Zealand price for standing timber but in addition the whole of the heavy trans-Tasman shipping costs. Australian stumpages therefore tend to be five times as high as New Zealand's exotic stumpages. As a result the Australian growers of P. radiata are able to apply such intensive silviculture as to force converters to saw logs down to a diameter inside bark of 3 inches (7.5 centimeters), as compared with a New Zealand economic minimum of more like 6 to 9 inches. Only in its few integrated plants is New Zealand able to use profitably any large quantity of the smaller material for pulp and paper. Elsewhere the market for posts for preservative treatment is so small as to be insignificant. Likewise the market for fuelwood is extremely small. Neither market is very remunerative.

No better instance of the influence of prices upon silviculture could be found than in this contrast between New Zealand and Australia. New Zealand, with a huge temporary surplus of exotica, is not only permitting the sale of logs to Japan, but is receiving such a poor return to the forest grower that both re-establishment and further expansion of the exotic resource, as well as the optimum silvicultural management, are threatened by the continued operation of price control and of prejudiced use restrictions. Australia, with an enormous shortage of softwood supplies, necessitating annual imports of 400 million board feet, is able to protect its exotic growers so that the stumpage on their thinnings, is five times that for New Zealand clear fellings, thus allowing optimum silvicultural management.

Without questioning the general desirability of a policy of economic stabilization during any war period, it would appear in retrospect as if a more liberal attitude could well have been taken by the government and the price control authority in the case both of the original base prices and of subsequent price rises. With stumpage as a residual value the forest grower has suffered the most, and though admittedly it was a shortage of manpower rather than of finance which prohibited silviculture during the war and early postwar periods, there is little doubt that interim strengthening of forest revenues would have ultimately resulted in a more sympathetic approach to such subsequent silviculture as was still practicable. The same effect would have resulted from a more liberal allowance to converters, whether they were sawmillers or pulp and paper manufacturers who were also forest owners. In actual fact, as control has relaxed and profits have increased, so have private forest owners tended to increase their silvicultural activities.

Nevertheless, it is necessary to terminate this section of the report with the inescapable conclusion that had it been possible to apply the correct silviculture as and when it was required, not only would the incidence of insect and fungal attack in the exotic forests been trifling but the substituting of exotica for indigenous timbers would have occurred automatically through preference of the wood user for the easy drying, treating and working qualities of the defect-free or defect-rare grades yielded by tended stands of general purpose exotic softwoods. It follows that the exotic grower would have received a very much higher stumpage, encouraging him to expand his resource and still further intensify his silviculture.

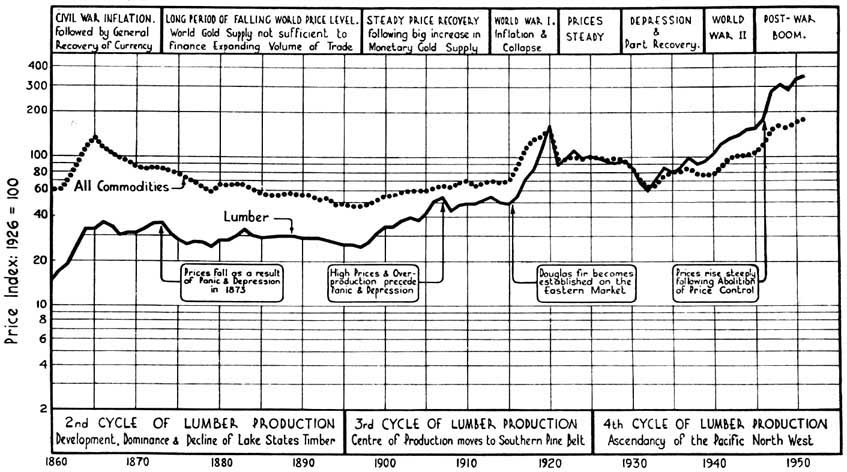

FIGURE 2. - The Relative Movement of Prices in the United States

In an effort to assure himself of the long-term financial prospects of exotic forestry in New Zealand as a source of supply for the international timber trade, the author ordered in the early postwar period a study of the long-term trend of timber prices relative to the movement of general prices. He wished to test a theory that, with the ever increasing remoteness of high quality virgin softwood lumber supplies as one forest region after another was exploited and exhausted, timber prices must be increasing relative to general prices.

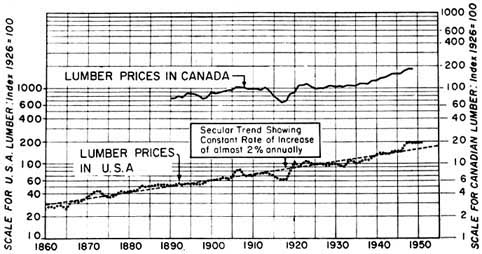

Figure 3. - Lumber Prices in North America corrected for Fluctuations in Currency Values

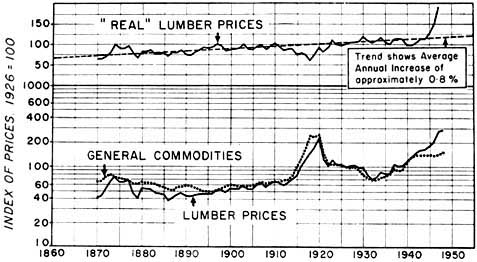

An unpublished departmental report by the Forest Service Economist, Mr. M. B. Grainger, sustained these views as may be gathered from a study of Figures 2, 3 and 4, which are largely self-explanatory. As regards the basic data used for all three graphs, suffice it to say that in each case a relatively homogeneous series was available. It is largely because timber prices in North America have, on a constant currency value, moved upward with remarkably little fluctuation for nearly a century at a constant rate of almost 2 percent annually that New Zealand has committed itself to the growing of exotics for the export trade. Exhaustion of the Pacific Northwest resource is in sight, and there are few other high quality virgin softwood resources left. The trend is likely not only to continue but eventually to increase.

The New Zealand decision presupposes that the improvement in silviculture which has been effected on state forests and others during the latter years of the postwar period will be continued. There is a full realization that unless silviculture can finally result in a significant yield of clear and defect-rare grades, participation in world trade is likely to be extremely difficult and unremunerative. " Real " lumber prices in Sweden have increased annually at an average rate of 0.8 percent. Even though Scandinavian forests do not yield any significant proportion of defect-free or defect-rare grades, the timber is of extremely high quality in the medium grades, as compared with New Zealand rapidly grown exotic softwoods. More significantly, Scandinavia is very close to the world markets for such timber.

FIGURE 4. - The Relative, Movement of Prices in Sweden

Experience on the export market to Australia fully confirms these views. There is little doubt that with a significant proportion of clear and defect-rare grades the exotic export trade could be increased from the current level of 50 to 150 million board feet annually, even to the extent of completely eliminating Scandinavian competition. But it cannot be achieved except by a policy of intensive silviculture, to which the profession must address itself.

If, however, the world trend in timber prices provides a happy augury for those countries contemplating an expansion of their forest resources, whether for internal or external trade, it is necessary to ponder the realities of current social and economic developments.

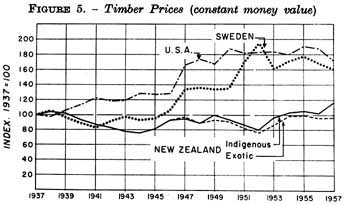

Figure 5 is taken from another unpublished report (1959) by the Forest Service Economist, Mr. M. B. Grainger, on the short-term influence of timber prices on the New Zealand forest economy. It compares the movement of sawn timber prices in New Zealand with those in the United States and Sweden from 1937 to 1957. As the common basis for comparison is in each case the level of wholesale prices in general (represented by the horizontal line 100) it can be seen that timber prices in the United States and Sweden have remained over the postwar period at anything from 40 to 90 percent above the general price level.

FIGURE 5. - Timber Prices (constant money value)

In contrast, the local price for the very high quality New Zealand indigenous timber in short supply has remained below the general price level for most of the period, and even now is less than 20 percent above, while that for the exotics still remains as it always has below the general price level. This is, of course, the effect of price control, and effectively demonstrates that however soundly based any forward long-term planning for forest development may be, it is subject short-term to the unforeseen exigencies of war and it's resultant social and economic upheavals. The one consolation left to the forester is that all economic laws are inexorable and that inevitably time will remove the short-term frustrations and allow the fulfilment of long-term plans and eventual attainment of objectives.

It can be stated with confidence that lumber prices on a worldwide basis have been rising steadily in relation to the general price level for the greater part of a century. The trend moreover is so pronounced, and the exhaustion of virgin softwood forest areas now so well advanced, that this appreciation of real lumber prices is certain to continue well into the foreseeable future. Such a trend is fundamental to the future of forestry and silvicultural treatment of the forests. It shows that over long periods there need be no fear that the increasing amount of necessary silviculture will be frustrated because of economic considerations, and it will give assurance to foresters to plan and work to optimum effect.

There is, of course, a school of thought that by disintegrating wood chemically and mechanically for the production of particle or fibreboard in substitution for natural wood products the silvicultural problems of the forester could be simplified. There have even been claims that thereby the profession would be justified in following a concept of quantity rather than quality production, the principal manifestation of which is the cult of open or widely spaced planting.

It is the author's contention that only by following the concept of quality production can either quantity production be achieved or forest soils be put to the optimum use for the satisfaction of the diverse requirements of mankind. Even though the geneticists are finally able to produce disease-resistant stock to yield inherently good form trees, the fact remains that only by a relatively high initial stocking can the soil be put to early optimum use. As the stand progresses from stage to stage and as the site finds itself unable to sustain continued growth of all living stems, either deaths must occur or the weaker be removed by thinning. Followed to an (il)logical extreme the forester would finish up with the equivalent of Nature's prolific regeneration by either windthrow or fire, which are so commonly the origin of the high quality virgin softwood resources of the world.

Obviously density of stocking must be determined by the two factors of labor costs and utilization practices. Of all peoples in the world, it augurs most for those of the underdeveloped countries in which low labor costs can be perfectly integrated with the utilization of almost miniature sized stems for fuel wood. At the other end of the spectrum a still fairly high density of stocking will be justified because of the increasing possibility of integrating chemical utilization of thinnings with saw timber conversion for the final crop trees.

The strength of the pulp and paper industry in particular, and of disintegrated products in general, in the world forest products economy is largely due to the fact that a significantly large proportion of the raw material is secured as a low value residue from both forest and sawmilling operations which carry by far the greater part of the cost of both growing and conversion. Had chemical utilization to carry its full share of growing and conversion costs its competitive power in the world economy would be significantly lowered. Slowly but surely, however, it is being forced to make a greater contribution to both growing and converting costs. Concurrently the premium on high grade over low grade lumber is increasing, and as the high quality virgin softwood resources disappear so will this premium increase.

Because of the relatively low labor, power, plant and investment costs in sawn timber conversion and plywood manufacture, as compared with the relatively high corresponding costs for chemical utilization, the natural products will always remain strongly competitive with the chemical products, there being little doubt that combinations of the two classes of products may afford the most economical utilization of the raw forest material.

Against this background it is believed that silviculture must remain forever the principal toot of the forester in the economic use both of the forest soils and of their products.

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}