![]()

![]()

![]()

BACKGROUND

Several countries of the Asia-Pacific region have imposed total or partial logging bans (or similar restrictions on timber harvesting) in natural forests as a response to natural disasters that are widely believed to have been caused by deforestation or degradation of forests. Banning or restricting timber harvests has thus been viewed as a corrective measure and as a strategy to promote forest conservation and protection, and to assure broader forest benefits for the future.

Other countries in the region are currently considering logging bans or restrictions, along with other options such as long-term multiple-use forestry, sustainable forest management, and modified or reduced impact logging (RIL) practices. It is thus important to assess the experiences of various countries in the Asia-Pacific region for indications of the efficacy of removing natural forests from timber production in achieving conservation goals.

The study of the efficacy of removing natural forests from timber production as a strategy for conserving forests, conducted at the request of the Asia-Pacific Forestry Commission (APFC) and coordinated by the FAO Regional Office for Asia-Pacific, sought to review the experiences with logging bans in selected countries. The objectives were to:

REGIONAL OVERVIEW

Over the last two decades, serious and growing concerns regarding the status and use of natural forests have emerged. In spite of long-term forest management systems and extensive reservations of natural forests for conservation, deforestation and degradation have continued at alarming rates. Successful reservations, which create a variety of protected areas, commonly prohibit commercial timber harvesting, and often strictly limit or prohibit other non-commercial forest uses for both timber and non-timber purposes. Creation of protected areas is normally the result of policy processes where non-timber priorities are deemed to outweigh timber values. Reservations for national parks, wildlife habitats, biodiversity, critical watersheds and other special purposes, remove forests from timber production and thus affect sustainable timber supply. Furthermore, declaration of protected areas does not guarantee effective protection, administration or active management for the intended purposes. Adequate human and financial resources, and, most importantly, a broad social consensus and support are required, particularly where forests have traditionally been a source of livelihood for local families and communities.

Logging bans to conserve natural forests

Despite such deliberate conservation efforts and the creation of protected areas, deeply rooted misgivings about conventional forest management and policies of timber harvesting and utilization abound. These misgivings rest on numerous perceptions about the negative consequences of previous uses of the natural forests and corollary assumptions about the desirability of shifts in policies that give greater priority to “forest conservation.” Many believe that even more of the natural forests should be allocated to primary uses, e.g. biodiversity conservation, habitat protection, environmental protection, watershed and soil and water conservation. Such uses are often perceived to be incompatible with timber harvesting, thus resulting in growing demands for logging bans even outside existing protected areas.

Continued deforestation and forest degradation are seen by some people as evidence of management and policy failures to provide sustainable timber supply and environmental protection. For them, logging bans have become an expedient mechanism to prevent further damage and to allow for forest restoration.

Questions about whether timber production is in fact compatible with sustainable forestry in the broader economic and environmental context are being raised more frequently. Sustaining timber production may generate negative consequences or reductions in other multiple-forest values, e.g. stream siltation impacting water quality, inducing flooding or reducing hydroelectric capacity of reservoirs. Thus, even if management is “sustainable,” a bias toward timber may lead to a less efficient “mix” of overall values than might be obtained from the same natural forest base.

Given the widespread concerns about the consequences of past natural forest uses, as well as the declining area and degraded condition of much of the remaining forests, should more forests be subjected to logging bans in favor of natural forest conservation? If so, where will timber come from in the future? Is the present level of harvesting sustainable and consistent with environmental priorities? Will new supply sources be required? Can forest plantations provide a meaningful alternative to continued deforestation and degradation of natural forests?

Natural forests of the Asia-Pacific region

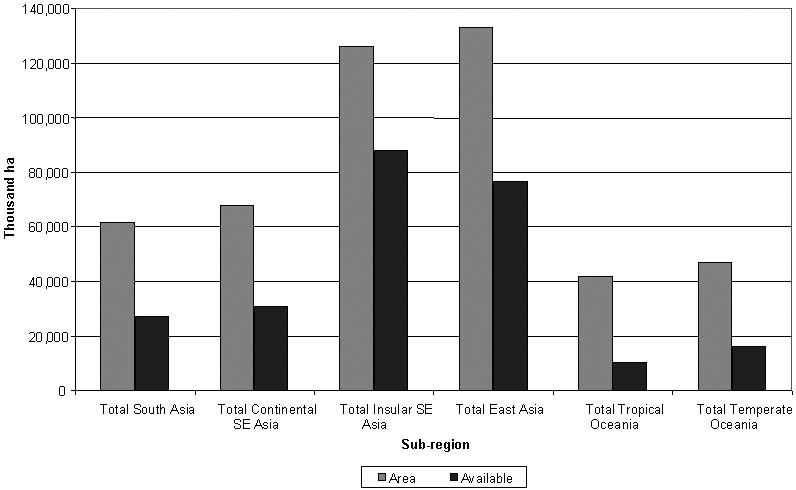

The Asia-Pacific region covers over 552 million ha of forests, of which 477.7 million ha are natural forests. However, only about 249 million ha are available for harvesting. The distribution by geographic subregion is shown in Figure 1.1 Insular Southeast Asia and East Asia dominate in terms of both total natural forests and the area available for harvesting. About 236 million ha are unavailable for harvest at present, including 89.5 million ha in legally protected areas and 146.5 million ha that are unavailable due to physical and economic constraints.

The region has experienced continuing deforestation and degradation, showing a decline of almost 16.3 million ha of natural forests, or approximately 3.3 million ha annually from 1990 to 1995. The largest losses were in Indonesia (5.4 million ha), Myanmar (1.9 million ha), Malaysia (2.0 million ha) and Thailand (1.6 million ha). The Philippines had the highest rate of deforestation at 3.5 percent annually, followed by Pakistan (2.9 percent), Thailand (2.6 percent), and Malaysia (2.4 percent). In addition, continued heavy cutting and lack of reforestation and afforestation have added to the problem2.

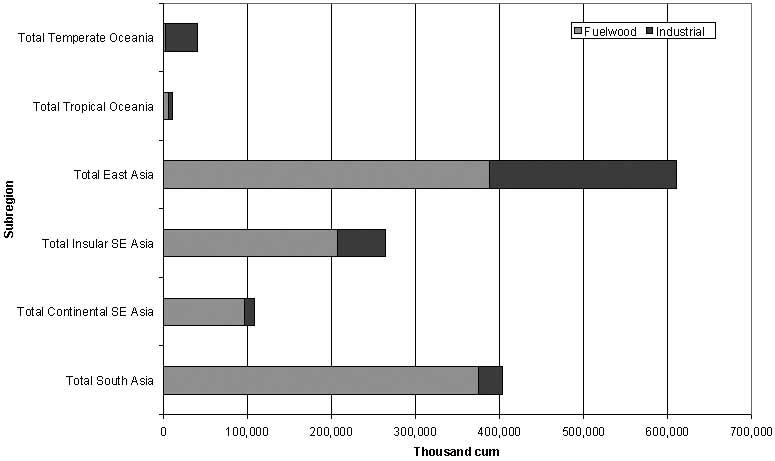

A substantial amount of roundwood, both for firewood and as industrial roundwood, is produced in the region. In 1999, the estimated production was approximately 1 438 million m3, including 1 075 million m3 of fuelwood/charcoal and 364 million m3 of industrial roundwood (Figure 2).

Figure 1. Natural forests in Asia-Pacific: total area and area available for harvesting

Figure 2. Asia-Pacific production of roundwood by type and subregion, 1999

Fuelwood made up a significant proportion of removals in the region, particularly in India with 297 million m3 of fuelwood and charcoal used annually. China (204 million m3) and Indonesia (153.5 million m3) account for a larger portion of the remaining firewood use.

Industrial roundwood production was primarily from East Asia (China) and Insular Southeast Asia (Indonesia and Malaysia). Oceania production was almost entirely from New Zealand and Australia, with a moderate volume (3.2 million m3) from Papua New Guinea3.

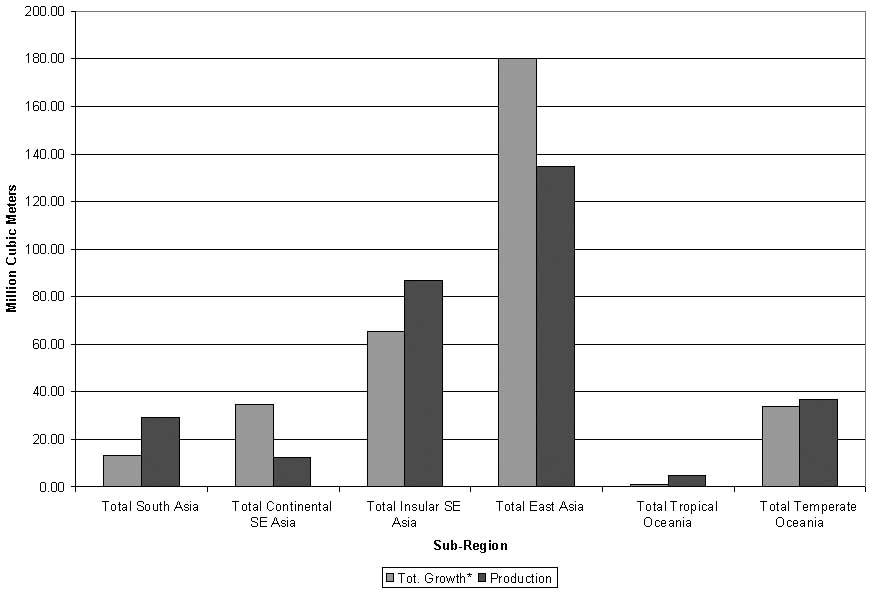

The comparison between industrial roundwood production and the estimated growth of commercial species on available natural forests is summarized in Figure 3. Total growth is estimated at 328 million m3, and industrial roundwood production is 304 million m3. While East Asia (China) shows an apparent volume of growth versus harvest, South Asia and Insular Southeast Asia both have large deficits in estimated growth against harvests. These subregions, together with Continental Southeast Asia, demonstrate high rates of deforestation and also face significant challenges in the production of fuelwood and charcoal. Temperate Oceania shows a slight imbalance.

Plantations in the Asia Pacific region

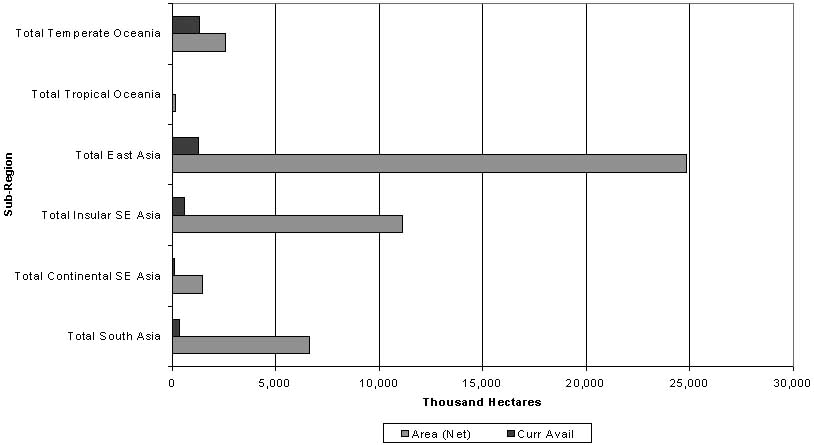

The Asia-Pacific region has a reported 57.4 million ha of industrial plantations, with a net area of approximately 46.8 million ha. However, only 3.5 million ha of industrial plantations are considered presently available for harvest (Figure 4).

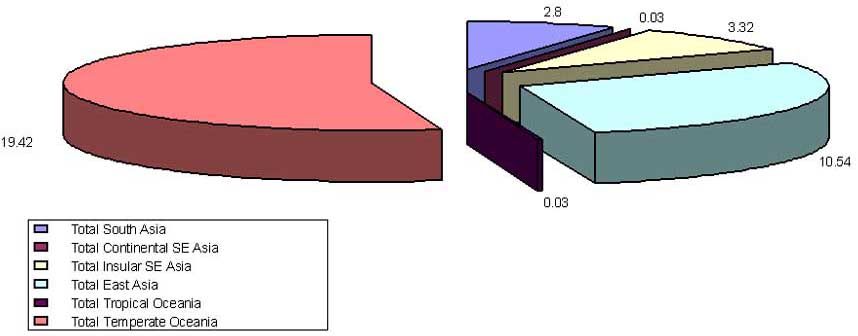

Large areas of industrial plantations in India, Malaysia and China are still young and immature, and as yet incapable of significant contributions to timber harvests4. The estimated annual growth of the Asia-Pacific industrial plantations available for harvest is 36.1 million m3 (Figure 5). By subregion, the highest share is in Temperate Oceania with a growth of 19.4 million m3 per year (Australia and New Zealand), followed by East Asia with growth of 10.5 million m3 per year (primarily China).

Figure 5. Estimated annual growth of available industrial plantations in Asia-Pacific by subregion

Experiences with logging bans in Asia-Pacific

The goals for timber harvesting bans in Asia-Pacific are seldom well articulated. Most bans are a response to forest policy “failures.” The undesirable outcomes from conventional forest practices and utilization are presented in arguing for swift and decisive actions to correct past problems and abuses.

Deforestation and forest degradation of natural forests are common and central themes in logging ban decisions. The problems of over-cutting beyond sustainable levels, the impact on other forest values and the assumed incompatibility of logging with the protection of environmental functions and related uses are typically intertwined. Loss of biodiversity, critical habitats and representative ecosystems, the deterioration of watersheds and water quality, soil erosion, sedimentation and flooding are frequently perceived as consequences of conventional forest practices and harvesting. Inefficient and poor logging technology and related practices have also been identified with damage to residual forest stands. Coupled with the lack of effective reforestation, these factors are often seen as serious consequences of logging. Opening of forests for uncontrolled human migration is blamed for a variety of undesirable, but non-forestry based, land-use consequences.

Logging bans can cause considerable, unanticipated impacts on timber supply. They can indirectly affect sectors and individuals dependent upon forest harvesting, transport, processing and consumption of forest products. Forest plantations are commonly seen as a logical alternative timber supply source. Seldom, however, are such linkages explicit in logging ban policies, legislation or implementation. An assumption of continued national self-sufficiency in timber supply, under conditions of growing demand, is implicit in almost all instances reviewed in this study. The growing role of economic reforms towards more market-based production and consumption decisions, together with the implications of open international trade in forest products, are only indirectly acknowledged in national logging ban policies.

SUMMARY OF COUNTRY CASE STUDIES

As part of the APFC study, case studies for six countries were conducted to assess major efforts in applying logging bans comprehensively to natural forests outside established protected areas. In addition, countries that are considering further restrictions on harvesting, or where bans have been recently announced but not fully implemented, were reviewed to gain further insights. The six countries selected were New Zealand, People’s Republic of China, Philippines, Sri Lanka, Thailand and Viet Nam. A brief summary of each case study is provided here as background to the overall findings and conclusions.

The experiences and findings from the six country case studies illustrate the linkage between natural forest conservation (objectives) and logging bans (means) for major policy decisions on natural forests.

New Zealand

New Zealand has approximately 8.1 million ha of forests, including 6.4 million ha of natural forests. Its logging ban will eventually affect 5.1 million ha of State-owned natural forests. Sustained yield restrictions were placed on another 12 000 ha of State-owned and 1.3 million ha of private natural forests as a result of major government policy changes in 1987.

Before 1987, logging was prohibited in some 300 000 ha of State-owned forests, including 80 000 ha that were previously classified as production forests. Policy changes, initiated in 1987, resulted in 4.9 million ha of State-owned natural forests being transferred to permanent conservation status under separate administration, including an estimated 1 million ha of State-owned natural forests with a potential for harvesting under sustainable forest management. An additional 670 000 ha of private natural forests are under voluntary protection agreements and restrictions, although only 124 000 ha are considered to have commercial potential.

In 1987, the Government began to phase out the public sector from the management and development of planted forests, simultaneous with imposing more restrictive measures for logging in natural forests. There are an estimated 1.7 million ha of planted forests, most of which are over 10 years of age. The area of mature plantations is expected to double during the next 10 years. A key aspect of the Government’s policy has been to sell the State plantations to private enterprises. Six firms now hold approximately 50 percent of the plantations, with individual holdings of over 50 000 ha each.

The New Zealand plantation program was initiated in the 1920s and 1930s, when it was foreseen that the capacity of the natural forests was being reduced and could not be expected to play a significant role in future timber supplies. Plantations of fast-growing softwoods (conifers), rather than imports, were seen as the logical resource substitute. A second phase of plantation development occurred in the 1960s and 1970s by the State, with the private sector continuing a rapid pace of planting in the 1990s to the present.

Conditions have been positive for plantation development in New Zealand. Relatively flat land is readily available for planting, particularly in the central part of the North Island. Population density is low, and local domestic demand for timber is modest. By early 2000, an estimated 1.7 million ha of commercial plantations, comprising 1.5 million ha of radiata pine and smaller holdings of Douglas fir and other introduced hardwoods, were established.

New Zealand’s timber harvest remained below 4 million m3 through the 1950s. By 1954, harvests from plantations overtook natural forest production at approximately the 1.9 million m3 mark. In 1970, about 6.8 million m3 were harvested from State-owned and private plantations, while natural forest harvest fell below 1 million m3. Plantation harvest has increased steadily to over 16 million m3 from 1996 to 1999, while natural forest production fell to below 90 000 m3 (with about 30 000 m3 coming from residual State-owned natural forests on the South Island West Coast, and the balance from private and Maori lands). Restrictions on private natural forests were progressively introduced with the Forests Act amendment of 1993, allowing for a gradual shift to alternative wood sources until the plantations are mature enough to be harvested.

The annual sustainable cut from plantations is expected to be 30 million m3 by 2010, compared to the 1999 production of 17 million m3. While volume is much greater than the declining natural forest harvests, the primary concern is the technical feasibility of radiata pine to substitute for natural forest species. There is currently no consistent supply of specialty or decorative natural forest timbers.

Much of the production from plantations is exported as logs or sawnwood and a range of finished products. In 1998, some 10.7 million m3 of logs were processed in New Zealand and 8.6 million m3 were exported. New Zealand is poised to be in a favorable position to supply plantation timbers to the Asia-Pacific region if radiata pine can meet consumer demands.

People’s Republic of China

Based on the 1993 forest inventory, China reported a total of 133.7 million ha of forests, with natural forests occupying 99.5 million ha (approximately 74 percent). Natural forests under protection covered 20 million ha in area, with scattered natural forests accounting for 17.7 million ha. China estimates that some 49.6 million ha of natural forests are in need of greater protection. Responding to natural disasters, China has established a priority for natural forest conservation and protection, shifting timber production to forest plantations.

Reflecting concern for the deterioration of the forest environment, and stimulated by severe flooding in the summer of 1998, China imposed a logging ban in State-owned forests to include the upper reaches of the Yangtze River and the middle and upper reaches of the Yellow River. In addition, the Natural Forest Conservation Program (NFCP) stressed the need for afforestation and greening of wastelands, increasing forest cover, rehabilitating forest stand qualities and expanding forest eco-functions.

The estimated total supply for China’s timber markets from both State and non-State sources increased from 52.3 million m3 in 1983 to 83.9 million m3 in 1987. After a brief decline, supply increased to over 90 million m3 per year from 1994 to 1996, and totaled 87.6 million m3 in 1997. Non-State forests have supplied more than 20 million m3 annually since 1992.

The NFCP aims to reduce natural forest timber production from 32 million m3 in 1997 to 12.1 million m3 by 2003. Strict logging bans will be imposed on 41.8 million ha of natural forests.

China is seeking alternative timber supplies by expanding its forest plantations and imports. It has aggressively pursued a program of establishing forest plantations, and has an estimated 34.3 million ha of plantations, of which 17.5 million ha are industrial timber plantations.5 Current forest plantations are relatively low in quality and their outputs are still below expectation. However, they may become the main source of industrial timber if they can meet the projected 39.3 million m3 of timber output by 2005. This will require improving forest management practices and adapting the plantation areas and species structure to market demands.

The volume of timber available for domestic consumption averaged 91.3 million m3 per year from 1993 to 1997. The volume of timber available is declining, while domestic consumption is increasing. Harvest reductions are to be phased in slowly to facilitate production and market adjustments. Initially, the shortfall is to be met by using old timber stocks and imports. Long-term supply is to be derived from both domestic and international sources.

Domestic supply will be stimulated through more intensive forest management (tending and thinning) and through technology and science to improve the utilization rate of forest resources. Substitution of wood-based panels for sawnwood, based on improved recovery and utilization of wood residues, is estimated to have saved the equivalent of 5.1 million m3 of standing timber.

China’s imports of logs totaled 93 million m3 from 1981 to 1997, averaging about 5.5 million m3 annually. Maximum import of logs was 10.7 million m3 in 1988. An increasing proportion of sawnwood and plywood has also been imported. China eliminated tariffs on logs in 1999, leading to a substantial increase in imports of logs (9.1 million m3, 115 percent increase) and sawnwood (2.4 million m3, 65 percent increase). Its trading partners have been the United States, Canada, Northern and Western Europe, Russia, Africa, and South America. Within the Asia-Pacific region, China traded most extensively with Indonesia, Malaysia, Philippines, Laos and Myanmar. It has also shown strong interest in the forest resources of Oceania, including Australia and New Zealand.

China concluded that although opportunities exist to increase timber supply outside the natural forests, e.g. through plantations and intensive management, the gap between supply and demand will continue to increase, necessitating more timber imports.

Philippines

The Philippines has about 15.9 million ha of land which is officially classified as “forestland,” although most of it is without tree cover. There are a little over 5 million ha of residual and old-growth natural forests, almost all of which are publicly owned. Some 20 million upland residents, including an estimated 6.3 million indigenous people, live in officially designated forestlands. There is widespread poverty in the uplands. The incidence of upland migration and illegal harvesting is high. Low royalty charges, and abuses of logging concessions led to over-cutting of forests. Ineffective operational management and population pressures have resulted in highly degraded natural forests. More than 5 million ha of public timberland have no clear form of tenure or management, essentially creating “open-access.”

Annual deforestation reached a high of about 300 000 ha from 1977 to 1980, decreasing to about 100 000 ha annually in the 1990s.

The Philippines has 1.38 million ha of watershed forest reserves. However, these areas generally do not have approved management plans or sufficient budgets for operational management. Most of the 1.34 million ha of protected areas also have no approved management plans.

Logging bans have been selectively imposed since the early 1970s on a case-by-case basis. General bans were initiated in 1983 covering much of the Philippines, with additional specific bans in 1986 and 1989. More that 70 percent of the provinces are now under logging bans or harvesting moratoria. The number of timber license agreements has been reduced from 114 in 1989 to 21 in 1998 down to 18 at present. The area under license has decreased to only 0.5 million ha. In 1991, the DENR issued an administrative order banning timber harvest in all old-growth forests of the Philippines. Similarly, the annual allowable cut was reduced sharply from 5 million m3 in 1990 to about 0.5 million m3 at present.

At present, two proposed bills are under consideration. The first, Senate Bill S. No. 1067, “An Act to Protect the Forest by Banning all Commercial Logging Operations, Providing Mechanisms for its Effective Enforcement and Implementation and for Other Purposes” would prohibit all commercial logging operations in all types of forest for a period of 20-30 years. The second, “An Act Providing for the Sustainable Management of Forest Resources and for Other Purposes” (Senate S.B. 1311) allows for logging in some residual forests and would constitute a partial ban (fragile areas, steep slopes, protected areas) and provide for sustainable management.

In 1998, the estimated demand for timber was about 5 million m3. This is expected to grow by about 2 to 5 percent annually. At present, the timber supply is comprised of about 588 000 m3 (or 12 percent of demand) from harvests of natural forests mostly under existing licenses and communities, 796 000 m3 (16 percent) from imports, about 721 000 m3 (14 percent) from coconut, and only 45 000 m3 (or 1 percent) from plantations. Over 57 percent are not formally accounted for and are believed to comprise “substitutes” (steel and cement) and illegal supplies of timber.

Plantations have been called the “only reliable source” of timber, together with the sustainably managed natural forest still under timber license agreements. Between 1986 and 1996, the Government and private sector developed 773 000 ha of plantations. However, only about 36 percent of the plantations are presently available for harvest. Current estimated yields are only about 300 000 m3 annually for the next decade, although projections made in 1990 forecast an output of 2.77 million m3 by 2000.

Government policies on industrial plantations have changed about 20 times between 1975 and 1995. This has caused instability and uncertainty, and subsequently very low investment. Weak incentives have led to only marginal private sector involvement, discouraging further expansion. Restrictions, lack of long-term financing, the need for local collaboration, and policy uncertainty all contribute to the low level of plantation establishment and management.

In lieu of a stronger role and capacity for plantations, the Philippines has shifted to imports as a source of timber supply. With an initial volume of about 400 000 m3 in 1989, log imports rose to more than 750 000 million m3 in 1997. Total imports increased from 5.5 percent of supply in 1989 to 16-20 percent in 1996-1997.

Sri Lanka

The natural forests in Sri Lanka are owned and managed by the State. In 1992, they covered about 2 million ha, out of which 1.5 million ha were closed forests. The State also has a monopoly on harvesting and marketing of timber from these forests and State-owned plantations. The Forest Department manages approximately 60 percent of the natural forests, while the Department of Wildlife Conservation oversees about 30 percent of forests located in protected areas. The Forest Department is also responsible for about 135 000 ha of forest plantations.

In 1989, a “temporary ban” on logging in natural forests was imposed on highly degraded areas to allow them to recover and to develop sustainable management plans, primarily in the wet zone in the southwest of the island. This was extended to a total ban in 1990, at which time another 31 areas, covering 61 300 ha, were added to the protected area system. Overall, the ban affects about 1 million ha of production forests. In 1995, a large proportion of natural forests was given protected area status, and residual natural forests outside the protected areas were set aside for sustainable multiple-use management.

Prior to the ban, the demand for industrial logs in 1985 was approximately 980 000 m3, of which 425 000 m3 (44 percent) were sourced from natural forests. Non-forest wood supplies - mainly from homegardens, rubber, coconut and palmyrah plantations - amounted to 455 000 m3, and forest plantations provided 80,000 m3 of industrial wood. By 1993, homegardens, rubber and coconut plantations supplied over 70 percent of wood while plantations contributed about 4 percent. The State Timber Corporation (STC) harvests from natural forests have declined sharply, and since 1990 State plantations are the main source of timber for the STC.

Plantation forestry began after the formulation of the first Forestry Policy in 1929, with extensive planting of teak, eucalyptus, mahogany and pine. From the 1950s to 1970s, emphasis was on industrial forest plantations, but the focus shifted to developing private woodlots and forestry farms in the 1980s. Industrial plantations on State lands were extended to local people, rural communities, industry and other private organizations. By 1998, the Forest Department was managing 92 340 ha of State plantations, in comparison to the 5 000 ha of private plantations. Annual timber production from plantations is expected to be about 90 000 m3 between 1999 and 2005. This will likely cover only 36 percent of the anticipated gap between demand and supply of logs. Actual plantation harvests averaged 37 700 m3 from 1985 to 1989 and only 27 100 m3 since 1990.

Sri Lanka was essentially self-sufficient in timber prior to the logging ban, with fuelwood demand accounting for some 90 percent of utilization. Industrial log production in 1985 was about 980 000 m3. Log imports were modest. Between 1985 and 1995, annual sawnwood imports ranged from 21 000 m3 to 38 000 m3; Malaysia, Singapore, South Africa and Indonesia were the main suppliers. Sri Lanka is also a net importer of wood-based panels but in modest volumes. Imports were 30 000 m3 in 1995.

Lack of proper management and inappropriate species, encroachment, fire damage, elephant damage, and the poor quality of plantations have all limited the plantations’ harvest potential. Incentives for private development of commercial plantations remain weak. Non-forest timber from homegardens and increased sawnwood imports have largely met the shortfall in industrial wood supply created by the logging bans in Sri Lanka.

Thailand

Thailand has experienced continuing deforestation over the last three decades, often at rates exceeding 3 percent per year. Forest cover declined from 53.3 percent of the land area in 1961 to 25.3 percent in 1998, leaving approximately 12.9 million ha of natural forests. Thailand has approximately 8.1 million ha of natural forests in protected areas, with additional areas pending approval. The large rural population that inhabits many of these areas is a major concern. Reforestation and rehabilitation of degraded forests are difficult or impossible because of illegal forest encroachment.

The logging ban in Thailand was imposed on 17 January 1989 in response to devastating floods in Nakorn Srithammarat Province in southern Thailand the previous November. Logging contracts and concessions were cancelled, and applications for new concessions were dismissed. In 1991, the Government reoriented its forest policies to emphasize management of some 27.5 percent of the land area as conservation and protected areas.

In 1992, the Government, through its Forest Plantation Act, encouraged forest industries to develop large-scale commercial plantations to supplement the State’s efforts. A forest plantation plan for 1994-1996 aimed to establish 800 000 ha of new plantations by both the private sector and Government. The Act also allowed local private sector groups to use degraded forestland with a special exemption from royalty fees. By 1997, however, it was clear that the goals of the reforestation programs would not be on schedule. Some 437 000 ha had been “reserved,” but planting was completed on only about 165 000 ha.

The pursuit of large-scale, industrial plantations has faced strong opposition from local farmers and villagers who believed that commercial plantations would divert land from local use and deprive them of their livelihoods. By the end of 1992, most large-scale commercial reforestation was halted. Since then, efforts to promote small-scale plantations with local participation have been undertaken, but with only little success. Bureaucracy, over-regulation, lack of economic incentives and the long gestation periods are seen as serious constraints to plantation development. Furthermore, the market system for the production, distribution and consumption of privately produced timber is weak, with consequent inefficiencies and loss of value.

From 1906 to 1997, between 850 000 and 900 000 ha of plantations were established, in sharp contrast to the reduction of approximately 14.4 million ha of natural forests from 1961. Thailand has an implicit policy of maintaining self-sufficiency in timber, but has often been accused of turning a blind eye to illegal logging and is increasingly dependent on imports from its neighbors and the expanding Pacific Rim market to meet its needs. The country has promoted an import policy and reduced log import tariffs. Myanmar has been a leading source of timber, leading to armed conflicts among different factions in Myanmar over log trade routes. Along the Thai-Cambodian border, log trade - much of it illegal - is estimated to have reached 750 000 m3 prior to the Cambodian export ban in December 1996.

Domestic wood production was reported to be 54,800 m3 in 1998, down from a high of over 2 million m3 in 1988 prior to the log ban. No separate data are reported for production from natural forests or plantations. However, it is clear that plantations are not yet meeting expectations, nor are they currently supplying a significant volume of industrial timber.

Viet Nam

Viet Nam’s forest cover is about 10.9 million ha, comprising one-third of the total land area, including 9.5 million ha of natural forests and 1.4 million ha of planted forests. In 1995, the production forests were about 5.9 million ha, which included 5.3 million ha of natural forests and 631 000 ha of plantations. The remaining forests were set aside as special-use forests (898 000 ha), and protection forests (3.5 million ha).

Between 1943 and 1995, about 110 000 ha were deforested annually. Concerns about the continued deforestation and degradation of the remaining forests led to a variety of restrictions on logging in the natural forests in the early 1990s. By 1995, State-owned production forests were yielding only about 1 million m3 of wood annually, mainly from depleted secondary forests.

In June 1997, the Government imposed the logging ban in natural forests on 4.8 million ha. It prohibited harvesting in special-use forests, and declared a 30-year moratorium on logging in critical watershed protection forests. Logging in the remaining natural forests is restricted to less critical natural forests in 19 provinces. Annual harvest volumes were expected to drop from 620 000 m3 in 1997 to 300 000 m3 by 2000. The number of enterprises permitted to log was reduced from 241 in 1996 to 105 by 2000.

Total industrial roundwood output declined from 3.4 million m3 in 1990 to 2.2 million m3 in 1998. Production from the State sector declined from 1.1 million m3 to only 300 000 m3 during the same period. Similarly, fuelwood exploitation decreased from 32 million steres to 25.9 million steres. Due to the timber shortages and the logging ban, the volume of illegal logging increased to at least 100 000 m3 annually.

Current timber supply is estimated at 1.35 million m3 of large-diameter wood (>30 cm) and 900 000 m3 of small-dimension timber. Large-dimension timber from natural forests is about 300 000 m3 under approved licenses, and as much as 100 000 without license. An additional 700 000 m3 are obtained from plantations (incl. rubber), and about 250 000 m3 are presently imported. Most of the large-dimension timber is used to produce sawnwood, with small volumes going to the handicraft and other sectors including pulp and paper. Small-dimension wood from plantations is used for basic construction, wood-based pulp and paper, pit props, matches, firewood, wood chips (for export) and boat building. Total demand is estimated to be over 4 million m3, suggesting shortages of 1.5 to 2 million m3 until 2005 when more plantation wood should be available.

Total annual wood imports (large and small dimensions) are estimated at 300 000 m3. It is expected that imports of industrial wood will increase to over 500 000 m3 per year from Malaysia, Laos, Cambodia, Myanmar, and Russia. Although the Government coordinates the flow of imports, some provinces close to Laos and Cambodia have direct contacts with the suppliers.

According to national policies, future wood supplies are to be secured only from plantations. Development of forest plantations has been slow, but has picked up recently. The volume harvested from plantations is increasing gradually. Most plantations are immature, and are located in the central and northeast regions. Under such circumstances, wood shortages are expected over the next 5 to 10 years.

By 2005, the annual production from natural forests is expected to remain at about 300 000 m3. With assumed new planting of 200 000 ha of plantations per year, production of 6 to 8 million m3 is projected by 2005. Scattered privately planted trees are also expected to yield 1 to 1.5 million m3. Added together, the projected outputs would be able to meet industrial wood demand, which is expected to double to about 9.5 million m3 by 2005.

In addition to industrial timber utilization, households and industries also consume approximately 14 million m3 of fuelwood. Approximately 8.7 million m3 is derived from natural forests, with 5.7 million m3 taken from plantations and scattered trees. Some rural communities face a shortage of firewood because alternative energy sources are scarce and largely unavailable to them.

The imposition of the logging ban in 1997 was accompanied by development of a plan to regenerate 5 million ha of forestland. If successful, the program will increase wood production to meet domestic demand by 2010.

Viet Nam is allocating land for long-term use (up to 50 years) to households, individuals and organizations. To assist farmers residing in forest areas, the Government allocated up to 3 ha of land to interested families for development of economic forests.

The ability of Viet Nam to adequately meet future demands, particularly after 2005, depends, in no small part, on the successful implementation the logging ban and the 5 million ha reforestation program. Major adjustments to State enterprises and wood industries, and attracting local and international investors, are also important elements necessary for success.

ISSUES AND CONCERNS

The country case studies reveal a highly complex and variable mixture of symptomatic reasons for imposing logging bans and restrictions on harvesting in natural forests. Concern over continuing deforestation is the dominant issue. Action is primarily driven by the aim of halting further deforestation and degradation of remaining natural forests.

Other concerns are also evident, and are often co-mingled with vague or undefined aspects of “forest conservation” or “forest protection.” From the case studies and broader review of the Asia-Pacific region, the major issues regarding natural forests include:

Timber harvesting is frequently perceived to be a major contributor to loss of biodiversity, habitats (primarily for wildlife) and representative ecosystems. Where natural forests are logged selectively, only higher-valued species are usually taken, with the consequent loss of seed source or natural regeneration for these species relative to lower-valued residual species. Non-timber components of the ecosystem can also be damaged or destroyed during logging. These concerns reflect the view that non-timber values of retaining biodiversity, habitats and ecosystems outweigh, at the margin, the value of the timber harvested and that timber output should be reduced to “protect” or provide a higher level of such values.

Removal of all or part of the forest cover reduces water retention capability of watersheds, resulting in increased peak water runoff and reduced water flows during periods of low precipitation. Watersheds with natural forest cover are frequently the source of both domestic and industrial (including agricultural) water. Reduction of vegetation in such watersheds also contributes to soil erosion, and thus to declining water quality.

Vegetation loss can expose soils to both wind and water erosion. In many areas of the Asia-Pacific region, soil loss and declining productivity are major concerns for both forestry and agriculture. Further, the disturbance of soils frequently leads to serious sedimentation of streams, rivers and reservoirs. Severe flooding, as experienced in Thailand and China, in recent years, has led directly to immediate and comprehensive logging bans in natural forests.

Use of ground-based logging equipment, and poor roading and skidding of harvested timber, frequently damage soils and residual forest trees. Large volumes of slash and debris also hinder reforestation efforts, and commonly increase the risk of fire. Applying reduced impact logging practices remain the exception rather than the norm across the region.

Where contract enforcement is lax or ineffective, violations of harvesting guidelines is common, resulting in site damage and deterioration of stand quality. Incentives to comply with logging standards are often weak, while the potential financial benefits of operational short cuts and inappropriate techniques may be great. Over-cutting beyond authorized levels may also yield direct financial benefits to harvesters while contributing to further forest degradation. Illegal harvesting is a common concern, both prior to and following the imposition of logging bans.

Where logging is carried out under permit or license systems, the capacity of governments to effectively monitor and enforce regulations may be insufficient. Even where logging is directly the responsibility of a subsidiary government unit, the lure of greater revenues and/or lower costs may lead to abuses or conscious avoidance of contract or permit conditions. The potential for corruption or complacency in enforcement can also lead to abuses. The lack of measurable criteria for contract conditions (for example, reforestation) can contribute to disputes and uncertainties about standards of performance.

Land tenure arrangements and instruments for assigning use rights vary greatly throughout the Asia-Pacific region. Frequently, rights are allocated for harvesting State-owned and administered forests, but obligations for reforestation or forest regeneration remain with the State. In cases where reforestation by users is required, standards and performance may be vague and inadequately monitored, without effective performance bonds or other provisions to assure compliance. The lack of capacity and funding for State follow-up to regenerate cut-over areas or to reforest barren or degraded lands leads to criticisms of the initial decision to grant logging permits, even when the logging itself is in compliance with existing regulations and guidelines.

Inadequate support for management and reforestation, combined with poor enforcement of restrictions and use rights, frequently lead to poor resource conditions and degradation. Logging is again the most obvious contributor to forest disturbance, creating a need for strong management plans and operations, especially in cut-over forests.

The natural forests of Asia-Pacific are, in most cases, subject to heavy population pressures. One consequence of logging in these forests is the creation of access through logging roads. In addition, the stand density is reduced by virtue of the logging and land clearing is consequently made easier. Shifting cultivation, small landowner settlement, illegal logging and increases in the forest populations may follow. Without logging roads, these forests would remain more remote and inaccessible. Hence, banning logging activities is seen as one means of preventing or reducing continued encroachment.

Encroachment and opening of forests to settlement also encourage forest conversion. Where conservation or production forests are considered to be the socially optimal choice of land use, such conversions reduce the overall contribution of these lands towards social welfare. They also fragment the remaining natural forests, making the enforcement of forest policies and regulations more difficult, and increasing the potential for further land-use conflicts.

The natural forests of much of the Asia-Pacific region are home to significant numbers of people, including many indigenous groups. The social and cultural values of these peoples often conflict with those of the increasingly urban population. Traditional rights and land tenure of local communities and cultures provide for many subsistence and non-timber values that are often unrecognized by commercial forest management operations. While timber production often disrupts traditional local use and dependency, forest protection measures may prohibit access and use. Centralized government regulation and control, together with inadequate recognition of local dependency and traditional rights, can make it difficult to forge consensus on forest management, production or conservation. Banning of commercial timber harvesting, particularly by government or “outside” contractors, is often seen as a viable option for protecting local rights and cultures.

Asia-Pacific countries have sought to protect scenic, cultural and aesthetic resources that frequently depend on undisturbed forest structures and natural topographic features. Forest disturbances caused by logging operations threaten these values which are largely non-market in nature and thus seldom given due consideration relative to the direct financial revenues and profits from logging.

Increasingly, non-timber and ecological values of forests are given greater weight in forest policies. Protection of biodiversity, conservation of gene pools, the still unknown potential of medicinal plants and other social values of forest fauna and flora are often incompatible with the management of natural forests for commercial timber. Timber production also potentially conflicts with efforts to sustain or increase the yields of non-timber products and services important to local people.

NATURAL FORESTS AND POLICY CHOICES FOR IMPROVED PROTECTION AND USENatural forests are increasingly recognized for their roles in sequestering carbon and mitigating climate changes. Through photosynthesis, forest growth reduces atmospheric carbon dioxide concentrations and generates oxygen. Capture of atmospheric carbon and its storage in forest biomass have become regional and global concerns, increasingly covered under international conventions and agreements. Harvesting reduces the biomass (at least temporarily) and if deforestation results, these values are permanently lost.

The policy issues and concerns behind logging bans in the Asia-Pacific region reveal two very different types of policy shortcomings: (i) inappropriate forest land-use allocation, and (ii) inefficiencies in managing and utilizing forest resources.

Forest land use

Forestland use issues involve the allocation of land to forests, and the subsequent decisions on the various uses of those forests. Forestland use often directly conflicts with alternative land uses such as settlements, agriculture or mining. Alternatively, there are many “mixed” land uses involving protected areas, watersheds, recreation and scenic areas, or agroforestry. National policies must reconcile and provide guidance and institutional arrangements for deciding priorities among forest and non-forest uses as well as for the level and “mix” of multiple uses.

“Forest use” and “timber production” have frequently been assumed to be synonymous in the past. Lands which have (or have had) forest cover are most often simply classified as “forestland” in spite of potential alternative uses. This classification has been quite rigid, making changes difficult. The conversion of lands from forests to agricultural land use, for example, is often viewed as “encroachment” on forests.

Land designated for forestry has frequently focused on wood production (both industrial timber and fuelwood). The maximum output of wood and fiber has often been the primary goal of forest policies. Other uses, including environmental protection functions, non-wood forest products, water flow, and so on, has often been relegated to secondary importance.

This conventional pattern of allocating forest use primarily for timber is now considered inappropriate by most people. But while multiple-use forestry is more widely acknowledged and appreciated than in the past, in practice timber is still given priority under most management schemes.

Most Asia-Pacific countries have long-standing policies for designating some forestlands as protected areas, where timber harvesting is prohibited. Sometimes, such designations have been based on intensive studies and analyses of the relative priorities and trade-offs with other land uses and values. In other cases, the administrative designation of protected areas has occurred without comprehensive planning and assessment of priorities. Where the objectives for such designations are not clear and specific, withdrawal of forests from production may have unnecessarily constrained productive sustainable harvests of timber. It is possible that other options could have achieved the desired results, but such options have rarely been pursued in the region. The need for total restrictions on timber harvesting, of course, depends on the actual resource conditions and the specific objectives.

How much forest should be allocated to alternative and mutually exclusive uses is a major policy choice that is usually controversial. Recent history demonstrates that “too much” forest may be allocated to timber and “too little” for other purposes. Resolutions and consensus over forest use are extremely difficult to achieve when “either-or” choices are required between two or more desirable uses that are indeed mutually exclusive. Certain forms of forest conservation and protection, for example, may be technically incompatible with even the lightest intensity of timber harvesting. In other cases, appropriate protection and conservation may be practical and feasible under broader concepts of “sustainable forest management.”

Efficiency in forest resource use

Concerns about inefficiencies in forest management and timber harvesting also frequently arise. Much of the debate centers on inappropriate management schemes, unregulated harvesting, poor institutional arrangements and environmentally damaging logging technology, which often result in unintended loss of environmental values. These inefficiencies and abuses are a primary cause for calls to ban logging. In many cases, the negative consequences of poor logging practices detract attention from viable options for improved practices that could maintain multiple values of forests.

Environmental forest functions may be seriously impaired or destroyed during conventional timber harvesting. Wasteful harvesting and damage to residual stands also negatively impact future forest productivity, and add significantly to private and social costs.

Clearly, there are conflicting opinions regarding the ability to overcome inefficiencies in forest resource use. The technical and economic viability of sustainable multiple-use management and modified management strategies such as reduced impact logging (RIL) to reduce both economic and environmental costs have been discussed extensively. It is evident from experiences throughout the region that modifications to current management practices are required if timber harvesting is to be widely accepted.

THE EFFICACY OF REMOVING NATURAL FORESTS FROM TIMBER HARVESTING AS A CONSERVATION STRATEGY

Recent experiences in implementing logging bans and harvesting restrictions in Asia-Pacific have been mixed. Following the imposition of logging bans, significant areas of natural forests have been classified as protected areas, or the absence of harvesting is taken as equivalent to protection. While limited success of some natural forest conservation objectives is evident, lack of effective protection remains a problem.

The lack of specific conservation and protection goals contributes to an inability to measure performance and achievements, while simultaneously creating confusion and disagreement regarding the objectives. Adverse economic and social impacts have also occurred, further undermining the incentives for sustainable management, conservation and protection of non-timber values. Removal of natural forests from timber production has had significant impacts on the forest product sector, and sometimes disruptive effects on neighboring countries through legal and illegal trade, timber smuggling, and market disruptions.

Finally, a distinction between simply banning logging and the correlated need to formulate and implement strategies and programs for effective conservation and protection is essential. An uncritical assertion that halting logging is either necessary or sufficient to assure conservation has resulted in many natural forests being declared as protected while deforestation and degradation continue largely unaffected. Only where logging bans have been accompanied by transitional adjustment policies for alternative timber supplies, social and economic “safety nets” to minimize local burdens, and sustained and effective conservation management have bans proven effective.

Impacts on timber production

The remaining natural forests of the Asia-Pacific region that are still available for harvesting are experiencing heavy pressures for increased harvests. These pressures also spill over onto natural forests that are “presently unavailable” for harvesting. While the country case studies have illustrated that logging bans reduce harvests, it is also evident that continuation of pre-ban practices would have also led to falls in production as the natural resource declines in area and quality.

With few exceptions, harvest volumes from the remaining natural forests can be expected to decline in most countries in the region. Harvest bans will impact the timing and rate of harvest decline, but not the fact that prior levels of harvests were also unsustainable. Total gross annual growth of commercial species on presently available natural forests exceeds present harvests of industrial timber by about 24 million m3, compared to the production of 304 million m3.

Further deforestation and degradation at or near the present rate of about 3.3 million ha annually will reduce the capacity of Asia-Pacific to produce industrial timber from natural forests. With an average cutting cycle of about 38 years, present harvesting intensity is about 34 m3 per ha for undisturbed natural forests and 17 m3 per ha for disturbed forests. Based on the ratio for available undisturbed and disturbed forests6, deforestation could reduce regional harvest by about 1.8 million m3 per year.

The present ratio of available natural forests also provides a rough estimate of the impacts of logging bans, assuming that bans impact both undisturbed and disturbed forests by the same proportion. The banning of harvesting on 1 million ha of available natural forests would reduce potential harvesting by approximately 550 000 m3 annually.7 For example, China’s logging ban affecting 41.8 million ha with an estimated reduction in harvest of 19.9 million m3 by 2003 implies an average reduction of 476 000 m3 per 1 million ha.

For the six countries included in this study, the impacts on timber harvests from the natural forests are considerable. The expected impact for China is a reduction from 1997 levels (pre-ban) of some 32 million m3 from State-owned natural forests to only 12 million m3 when the ban is fully implemented by 2003. For the Philippines, the production was an estimated 5 million m3 prior to the 1991 general ban, before declining to about 0.5 million m3 most recently. Similarly, Thailand’s natural forest harvest was about 2 million m3 prior to the 1988 logging ban, then falling to only about 55 000 m3 (recorded harvest) in 1998. Sri Lanka saw the harvest from State-administered natural forests fall from 425 000 m3 in 1990 to nearly zero, creating an almost total dependence on alternative supplies. Viet Nam likewise experienced a sharp drop in natural forest timber production from about 1 million m3 annually between 1990 and 1995 to a presently authorized level of only 300 000 m3 after the 1997 general logging ban.

For these five countries, the aggregate reduction following comprehensive logging bans is approximately 29.5 million m3 per year.8 New Zealand is the only country among the case studies that did not suffer such a large decrease in the volume of timber harvested. It had anticipated a declining capacity for natural forest harvests over several decades, and had pursued a strategy for both government and private plantations to supply its industrial timber. The transfer of almost all State-owned natural forests to conservation status in 1987, therefore, had only a minor impact on commercial timber supply. Harvest of natural forests was about 2 million m3 in the early 1950s, falling to below 1 million m3 by 1970. Natural forest harvest (including West Coast forests) was below 90 000 m3 in 1999, compared to 17 million m3 from plantations.

Alternative timber supplies

The imposition of logging bans in natural forests involves significant assumptions about timber supply from current or future plantations. For example, China’s shift of focus is founded on the rapid expansion and maturing of fast-growing industrial plantations, complemented by other NFCP strategies. Viet Nam is relying on the successful implementation of its 5 million ha reforestation program. Serious consequences in both the Philippines and Thailand illustrate the problems when commercial plantations do not develop as planned. Thailand’s goal of some 800 000 ha of new commercial plantations has fallen short, reaching only 164 800 ha by 1999. The 773 000 ha plantations in the Philippines are now expected to yield only approximately 300 000 m3 annually in contrast to 1990 projections of 2.8 million m3.

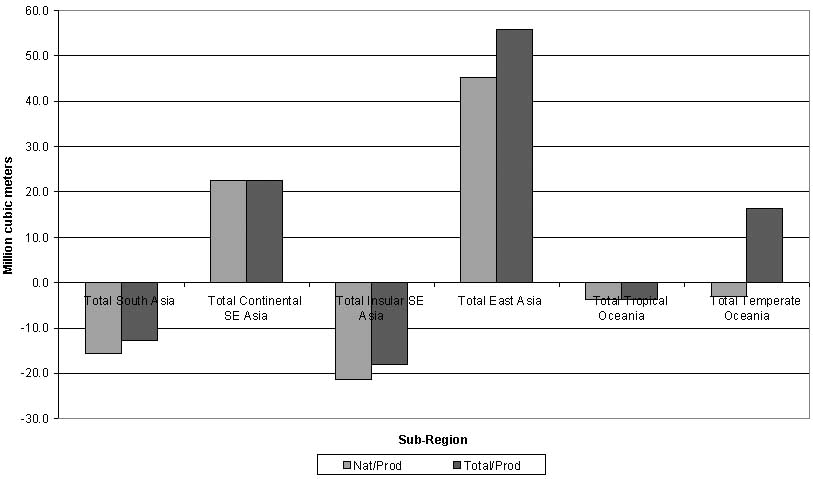

The Asia-Pacific region has reached a point where the production of industrial roundwood is very close to the net growth from available natural forests (FAO 1998). Current plantation yields still fall far short of the volumes required to offset logging bans, declining production and increasing demands. The regional relationship between estimated growth of commercial species in available natural forests and industrial roundwood production is shown as the first series (“Nat/Prod”) in Figure 6. The corresponding comparison of combined natural forest and plantation growth with industrial roundwood production is displayed as the second series (“Total/Prod”).

If it is assumed that both the total growth of commercial species from available natural forests and from industrial plantations are available for harvest, the overall situation for Asia-Pacific would improve. The overall balance between total growth from both natural forests and plantations and the 1996-level of industrial timber production improves to a positive net balance of 60 million m3. However, there are significant differences between individual subregions and countries (Figure 6).

All subregions show an improved balance when plantation growth is included, although the very small growth for Continental Southeast Asia and Tropical Oceania does not significantly change the situation for these subregions. South Asia, Insular Southeast Asia and Tropical Oceania continue to show a deficit between estimated total growth and industrial roundwood production. Only Temperate Oceania switches from a deficit to a positive balance when New Zealand’s plantation timber is taken into account. Malaysia and India continue to show significant deficits even when the contribution from their plantations are included.

Reduced log production due to the logging bans in the six case countries totals nearly 30 million m3 annually. Plantations, as an alternative supply, are estimated to provide 36.1 million m3 (Figure 6), but only if all net growth from available plantations can be efficiently harvested. Additional withdrawals of natural forests together with continuing deforestation and degradation can be expected to further reduce wood supplies. More productive plantations and more effective management of such plantations will be needed if the balance between growth and consumption is to be maintained on a region-wide basis under growing demands. However, continuing reluctance to support intensively managed, single-species commercial plantations in many countries, and emerging challenges to genetically altered trees will make such expansions in plantation forestry less likely.

International trade implications

Countries of the Asia-Pacific have long engaged in international trade - both importing and exporting - as resource stocks and markets for wood products dictate. While trade barriers and national consumption policies have frequently distorted true open trade in the past, and trade has been sometimes reserved as a national government monopoly, considerable volumes of wood are traded in the region and worldwide.

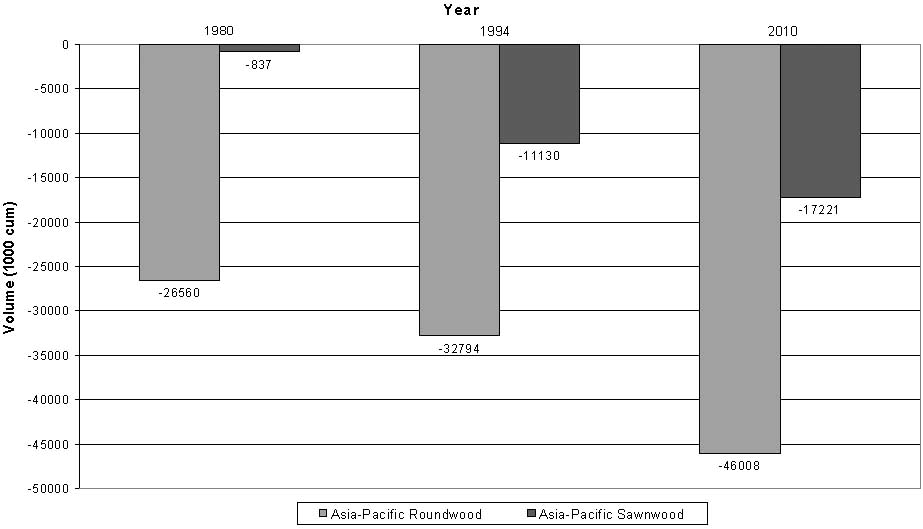

The Asia-Pacific region has consistently been a net importer of roundwood (industrial and fuelwood). Already in 1980, the region imported over 70.6 million m3 while exporting 44.1 million m3 (a net deficit of 26.6 million m3 derived from outside the region). This deficit grew to over 32.6 million m3 by 1994. FAO provisional projections for 2010, based on the “most likely” scenario of development and economic trends, forecast a net trade deficit of 46 million m3 (Figure 7).

The region also trades sawnwood, plywood and wood-based panels, joinery products, pulp, paper, paperboard and many specialized products. Sawnwood is, by far, the most significant processed solid wood product traded. As shown in Figure 7, the region has also been a net importer of sawnwood; the net trade deficit by volume is smaller than for roundwood but is increasing. In 1980, the region had net imports of 837 000 m3 of sawnwood. The deficit grew to over 11.1 million m3 by 1994. In addition to Japan’s role as a large importer, both China and Thailand became significant importers of sawnwood. FAO’s provisional projections indicate a potential net trade deficit of 17.2 million m3 of sawnwood by 2010.

While many countries maintain policies of remaining self-sufficient in timber or aspiring to self-sufficiency, the Asia-Pacific case studies indicate the difficulty in doing so in the face of deforestation, forest degradation and lack of adequate plantation resources. In addition, logging bans which are abruptly imposed over a short period without adequate consideration of realistic timber supply alternatives (including trade) and likely growth of demand, create tremendous pressure for increasing imports.

Figure 7. Projected Asia-Pacific net trade in roundwood and sawnwood, 1980, 1994 and 2010

As noted, Thailand, the Philippines, Viet Nam, and Sri Lanka have all had minimal success in developing greater production from plantations to compensate for the loss of production from natural forests resulting from logging bans. While Sri Lanka has significant capacity for timber production from homegardens and other non-forest resources, Thailand, the Philippines and Viet Nam do not have such a supply base. All four nations have become net importers of industrial wood, with imports expected to increase even further. China has identified the need for greater imports, at least for a transitional period. Only New Zealand has sufficient plantation resources to meet domestic demand and for export.

International trade also opens the possibility of “exporting” or “externalizing” the problems associated with timber harvesting to other countries. For example, there have been allegations that Thailand’s logging ban has resulted in both illegal logging and greater imports along the borders with Laos, Cambodia and Myanmar. Protection of natural forests in China has led to greater imports from Myanmar and the Russian Federation, potentially contributing to unsustainable harvesting in northern Myanmar and parts of the Russian Far East and East Siberia. Viet Nam also imports timber from Cambodia and Laos, allegedly in part from illegal harvests. While difficult to document, these negative effects raise important issues regarding the environmental and protection policies of exporting countries.

Recent analyses by Sedjo and Botkin (1997) and Sohngen et al. (1999) provide some insights into the relationship among natural forests, plantations and the implications of international trade. Although dealing with natural forests in the aggregate, their analyses suggest that declining natural forest harvesting (due to deforestation, degradation or logging bans) on the part of one country alarms both domestic and international markets through costs and pricing, stimulating three potential responses: 1) extended harvesting of natural forests into marginal and inaccessible areas (legally and illegally), 2) more intensive management of natural forests for improved sustained yields, and 3) expanded, intensive timber plantations. As seen in the case studies, the primary assumption is that countries will be able to expand plantations to offset declines in natural forest harvests. In practice, however, plantation development has been generally been disappointing, with shortfalls largely met by increased imports.

Comparative advantage

Reduction in output from natural forests either through deforestation, degradation, logging bans, more stringent management requirements, or enlargement of protected areas also leads to price adjustments and responses by both suppliers and consumers to the extent that market-based prices prevail and influence timber production and output decisions. The impacts are not, however, limited only to the country initiating harvest bans or restrictions.

A country that has enjoyed a comparative advantage in harvesting natural forests may not automatically enjoy such an advantage in alternatives such as domestic plantations. This is particularly true where the domestic economy is undergoing both macro- and microeconomic reforms, giving more influence to market-based incentives and prices. Where prior harvesting and marketing decisions have reflected strong government control or regulation, distortions in both production and prices have frequently developed. When economic reforms unleash free market forces, such distortions become apparent and market-based incentives quickly orient decision-making toward economic efficiency rather than simply resource availability. The ability to address socio-economic impacts through plantations may also shift.

A large number of obstacles constrain economically viable creation of commercial plantations in the Asia-Pacific region, particularly in relatively small-scale operations. The comparative advantage may shift to other areas within a country, or even to other countries. For China, the shift to plantations will have substantial impacts intraregionally. Changing timber supplies pose a serious threat to established forest-based enterprises in the traditional State-owned natural forest regions of the Northeast, Inner Mongolia and Southwest China. Plantations will result in new production capacity in the southern coastal provinces that have more favorable conditions for high-yielding, fast-growing species and better access to markets.

New Zealand, as a prime source of intensively produced plantation timber, may well exploit export markets in Asia-Pacific at the expense of potential plantation development within individual developing countries. An emphasis on small-scale, community-based or individual household plantations may ultimately prove difficult, if not uneconomic, in light of international trade potential from outside a country’s borders. Industrial-scale plantations may meet increasing challenges from local interests, environmental organizations and others. Lack of investment capital, available productive land for planting, equipment, marketing structures, transport and technical knowledge can all contribute to difficulties in developing domestic plantations as alternative sources of timber.

Comparative advantage is an elusive concept, largely based on market economics, prices and costs, and relative resource endowments. The specific conditions of species composition, stand volumes and quality, efficiencies in timber growing and harvesting, transport, scale of operations, and a number of other such considerations, determine costs and returns, and consequently where and how plantations will develop most efficiently throughout the region. In the past, non-economic factors, including biophysical forest and species characteristics and political considerations, have influenced many decisions regarding plantations. Free market forces, however, increasingly influence (if not determine) such decisions.

New Zealand illustrates the potential for a major reallocation of harvesting away from natural forests for timber production towards conservation objectives (in the public sector), and a transition to greater harvests from the mature plantations (increasingly private). Sri Lanka also demonstrates the possibility of restricting harvests in natural forests by shifting output to economically viable alternative timber supplies derived from homegardens, plantations and imports. The availability of suitable land and the incentives for non-State plantations have been instrumental in offsetting the reduction in natural forest timber output.

Thailand and the Philippines continue to struggle to effectively implement their long existing bans on harvesting in natural forests. In spite of the bans, the achievement of effective protection and conservation remains elusive. The lack of effective institutions and policies to deal with reduced natural forest timber supplies (and enforcement of harvesting restrictions), together with substantial unanticipated adverse social and economic impacts, have made the realization of natural forest conservation difficult. At the same time, the institutional, policy and investment infrastructures in both countries have adversely impacted the potential for commercial plantation development as an alternative timber supply.

As a consequence, both Thailand and the Philippines have become major net importers of timber since imposing harvesting restrictions. The shift towards imports indicates, at least indirectly, that the comparative advantage for increasing timber supplies may reside with countries that have viable, maturing intensively managed plantations or those still allowing the export of timber from their natural forests (for example, the Russian Far East). Such developments are leading to greater concerns over the harvesting practices and the ultimate sustainability of harvesting in supplier countries. Pressures on neighboring countries create incentives for increased harvesting and exports (including illegal harvesting and smuggling) in spite of policies in those countries to also restrict harvesting to sustainable levels or to set aside their forests for protection and conservation.

China is now in the early phases of introducing new logging bans intended to conserve and protect much of the remaining natural forests. In the past, China has relied heavily on natural forests for timber production, resulting in widespread over-harvesting and environmental degradation. A long-term strategy has been adopted for increasing plantations for future harvesting (timber base) while allocating much of the remaining natural forests for environmental protection and the restoration of degraded forests. Closing much of the natural forests in the headwaters of major river systems as an emergency measure was introduced in 1998 under the country’s NFCP. China has also developed substantial plantation resources for both protection and production. It remains unclear, however, how much additional plantation development will prove to be technically and economically viable under the ongoing economic reforms.

Viet Nam is also at an early stage of further restricting timber harvests in its natural forests. The success of this effort will be largely determined by the simultaneous implementation of the country’s 5 million ha reforestation program. Funding and transitional adjustments will remain critical issues over the next decade or longer until the presently inadequate plantation resources are sufficient to meet both industrial and fuelwood needs. To date, many technical, social and economic issues remain unresolved, and thus the comparative advantage of plantation establishment within Viet Nam relative to other opportunities in the Asia-Pacific region is still uncertain.

New Zealand represents the clearest example of comparative advantage for commercial plantations as a substitute timber resource. As natural forest supplies declined, plantations were in place to supply both domestic and export markets. Favorable conditions of land availability, technical development of fast-growing radiata pine, market development, and a strong private industry willing to invest in plantations have given New Zealand an edge over other countries. This, of course, represents conditions and economics of the past decade, and may well change in the future if and when other countries formulate viable plantation policies and the supporting technical and economic frameworks.

Achieving conservation

Asia-Pacific has been a leader in the designation of legally protected areas, having so classified a total of some 89.5 million ha, effectively removing these natural forests from harvesting. The largest aggregate protected natural forest is in Insular Southeast Asia, with some 43.3 million ha, including almost 40 million ha in Indonesia and 2.8 million ha in Malaysia. East Asia accounts for 15.4 million ha of protected area, with over 13 million ha in China. Temperate Oceania and South Asia each has over 10 million ha in protected areas. Continental Southeast Asia accounts for about 6.8 million ha (mainly in Cambodia and Thailand). These areas include, of course, some natural forests that would otherwise be available for harvest, as well as areas that would be unavailable due to physical and economic limitations.

Despite the legal designation of protected natural forests, there is substantial concern about the adequacy of the on-the-ground protection of these areas. As well, controversy about the need to set aside additional areas for protection of representative biodiversity, critical watersheds and habitats for rare and endangered fauna and flora continues. Unfortunately, qualitative assessments of protection and conservation are largely lacking. This is in part due to the non-specific policy objectives not translatable to measurable actions beyond area statistics, and the lack of adequate indicators of conservation, protection, biodiversity, ecosystem health, and so on. Monitoring and evaluation are thus weakened, and relatively little factual information is available to assess whether the various forms of legal designations are effective.

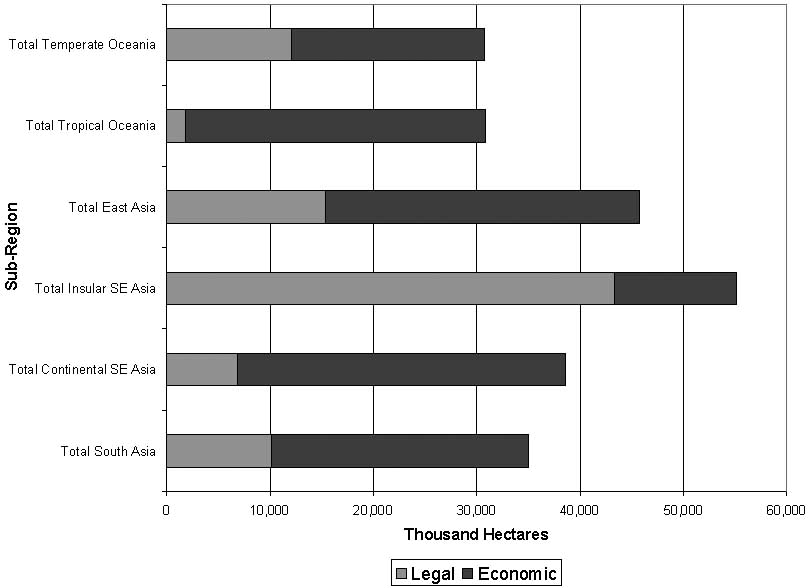

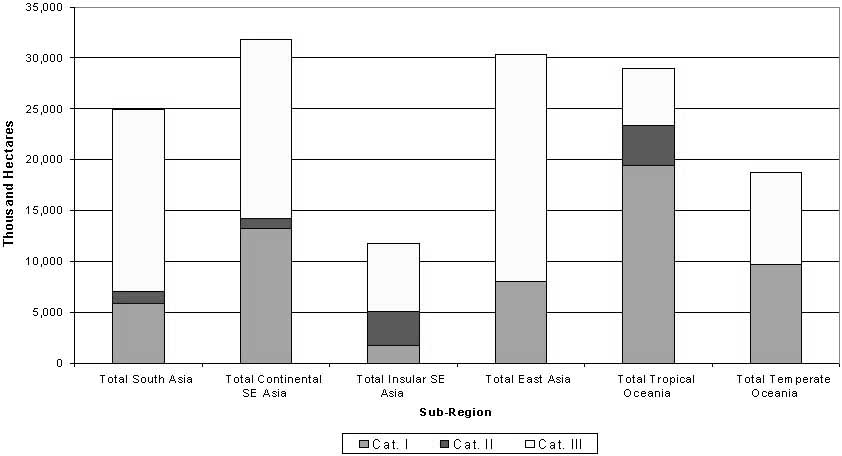

Over 236 million ha of the natural forests of Asia-Pacific are presently unavailable for harvesting due to physical and economic factors. Figure 8 shows the breakdown, led by Insular Southeast Asia (55.1 million ha), East Asia (45.7 million ha), Continental Southeast Asia (38.6 million ha) and South Asia (35.0 million ha). Some 89.5 million ha of this area are legally protected.

Over 146.5 million ha are unavailable without being legally “protected.” In many instances, these “unavailable” natural forests are at the most risk for continuing deforestation and degradation. Even available natural forests (not yet closed to logging) face pressures from over-cutting and encroachment, leading to further degradation. Figure 9 classifies three categories of such constraints as follows:

Category I presently restricts harvesting on some 58 million ha in the region, primarily in the Tropical Oceania subregion (Papua New Guinea - 17.6 million ha) and Continental Southeast Asia (Laos 4.5 - million ha; Myanmar - 5.7 million ha; Thailand - 2 million ha). Other countries with substantial physical constraints on their natural forests include India (4.8 million ha), China (5 million ha) and Australia (9.7 million ha).

Remoteness and lack of access are less of a constraint in Asia-Pacific due to generally heavy population pressures in the rural areas and developed infrastructure. Category II accounts for 9.5 million ha of natural forests being unavailable for harvesting at present, with Indonesia (3.4 million ha), Papua New Guinea (4 million ha), Laos (1 million ha) and Nepal (0.9 million ha) accounting for almost all of this area.

Category III limits harvesting on a total of 79.1 million ha. East Asia, led by China (16.3 million ha) and Japan (4.5 million ha) accounts for about 23 million ha in this category, with South Asia (India - 15 million ha) accounting for an additional 17.9 million ha. In Continental Southeast Asia, Thailand has an estimated 6.8 million ha of such natural forests followed by Laos (4.4 million ha) and Viet Nam (3.9 million ha). In Temperate Oceania, Australia has about 8.5 million ha of such areas.

Figure 9. Asia-Pacific natural forest unavailable for harvest due to technical/economic constraints

Despite being “unavailable,” much of the natural forests are continually exposed to pressures leading to deforestation or further degradation. A simple change in legal status from “available for harvesting” to “unavailable” or “legally protected” status does not in itself assure either protection or conservation. Much of the 89.5 million ha of legally protected natural forest are at risk of further deforestation or degradation due to ineffective policies for protection, inadequate resources for management planning and implementation, presence of rural people dependent on forests, and other constraints.

The country case studies indicate that substantial areas of natural forests have been brought under legal protection status or de-facto protection. Some of these are included in the totals reported above for legally unavailable forestland. The recent implementation of the NFCP in China will initially encompass some 41.8 million ha of natural forests most critically in need of protection and rehabilitation. About 5 million ha of natural forests in both New Zealand and the Philippines were reclassified as protected - under separate legal administration as conservation forests in New Zealand but as de-facto conservation in the Philippines. About 8.1 million ha in Thailand were closed to logging and are either declared protected areas or are awaiting formal designation. Sri Lanka increased legally protected natural forests by about 1 million ha under the logging ban. Finally, Viet Nam has added some 4.3 million ha to protected areas as a result of the total logging ban. Over 64 million ha in the six countries have, as a result of logging bans, become, theoretically at least, subject to protection.

The extent to which these lands will be actually protected in the long run is yet unclear. New Zealand and Sri Lanka have transferred administration of the protected natural forests to separate State institutions, thus clearly separating protection and production functions. In the other countries, such separation of functions is not fully defined in their organizational structures or practical operational management, potentially creating confusion or conflicts within traditional forestry-natural resources units. The “timber culture” of traditional foresters frequently casts doubts about their commitment to protection and conservation.