![]()

![]()

![]()

Presented by

Germain

Denis

Executive Director

International Grains

Council

We appreciate the FAO's invitation to the Secretariat of the International Grains Council to join other international commodity bodies in sharing their assessment of factors affecting world market conditions for a number of agricultural commodities. This IGC contribution is focused on wheat and coarse grains.

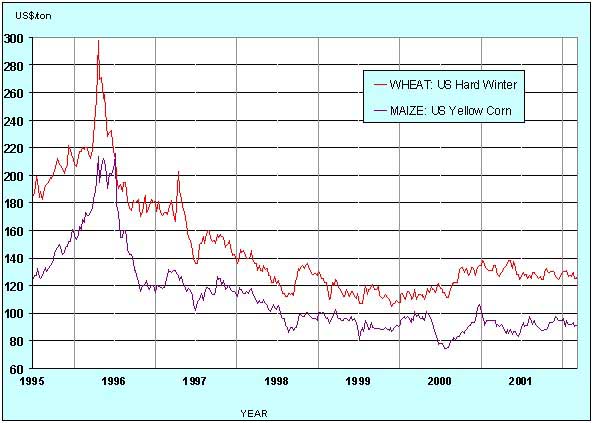

In the mid-1990s, the world grain market experienced a relatively short period of tight supplies and high export prices. Production rebounded rapidly, especially in the main exporting countries, and stocks were rebuilt. By mid-1998, prices of wheat and of maize had fallen to nearly their lowest since the 1970s. Latterly, markets have stayed relatively depressed, with supplies being adequate to meet the continued growth in commercial needs, and prices showing considerable stability (see Chart).

Since world wheat and coarse grains production reached a record in 1996, it has remained a little lower. Output in the main exporters was sustained at a high level, as yield increases offset area reductions, but their crops fell in 2001 after bad weather in several key producing areas. In China, there was also a significant fall in output driven by new policies to deter production of lower-quality grain. Production in the CIS and Eastern Europe was variable but there was major improvement in 2001 as better marketing conditions encouraged farmers to apply more agricultural inputs. In many developing countries, wheat production was relatively stable, but there was an overall increase in their output of coarse grains.

Overall growth of world grain consumption has been slowing down in the early 1990s. However, feed use of grains continues to expand at a moderate rate in major exporting countries reflecting growing meat production, especially in the United States. The steep decline in use in the CIS and Eastern Europe appears to have bottomed-out in 2001/02 but consumption in China has levelled-off. Food and feed use grain continues to increase in many developing countries in Asia and Latin America.

World grain trade has increased by about 10% since the mid-1990s to nearly record levels, with most of the growth in imports attributable to developing countries. Some former major wheat importers, notably China and Pakistan, have considerably reduced their purchases since the mid-1990's, while imports by Iran, Brazil, North Africa other than Egypt, and many least developed countries are higher. Coarse grains imports by Mexico, North Africa and Near East Asia have grown, principally to supply their expanding livestock industries, but the increase of imports by Pacific Asia has temporarily come to a halt.

In terms of exports, the share of the major exporting countries in world grains trade has fallen in the last two seasons, because of much larger exports by countries in the Black Sea region, South Asia (for wheat) and Brazil (for maize). Sales of maize by China have been variable, but very large in some years.

World grain stocks rose steeply in the latter 1990s, but have recently been falling, mainly because of a considerable drop in China's carryovers. Stocks in the five major exporting countries remained large until the current season, when they declined after their poor harvests. Following a succession of large crops, stocks in India have reached record levels.

These developments have kept world grain prices relatively low, fluctuating within a narrow band. At those levels, prices do not provide satisfactory returns for many grain producers, who have turned to their governments for substantial financial support to supplement market returns.

Assessment

The food and animal feed needs of many middle and lower-income developing countries are now the main dynamic factor in international grain trade. Developing countries' imports of wheat and coarse grains have now reached 150 million tonnes, close to three-quarters of the world total. During the temporary high world grain price situation, which prevailed in the mid-1990's, world production responded quickly to market signals.

Rising trends in grain yields have slowed down but have not faltered, even in countries where they are already high, as new varieties come into use and more farmers adopt improved agricultural practices. Areas planted with grains in many major producing countries have declined, although some areas could no doubt be brought back into use under adequate market incentives.

In sum, if the overall growth in world grains consumption and production appears to have slowed down in recent years, the process of change in the global grain economy has accelerated. Trade in grains and products is flowing in new directions and in more processed forms in response to more open markets and to changing consumer requirements, where quality factors are becoming a key factor in the market place.

EXPORT PRICES (fob Gulf) OF US WHEAT AND MAIZE - July 1995 - March 2002

![]()

![]()

![]()