![]()

![]()

![]()

Colin O’Loughlin1

There is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success, than to take the lead in the introduction of a new order of things because the innovator has for enemies all those who have done well under the old conditions, and has lukewarm defenders in those who may do well under the new. Machiavelli (fifteenth century)

New Zealand’s forests have played an important role in national development and economic growth since the arrival of the first Europeans in the late eighteenth century.At that time, indigenous forests occupied approximately 15 million hectares or 55 percent of the land area. From the 1840s, European colonization and settlement was accompanied by large-scale deforestation, mainly to provide land for cultivation and grazing but also to provide wood for housing, fuel, ship building and other constructions. Today indigenous forests occupy about 6.6 million hectares (24.8 percent of the total land area) and introduced planted forests, dominated by Pinus radiata, cover 1.83 million hectares or 7 percent of the total area. The indigenous forests are mainly protected for conservation, recreation and amenity purposes. The introduced plantation forests provide more than 99 percent of New Zealand’s wood production which contributes to about 4 percent of GDP (New Zealand Institute of Forestry 2005). Wood production from indigenous forests has declined steadily from the 1950s to the present day and currently amounts to a total of about 20 000 m3 per year.

The involvement of the state in forestry began in earnest in 1919 when a new State Forest Service was established and, two years later, operated under the auspices of the Forests Act (1921–1922). This fledgling government department, which later became the New Zealand Forest Service (NZFS), was largely responsible for the large-scale development of an exotic plantation resource, a progressive timber sales policy, the establishment of a forest research facility and a forestry school and the development of a raft of policies covering, inter alia, protection and good management of a large part of the country’s total forest estate.

Major planting booms from 1926 to 1935 and from 1960 to 1985 created an exotic plantation resource of over one million hectares, approximately 600 000 hectares of which was under the stewardship of the NZFS. By the 1960s, this department had grown into a large multifunction organization with a complex structure and numerous responsibilities, not only for the exotic plantations and their management, but also for the management and protection of most of the indigenous forests, animal pest control, fire protection over a large area of rural lands, timber processing at two of New Zealand’s largest sawmills as well as forest and forest product research and development and timber sales, both domestic and overseas.

In the 1970s and early 1980s, a growing public debate about the future management and conservation of indigenous forests led to a view, particularly from the environmental NGOs, that the NZFS was not the most suitably structured organization for efficiently delivering good forest management outcomes. At the same time there was growing concern about the ability of the department’s accounting and financial management systems to provide the level of accountability required by the government. Furthermore, some critics suggested that some of the functions of the department conflicted with one another. In particular, it was suggested that the forest conservation and protection roles of the department were not compatible with the timber production and commercial roles that increasingly demanded more attention as the exotic plantation estate expanded and timber production increased. It was these concerns that finally contributed to massive restructuring of the New Zealand State Forestry Sector in the mid-1980s.

The policies and strategies that had guided the NZFS since its establishment in 1919 were founded on the principles of multiple-use forestry which addressed the close integration of environmental, social, amenity, production and other commercial activities. The guiding philosophy of the department had much in common with the “forest ecosystem management” approaches adopted by the United States Forest Service in the 1990s and the polyfunctioneller Waldwirtschaft approach adopted by the German Bundesforstverwaltung to manage state forests. Ironically, adherence to the multiple-use management approach finally brought about the department’s demise.

In the mid-1980s, the new Labour2 Government vigorously set about reforming the economy. The major drivers behind the government reforms were the need to reduce the country’s accumulated debt, prevent further accumulation of debt and increase efficiency in the production of goods and services (Douglas 1993). To achieve these ends, government departments were restructured and many were disestablished. Many government assets were sold to the private sector, including forestry assets. Numerous regulations in the non-trading sectors and price, wage and income controls were removed. A relatively flat tax structure was introduced and a goods and services tax (GST) of 12.5 percent was imposed. Additionally, government subsidies, which had helped to prop up inefficient industries for decades, were also removed. New Zealand was transformed from one of the world’s most tightly regulated and controlled economies into one of the most liberal, market-based economies at that time. The forestry sector, both state and private, was heavily affected by the reforms. From the late 1980s to the early 1990s, these government-implemented changes gained international attention and were heralded by some observers as a groundbreaking model for restructuring whole country economies.

Restructuring and other changes that took place within the forestry sector after 1986 more or less signalled the end of the multiple-use approach to forestry and the introduction of a sharp separation of production and commercial forestry from environmental and conservation forestry. Within the forestry sector this was expressed by, not only a re-invention of agencies, but also re-invention of the philosophical underpinnings of land management. Thousands of people were affected by the changes.

This report examines the reasons for the restructuring, the processes involved, the goals, concomitant new legislation, the physical nature of the pre- and postrestructuring forest agencies, transformation success in terms of achieving desired outcomes and the changes in attitudes, capacities, capabilities and management approaches which occurred in the forestry agencies in the era after restructuring.

From meagre beginnings in the 1920s, the NZFS had grown and diversified into a large government department employing more than 7 000 people nationwide by the mid-1980s. The department controlled approximately 3.5 million hectares of state forests of which 600 000 hectares comprised intensively managed plantation forests, mainly Pinus radiata. As indicated earlier, the department’s planning strategies and operations were guided by a multiple-use approach to forestry which necessitated the development of a complex departmental structure and employment of highly diverse staff with a wide range of skills and disciplines.

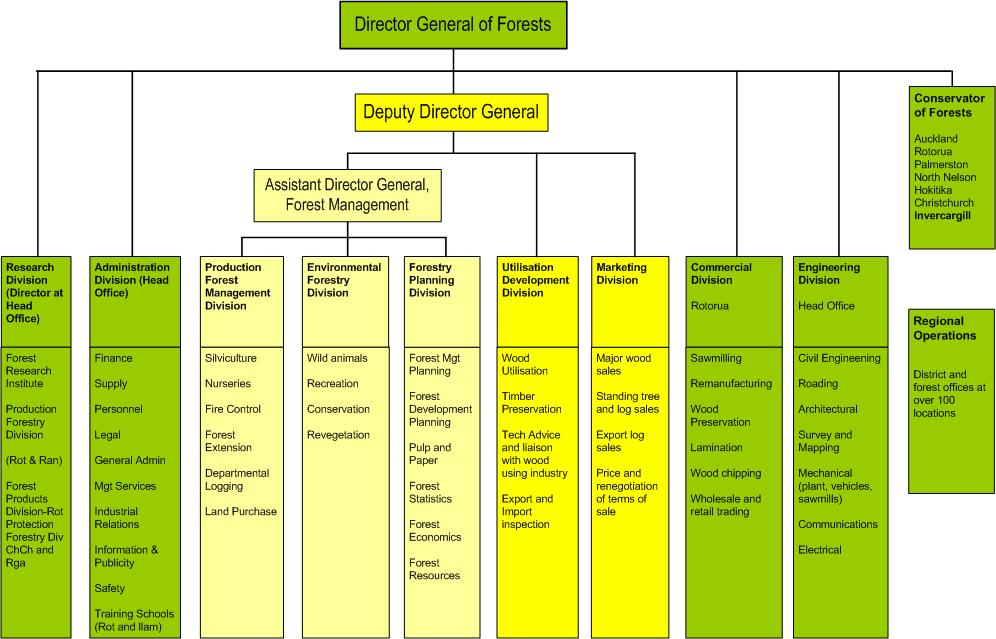

Physical structure and legislative functions: The complexity of the NZFS structure in the mid1980s is outlined in Figure 1.

The structure of the department reflected the multiple functions it was required to carry out. Essentially, the department comprised eight Wellington-based divisions, a Commercial Division based in Rotorua, seven conservancies, each under the control of a Conservator of Forests and a Forest Research Institute (FRI) based in Rotorua and Christchurch/Rangiora. Although the structure appears to be very cumbersome, from an operational viewpoint, the department apparently functioned reasonably well with the notable exception of the financial management and reporting areas (State Services Commission 1982). The bulk of the employees was located in the various conservancies — either in the main conservancy offices in Auckland, Rotorua, Palmerston North, Nelson, Hokitika, Christchurch and Invercargill — or in smaller district offices and in the various state forests. Another large component of the department was the FRI, which employed about 500 people. In terms of staff complement, the NZFS was one of three major government departments in the mid-1980s (the Department of Energy and the Ministry of Works being the other two).

The legislative functions of the department were defined by the Forest Act, 1949. This act empowered the Minister of Forests and by delegation, the NZFS, to:

In addition, the Forests Amendment Act, 1976 required state forest land to be managed so as to “ensure the balanced use of such land, having regard to the production of timber or other forest produce, the protection of the land and vegetation, water and soil management, the protection of indigenous flora and fauna and recreational, educational, historical, cultural, scenic, aesthetic, amenity and scientific purposes”. The 1976 statute provided the legislative basis for a multiple-use approach towards the management of state forest lands.

The NZFS was also responsible for the administration of three other major acts (State Services Commission 1982) — the Wild Animal Control Act (1977), the Forestry Encouragement Act (1962) and the Forest and Rural Fires Act (1977).

Objectives and management functions of the NZFS: The broad objectives of the NZFS were outlined by the NZFS Review Committee (State Services Commission 1982). These were to:

Figure 1. The structure of the NZFS

To achieve these objectives NZFS management functions were to:

The NZFS will probably be best remembered for five of its many achievements:

|

1) |

Expanding the plantation forest estate and developing efficient cutting edge approaches for managing plantations. The success of the highly profitable plantation forest industry, which was internationally recognized by the global forestry profession, was largely the result of the high level of multiple skills within the NZFS, especially in forest planning, forest management and forest research, and the high level of cooperation between researchers, planners and practical forest managers which enabled efficient uptake of innovative approaches in plantation establishment and management. These capabilities facilitated the development of a large estate of fast growing, genetically improved radiata pine plantations that were efficiently and intensively managed to produce high volumes of softwood. |

|

2) |

Research and development. By the 1980s the FRI had established itself as a centre of excellence for its research and development work in most aspects of establishing, growing, managing and harvesting plantation forests; genetically improving radiata pine; wood processing and developing innovative wood products; pulp and paper processing and new product development; environmental and protection research; fire research and surveying; and mapping the nation’s forest resources. |

|

3) |

Development of novel and highly effective forest protection strategies, plans and operations to ensure that the nation’s indigenous and plantation forests were protected from pests, diseases and fire. The fire protection system developed by the NZFS for its plantation forests was a well-coordinated system supported by research and development and using modern approaches that provided excellent protection against fire. There was considerable concern among foresters and others concerned with rural fire control, that the disestablishment of the NZFS would be accompanied by a less coordinated and less efficient fire protection system for protecting the forest estate. After an extensive review, in 1989, the government decided to place national rural fire protection and control in the hands of the New Zealand Fire Service (Cooper 1990). |

|

4) |

The training programmes that the NZFS put in place. These ensured that the forestry sector was staffed by well-trained professional foresters, forestry scientists, economists, engineers and other technically trained people. |

|

5) |

The leadership and vision that the NZFS provided to the forestry sector. As the largest player in the sector, the NZFS wielded great influence on the policies and strategies that determined the overall direction that the sector’s development took. Furthermore, the knowledge, information and capabilities that resided in the department were sought after by other forest and wood-processing entities, not only in New Zealand but also overseas. The leadership and vision provided by the NZFS that helped to weld the forestry sector together in a more or less coordinated fashion, was not really replaced with a new dominant leadership and vision after the disestablishment of the department. |

Through the 1970s and early 1980s, there was growing dissatisfaction with the organization and performance of the state forestry sector. Concerns came from several quarters. The growing environmental movement in New Zealand, championed by several environmental NGOs, began to agitate for changes in the way the NZFS operated and mounted strong challenges against NZFS philosophies and practices (Roche 1990; Kirkland 1988). Their particular concerns focused on the management of the indigenous forest estate and its protection. There was a growing perception by some conservationists that social and environmental aspects were accorded only subordinate status in agencies with commercial functions, such as the NZFS. Voices in the general public and the media, sympathetic to the concerns of the environmental NGOs, were also critical of the way in which the NZFS managed state indigenous forests. As far back as 1976, the so called “Maruia Declaration”, supported by 341 000 signatories, called for the splitting-up of the Forest Service and the establishment of a Nature Conservancy to protect publicly owned indigenous forests.

At the same time, there was a growing emphasis on an increasingly cost-competitive, market-oriented approach to commercial forestry by the government (Roche 1990; Clarke 1997; Kirkland 1988; Birchfield and Grant 1993). In 1978 the Auditor-General was unable to reconcile the value of assets managed by the NZFS to that shown in the department’s accounts (Roche 1990). The Auditor-General was also critical of the department’s accounting system. The government responded by establishing a Parliamentary Select Committee chaired by Ian McClean to investigate the department’s accounts. In its report the committee, claimed that the SIGMA cash accounting system used by the NZFS, although satisfactory for managerial purposes, was not suitable for commercial accounting purposes. The report also emphasized that the valuation of forest resources was “woefully inadequate” and that the ability of the NZFS to manage forest resources efficiently and engage in commercial activities was seriously constrained by the government department vote allocation system and lack of access to short-term funding.

Both the McClean report and a Forest Industry Study, completed by the Development Finance Corporation for the NZFS in 1980, stressed the disadvantages of the NZFS continuing to undertake a raft of trading (commercial) and social (non-commercial) functions. In response, the New Zealand Institute of Foresters was critical of the McClean report and strongly defended the multiple-use approach to managing the nation’s state forest resources (Roche 1990). The NZFS also provided a defensive response which highlighted the lack of justification for separating trading and nontrading functions within the NZFS.

Yet another review of the functions and objectives of the NZFS was conducted in 1982 by a committee comprising the State Services Commission, the NZFS, the Treasury and private sector representatives. The committee recommended that both the commercial and non-commercial roles of the department could and should be performed by the same organization, but also recognized that this could only be achieved effectively if financial and other management information systems were improved and the department was given more flexibility to manage its functions more efficiently. The committee also proposed a new senior management structure for the NZFS (State Services Commission 1982).

The saga of reform proposals for the State Forestry Sector continued when, in 1982, the government considered the possibility of merging the NZFS and the Department of Lands and Survey. For a variety of reasons this proposal lost support and was finally overtaken by other events when the Labour Government swept into power in July 1984.

The restructuring of the NZFS in 1987 represented only a part of a much wider set of reforms that affected a large portion of the wider public service, including at least 18 departments and other agencies in the late 1980s. However, the restructuring of the NZFS was one of the largest and most significant changes within the public sector at that time.

In 1984, the Treasury briefing document prepared for the incoming Labour Government laid out serious criticisms of the existing administrative regimes within government departments. Criticisms included:

In 1984, New Zealand provided almost ideal political, economic and intellectual conditions for a major restructuring and reform experiment (Kelsey 1997). At that time the economy was intrinsically vulnerable and suffered from massive debt, inflation, stagnation and a rising unemployment rate. The process of adjustment which was about to begin, was made easier by what Kelsey referred to as “the shallowness of the New Zealand political system — a classic single tier Westminster-style Parliament elected by a first-past-the-post system and an entrenched two-party monopoly”. Kelsey pointed out that new Cabinet intent for reform was virtually guaranteed, unimpeded power to rule. Furthermore, there was no formal constitution or supreme Bill of Rights by which the courts could constrain the Executive’s power. Over the decade following 1984, successive governments set about redesigning the economic and social structure of New Zealand. It was the state sector that bore the brunt of the reform process after 1984, but the private sector was also forced to make wide-ranging changes.

The influence that the Treasury exerted over the nature and course of the reforms that were to change the State Forestry Sector cannot be overstated. In addition to the initial briefing paper prepared for the incoming Labour Government, the Treasury also produced other briefing papers for the government including “Economic management, land use issues” (Treasury 1984) which criticized the forestry management policies of the recent past and outlined a market-oriented approach and the reforms required to put such an approach in place. The Treasury was also critical of the plantation planting targets developed by the NZFS, grants and subsidies for planting and agroforestry schemes and the nature of the tax arrangements for forestry schemes. The removal of grants was deemed necessary to place forestry on the same basis as other primary industries. The Treasury supported a “users pay” policy for the FRI that would force private forestry investors to pay for research and development services thus reducing taxpayer subsidies. The Treasury was also opposed to the concessionary wood sale policies used by the NZFS and promoted the need to sell wood at world market prices. To facilitate the change to a more market-oriented forestry sector and overcome the conflicts between commercial and non-commercial objectives within the NZFS, the Treasury proposed that the commercial activities of the NZFS should be transferred to a separate state-owned enterprise with commercial objectives.

The new Labour Government immediately embraced a neoclassical, market-oriented approach in line with the Treasury’s philosophies. The basic tenet was that efficiency in the economy would be maximized if markets were allowed to operate with a minimum of government interference and distortion (Brown 1997). The government soon introduced economic policy changes, the most important of which were the removal of subsidies to agriculture, forestry and industry generally, removal of a wide range of regulations in the non-trade sectors and removal of all price, wage and income controls and foreign exchange controls. The government also introduced a new tax regime that was unfavourable to forestry and resulted in a dramatic decline in new planting after 1985. Such changes initiated a return to the free play of market forces in the economy and strongly impacted on industry, including the forest industry. The economic philosophy that underpinned the state sector reforms became known as “Rogernomics” in recognition of Hon. Roger Douglas, the Minister of Finance and the leading figure driving the reforms.

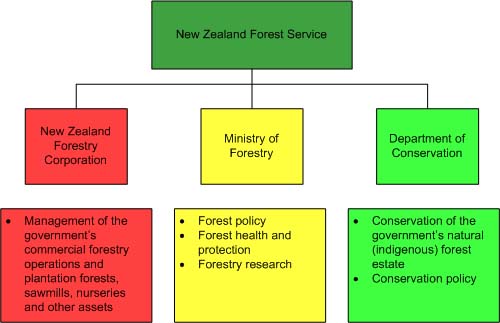

In September 1985 the government decided to separate the commercial and non-commercial management of the state forests (Roche 1990; Kirkland 1988). However, it was not until December 1985, after further government reform planning had taken place, that the details of the split were finalized. A commercially focused corporation was to administer state forest production and wood processing. A separate organization, the Ministry of Forestry, was to undertake the sectoral and regulatory functions of the NZFS. In addition, it was proposed to establish a Department of Conservation with responsibilities for administering conservation lands including indigenous forests, managing indigenous and introduced fauna and managing public recreation. A Forestry Corporation Establishment Board was set up in February 1986 chaired by Auckland merchant banker, Alan Gibbs. In July 1986 Andy Kirkland, the former Director-General of Forests and head of the NZFS, was appointed as the Interim Chief Executive of the Forestry Corporation.

Finally, on 1 April 1987 the NZFS was disestablished and its functions were transferred to three new organizations, the New Zealand Forestry Corporation (established under the new State Owned Enterprises Act, 1986), the Ministry of Forestry and the Department of Conservation (established under the new Conservation Act, 1987). At the same time, eight other state-owned enterprises came into existence under the new State Owned Enterprises Act, which set them up as limited liability companies with the goal of functioning as successful businesses (Kirkland 1988). Figure 2 illustrates the changes that occurred when the NZFS was disestablished.

The lands and forests administered by the NZFS were split between the New Zealand Forestry Corporation and the Department of Conservation depending on whether or not wood production was earmarked for the government as the owner (Kirkland 1988).

Figure 2. The restructuring of the State Forestry Sector (after Clarke 1997)

One of the most contentious issues in the restructuring process was the change in staffing requirements that resulted from disestablishment of the NZFS. Throughout the latter part of 1986 the interim Forestry Corporation Establishment Unit had been involved in rather tense negotiations with the State Union (State Services Commission), the Timber Workers Union and other unions on overstaffing of the new corporation and the estimated job losses that would occur, and the conditions under which the new corporation would employ staff. Roche (1990) summarized the final staffing changes that occurred with the disestablishment of the NZFS. At disestablishment, the NZFS employed about 7 000 people. However, the Forestry Corporation only required 550 salaried staff, 467 wage workers and 1 337 other contract workers for silvicultural and tree-felling work. By 1 April 1987 2 340 wage workers and 865 salaried staff previously employed by the NZFS, had taken voluntary severance. The Ministry of Forestry, which included the FRI, absorbed about 850 NZFS staff and the Department of Conservation about 300 staff.

The rapidity of the changes that occurred in the State Forestry Sector and the fact that there was little public discussion about the intended restructurings before they were implemented were two issues that raised the ire of many within the forestry sector and within the general public. Lindsay Poole, a former director-general of the Forest Service, was particularly critical of the Labour Government’s reforms (Poole and Johns 1992; Poole 1998) and believed that the changes imposed on the forestry sector would leave a legacy of regrets and costly problems.

After the disestablishment of the NZFS, the State Forestry Sector operated in a very different way. The concept of multiple-use forestry, which was the driving philosophy behind the way in which the NZFS operated, soon became only a memory and was replaced by an approach which sharply separated commercial forestry activities from non-commercial and social forestry activities. The three new organizations with responsibility for managing NZFS functions were very different in terms of their structure and their objectives and range of responsibilities.

Ministry of Forestry (MoF). The MoF was established as a small stand-alone government department with the stated mission of “promoting the national interest through forestry including wood-based industries”. The MoF’s head office, including the chief executive and senior managers, was based in Wellington with regional offices located in Auckland, Rotorua, Palmerston North, Nelson, Christchurch and Dunedin. The ministry’s thrust was to promote and protect business opportunities for the forestry sector, encourage public understanding of forestry and foster cooperation within the forestry sector. The head office-based Policy Division was responsible for providing policy advice to the government and monitoring trends, prospects and issues in forestry. The Forestry Services Division provided forestry consultancy services (forest growing, wood processing, harvesting, marketing contracts) and training on a “user pays” basis. The Forestry Services Division and the Forestry Development Group (promotion and advocacy) within the MoF were largely abandoned in the mid-1990s because their functions were considered to be inappropriate for a predominantly policy government department. The ministry also had statutory responsibilities for administering the quarantine, forest disease, wood preservation and forest and rural fire regulations that protect and maintain the quality of New Zealand’s forests and wood products.

The internationally renowned FRI, with facilities in Rotorua and Christchurch, constituted the largest part of the ministry. Originally established in 1947, the FRI undertook research and development work across a full spectrum of forestry areas including: establishing, growing, genetically improving and harvesting planted tree crops and marketing timber products (Forest Production Division); developing new solid wood-processing methods and new wood products (Wood Products Division); new pulp and paper processing and product developments (Pulp and Paper Division); and environmental forestry, including introduced wild animal control, soil and water protection, monitoring the condition and trends in indigenous forests and mountain lands and identifying the best tree and shrub species and establishment techniques for revegetating difficult or eroding sites (Protection Forestry Division). The FRI was transferred to the MoF more or less intact and with no major staff losses or changes in its research programmes. The FRI was eventually separated from the MoF in 1992.

The ministry reported directly to the Minister of Forests and initially received government funding amounting to approximately NZ$60 million per annum. In 1998 the MoF was merged into the Ministry of Agriculture and Forestry under a later restructuring.

The Department of Conservation (DoC). The department was established under the Conservation Act, 1987 to administer and manage those parts of the Crown estate that are protected for their natural, scientific, historic, cultural or recreational values. This includes national parks, forest parks, world heritage areas, marginal strips around lakes and rivers and more than a thousand other reserves of different kinds. The total conservation estate amounts to approximately one-third of the area of New Zealand. The department also has a stewardship role for lands that have no immediate commercial use, but are not necessarily fully protected and, in some instances, protects privately owned land under a special arrangement with the landowner. The DoC also has responsibility for conservation in New Zealand’s sub-Antarctic islands and the Ross Dependency in Antarctica.

The department inherited the non-commercial parts of the NZFS and the Lands and Survey Department which were combined with the Wildlife Service (formerly part of the Department of Internal Affairs), Historic Places Trust, the Harbour Act responsibilities of the Ministry of Transport and the marine reserve and mammal protection functions of the Ministry of Agriculture and Fisheries.

The DoC has a head office in Wellington, district offices in 14 locations and other centres scattered throughout the country. It employs approximately 1 500 permanent staff and receives government funding of about NZ$160 million per annum. The department is required to act as an advocate for conservation while, at the same time, acting as the custodian for water, mineral, recreational and game animal resources. One of the challenges for the department has been balancing its conservation role with the role of developing the resources under its control.

The New Zealand Forestry Corporation Ltd (NZFC). The corporation was set up under the State Owned Enterprises Act, 1986 to act as an efficient business enterprise comparable with businesses in the private sector. In order to achieve this aim, the corporation slashed overheads by reducing salary costs and increased productivity at the operational level compared to the previous NZFS commercial operational areas.

The corporation was governed by a board of directors chaired by Alan Gibbs, a well-known merchant banker and entrepreneur. Andy Kirkland, who had previously been the Director-General of Forests and head of the NZFS, was appointed as the CEO of the new NZFC. Kirkland, who had previously been a strong supporter of the multiple-use approach to forestry, became a strong advocate for the separation of commercial and non-commercial activities and for single-purpose commercial organizations.

Essentially, the NZFC consisted of two subsidiaries: New Zealand Timberlands, which had responsibility for managing and harvesting the 550 000 hectares of plantation forests under its control and Prolog Industries Ltd, which was responsible for processing timber at its two sawmills at Waipa and Conical Hill. New Zealand Timberlands was divided into three regions, each with a regional office and profit centre with responsibility for a number of districts. In total 14 districts were scattered throughout New Zealand.

The shareholder of the NZFC, the government, was represented by two shareholding ministers, the Minister of Finance and the Minister of State Owned Enterprises.

The establishment of the NZFC heralded a startling turnaround in the profitability of the state-owned forest industry. In the mid-1980s, the NZFS was costing approximately NZ$210 million annually to run. By its third year of operation the NZFC had turned around a precorporation annual deficit of NZ$71 million into an annual operating surplus of NZ$63 million (Birchfield and Grant 1963). Kirkland and Berg (1997) indicated that over its 3.5-year lifespan the NZFC doubled the operating surplus per cubic metre of wood produced before investment from approximately NZ$15 to about NZ$30. Despite this commercial success, the corporation was destined to be a short-lived organization. In 1990, privatization of the state forests sealed the fate of the NZFC.

The demise of the NZFS fundamentally altered the commercial relationship between the government as a wood seller and the industry as a wood buyer. Neilson and Smith (1995) indicated that two changes in particular affected the relationship. Under the corporation’s management there was a strong reduction in the length of log sale contracts (from 25 to ten years for pulpwood and from 25 years to five years for sawlogs) and stumpage sales were largely replaced with “on truck” sales.

The NZFS had provided subsidized wood supplies to the private sector for a long time. In this respect, the guaranteed supply of logs until 2030 to Tasman Forestry (a subsidiary of Fletcher Challenge Forests) at subsidized prices, which originated when the Crown and Tasman signed an agreement in 1955, was most significant. The demise of the Forest Service was accompanied by removal of most subsidies (although the Tasman deal remained in place), which impacted most severely on the sawmilling sector. Annual sawntimber production between 1986 and 1988 fell by 24 percent. Similarly, the removal of planting incentives was accompanied by a fall in new planting over the same period by 38 percent with private and state planting declining by similar proportions (Brown 1997). Small inefficient mills closed. Most companies restructured, reduced staff, upgraded machinery and revamped processes; production focused on areas of competitive advantage. Between 1988 and 1992, 3 000 jobs were lost in the sawmilling and remanufacturing industries.

The social impacts of dismantling the NZFS were widespread and variable. The communities in small forestry towns such as Kaingaroa, Murupara and Tapanui were extremely nervous about their future when it became known that the new forestry corporation would have much smaller staff requirements than the NZFS. The once busy and thriving Kaingaroa township soon became a rather depressed town with many unemployed people (Birchfield and Grant 1993). Other small forestry towns also underwent hard times after forestry workers lost their jobs and drifted to other localities. In addition, restructurings and privatizations within other sectors such as postal services, railways and the telecommunications industry, led to the dismantling of infrastructure in many rural towns.

The social impacts influenced not only towns but also whole regions. For instance, Mason in Le Heron et al. (1996) observed that the Northland region was particularly badly affected by the demise of the NZFS. Before 1987, the commercial forests of Northland, mainly owned by the NZFS and NZ Forest Products Ltd, provided jobs and career training for a large work force, a high percentage of which was Maori. Corporatization and later privatization of the state plantation forests was accompanied by a drastic drop in labour requirements and a marked deterioration in the economy of the region.

There is no doubt that the social costs across New Zealand were extremely high but, to this author’s knowledge, these costs have never been quantified.

When the Labour Government was re-elected in 1987, the Treasury prepared a “Brief to the Incoming Government”; this indicated there were some residual problems with the various State Owned Enterprises (SOEs) including the NZFC. The briefing paper suggested that the SOE model did not provide the pattern of incentives that deliver services in the most efficient manner and that a full private sector approach would be superior. This view, largely based on economic theory (Kirkland and Berg 1997), was re-inforced by the practical problems of establishing business values for the SOEs, controlling pricing policies of the SOEs and the need to obtain agreement on principles for shareholder monitoring of SOE performance. One of the major problems was obtaining a value for the Crown businesses transferred to the various SOEs. This depended on negotiations between the SOE boards and the Crown. Generally, the Treasury regarded the SOE valuations as too low and the corporations regarded the Treasury’s valuations as too high. Kirkland and Berg (1997) point out that the resulting standoffs were difficult to resolve because most SOEs had not been run as businesses before and had no private sector counterparts to use as valuation yardsticks. The Treasury also reminded the government in its briefing document that there was general agreement internationally that governments should transfer the ownership of the state’s commercial businesses and assets to the private sector when non-commercial functions had been removed from SOEs and the SOE regulatory environment had been reformed. It was not difficult to convince the Minister of Finance, the Hon. Roger Douglas, because he already firmly believed that privatization was the only answer (Douglas 1993). It also seems that he was influenced by the actions of Margaret Thatcher’s government which privatized 29 major state enterprises between 1979 and 1989 including its interests in water, gas, steel and most of its transport and telecommunications businesses (Douglas 1993).

However there was a more urgent and potent driving force behind the move to privatize New Zealand’s state enterprises than the government’s assessment of the capabilities of the SOEs to act as fully commercial enterprises. In 1987, New Zealand’s gross public debt had risen to approximately 75 percent of the GDP, the fourth highest debt to GDP ratio among OECD countries (Douglas 1993). Debt servicing amounted to about NZ$4.5 billion annually. One of the prime aims of the Labour Government’s reforms and restructurings of the public sector generally and the State Forestry Sector specifically, was to reduce debt. Selling state assets presented a quick partial solution to the challenge of reducing debt. Douglas acknowledged that selling assets would only provide a short-lived easing of debt levels or slow the escalation of debt and that the long-term solution depended on reducing government expenditure.

In July 1988 Douglas, in his budget speech to the House of Representatives, outlined the criteria for the sale of SOEs. The NZFC was not one of the SOEs earmarked for privatization. However, Douglas did announce the government’s intention to sell the state’s forest assets, but such a sale would be delayed until further investigations of various issues were completed and a decision could be made about the form of the sale. He also revealed that the government was examining ways in which it could retain the land under state ownership while maximizing the sale value of the forest assets.

The government perceived that the most important problems vis-à-vis the continuing operation of the NZFC were:

The valuation of forestry assets, initiated by the NZFC when it was first established in 1987, developed into a continuing, and at times, bitter contest between the Treasury and the NZFC. Birchfield and Grant (1993) examined the valuation dispute in some detail. Part of the problem appears to have been related to the fact that there had been no major forest sales in the past and therefore no precedents to serve as a guide.

The Treasury considered that a successful assessment of the performance of the corporation based on earnings from the resource it controlled and any future sale of state plantations, hinged on achieving an agreed valuation of the plantations. In fact, when the state plantations were initially transferred to the NZFC in 1987, the government expected that the corporation would establish a robust and defendable valuation of the plantation resources. However, this did not happen and it was a most significant factor in influencing the government to sell the plantation forests. It was the actual sale of the forests that finally led to the establishment of a robust market value for the plantations based on what the private sector was willing to pay.

In the 1970s, the FRI developed a forest estate model that was able to simulate the growth of a forest from establishment to harvest time. The model was known as FOLPI (Forest Oriented Linear Programming Interface). This model could be used to provide theoretical values of plantation forests. One of the problems with applying FOLPI was its sensitivity to variations in the discount rate used for valuation estimates. Some of the disputes that erupted between the NZFC and the Treasury were concerned with the appropriate discount rates to use in valuation assessments. In 1986 a NZFS mensuration group working in close collaboration with the FRI, developed an upgraded version of the FOLPI model which, when applied to the state’s plantations, yielded a value of about NZ$1.5 billion. In early 1987, the NZFC Establishment Board attempted to value the state forests with the help of Canadian consultants. However, no agreed valuation was achieved from this exercise and the issue was more or less sidelined by the board.

The situation, whereby the corporation held all the resource data and the valuation model and was the only organization capable of completing a credible valuation of the assets it was intending to buy, seems to be a rather curious one. The dispute about the valuations between the Treasury and the NZFC appears to have centred on the discount rates used by the corporation and the assumptions made about future wood prices. The corporation based its estimates of future wood prices on current average local prices while the Treasury believed that future wood prices would be dictated by export prices.

The Treasury employed the local economic consultancy firm BERL to help with the valuation process. BERL examined both local wood sales’ data and export prices and markets to establish a set of scenarios for valuing future trends in wood prices. By the time the BERL study was complete the corporation was understood to be suggesting a valuation of NZ$830 million for the forests. Using the same model but making the price assumptions that were produced by the BERL study, the Treasury estimated the value of the forests to be NZ$2.02 billion. Although further attempts were made to overcome the divergence in valuations between the two parties and establish an agreed valuation for the forests, this was not achieved. In fact, the divergence appeared to be widening until the time it was announced that the government had decided to sell the forest assets to the private sector. The failure to reach agreement about the value of the forest assets provided the government with the major justification to sever ties with the plantation forests (Neilson and Smith 1995).

The NZFC assumed responsibility for the sale of the plantation forests and was appointed as the principal sales agent by the government. An asset sales team was established within the corporation to document the main features of the state forest assets for prospective buyers and prepare a prospectus (Kirkland and Berg 1997). In October 1989, the corporation issued the “Sale of State-owned Forests in New Zealand” prospectus.

The sale process was complicated by Treaty of Waitangi obligations. The 1840 treaty signed by Maori leaders and representatives of the Queen of Great Britain guaranteed continued Maori ownership of their land and other natural resources. However, extensive areas of Maori land had been dubiously acquired by European settlers and other companies over the years. A Waitangi Tribunal was set up to consider and make decisions about Maori grievances concerning land and other assets taken from the Maori in the past. Large areas of the land on which the plantations were located were under Maori claims. The Maori were also concerned about the proposed sale of cutting rights, which could prevent Maori from using their land in the event of a successful claim. After a period of negotiations between the Crown and the Maori including two national huis (Maori meetings to resolve important issues), a mutual agreement was reached in 1989 that would enable the Crown to sell the existing tree crops and associated assets for an immediate payment. The agreement also provided for annual land rental payments to be placed in a trust.

The accumulated payments for any particular area of land could then be paid to any successful Maori claimant. Furthermore, the agreement provided that, if the Waitangi Tribunal recommended return of the land to the Maori, the Crown would transfer its ownership to the successful claimant; including the right to the rental from that time and progressive control of the land as the trees on that land were felled. The agreement also provided for payment of compensation to successful claimants for the fact that the then existing crop was retained by someone else. The final signed agreement successfully preserved Maori rights without appreciably weakening the interests of the bidders in the sales process (Birchfield and Grant 1993).

Another complicating factor that delayed the sale of some of New Zealand’s largest and most valuable forests were the agreements the government had with Tasman Forests and Carter Holt Harvey, New Zealand’s largest private forestry companies at that time. The details of these agreements are outlined by Birchfield and Grant (1963). In brief the agreements, which dated back to the 1950s and 1960s, provided for the supply of logs to these companies at favourable prices for decades into the future. In the Tasman case, the agreement involved provision of logs from Kaingaroa forest while, in the Carter Holt Harvey case, the agreement concerned supply of logs from Canterbury and Hawkes Bay state forests. Attempts by the NZFC to renegotiate the contract terms with Tasman Forests caused much acrimony and legal action. The corporation and the government realized that the only way to extinguish the contracts was to sell part of Kaingaroa forest to Tasman. In 1990, a Tasman offer for part of Kaingaroa was rejected on the basis that the price offered was too low. The continuing standoff between the state and Tasman was not resolved until the central North Island and Bay of Plenty forests were finally sold to a Tasman consortium in 1996. The Carter Holt Harvey contract problem, which also involved legal actions by the company against the Crown, was resolved in 1990 when the company bought the Canterbury and Hawkes Bay forest under the initial forest sales process.

Working closely with consultants from the Treasury, the corporation developed a design for the pending sale of forests. In 1989, the Crown Forest Assets Act provided the enabling legislation for the forest sales to proceed.

The sale was structured so that the purchaser bought the existing trees, buildings and other fixed assets on the land. However, the land itself remained under Crown ownership, but could be leased back to the purchaser for any legal purpose including planting of replacement crops. The main feature of the sale arrangements was a new legal instrument, a Crown Forestry Licence, which was designed to cater for the particular nature of the forest sales outlined above. The term of the licence was 35 years, which provided sufficient time for a newly planted crop of radiata pine to mature. The term of the licence was extended by one year, each year, unless notice was given to the contrary. A termination notice could only be initiated by the Waitangi Tribunal if it recommended that the land should be returned to the Maori. If the land was not liable to a Maori ownership claim, the licence term would be extended by adding a further term of 35 years, thus effectively providing 70 years or two rotations of radiata pine (Kirkland and Berg 1997).

The sale prospectus provided details of the forest assets including the fact that, of the 554 214 hectares of stocked forests, 81 percent was radiata pine. The sale involved about 90 individual state forests. The prospectus concluded that the sale would determine the pattern for the future shape of the New Zealand forest industry. The importance of the sale was highlighted by the media when they referred to it as “the sale of the century”.

Prospective bidders were formally invited to register their interest by completing a form in the prospectus and paying a refundable fee. This then entitled the intending bidders to resource descriptions, access rights to the forests to carry out their own evaluations, and access to a range of other written information and electronic databases. Detailed inventory resource documents had been prepared by the forest consultant Jaakko Poyry Pty of Finland.

The sale was an international one. The corporation’s asset sales staff made presentations to overseas companies in Asia and North America to widen interest in the forest sales. Tenders finally closed on 4 July 1990 and the Treasury assumed direct control of the sales process. The initial sales process was finalized in November 1990 when 246 700 hectares of forestry rights were sold realizing NZ$1.027 million. Details of the purchasers, areas of forests sold and amounts paid are listed in Table 1.

Table 1. State forest asset sales in November 1990

|

Purchaser |

Area (ha) |

Price paid (NZ$ million) |

|

Ernslaw One Ltd |

23 801 |

102 |

|

Tasman Forestry (Nelson) |

48 852 |

262 |

|

Carter Holt Harvey |

92 704 |

383 |

| Juken Nissho |

43 531 |

125.5 |

|

Wenita Forestry Ltd |

20 521 |

115 |

| Other sales |

17 291 |

39.6 |

|

Total |

246 700 |

1 027.1 |

An area of 303 600 hectares of state forest, much of it in central North Island, was left unsold. Although bids for the central North Island and Bay of Plenty forests had been received from Carter Holt Harvey, Fletcher Challenge and an Elders–NZ Forest Products consortium, the bids fell well short of the minimum estimated value of these forests and the bids were rejected (Birchfield and Grant 1993). A subsidiary of the NZFC (NZ Timberlands Bay of Plenty Ltd) was formed to administer the approximately 300 000 hectares of remaining unsold state forests, including the Kaingaroa forest and associated Bay of Plenty forests. At the same time, another SOE (Timberlands West Coast Ltd) was created to manage unsold state indigenous and plantation production forests on the West Coast. In 1991, the NZ Timberlands Bay of Plenty Ltd was renamed the Forestry Corporation of New Zealand. Most of the remaining state forests outside the Bay of Plenty (constituting an area of 97 000 hectares) were sold to the North American company Rayonier Incorporated in May 1992 for NZ$366 million. The sale conditions differed somewhat from the 1990–1991 sales in that Rayonier Incorporated was obligated to replant after harvesting.

It was not until early 1996 that Kaingaroa forest and the associated forests in the Bay of Plenty were sold. As in the previous sales, the offer was structured to provide cutting rights to the trees, while the land remained with the Crown, but was leased to the successful bidder under a Crown Forestry Licence. The obligation to replant after harvesting was retained in this sale offer. Three consortia registered bids for the 190 000 hectares of forests and two wood-processing plants including Waipa sawmill. In August 1996 the government announced that the successful bidder was New Zealand-based Fletcher Challenge Ltd in association with Brierley Investments and Citifor, the forestry arm of a Chinese international investment company. The Fletcher Challenge consortium paid NZ$2.03 billion for the forests and other assets.

This major sale engendered a good deal of controversy. Sutton (1996) pointed out that the sale attracted substantial attention from the New Zealand public, which was about evenly split on supporting and opposing the sale. The two major political parties (National and Labour) supported the sale, but the two largest minor parties (NZ First and Alliance) opposed the sale and both vowed to buy back the assets. The purchase enabled Fletcher Challenge to become New Zealand’s largest plantation manager with 380 000 hectares or about 25 percent of the total plantation estate.

The 1996 sale resulted in the bulk of the formerly state-owned plantations being transferred to private ownership with only about 4 percent of the total plantation estate remaining under Crown ownership under the administration of Crown Forestry Management Ltd, a Crown company that replaced the Forestry Corporation of New Zealand. The complex succession of state organizations with responsibility for managing the state plantations is summarized in Figure 3.

Before examining the consequences of privatizing the plantation forests, it is probably worthwhile to briefly broaden the focus and assess the impacts of the wider government sales programme on the national economy. Both the Labour Government and National Government, which assumed power after 1990, were committed to selling state assets including the state plantation forests and strongly supported the sales process. The rationale underpinning the Labour and National governments’ stances on privatization of state forests and other government assets was, first and foremost, to reduce public debt which had reached an alarmingly high level. Douglas (1993) believed the burgeoning debt was an unsustainable situation that needed radical action. Among the ten principles for politically successful structural reform that Douglas discusses in his 1993 book, the second principle “implement reform in quantum leaps, using large packages” and his third principle “speed is essential; it is almost impossible to go too fast”, were both rigorously applied in the Labour Government’s approach to privatization.

The sale of state forests between 1990 and 1996 realized approximately NZ$3.5 billion. During this period other privatizations included the Bank of New Zealand, Petrocorp, New Zealand Steel, Development Finance Corporation, Postbank, New Zealand Shipping Corporation, Rural Bank, State Insurance, Government Printing Office, Tourist Hotel Corporation and Telecom. When it was re-elected in 1987, the Labour Government had set a target to raise NZ$14 billion from asset sales to lower the debt burden. By 1992 the sale of government businesses including the plantation forests had raised NZ$12 billion (Douglas 1993).

Kelsey (1997) provides a comprehensive analysis of the impacts of the reforms and sales programme on the national economy. The response of the key economic indicators (economic growth, inflation, public debt, balance of payments and employment) were variable, but mainly positive after 1992. For instance, between 1985 and 1992 economic growth in New Zealand was negligible, while over the same period the economic growth for all OECD countries had averaged +20 percent. After 1992, economic growth rose to +5 percent in 1993 and +6 percent in 1994, respectively. Net public debt fell from about 51 percent of the GDP in 1992 to about 30 percent of the GDP in 1996 to 1997. However, Kelsey observed that the economic miracle was relatively short-lived. After a three- to four-year period of high growth and positive outcomes, key indicators began to turn sour. By the end of 1996, falling growth rates, above target inflation, rising overseas debt, excessive real interest rates, an overvalued dollar, an influx of speculative short-term investment, a burgeoning external deficit, falling employment growth and a significant movement of jobs offshore, signalled a declining economy. However, as Brown (1997) correctly observed, through the 1990s the forestry sector appeared to be somewhat disassociated with the general economy. The sector was characterized by continued growth buoyed by a steady increase in the harvested volumes of wood, price booms in log markets and in solid wood products in the mid-1990s and to a lesser extent, in the pulp and paper products in the late 1990s, and increased investment in wood-processing plants.

Figure 3. Institutional, structural and nomenclature changes after NZFS disestablishment in 1987

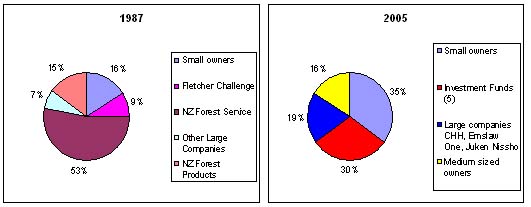

Ownership of plantation forests. The privatization of state plantation forests decreased the Crown’s ownership of the plantation estate from 53 percent in 1987 to about 6 percent after 1996. After completion of the sales, the two largest corporate owners were Fletcher Challenge (28 percent) and Carter Holt Harvey (25 percent). Small private owners made up about 22 percent. Perhaps the most notable feature of the new ownership pattern — after the 1990 sales — was the rapid increase in foreign ownership of plantation trees (cutting rights). Direct foreign ownership of the plantation forests increased from less than 2 percent in the 1980s, to about 18 percent after 1996 (Gilbert 2000). However, total foreign interest in the plantation forests, taking into account foreign stakes in the New Zealand forestry companies, increased to about 48 percent. Although much of the public concern about the forest sales process focused on the “take over of New Zealand’s plantations by foreigners”, the Labour and National governments did not hold the same concerns and considered that international companies such as Rayonier (NZ) Ltd and Juken Nissho would promote radiata pine in the United States and Japan respectively, and generally benefit New Zealand’s efforts to market wood products offshore. Birchfield and Grant (1993) also point out that the sale of forests to foreign companies shortened the distribution chain from forest to overseas users of end-wood products.

Wood-processing capacity. Prior to the sale of the state forests, the New Zealand Forest Industries Council estimated that about NZ$7 billion of investment was required to satisfactorily develop the forestry sector over the next few decades. The government was adamant that such high investments could only be made by the private sector and many of them needed to be sourced from overseas. In the 1980s, potential overseas investors had viewed New Zealand rather negatively (Edgar et al. 1992). A survey of overseas companies with interests in forestry investment indicated that the reforms, restructurings and privatizations implemented by the Labour Government between 1984 and 1990, were viewed positively by potential investors (Edgar et al. 1992), but major concerns remained about labour conditions, location (isolation) and cultural immaturity.

The sales process had created a mix of domestic and international companies operating within the New Zealand forestry sector which Birchfield and Grant (1993) believed provided an improved situation to deal with the burgeoning wood-processing opportunities. This certainly proved to be the case. Aggregated investment in wood-processing facilities reached NZ$250 million in 1990 and NZ$300 million in 1991 (Le Heron et al. 1996). A reasonable rate of investment in wood-processing facilities continued through the 1990s. Notable investments in the early and mid1990s included the establishment of a NZ$62 million laminated veneer plant in Masterton, the building of a NZ$40 million plant in Gisborne and a multimillion dollar upgrade and expansion of a wood-processing mill in Kaitaia by Juken Nissho. Rayonier (NZ) Ltd invested NZ$2 million in a sawmill upgrade in Gisborne and NZ$120 million in a new medium density fibreboard (MDF) plant at Mataura. Carter Holt Harvey spent NZ$75 million on doubling the capacity of its Canterbury MDF plant in 1992, NZ$8 million on sawmill upgrades in Nelson and NZ$1.3 million on drying kilns at Tokoroa (Le Heron et al. 1996).

Despite these investments in wood-processing facilities, concern continues about the lack of wood-processing capacity in New Zealand to deal with increasing plantation wood volumes. For instance, Rumker (2004) commented that future forestry investment returns will be dependent on the forestry industry’s ability to address the growing imbalance between timber supply and value-added processing. Obviously, there is a need for a great deal of further investment in wood-processing plants in New Zealand.

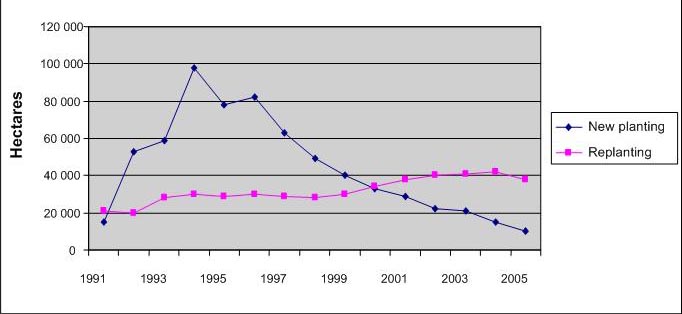

New planting. Although it is difficult to directly link the privatization of the state forests to an increase in the rates of new planting, there is little doubt that the new ownership patterns contributed to an overall growing optimism within the forestry sector in the early to mid-1990s. Between 1993 and 2000, the sector underwent a third planting boom which culminated in 1994 when about 100 000 hectares of new plantings were established (Figure 4). During this seven-year planting boom, about 430 000 hectares were added to the national plantation estate. Nearly all of this new planting was carried out by non-corporate foresters (farm foresters, investment foresters and other small landowners). After 2000, the government’s approach for dealing with carbon credits, the strength of the New Zealand dollar, burgeoning shipping costs, the way in which the tax regime applied to forestry, generally falling profitability within the wood export industry and a growing perception that investments in forestry were risky, caused new planting rates to fall dramatically.

Figure 4. New planting and replanting rates (hectares) from 1991 to 2004

Multiple-use forestry. The forest sales concluded the demise of the state’s dominant role in the forestry sector and the strong emphasis on multiple-use forestry, which had underpinned the modus operandi of the NZFS for many decades. Although the corporatization of the state’s plantations had signalled the end of large-scale multiple-use forestry, the privatization of the plantations strengthened the strong focus on production and commercialism within the plantation industry and widened the separation of the plantation industry from conservation and protection forestry, which was now largely under the control of the DoC. However, it would be wrong to consider that the large forestry corporations and other plantation owners did not have multiple land-use roles. For instance Carter Holt Harvey Forests and Fletcher Challenge Forests have extensive tracts of indigenous forests often intimately located within the plantation estate. These require management to protect their health and other values. Moreover, many of the plantations cover areas with valuable water resources or fragile soils that need protection; this necessitates special forest management approaches such as limiting the size of clear-cut areas or providing substantial riparian protection zones.

Harvest rates and export revenues. Harvest rates continued to rise steadily between 1994 and 2003 when total harvest volumes reached 22.4 million m3. After 2003, harvest rates declined due to deteriorating market conditions, the strong New Zealand dollar and the decision by some new private owners of the forests to reduce the areas of harvest in their forests. Similarly, export revenues from the sale of logs, sawntimber, board products, pulp and paper and other remanufactured wood products, continued to rise steadily between 1994 and 2003, reaching NZ$3.488 billion in June 2003 (Ministry of Agriculture and Forestry statistics 2004).

Environmental and social consequences. The environmental impacts of the sale of the state plantations are difficult to assess, but were probably not very significant. The standards of plantation management, according to a number of people involved in the forestry sector at that time, did not change to any noticeable extent. The introduction of the Resource Management Act (RMA) in 1991 placed considerably more pressure on plantation managers to manage their forests in a sustainable manner and through the 1990s there was a gradual overall improvement in the standards of plantation management, particularly in the areas of soil and water protection and conservation of biodiversity. The administration of the RMA (discussed below) led to improved harvesting and road construction, particularly on hill country, and improved riparian protection alongside lakes, streams and rivers. Some private companies became involved in projects aimed at conserving or protecting important rare or endangered bird and plant species such as the native kiwi, native falcon and the native flowering tree, the pohutakawa. Over recent years several of the large and medium-sized plantation owners have gained FSC certification which adds to the need to manage the plantation estate to very high standards.

The social consequences of the sale of the plantations were not of the same scale as those which occurred when the Forest Service was disestablished. Some NZFC staff lost their jobs, but many of the field contractors involved with harvesting, silvicultural operations and plantation establishment simply carried on under new contracts with new plantation owners.

Since its establishment in 1987, the DoC has retained the stewardship of approximately 4 million hectares of indigenous forest and scrub land making this department the country’s largest forest land manager. Since 1987, the total area of forest under the DoC’s control has gradually increased as indigenous forests have been withdrawn from production and placed in the conservation estate. The largest addition to the conservation estate occurred in 1999 when the Labour Government decided to halt all timber production from state-owned indigenous forests (mainly under the control of Timberlands West Coast Ltd) and placed them in the conservation estate.

Ever since it was established, the DoC has always appeared to receive insufficient government funding to carry out its departmental objectives (Young 2004), despite the fact that its funding has increased substantially since 1990. The DoC also appears to suffer from the fact that it is not only responsible for developing conservation, preservation and protection policies, but also for managing and implementing them. In addition, the DoC has an important advocacy role for the conservation of natural resources, which makes this department truly multifunctional. These circumstances force the DoC to manage competing demands on its resources (Hartley 1997). Hartley suggested that to enable the DoC to manage the conservation estate more efficiently and effectively, its advocacy role should be removed from the department and its policy development and advisory role should be separated from its service function role. To date this has not happened.

The funding and competing function anomalies within the department were highlighted in 1995, when a DoC viewing platform located on the West Coast of the South Island, collapsed, killing 13 people. An investigation of the incident showed that systemic problems and underfunding contributed to the tragedy and led to a restructuring of the regional organization of the department. Since 1995, the DoC has appeared to operate more efficiently than in earlier years and has initiated some groundbreaking conservation projects such as its “mainland island” programme, pest eradication projects, habitat restoration programmes and endangered species breeding and release projects.

The MoF lost approximately half its total staff when the FRI was severed from the ministry in 1992, as part of a major restructuring of New Zealand’s government science and research organizations. In 1997, a review team consisting of senior public officials from the State Services Commission, the Ministry of Agriculture, the MoF, the Treasury, the Department of the Prime Minister and the Cabinet and Te Puni Kokiri, recommended that a merger of the MoF and the Ministry of Agriculture should proceed. A cost–benefit analysis showed that the benefits (ongoing efficiency gains and cost savings) outweighed the costs of the merger. The review team also recognized that such a merger would not occur without risks and that explicit attention would need to be given to forestry stakeholder concerns that a merger could lead to a loss of forestry skills, focus, capability and knowledge (Government Review Team Report 1967). In 1998, the remaining small MoF was merged with the Ministry of Agriculture to form the Ministry of Agriculture and Forestry (MAF). At the time of the merger, the forestry sector expressed concern that the forestry component of MAF would be very subordinate to the larger agricultural component and would lose some of its ability to effectively bring forestry issues to the attention of the government and provide policy advice in a timely fashion. The merger did bring about a rather unusual situation in that the MAF reported to two ministers, the Minister of Forestry and the Minister of Agriculture. The forestry activities of MAF, at least in the first few years after it absorbed the MoF’s activities, have appeared to mainly focus on collecting and publishing statistics, border control activities and trade development activities.

Institutional structural changes that have occurred since the demise of the NZFS are presented in Figure 3.

The bulk of forestry and wood product research has been conducted by the state-owned FRI in Rotorua since its establishment in 1947. Other providers of forest and wood product research have included the two largest private companies, Carter Holt Harvey and Fletcher Challenge Forests, universities (particularly Canterbury and Auckland universities), the Department of Scientific and Industrial Research (DSIR), the Soil and Water Division of the Ministry of Works and two government research associations (Logging Industry Research Association and Building Research Association of New Zealand).

The state sector reforms set in motion by the Labour Government in the mid- and late 1980s soon extended to the science and research sector. The FRI, which had been almost entirely supported by an allocation from the Forest Service’s departmental funding up until the early 1980s, operated on a diminishing government funding allocation after 1984 and an increasing commercial revenue stream from work done under contract for the private sector, overseas organizations and other New Zealand government agencies (Kininmonth 1997). By 1991/1992 the FRI operated on a total budget of NZ$34.1 million; NZ$20.2 million from the government Public Good Science Fund and NZ$13.9 million from commercial activities (Kininmonth 1997).

Two reviews of science, research and technology in New Zealand were conducted in quick succession in 1986 and 1987–1988 respectively. The first review known as the Beattie Review was conducted by a Ministerial Working Party on S&T under the chairmanship of Sir David Beattie and aimed to determine the role that the government should adopt in science and technology (S&T) in New Zealand. Although the report of the Ministerial Working Party made a number of far reaching recommendations including the appointment of a minister for S&T responsible for the funding and operation of three research councils, 150 percent tax deductibility for expenditure on research and development and a doubling of New Zealand’s expenditure on research and development in both the public and private sectors by 1993/1994 (Report of the Ministerial Working Party on Science and Technology 1986), the government took little immediate action in response to these recommendations.

The second review was carried out by the Science and Technology Advisory Committee (STAC) to examine the organization and funding of science and technology. The review report (STAC 1988) highlighted the need for the government to fund research outputs, rather than to fund inputs, and the need for contestability in the allocation of government funding. The concept of a single contestable pool of funding for which various research organizations, including universities, would bid for funds appealed to the Labour Government.

One aspect of the review report which concerned the FRI was the statement that “There are particular difficulties in justifying a continuance of government funding for forestry research that is related to commercial exotic forestry”. Fortunately for the FRI, the government took no action in this context. However, the government (the Treasury) continued to debate the differences between appropriable research and public good research and the fine line which separated the two research types.

In 1989, the government announced that it intended to act on some of the recommendations contained in the two reviews and establish a Ministry of Research, Science and Technology (MORST) to provide research policy advice and determine research priorities, and a Foundation for Research, Science and Technology (FRST) which would also help determine priorities, but also administrate a contestable research fund. Allocations from the fund were to be based on a bidding process. The change from departmental allocations for research to a competitive bidding process started in 1990/1991. However, this was just an embryonic reform of the science sector and more dramatic changes were soon to occur.

In 1992, after much planning and consultation by a Science Task Group that had been set up to report to the government about the re-organization of the state science sector, the four major state research organizations (FRI, DSIR, MAF Technology and the Meteorological Office) were reorganized into ten Crown Research Institutes (CRIs). The CRIs were established under the Companies Act (1955) and were Crown companies with more commercial powers than the research agencies they replaced. Each CRI operated under a CRI board appointed by the minister of CRIs. Each board reported to the two shareholding ministers of the CRIs (Finance and CRI ministers).

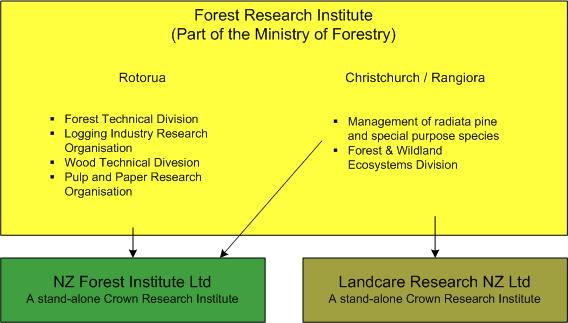

The shift in the organization of the government science sector to a CRI structure resulted in some structural and status changes for the FRI. It became detached from the MoF to become a standalone CRI. The Rotorua-based component of the FRI remained largely intact, although there were losses of science and technical staff in some areas of research deemed to be superfluous to requirements in the new CRI. However, the bulk of the Christchurch/Rangiora-based component of the FRI, which was known as the Forest and Wildlands Ecosystem Division of the FRI, was transferred to a new CRI, Landcare Research NZ Ltd. The areas of research transferred to Landcare Research NZ Ltd included wild animal management, forest biophysical processes, forest hydrology, rehabilitation of modified landscapes and forest and wildland ecology. Only a small contingent of Christchurch/Rangiora people working in the management of radiata pine and the special purpose species section remained with the FRI and its nomenclature changed to NZ FRI Ltd. The broad structural changes are illustrated in Figure 5.

Figure 5. Re-organization of the FRI in 1992

The impacts of the re-organization of the FRI into a CRI have been both positive and negative. Kininmonth (1997) noted that on the positive side, the government gained greater appreciation of the importance of research and development, including forestry research, to the economy and development of the nation; greater commitment to increased funding for research and development and the company structure has enabled a more commercial orientation which has helped to stimulate development and commercialization of new technologies and encouraged partnerships between industry and CRIs.

On the negative side, the cost of research has risen because of (1) an escalation in transaction costs and overhead costs, (2) considerably more attention being accorded to safe, short-term commercial research and revenue-earning projects, possibly at the expense of longer term innovative research and (3) apparent growing dissatisfaction among scientists owing to limited advancement prospects, their inability to influence the prioritization of research and the considerable extra-curricular time they spend on developing bids and performing short-term commercial work. In 2005, scientists from a number of CRIs attracted considerable media coverage when they raised some of these issues.

NZ FRI Ltd nomenclature changed to Forest Research Ltd in 2002 and then to “Scion” in 2005. Much of the original production forestry research including genetic tree improvement and forest protection work has been incorporated into a joint Scion–Australian CSIRO research arrangement called “ENSIS”. There has also been a noticeable shift in the focus of forestry and wood product research over the last decade. The proportion of research into wood product development, wood processing and pulp and paper products and processing has steadily increased as the proportion of research effort into the establishment, growing and harvesting of forest has declined. Most of the wood products and processing research is concerned with radiata pine. Currently, one of Scion’s main thrusts is on the development of new biomaterials from radiata pine.

The ownership of plantation forests has continued to change since the late 1990s. The most notable change has been a large expansion in ownership of the New Zealand plantation estate by North American institutional investors. Investor firms known as Timber Industry Management Organisations (TIMOs) have dominated the purchase of plantation forests since 1998. In simple terms a TIMO is an investment adviser who manages funds that focus on generating investment returns from timberlands (McKenzie 2003). By late 2005, five large TIMOs accounted for approximately 30 percent of the total plantation estate (Edgar 2005). Unlike many of the forestry corporates, TIMOs are usually free of debt and are therefore free of the problems associated with having to concentrate on maintaining cash flows. Instead, their focus is on increasing the value of their asset base. Of particular interest is the ownership by Harvard Management Company (Kaingaroa Timberlands) of most of the central North Island plantations including Kaingaroa forest. Harvard Management Company purchased the Central North Island Partnership forests managed by Fletcher Challenge Forests in December 2003. In the same year the other forests managed by Fletcher Challenge were purchased by foreign investors thus effectively ending Fletcher Challenge’s involvement in plantation forest ownership.

There is a stark difference in the pattern of ownership of the plantation estate in 1987 prior to the corporatization and privatization of the state-owned plantations, and the ownership pattern in 2005. Figure 6 shows that the Crown owned over 50 percent of the forests in 1987. In 2005 Crown ownership was a little over 2 percent (plantations under the stewardship of MAF and Land Information New Zealand) and the bulk of the ownership was in the hands of companies, TIMOs and other medium- to small-scale private owners who were not involved in the New Zealand forestry sector in 1987.

| |

| Total area of plantation 1.09 million hectares | Total area of plantation 1.83 million hectares |

| Figure 6. Ownership of New Zealand’s plantation estate in 1987 and 2005 | |