![]()

![]()

![]()

Benjamin F. SanvictoresBenjamin F. Sanvictores is Vice-President of the Philippine Lumber and Plywood Manufacturers' Association. This article was originally presented at the FAO World Consultation on Wood-based Panels held in New Delhi in February 1975.

The big timber-exporting countries of the Pacific are phasing out of log exporting and moving toward the manufacturing of their own wood products. The author describes the problems and implications of this change in the Philippines. He calls for common southeast Asian policies on log exports and urges log-importing areas to move into secondary processing at a time when the traditional log exporters want to make and sell semifinished products.

During the past three decades, extraction of timber from Philippine forests has steadily accelerated with the increasing demand for Philippine logs from Japan and other Asian countries. For more than a decade now the forest products industry has been among the country's top foreign exchange earners, accounting for about 29% of the aggregate export receipts in 1973 and 22% in 1972. Exports of logs were valued at over US$303 million f.o.b. in 1973, and $157 million in 1972. Plywood exports were worth more than $77 million f.o.b. in 1973 and $51 million in 1972. However, although these products remain among the country's top ten earners, the situation during the third quarter of 1974 was bleak because of a significant decline in demand and prices in the world market.

As of 30 June 1973, 338 timber licences were in operation with an allowable cut of 16.9 million cubic metres. There were 421 processing plants with a log requirement of 11.5 million cubic metres, representing 68% of the total allowable cut. These included 370 sawmills (using 69.3% of the actual cut), 18 veneer plants (5.6%) and 31 plywood plants (25.1%). There are only 10 blackboard plants, l hardboard plant, 1 particle board plant and 3 pulp and paper mills utilizing wood wastes.

The export of logs has always been the most profitable sector of the Philippine wood industry, which is consequently to this day still largely confined to logging operations. By 1973, only about 33% of the country's timber output was being processed into lumber, veneer, plywood and other products. The rest was exported in the form of raw logs. Most processing plants are underutilized. In 1973 sawmills were operating at about 25% of rated capacity, veneer plants at 84% and plywood plants at 59% (later figures were not available at the time of writing).

The need to redirect the development of the Philippine wood industry has become increasingly apparent in the light of the nation's more serious and pressing problems. The swelling population, for instance, which stood at about 42 million in 1974, is increasing at the rate of about 3% per year-thus intensifying the already serious unemployment problem.

Other problems which concern the industry include the growing need for foreign exchange to support the industrialization and development programme; the need to ensure a continued supply of timber for future generations; the prevention of disastrous floods and droughts.

The government's policy is thus to gradually phase out log exports until it enforces a total ban, starting from 1 January 1976.

Problems of the wood-based panels industry - The policy of log export phase out brings into focus the existing problems of the industry and how these are bound to worsen as a result of the projected local processing of the several million cubic metres of logs still being exported.

It must be noted that this policy is part of an overall national economic development plan and therefore government action is the key to its implementation. To start with, the policy is supported by a set of incentives through the Investment Incentives Act (R.A. 5186) and the Export Incentives Act (R.A. 6135), as well as monetary and financing policies which favour the wood-processing industry but not the log export industry. Disincentives are also seen in the higher export duties and fees imposed on log exports.

High cost imported machinery, spare parts, supplies, materials and fuel - since the energy crisis in 1973 the cost of production has shot up in unheard of proportions. By mid-1974 oil prices had increased fivefold, precipitating a worldwide inflation. Consequently, prices of all manufactured goods also rose sharply.

In the Philippines, except for labour and the wood raw material, all the factors involved in the manufacture of wood-based panels (adhesives, machinery, fuel, etc.) have to be imported at inflationary prices. Furthermore, most wood-processing plants have to generate their own electric power because none is available in the remote areas where the mills are located.

By mid-1974, cost of production was estimated to be about 77% higher than 1973. Recent studies show that (compared to 1973 figures) the cost of wood rose by about 80% in 1974; prices of glue and flour-both imported items - increased by 125 %. Labour costs went up 35% and general overhead by 58%. Estimates of average mid-1974 production costs for wood-based panels are shown in the table.

Since inflation in the Philippines and the world over continues unabated, it is expected that these costs will continue to rise.

These facts point to the necessity of intensified wood product research, so that the development of the Philippine wood industry will be less dependent on imported components and machinery.

COST OF PRODUCTION OF WOOD-BASED PANELS, 1974 ESTIMATES

|

Components |

5.5-mm plywood |

19-mm blockboard |

||

|

US$ per cubic metre |

Percent |

US$ per cubic metre |

Percent |

|

|

Wood |

76.34 |

52.41 |

41.41 |

36.27 |

|

Glue and flour |

25.17 |

17.28 |

15.18 |

13.30 |

|

Direct labour |

11.11 |

7.63 |

16.93 |

14.83 |

|

Overhead |

33.04 |

22.68 |

40.64 |

35.60 |

|

Total |

145.66 |

100.00 |

114.16 |

100.00 |

Great financing requirements - To process all the logs still being exported will mean the full utilization and expansion of existing plant capacities.

In addition, it will be necessary to establish new and bigger mills. The wood industry is capital intensive. In 1973 the Philippine government interagency group estimated that the nation's log export phase out programme will require about US$100 million, plus about Phil. $750 million to establish the additional mills needed to process the logs that will not be exported from the beginning of 1976.

And although no 1974 estimates were available, it is known that these figures have risen even higher considering world inflationary trends. Increasing interest rates from world financing institutions compound the problem.

Studies are under way on how the government can give financing assistance to the wood-processing industry, making such assistance part of the package of incentives. For a chain of valid reasons, the government realizes that the industry has to be helped financially, especially during times of recession in foreign markets. The principal of these reasons is that the only alternative action of industry would be to cut down or even stop operations, and the economy could ill afford the inevitable laying off of factory workers.

Under a set of guidelines, joint ventures with foreign investors are being encouraged by the government in certain areas of development.

Low recovery from the forest - About 30% of the tree, consisting of stumps and branches, is left to rot in the forest because of the prohibitive cost of transport from widely dispersed logging areas to the mill site.

Low recovery in the mills - Average yield from logs in plywood mills is about 50%; in sawmills about 60%. This may be attributed to the lower quality of the logs being processed, as the mills are completely dependent on their own logging operations. On the other hand, wood processors in Japan and the Republic of Korea buy logs from several sources and are thus able to specify and get the quality they need.

Lower standards of skilled labour and technology are another important reason for low recovery. Hence, part of the government s policy is an intensive manpower development programme to supply the needs of the industry.

Nonutilization of wood wastes from mills - The bulk of the wood wastes from processing mills is burned. Some is used for boiler fuel. In other countries, factory wood wastes find a market in wood chips for pulp mills.

In view of the current oil shortage and high prices, the use of factory wood waste for boiler fuel seems to be indicated in a country that has to import its fuel needs to support industry.

Problems of marketing - More than 90% of the Philippines' plywood production is exported. From the 1950s up to the early 1960s the industry showed remarkable and steady growth, due to the great demand of the United States market which absorbed about 97% of the country's total plywood exports.

Since the mid- 1960s, however, the Republic of Korea has increased its share in the United States market for imported hardwood plywood, and by 1973 this share represented about 58%. The Philippines' share of this market is now about 15%.

Japan's reduced exports of plywood can be explained by the spectacular rise in its domestic consumption. As a matter of fact, beginning in 1973, Japan has become a big plywood importer.

This unfavourable export situation for the Philippines is due principally to the following factors:

· High freight rates to both domestic and foreign markets. Freight costs remain the biggest problem in the marketing of plywood both locally and abroad. Past government policies caused the establishment of small-scale veneer and plywood mills within the timber concession areas all over the archipelago. These resulted in insufficient cargo being loaded in numerous outports with inadequate facilities, causing delays in shipment and raising the cost of freight: This is the principal reason why the Philippines has steadily lost its share in the United States plywood market.

Recent studies show that freight rates from the Philippines to the United States went up by about 44% from February 1973 to February 1974.

Recognizing the advantages of other Asian countries where plywood exports are shipped from only two or three ports, Philippine government economic planners have recently come up with the suggestion that new wood-processing plants be established only where the government has a definite programme for port development.

Government incentives are also aimed at accelerating the expansion of the local shipping industry, so that logs can be more easily and cheaply transported to the mill sites.

During the past few years the freight situation has somewhat improved, due to the practice of transhipment to fewer main ports and the incentives offered by shipping companies for bigger volume shipments and faster loading rates.

Priority is being given to the port development programme so that certain main ports will have adequate facilities for handling wood and other exports.

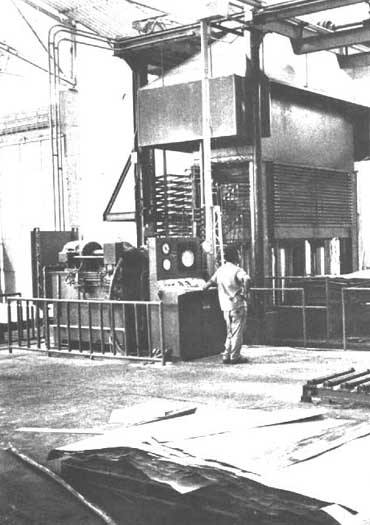

FEEDING SHEETS INTO A PLYWOOD PRESS At times, easier made than sold

· Overdependence on the United States market. The United States is still the principal market for Philippine plywood. In 1968 it took about 97% of the country's total plywood exports. Although this figure went down to 81% in 1973, any slump in the United States market is still felt much more severely in the Philippines than in other ply-wood-exporting countries that are not as dependent on it. The slump in the world market during the third quarter of 1974 resulted in the slowing down and even the closure of some of the country's plywood factories.

The high cost of construction during these inflationary times, coupled with increased interest rates, has slowed down the construction industries of the United States, Europe and Japan. Consequently, large volumes of plywood and veneer have accumulated in the warehouses, particularly of the big producers awaiting more favourable conditions to dispose of their production, even if only to tide them over the bad times.

In the Philippines, the government is undertaking an intensive low-cost housing and infrastructure development programme, to build up the domestic market for plywood products used in construction and thus alleviate the worsening situation of the wood based panels industry.

The possibility of establishing barter trade agreements with oil-producing countries and trade relations with centrally planned countries, with which the Philippines has had no trade relationships in the past, is now being seriously considered by government economic planners.

In the light of recent developments, the search for new markets for Philippine wood products is more than ever indicated. Diversification is needed so that the industry will not be dependent on only one product for export. Market research should also reveal which new wood products could be used in importing countries, preferably those that would utilize wood wastes from the mills and the forests.

· Tariff barriers. To protect their own plywood industries, developed countries have set up tariff barriers on imports of processed wood products originating from developing countries such as the Philippines. While in 1971 duties on veneer and sawnwood were reduced by 50% in Japan, there has been no reduction of duty on plywood. The United States still imposes an import duty of 20% on Philippines mahogany, although many European countries have reduced tariffs on imported plywood by applying the generalized scheme of preferences toward developing countries.

· Local government taxes that prejudice the wood export industry. One factor that has raised the cost of shipping plywood from the Philippines is the export tax on wood and products imposed by the government. When the market was good a premium tax was also levied on the wood export industry. Now that the industry is again in great difficulties, the government is taking a second look at this tax structure.

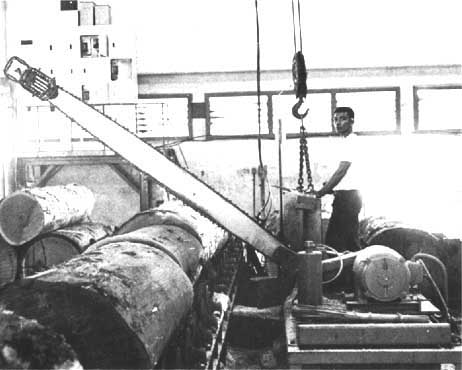

A FILIPINO WORKER TRIMS VENEER LOGS And keeps a larger slice of wood profits at home

Prospects of the Philippine wood-based panels industry - In spite of the bad export market for timber and timber products in mid-1974, the wood industry can look forward to better times. However, unless the major log-producing countries in southeast Asia - Indonesia, Malaysia and the Philippines - can cooperate and work out a regional policy on log exportation, the development of the wood-processing industry in these countries will be burdened with difficulties and will be very slow indeed.

Already some form of cooperation among the log-producing countries exists. In 1969, technical and economic agreements were concluded between Indonesia and the Philippines. These were renewed in 1974, and two of them have a direct bearing on forestry and forest industries. Through the Association of Southeast Asian Nations, which includes the Philippines, Indonesia, Singapore, Thailand and Malaysia, economic and trade cooperation in the field of timber processing, among others, is now being studied.

Sooner or later the other log-producing countries in the Pacific area will decide to put a total ban on log exportation and ship only processed wood products, even if these products are only in the first stages of manufacturing - such as veneer and plywood. Accordingly, the log importers - Japan and the Republic of Korea, for example-should start to plan on a vertical diversification. They could move toward the "secondary processing" of plywood and wood-based panels, and produce the more sophisticated products requiring higher technology.

To support the country's programme of expansion for the wood-processing industry, and to ensure a continuous and steady supply of the needed raw materials, the government has undertaken intensive and comprehensive studies of forest resources so that log-surplus and log-deficient areas may be definitely identified. Both the government and private sectors are now actively engaged in reforestation projects. Industrial tree-farming ventures are being established jointly with foreign investors.

At the time of writing, the prospects for the establishment of plants to manufacture panels utilizing wood wastes is dim. The spiralling costs of the imports required would raise production expenses to prohibitive levels. Furthermore, except for blockboard which is made from low-grade lumber, all other panels utilizing wood wastes (e.g., fibreboard and particle board) are oriented toward the domestic market. Their export is difficult due to high freight charges, and also because developed manufacturing countries produce them from their own factory wastes.

It is therefore necessary to build up the local market for these products, and until the local market can absorb them the only use that can be made of the bulk of factory wastes is for fuel - a measure that can help save the foreign exchange currently used for fuel imports.

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}