![]()

![]()

![]()

A view of the world situation with emphasis on trade with the United States

S.L. Pringle

S.L. PRINGLE is Chief of the Policy and Planning service as well as senior economist of the FAO Forestry Department. This article is adapted from a paper given at the Forest Products Research society symposium "Timber supply: issues and options," October 1979, San Francisco.

The purpose of this article is to appraise the outlook for United States imports of wood from tropical areas. The future level of these imports will, of course, depend upon many factors, including the pattern of expanding national demand, both quantitatively and qualitatively, the level and nature of the country's wood production, developments in the tropical forest; the growth of consumption in other major consumer-importer regions, and in the tropical producing countries themselves; tariff changes and particularly quantitative and qualitative limitations on exports; as well as developments in other traditional or potential exporting regions of the temperate zone. Various trends and prospective development, related to these factors will be considered in turn after first assessing the relative importance of tropical wood imports into the United States and summarizing trends in the development of these imports¹.

(¹ Because of the use of tropical logs in temperate countries and eventual export in the processed form, sometimes in mixture with other wood raw material, it is not always possible to precisely identify tropical wood from trade data. Consequently, figures provided in this paper are subject to a degree of error.)

(² References 2, 3, 4, 5, 8, 9, 10 and 12.)

Imports of tropical logs into the United States have never been large, reaching about 0.5 million m³ (slightly more than 100 million board feet log scale) in the early 1950s. Since then, these imports have declined continually and currently amount only to about 25 thousand m³ (5 million board feet), barely more than a tenth of 1 per cent of the country's hardwood con gumption. It should, however, be noted that 22 thousand m³ (5 million board feet) of coniferous logs, ire.. ported from Chile in 1978, have not been included as tropical logs.

Imports of tropical hardwood lumber, by contrast, are considerably more important. These grew from 200 thousand m³ in the sawn form (80 million board feet) in 1950 to 580 thousand m³ (388 million board feet) in the peak year of 1973 when they amounted to more than 5 percent of domestic consumption of this product category. Although imports dropped very steeply in 1975, they had recovered to nearly 600 thousand m³ (250 million board feet) by 1978.

Softwood lumber imported from tropical countries is also fairly important in the nation's consumption, but has shown a declining trend over the past three decades. Imports from Mexico have declined markedly from their 1950 level of 450 thousand m³ (190 million board feet). Current softwood sawnwood imports from all tropical regions are about 140 thousand m³ (60 million board feet). At the peak import period in 1973, these imports accounted for less than one half of 1 percent of national consumption.

Although tropical logs and sawn-wood do not comprise a Large portion of consumption, they often serve specialized uses. Lauan lumber is widely used for millwork and construction. Other groups of species are used where strength and durability are important on where workability is important. A number of specie, have specific uses for furniture, mill work, boat-building or pattern-making.

It is, however, hardwood plywood that plays the most striking role in supplying the country's demands for tropical woods. :In the peak period of consumption in 1972, tropical hardwood plywood comprised 58 percent of national hardwood plywood consumption by volume and considerably more on a square-metre basis. Imports of tropical plywood (including some softwood and some mixed softwood-hardwood) have grown rapidly from approximately 7 000 m³ (12 million square feet) in 1950 to nearly 2.7 million m³ (6.2 thousand million square feet) in the peak import year of 1972. Although declining sharply in the mid-1970s, imports of tropical plywood had recovered in 1978 to more than 2 million m³ (nearly 5 000 million square feet).

Lauan and meranti plywood have been extensively used for construction of mobile housing, residential housing, nonresidential building and in remodelling. Much is used for siding, both interior and exterior. It is sometimes used for its decorative value, but much is for general construction. Other plywoods are more frequently used for cabinet and furniture manufacture.

Hardwood veneer imports from the tropics are also quite important. They have grown from 154 thousand m³ (6.3 million square feet) in 1950 to 378 thousand m³ (1.7 hundred thousand square feet) in 1973, although the current import level is less than half of that amount.

Most Lauan veneer is used for cores or backs of plywood manufactured in the United States with domestic facing. Other imported species are often used for facing.

In 1973, total imports of tropical hardwood logs, sawnwood, plywood and veneer were the estimated log equivalent of 7.4 million m³ (260 million cubic ft or about 1.7 thousand million board feet), slightly less than 2 percent of the nation's total industrial wood consumption. Nearly two thirds of these tropical imports, in log equivalent, were in the form of plywood. The total value of tropical forest products of these major categories was, in 1978, in the order of $625 million, with plywood and veneer comprising nearly four fifths of the value. A further value of about $100 million was in other tropical mechanical forest products imports, of which mouldings and furniture parts were most important. Other manufactured wood imports, notably furniture, also have tropical origin.

TROPICAL LOGS AWAITING EXPORT more will be used in the countries that grow them

MAJOR TRADE FLOWS: Tropical Hardwood LOGS 1978 - Total: 42.9 million m³

The major exporters of tropical hardwood logs are Indonesia, Malaysia (Sabah and Sarawak), the Ivory Coast, the Philippines, Gabon, Ghana. The big importers are the Republic of Korea, China, Singapore, Italy, France and Hong Kong. The bilateral flows from Malaysia to Japan and from Indonesia to Japan, account for about 45 percent of the entire tropical hardwood log trade. Those from Indonesia to Korea, and to China; from Malaysia to China and to Korea; from the Philippines to Japan, and from Indonesia to Singapore are the largest. All these flows are in excess of one million m³. Flows from the Ivory Coast to Italy and to France; from Gabon to France, and from the Ivory Coast to Spain are the largest to individual European countries. These flows are in excess of 350000 m³ but are less than one million m³.

(³References 3, 5, 10.)

During the early 1950s, when logs accounted for the largest share of tropical wood imports, Latin America, Africa and the Far East were all substantial contributors to the supply with mahogany being an important species.

Since the rapid developments of plywood, sawnwood and veneer imports from the East in the latter part of the 1950s, that region has been increasingly the most important supplier. The region's exports have been based largely on Lauan, the so-called Philippine mahogany, and meranti, two important groups of dipterocarp species, but a large variety of other woods bulk increasingly in the total. African imports of all categories have shown a declining trend since 1960.

In recent years Latin American lumber imports have increased, to be the most important source of that product, with Brazil as the predominant supplying country. Malaysia and the Philippines are also major sources of lumber. These three countries account for two thirds of the imports. The United States has become the largest single net importer of tropical sawnwood.

Developments in imports of hardwood plywood have been dynamic. In the early 1950s, imports from Japan began to grow very rapidly and this product soon became the most important tropical wood import. By 1960, however, imports from Japan had levelled off and the trend has been strongly downward since the peak year of 1968 as Japanese domestic consumption of plywood and other wood products, as well as wage costs, increased rapidly. In the mid-1950s the Philippines, the original wood source for most of the Japanese exports, came into prominence as a plywood producer and exporter. Exports to the United States grew steadily until 1973 but then declined rapidly and are now at only one third of their peak level. This reflects both a more restricted log supply and market competition from other exporting areas.

Successively, China (Taiwan), in the latter part of the 1950s and the Republic of Korea, at the start of the 1960s, followed as new sources of plywood imports, both basing production on log imports from Southeast Asia. Imports from both countries grew rapidly until 1972 but have since declined and levelled off because of less demand. Malaysia, Singapore and, more recently, Indonesia have also become exporters of substantial amounts of plywood, but US imports from these countries have to date been relatively modest. The Republic of Korea has accounted, in recent years, for well over half of all US hardwood plywood imports.

Production of tropical logs and, even more, their exports are concentrated in a very few countries. In 1977, two only accounted for 47 percent of production and 77 percent of exports in the log form; six countries produce 75 percent of the logs.

Fifteen tropical producing countries that accounted for most of the world's production, together with another 10 or 12, include the great bulk of the tropical moist forest area and volume. These are: Indonesia, Malaysia, the Philippines, Brazil, India, the Ivory Coast, Colombia, Thailand, Gabon, Ghana, Nigeria, Burma, Madagascar, Costa Rica and Ecuador. A few in this group, including Zaire, Peru, Bolivia, Papua New Guinea and Cameroon, have considerable forest areas which, largely because of difficulties of access, have not made corresponding contributions to world production and export.

Most tropical forest countries might be classified into one of the following categories, as an indication of the state of exploitation.

1. Traditional suppliers of tropical wood. Nigeria, Ghana, Thailand and the Philippines are in this category. They do considerable processing for both domestic and export markets. Their resources for expansion are now limited and they are interested in processing for domestic needs and higher value exports only.2. More recent, but well-established exporters. Sabah (Malaysia), Peninsular Malaysia and the Ivory Coast have experienced extensive exploitation over the past decade or two for export logs. Their forests are now being systematically worked over and the remaining unexploited areas are less accessible. Their forests have fairly limited potential for future exploitation at the current rate of cutting; a decade or two, at most.

3. Countries with considerable forest areas and considerable exploitation. The level of exploitation is generally intense in accessible forest areas of the Congo, Zaire, Venezuela, Peru, Ecuador, Madagascar, Papua New Guinea, Bolivia, Cameroon, Brazil, Indonesia, Sarawak (Malaysia), Burma, Democratic Kampuchea, Guyana, Suriname and Liberia. But in all these countries there are also extensive unexploited or slightly exploited forests.

4. Essentially unexploited areas. In the Central African Republic and Lao there is as yet little commercial logging, but there is also difficulty of access.

5. Special situations. India has considerable forest under permanent management and Gabon has ready reproduction of okumé, a highly marketable species.

Unless there is a major change in the range of species and qualities reaching the market we can expect the following to occur:

· It seems clear that countries in the first group will not supply additional logs and that their export supply of tropical forest products will probably decline in volume, but not necessarily in value.· The second group will have a short continuing period of maintaining (or expanding) exports.

· Any major increase in supply and even maintenance of existing levels must depend on the third and fourth groups.

MAJOR TRADE FLOWS: Tropical Hardwood SAWNWOOD 1978 TOTAL: 3 4 million m³

Major exporters of tropical hardwood sawnwood are Malaysia, Singapore, Indonesia, the Philippines and the Ivory Coast. Major importers are the Netherlands, Italy, the United Kingdom, the Federal Republic of Germany, France, and the United States. The major bilateral trade flows are from Malaysia to the Netherlands, to the Federal Republic of Germany and to the United Kingdom, from Indonesia to Italy and from Singapore to the

Netherlands. There is also a substantial flow from Malaysia to Australia that is not indicated on the map.

Exports of sawnwood from developing countries more than doubled from 1967 to 1977. Most of this growth occurred in Malaysia, Singapore and Indonesia.

The flow from Latin America to the United States shown on the map includes some coniferous sawnwood.

An examination, country by country, of forest depletion and wood production undertaken by FAO and an outlook appraisal for the future (8) see production of logs from the developing countries' natural hardwood forests increasing from the 1975 removal level of 109 million m³ to a potential 191 million m³ in the year 2000, an increase of 75 percent. This estimate, however, assumes a much wider range of species use. Even so, some traditional exporters including Malaysia (Sabah and Sarawak included) and the Philippines, as well as several countries of West Africa, show an actual decline in estimated production. The biggest increases are estimated for the Asia and Far East region (39 million m³) and Latin America (35 million m³). Substantial increases are foreseen for Indonesia, India, Brazil and for the central African countries. In some cases a large portion of the harvest is seen as coming from forest clearing for agriculture expansion. The area of natural closed hardwood forests is estimated to decline by 65 million ha or 10 percent in the 25-year period.

It must be stressed, however, that knowledge of main areas of remaining production potential is limited and precludes any but a crude appraisal of the longer term potential. Three major countries, Indonesia, Zaire and Brazil, which account for more than two thirds of the tropical forest area, have not yet been able to assess their forest resources with appreciable accuracy.

(4References 8 and 12.)

A major factor favouring export of logs rather than veneer and plywood from the producing countries has been the tariff protection often provided to processors in the importing countries. Much of the effect of these barriers has, however, been overcome through the Generalized System of Preferences which favours developing countries. Logs and sawnwood tropical species have generally been free of tariffs. There has been, over time, a reduction in tariffs on veneers and plywood in most countries. Tariffs on veneer sheets have been removed in many cases, but may still be appreciable and as high as 37.5 percent. Plywood, again, may be free of tariffs, but rates as high as 50 percent are still in force and concessions have been less generous for this product. The rather high tariffs on veneers and plywood which the United States has had until fairly recently do not appear, however, to have greatly favoured imports of logs as compared with the processed products.

The continuing existence of mills in the importing countries which are dependent on raw materials from outside has, of course, perpetuated the flow of logs. In recent years, however, there has been less tendency to establish such mills except in a few countries of Southeast and East Asia which have had available skilled labour at relatively low wage rates.

A number of recent developments will encourage processing at source. Notable among these are restrictions on log exports. Although approaches of this sort have been used in the past, they have frequently failed because of the general availability of alternative supply sources, international competition and a corresponding lack of political solidarity. Among recent restrictive actions have been complete (Nigeria, the Philippines) or particular species (Ghana), bans on log exports and the requirement of a certain level of processing by concessionaries (Liberia, the Philippines, the Ivory Coast and Cameroon). Indonesia is now in the process of applying a quota system for exports of logs and sawnwood.

There continues to be rapid growth in consumption of forest products in most of the countries producing and exporting tropical woods. In some instances this has caused traditional exporters such as Thailand and Nigeria to reduce exports or even to import. Peninsular Malaysia must depend on imported logs if it is to maintain its existing industry, production and exports.

In the case of plywood, countries which have developed essentially as in-transit processors have shifted more and more of their output to domestic use. Already Japan consumes all but approximately 2 percent of its own production of hardwood plywood. China (Taiwan) and the Republic of Korea which in the 1960s directed essentially all their production to export are now consuming about 30 percent and 10 to 15 percent of the production for domestic consumption. Europe still exports about 30 percent of its declining production, but imports have been growing while exports have been declining with apparent consumption remaining relatively stable.

It is clear that a larger portion of output will be directed to the consumption of producing countries rather than to exports. In the case of East Asia, plywood producer-exporters will have the additional limitation emerging from restrictions on the export of logs from the basic supplying countries. These two factors will have an impact on export potentials which may seriously affect countries which have been depending on this source of supply

MAJOR TRADE FLOWS: Tropical Hardwood PLYWOOD 1978 TOTAL: 3 1 million m³

Major exporters of tropical hardwood plywood are the Republic of Korea, China, Singapore and Malaysia. Major importers are the United States the United Kingdom, the Netherlands, Belgium. and Canada. Important individual flows are from the Republic of Korea to the United States, China to the United States, Singapore to the United Kingdom, and from Korea to the United Kingdom and to the Netherlands.

The tropical hardwood plywood trade has grown very rapidly, increasing by 1977 to more than four times its 1967 level. Growth of exports has been predominantly from Asia and has been particularly rapid in Korea, Malaysia, Singapore and Indonesia.

In the second half of 1979 and early 1980, price increases in plywood that were caused mainly by increases in the prices of logs imported into East Asia have had an adverse effect on the plywood trade to North America. Domestic substitutes, particularly particle board, are replacing the imported product.

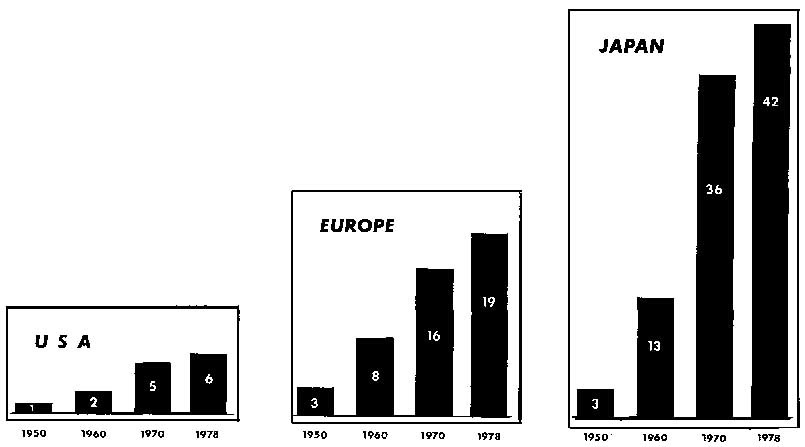

Imports of tropical hardwoods into major markets of the developed world grew rapidly from the late 1940s to 1973, declined rapidly in 1974 and 1975, but revived by 1978 to approximately the peak 1973 level. Imports of the three developed country areas in the graphs above are substantially different in nature. The imports of the United States have been predominantly in processed form, particularly as plywood. European imports were originally largely in the log form but have changed gradually until about half are now processed wood, predominantly sawnwood. Japan, however has continually imported tropical hardwood al most solely in the form of logs, until quite recently.

It requires in the range of 1.7 to 2.5 m³ of tropical hardwood logs to produce one m³ of sawnwood or plywood. The residues from this production find ready use, particularly as pulpwood or raw materials for particleboard in the Japanese and European markets.

In 1978 total imports of tropical hardwood logs by developed countries were little more than in 1970, while imports in the processed form have more than doubled. However, the processed portion still accounted for less than 40 percent of the total (in log equivalent) in 1978.

Estimates of future consumption and trade of forest products generally, and for tropical wood products in particular, have become seemingly more uncertain and extremely varied over recent years. This reflects not only the extreme fluctuations caused by the inventory building period of the early 1970s and the 1975 depression but, even more, the failure of consumption and trade to recover, especially for the mechanical forest products in many of the developed countries, much beyond the levels of the first part of the decade. Estimates made prior to the mid-decade developments are now generally considered much too optimistic but, however, neither can the common pessimism of the latter part of the decade be accepted without question. Apparent consumption in many developing countries continues to grow at a rapid pace and even in the event of a general economic slowdown in the developed countries, there remains the possibility of aggressive residential building programmes.

In The outlook for timber in the United States, published by the United States Government in 1973 (11), imports of hardwood lumber and plywood were not seen to increase rapidly under any of the alternate price development assumptions. The maximum rates of import growth estimated for these products were approximately a doubling from the early 1970s to the year 2000. Estimates by FAO (8) and the World Bank (13) have been slightly higher than this, suggesting a tripling of levels. However, a recent study provided to FAO by an industry and forestry working group, led by Crown Zellerbach Corporation, even foresees a decline to zero of net imports of hardwood sawnwood and an increase of only about 50 percent in those of hardwood veneer and plywood. (6)

The expansion foreseen for Western European and Japanese net imports by the last-mentioned study is, however, quite substantial for these products; more than doubling for hardwood sawnwood and with a sixfold expansion for solid wood panels in Western Europe, while for Japan a shift is foreseen to considerable import of these products from a position of small net imports or net export. Simultaneously, tropical hardwood sawlog and veneer log imports to Western Europe are foreseen to decline only slightly. However, those to Japan are estimated to decline appreciably, while imports to that country of softwood logs and especially of both softwood and hardwood pulpwood logs or chips will increase rapidly. Much of the hardwood would come from tropical areas.

Other studies (1, 2) suggest for Western Europe and Japan an even larger increase of tropical hardwood imports, especially to the latter.

Even at the lowest outlook level, Japan may be expected to require by 2000 at least the current level of 20 million m³, log equivalent (4.4 thousand million board feet) of hardwood sawlogs, veneer logs, sawnwood or plywood and as much as 50 million m³ or more of hardwood pulpwood or pulp products. Western Europe will probably also need at least 20 million m³ of :hardwood log equivalent (4.4 thousand million board feet) in the mechanical products and 30 million m³ roundwood equivalent (1000 million board feet) in the pulp category. Essentially all of the mechanical products must be tropical, as may be a good portion of the pulp products Other more optimistic demand out" look studies have suggested the need to import higher levels of tropical hardwood log quality products into Japan (40 million m³) (8.8 thousand million board feet) and Western Europe (35 million m³) (7.7 thousand million board feet) by 2000.

By contrast, the United States might be seen to require in these product qualities only some 5 or 6 million m³ (a thousand million board feet) log equivalent of imports (the current level) at lower estimate levels, al though as much as 20 or 25 million m³ might be needed according to higher trend estimates.

In any event, it is clear that the other major tropical wood-importing regions will continue to have much more import dependence on the tropical forest than will the United States. This is especially so because of their growing gaps between total wood demand and total domestic supply.

It seems apparent that:

- there must be a shift in tropical wood supplies to a wider range of' currently lesser used species and to those from less accessible areas;- domestic requirements of both log and plywood producing countries will increase rapidly;

- there will be a growing dependence of Japan and Western Europe on wood product imports including tropical hardwoods;

- in-transit lumber and plywood producing countries may be seriously affected by constrictions on the log supply;

- substantial price increases may be consequently expected for tropical wood products based on large logs of high quality.

All of this suggests that the United States may be facing declining supplies of hardwood plywood from its major sources. A. variety of resultant actions may be considered. For instance, there could be a concentration of imports of limited amounts of the better quality and high-priced products to serve specialized and luxury uses, and an expanded utilization of the countries' own increasing quantities of lower grade hardwood raw materials. There may also be a further shifting of purchases to the growing plywood industry of Southeast Asia. These shortages may also have the effect of encouraging and promoting production and use of tropical species not strongly in current demand. Or there may be a combination of the above three possibilities.

1. ECE/FAO. European timber trends and prospects, 1950-2000. Geneva, 1976.

2. ECE/FAO. Study on the trade and utilization of tropical hardwoods. Timber Bulletin for Europe, Suppl. 10 to Volume XXX.

3. FAO. Forestry Department. Monthly Bulletin-tropical forest products in world timber trade.

4. FAO. Statistics and Economic Analysis Unit, Forestry Department. 1978. Direction of trade in forest products-a compendium of summary tables.

5. FAO. Forestry Department. Year-book of forest products. Annual.

6. JOINT FORESTRY AND INDUSTRY WORKING PARTY. 1979. Report to FAO on world outlook for wood products and wood supply. (Not available for general distribution)

7. LANLY, J.P. & CLEMENT, J. Present and future forest and plantation areas in the tropics. FO:MISC/79/1. FAO, 1 979.

8. PRINGLE, S.L. Tropical moist forests in world demand, supply and trade, in management and utilization of the tropical moist forest. Unasylva, Vol. 28, No. 112-113. FAO, 1976.

9. STADELMAN, R.C. The United States market for tropical hardwoods. UNECE. Meeting document for seminar on the utilization of tropical hardwoods. (Restricted) Geneva, 1979.

10. US DEPARTMENT OF AGRICULTURE, FOREST SERVICE. 1977. The demand and price situation for forest products, 1976-1977. Misc. publication No. 1357.

11. Us DEPARTMENT OF AGRICULTURE, FOREST SERVICE. 1973. The outlook for timber in the United States.

12. US INTERNATIONAL TRADE COMMISSION. 1978. Summary of trade and tariff information, hardwood plywood. USITC publication No. 841, Control No. 2-3-1.

13. WORLD BANK STAFF, communications.

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}