![]()

![]()

![]()

LATIN AMERICA AND THE CARIBBEAN

The economic environment in Latin America and the Caribbean in 1995-96 has been strongly influenced by the effects of the financial crisis that took place in late 1994 in Mexico and successively in Argentina. The deep recession that followed the crisis in these two countries was largely responsible for a significant slow-down in the region's rate of GDP growth. The reduction of capital flows to the region was not as pronounced as initially feared, however; growth in most other countries slowed only slightly, inflation continued to decline - with the major exception of Mexico - and exports remained buoyant. Nevertheless, there are concerns over current account deficits which, particularly in Brazil, have reached extremely high levels, as well as over the sustainability of capital inflows, competitiveness problems linked to currency overvaluation and the deteriorating social conditions in several countries. In this general context, the performances of regional agriculture have remained disappointing despite remarkable success stories, particularly in the agro-export sector, in some countries.

After a healthy 3.6 percent average annual economic growth rate between 1991 and 1994 - with the 5 percent of 1994 being the highest since the late 1970s - the region's economic growth slowed sharply to less than 1 percent in 1995. The financial crisis and measures to reduce macroeconomic imbalances and regain international credit resulted in strong economic recession in Mexico (-7 percent) and Argentina (-4.4 percent). Uruguay also experienced a reduction in economic activity that was caused mainly by the growing interdependence with the Argentinian economy within the framework of the Southern Common Market (MERCOSUR). In Brazil, on the other hand, the remarkable success of the Real stabilization plan favoured a substantial reactivation of the productive activity in 1994 and 1995. Although lower than the previous year, GDP growth was still a healthy 4.2 percent in 1995, thanks in particular to very good performances in the agricultural sector. Estimates for 1996, however, point to a significant deceleration in Brazilian growth, to 2 percent or less, with agriculture being again a major, this time negative, factor in the overall performance. Venezuela recorded a slight improvement after the deep recession of 1994 which reflected favourable results in the oil sector. Chile and Peru achieved growth rates above 7 percent.

Growing unemployment and lower real wages were recorded particularly in Argentina, Mexico and Uruguay. The need to respond to the financial crisis forced Argentina and Mexico to implement painful fiscal adjustments including substantial rises in taxes and public-sector service fees and, in the case of Argentina, public-sector wage cuts. These measures had the inevitable effect of aggravating situations of poverty and social tension.

From 1994 to 1995 the average regional inflation rate fell from about 337 percent to 25 percent, the lowest in 25 years. Such spectacular progress reflected mainly the success of anti-inflationary policies in Brazil, strict monetary management in Argentina and other successful stabilization efforts throughout the region. By February 1996 the annual inflation rate in Argentina had fallen to a negligible 0.3 percent and the monthly rate in Brazil to 0.7 percent, the latter being the lowest in over 20 years. In Mexico, by contrast, the financial crisis and new peso devaluation caused an upswing in inflation to 52 percent in 1995. Venezuela's inflation was also around 50 percent.

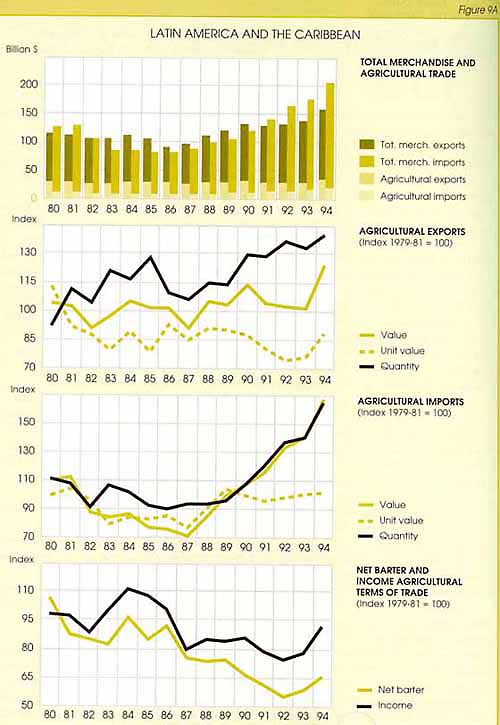

In the external sector, a significant improvement was achieved in the trade balance, with the region recording a US$8 billion surplus in 1995. This was the result of a 13 percent increase in real exports, with those of Argentina rising by 30 percent and eight other countries in the region reporting rates of over 10 percent. Improvement in the export performance was caused largely by higher commodity prices, in particular for copper, cotton, wheat and wool, which enabled a improvement of nearly 2 percent in the region's terms of trade. In the case of Mexico, the gains in competitiveness brought about by devaluation strongly boosted exports and this, together with a contraction in imports, contributed to a virtual balancing, by end-1995, of the previous large deficit in current accounts.

Agricultural performances and issues

For the region as a whole, agricultural (crop and livestock) production was estimated to have increased by 1.8 percent in 1995, a significant drop from the 4.0 percent growth recorded the previous year and only slightly better than the mediocre average growth of 1.4 percent during 1990-94. This overall result stemmed from widely varying country situations. Among the largest producers, output in Argentina rose by 5.5 percent in 1994-95, having stagnated since the early 1990s. This increase was the result, in particular, of good rice, wheat and sunflower crops. The recovery was short-lived, however, and agricultural output was expected to fall in 1995-96 after the worst drought for 20 years affected extensive agricultural areas of the country in 1995. Agriculture was also hit by higher credit costs in the aftermath of the financial crisis. While the international competitiveness of Argentinian agriculture continued to be negatively affected by the peso overvaluation, the elimination of export taxes provided compensation to exporters. Among the main export items, the market outlook for meat appeared especially bright in view of the progress achieved in eradicating foot-and-mouth disease, increased demand for Argentinian meat in Europe following concerns over "mad cow disease" and preferential access to Brazilian markets in the context of the MERCOSUR agreement. The prospects for grain exports also appear favourable in view of the current tight international market situation and high prices for these products.

In Brazil the stabilization plan seems to have had negative effects on the agricultural export sector because the ensuing currency overvaluation and credit tightness coincided with weak prices for some important export products. Agricultural production was expected to decline by about 5 percent in 1996, largely reflecting credit restrictions introduced the previous year, having expanded by about 6 percent in 1995. Cereal and oilseed output were expected to fall by 10 percent in 1995-96, while meat production was expected to increase significantly.

In Chile, the agricultural sector continued to show strong dynamism, particularly export crops, led by forestry products and pulp for paper. In 1995 the sector increased by 5 percent despite a winter drought. A key factor in the expansion of agriculture was the strong rise in prices, in particular of fish-meal, which rose by over 20 percent, and woodpulp by over 60 percent relative to the previous year. For the first time, exports of forest products exceeded traditional agricultural exports, while the area under commercial forest plantations continued to expand, partly at the expense of traditional crop area. Production and trade of fresh and processed fruit also remained dynamic.

In Mexico the economic and financial difficulties and depressed internal demand, along with a severe drought in the northern parts of the country, resulted in severe production shortfalls, particularly for cereals and oilseeds. Restrictive monetary policies led to a 36 percent decline in total agricultural financing during the first months of 1995. Interest rates rose to exceptionally high levels before stabilizing at 30 to 40 percent by the end of the year. The peso devaluation favoured exports of vegetables and fruits, which had already been enjoying good competitive positions in international markets, but also resulted in higher costs of, and reduced demand for, imported inputs.

The agricultural sector in Peru continued to show dynamism, despite a marked slow-down from the 14 percent growth recorded in 1994, thanks to good climatic conditions, a strengthening in internal demand and an improved environment for investment. Potatoes, sugar, coffee and livestock products had the strongest production performances, while rice crops declined. In the case of potatoes, good production conditions actually led to some overproduction and depressed prices, damaging small producers and emphasizing the need for better crop programming and management, market information and crop diversification.

In Cuba, reform measures contributed to the revival of a number of subsectors including meat, tobacco and vegetables, which showed booming performances in 1995. The key sugar-cane sector is facing a deep crisis, however, with production in 1995 having fallen to 3.3 million tonnes, the lowest in decades. Shortages of machinery and fertilizers, as well as labour problems during the harvest period, contributed to the crisis.

Agricultural performances in the Central American and Caribbean subregions ranged from mediocre to poor in most countries. Indeed agricultural production in 1995 fell from the previous year's level in Antigua and Barbuda, Belize, Cuba, El Salvador, Dominica, Haiti, Panama and Trinidad and Tobago, although in the latter country the decline took place after an exceptionally favourable crop year in 1994. Only a few countries, including Guyana, Guatemala, Honduras and Nicaragua, achieved agricultural production increases significantly above population growth. Such generally disappointing performances occurred against the background of already poor trends since the early 1990s. (The experience of Central America is discussed in The State of Food and Agriculture 1995.)

The role of agricultural policies

Agricultural policies in the region have been strongly influenced by the general economic policy environment. In general, the process of agricultural market liberalization and external opening has been pursued, but with varying degrees of policy commitment ranging from the example of Argentina, where the process has been radically pursued, to that of Venezuela where state intervention in market and pricing mechanisms has remained significant.

In the case of Argentina all forms of subsidies, market intervention and export taxes were eliminated. Only minor support measures to agricultural production subsisted, such as a special credit line introduced in mid-1995 through the national bank for financing oilseed and maize crops, although at conditions close to those of the market. Such measures were intended to ease the credit shortages and high lending costs arising from the rigid financial control policy. The other remaining form of direct support is a special fund for tobacco production, although its elimination is also under discussion.

In Brazil, one of the elements of the ongoing stabilization programme has been the replacement of the old system of indexed interest rates by a system of variable interest rates, which are also applicable to agricultural loans. Following the dramatic abatement of inflation, interest rates declined by half, but many farmers still considered agricultural credit availability too limited and its cost too high. New loans at fixed interest rates have been created for maize production, however, and special lines of soft lending have been introduced for small farmers and selected products (cotton, rice, manioc). Moreover, the government requests the banks to devote part of their portfolio to agriculture and is also pressing large producers to enter commodity futures markets. Support to the Real resulted in currency overvaluation which reduced external competitiveness for exports and created greater incentives for imports. This caused protests from agricultural producers, especially because compensation from subsidized support programmes were no longer available. Complaints were also raised about the high taxation of primary product exports, which diminishes according to the product's degree of processing. The harmonization of phytosanitary regulations and the adoption of common tariffs under the MERCOSUR agreement have represented enhanced opportunities but also challenges to the competitiveness of Brazilian products. Tariffs have been reduced to an average 20 percent, although for some products they were raised; in the case of rice, for example, from 10 to 20 percent. For the first time, cocoa will be imported in competition with local production.

Agricultural policies in Chile include support for some products, credit for disadvantaged farmers, export promotion and investment in infrastructure and services for agricultural production and marketing. In particular, support measures were introduced or strengthened in response to the competitive losses associated with currency appreciation since end-1994. Among the most significant measures were the establishment of an export promotion fund with an initial US$10 million capital and the introduction of additional duties on imports of some products, including wheat, sugar and vegetable oils, when prices fall below predefined levels and during certain periods of the year. A number of phytosanitary restrictions are also applied on imports. Chile has a diversified tariff system that varies according to the existing agreements with trading partners. A recent study by agricultural entrepreneurs concluded that the entry of Chile to the North American Free Trade Area (NAFTA) and MERCOSUR would reduce traditional crop production significantly. MERCOSUR would have negative effects on Chilean agriculture overall, while NAFTA would benefit exporters, especially of processed products.

An issue of considerable concern in Chile is forest management. A recent study by the central bank estimated that, at the current rate of deforestation, only half of the current 7 million ha of forest land will subsist over the coming 25 to 30 years. The results of the study have been challenged by industrial organizations. Another study, sponsored by the French forest agency, concluded that under current rates of exploitation all perennial tree species will have disappeared in 30 years. The seriousness of the problem prompted the government to introduce new legislation to regulate forest exploitation.

The entry into force of NAFTA has considerably influenced agriculture in Mexico. Trade liberalization under the Agreement had resulted in a 17 percent increase in agricultural imports from, and a 7 percent increase in exports to, the United States in 1994. The financial crisis and devaluation of the new peso radically changed the picture; in 1995 agricultural exports to the United States rose by 35 percent, and imports fell by a similar amount. Along with the process of tariff elimination, for which a 15-year transition period has been established,29 negotiations have been pursued on the harmonization of phytosanitary and labelling standards.

After a probationary period, the Procampo programme of direct income support to farmers, which replaced the old system of price support, entered a permanent phase of implementation in 1995. It recognized a contribution per hectare (440 pesos in 1995) and according to type of product (grains, cotton, rice). The government also announced a new scheme to restructure agricultural debt in the face of problems arising from the financial crisis, although such a scheme may involve public expenditure costs and inflationary pressure.

Following the presidential elections in April 1995, the Government of Peru has adopted important measures in favour of agriculture. In July 1995 a new landownership law was promulgated that was expected, inter alia, to provide a better climate for credit and investment. At the same time, new regulations were issued to protect small farmers and indigenous communities who had, or were at risk of having, their land occupied by other groups. New legislation was also being studied to reduce the inefficiencies and abuses that characterize water use through the sale of utilization rights. A new law was also being discussed in Parliament that aimed at environmental protection as well as addressing employment and investment concerns. The introduction of an 18 percent tax on the sale of agricultural inputs has been the object of intense debate. The Ministry of Agriculture is undertaking a major programme to regularize landownership titles, which will enable landownership to be used as collateral for agricultural loans. Inadequate credit availability is, indeed, a major limiting factor to agricultural development in Peru. The government offers special credit lines for the purchase of inputs, but their scope is inadequate to meet demand. Some agricultural associations have proposed the creation of a rural bank to complement the role of existing rural financing funds by offering long-term credit. Another government initiative, so far little used by farmers however, has been the establishment of a market information network.

Agricultural policies in Venezuela differ from those in most other countries in the region in that they have maintained a strong interventionist and protectionist character, despite various attempts at liberalization between the years 1988 and 1993. New legislation for agricultural development is currently under discussion to provide the legal framework for agricultural policies in the coming ten years. The general aim is national self-sufficiency in food, to be achieved through various mechanisms of state protection of the sector. Temporary foreign exchange control measures, aimed at limiting imports, were being applied in 1995. A number of import priorities were established, including some essential foods and inputs for agricultural and agro-industrial production. A price band system was adopted in May 1995 in line with Andean Pact (AP) provisions and aimed at stabilizing domestic market prices and ensuring a certain protection to agricultural producers when international prices fall below predetermined levels. Rigid phytosanitary controls and regulations, implemented on the basis of over 300 obligatory standards, have been established by the competent agency as a means of regulating imports. Price controls on over 120 consumer items, including foodstuffs, have been enforced since 1994. Attempts were made in 1995 at liberalizing prices within the framework of an anti-inflationary pact between the government and enterprises, but these did not reach any concrete result. One of the most important programmes of government support to agriculture concerns debt refinancing at subsidized interest rates. In addition, subsidies are granted for the purchase of food by poor and vulnerable groups (schools, children, lactant mothers). In December 1995 a new pilot programme was introduced in five cities to enable poor population groups to purchase essential foods at prices below those officially controlled.

In Cuba, the government has been pursuing economic reform slowly, within a context of major economic and financial difficulties. An important element of the reform in agriculture has been the accelerating decollectivization of the land. Less than one-third of the cultivatable land remains under state farms (about three-quarters in the early 1990s), the rest having been progressively allocated to various forms of cooperatives and private small farms. While the state still provides production requisites on preferential terms and establishes production quotas for public procurement, the private sector is allowed to sell any amount of production in excess of the quota on the free market.

The outlook for the region's agriculture will be largely determined by the ability to overcome the problems and uncertainties that cloud the macroeconomic environment. The severe shock represented by the Mexico crisis showed, on the one hand, considerable resilience within the region's economies, in sharp contrast with the events that followed the crisis of the early 1980s. On the other hand, it also underlined the risks involved in capital flow volatility and the importance of maintaining international confidence through unflinching commitment to economic stability and reform. If the region's economies emerged relatively unscathed from the recent crisis it is to a large extent because Argentina and Mexico, as well as some other countries, proved such a commitment to exist. In addition, two major elements of the reform effort played an important role: the economic opening, which enabled exports to become central parts of the post-crisis adjustment; and the economic liberalization and integration, notably within the NAFTA and MERCOSUR agreements, which proved to be major elements of stability.

While the need for pursuing and deepening economic reform is beyond question, there are, however, elements of the process that raise concern, notably for agriculture. The actual or perceived consequences of the deregulation of the agricultural and rural economy are subject to considerable controversy. One theme fuelling the debate is the disappointing performance of the agricultural sector since the early 1990s, in coincidence with the accelerated process of market liberalization. The 1990s have witnessed significant improvements in average yields, which have risen by 3.3 percent per year compared with 1.3 percent during the 1980s; the cultivated area, however, far from expanding as it did during the 1980s, has declined by 2.2 percent annually, the result being a 1.4 percent annual increment in production. This rate of growth, below even that of the depressed 1980s (2 percent), is clearly insufficient to allow agriculture to contribute adequately to the food security and economic growth of the region. Obviously, such overall mediocre performance reflects many factors not necessarily related to the reform but, as reviewed above, a number of features stemming from recent policies - such as overvalued exchange rates, the reduction of public support, higher credit costs, and the overall demand-compressing effects of fiscal and monetary restraint - have undoubtedly played an important role.

Another debated issue is the extent to which economic liberalization has contributed to accentuating income inequalities, overall and in rural areas. Economic Commission for Latin America and the Caribbean (ECLAC) estimates suggest that the already notoriously unequitable income distribution patterns in the region have tended to get worse in many countries throughout 1980-1992. How this phenomenon has affected the rural sector in recent years has not yet been fully assessed, but evidence points not only to an accentuation of income inequality, but also to cases of growing pauperization in rural areas, where over half of the people live in absolute poverty. This is largely attributable to the deregulation of the rural economy which favours primarily the larger producers and traders who already enjoy conditions of competitiveness and are better able to capture the opportunities offered by unrestricted markets. By contrast, the progressive retreat of the state has translated into serious problems for large segments of the traditional peasant sector for whom economic viability was strongly linked to state support. The recent financial difficulties faced by several countries further restricted the ability to help small producers in such areas as technical assistance, credit and debt alleviation.

These features underline how difficult it is to find a policy blend that simultaneously addresses the needs to consolidate macroeconomic stability, resume sustainable growth and share equitably the benefits of growth among all segments of society. Furthermore, they point to the need for coherent policies to facilitate an orderly transition to a deregulated rural economy. Such policies should encompass restructuring of factor ownership in conditions that ensure equitable sharing of resources, safety of investment, dynamism of land markets and efficient use of resources. Experience has shown, most recently in the example of Peru, that this form of policy action can compensate effectively for the reduction or elimination of previous forms of direct support. At the same time, fiscal policies should orient economic activity towards rural areas with productive potential. Such policies are needed in order to avoid a process of rural transformation that merely takes the form of an abandonment of the land.

In a region where economic volatility is the norm, Colombia stands as an island of relative economic stability. This result is a consequence of decades of prudent and stable fiscal, monetary and foreign exchange rate policies. Such policies have kept the economy insulated from the great booms and recessions experienced by other Latin American countries. As a result, the Colombian economy remained virtually unaffected by the debt crisis of the 1980s displaying instead the region's highest growth in GDP for that decade.

Stability in economic performance has been achieved simultaneously with substantial changes in economic structure. After a large coffee boom in the mid-1970s, economic growth was led by the service sectors of the economy until 1982. In the 1980s, the mining sector accelerated dramatically, as a consequence of important findings of coal and petroleum. In the latter half of the decade, after a mild macroeconomic adjustment programme, agriculture and manufacturing both outpaced the service sectors, spurred by the devaluation of the real exchange rate.

From 1986, a new attitude of "internationalization" of the economy took form in a programme of gradually increasing exposure to world market forces. The pace of the programme accelerated rapidly in 1990, when major economywide reforms were announced as part of the apertura (opening) of the economy. Apertura was the Colombian version of the programmes of trade liberalization and increased reliance on market forces that took place throughout the region from the mid-1980s onwards. In Colombia, the reforms were presented as the antidote to slowing rates of productivity growth recorded in several sectors during the 1980s and to the limitations stemming from the relatively small size of the domestic market.

The economy responded well to the new policy regime. Rates of growth have surpassed 5 percent per annum since 1993. Private investment increased to record levels and unemployment has exhibited a continuous decline since 1990. However, some of the reforms posed difficulties in certain sectors that had traditionally been protected from world market volatility, including tradable agricultural crops. Falling profitability in these sectors was exacerbated by the appreciation of the exchange rate caused by the massive inflow of capital from abroad attracted by high domestic interest rates, the discovery of large oil reserves and increased confidence in the economy.

Agriculture as a whole benefited from trade liberalization, since import barriers for manufacturing had traditionally favoured the allocation of resources to non-agricultural activities. Nevertheless, immediately after the trade and marketing reforms, many tradable crops suffered a sharp fall in profitability as a result of lower tariffs, falling world prices and an appreciating exchange rate. On the other hand, non-tradable crops such as tubers, vegetables and meat products benefited greatly from increased domestic demand and new intraregional trade opportunities with Ecuador and Venezuela, albeit after suffering harvest losses during the intense drought of 1991-92. The negative results of 1991-92, however, turned farmer opinion against the reforms and generated pressures for compensatory measures.

Since 1993, planted areas and production levels have displayed uninterrupted growth, partly as a result of the implementation of emergency government measures, better meteorological conditions and increasing international prices. In spite of the rapid growth of agricultural imports, after the adjustment to lower real prices, domestic producers are now in a better position to compete with foreign suppliers. Public and private efforts have concentrated on carrying out the research and infrastructure development required to guarantee long-term profitability. As a result, Colombian agriculture is better prepared to face the challenges of the next century than it was before 1990.

Economic setting: 1985-1990. After a period of recession and growing economic imbalances since 1981, the Colombian economy was subjected to a mild adjustment programme starting in 1985. Public expenditures were reduced, the tax burden was increased and measures to devalue the exchange rate were put in place in order to correct the overvaluation accumulated since the late 1970s. As a result of these measures, the fiscal accounts improved rapidly and the current account switched from a deficit in 1985 to a surplus by 1986. GDP growth strengthened to an average 4.4 percent per annum in the 1985-89 period, after having grown at only 2.5 percent per annum from 1980 to 1984.

Export growth was particularly rapid in the second half of the 1980s, generating a sizeable trade account surplus as a result of favourable terms of trade and devaluation of the real exchange rate (after falling by 20 percent in 1985, the real exchange rate continued to depreciate at an average rate of 4.5 percent annually until 1989, when it was further devalued by 13.5 percent). As a consequence, non-traditional exports grew at an annual rate of over 20 percent. Export growth was further enhanced as from 1988, when measures were taken to implement a plan of internationalization of the economy.

The new policy framework: apertura policies. In August 1990, the pace of liberalization was quickened with the announcement of structural reforms in the trade, financial and foreign investment regimes. These measures were followed, over the following three years, by the passage of new legislation pertaining to, among others, foreign exchange, monetary and labour regimes.

On the trade front, the gradual liberalization process that commenced in the final years of the 1980s was accelerated in 1990. In that year, import quotas and other trade restrictions were abolished. A timetable for tariff reduction over a three-year period was announced, although its targets were met in less than 24 months. Tariff rates were reduced from 36.3 percent in 1990 to 11.6 percent in 1993. Additionally, an aggressive agenda of trade negotiations led to special agreements with Venezuela, Ecuador, the Andean Pact, G3 (Mexico, Venezuela and Colombia) and Chile. Colombia also benefited from the Andean Trade Preferences Act granted by the United States in 1992, which allows most Colombian goods tariff-free access to the United States market until 2001. A similar scheme was negotiated with the European Union (EU), with preferences lasting until 2004.

A new financial regime was approved in 1990, designed to stimulate competition and the entry of new participants, including foreign investors, into the financial services arena. Under the new scheme, the segmentation of financial markets into specialized institutions was replaced by universal banking provisions. Forced investments were reduced and the government announced a rapid timetable for the privatization of a number of state-owned banks. The new regime also strengthened banking supervision norms and increased capital standards to international levels.

Provisions limiting the presence of foreign interests in the Colombian economy, which had been established in the early 1970s, were eliminated in 1990. Controls on foreign investment were lifted for most areas of the economy and investors from abroad were guaranteed equal tax treatment. Controls on remittances were also relaxed.

In 1991, controls on the capital account were abolished and Colombian nationals were allowed to contract debts directly from foreign lenders. The monopoly on transactions in foreign exchange held by the central bank was abolished and the market for foreign currency was transferred to the private financial system. The "crawling peg" regime of exchange rate management was replaced at the end of 1991 by a "dirty" float and, since 1994, a pre-established band has been in operation in order to allow greater influence of market forces in the determination of the price of the currency.

The labour reform of 1990 removed uncertainties about the costs of hiring personnel and made contracting procedures more flexible. The social security system was changed in 1993 from a pay-as-you-go system to one of private capitalization. The new legislation expanded coverage of pension and health benefits to a greater share of the population and allowed private pension funds to compete with the public agency in charge of social security. In addition, a new universal health system was introduced, according to which all workers are entitled to a mandatory health plan, to which they must contribute 12 percent of their wages.

In 1991, a new constitution made the central bank independent from the executive branch. The mandate of the new monetary authority emphasizes inflation reduction goals. The focus of monetary policy shifted from the growth of monetary aggregates to regulation of interest rates through open market operations. The constitution also mandated an ambitious fiscal descentralization regime, with increasing shares of central government revenues transferred to local levels. To compensate for revenues lost through these transfers and from the lowering of tariff rates, the income, sales and gas tax regimes were modified in 1992. The government achieved a neutral fiscal stance in the 1990-94 period, reflecting the high priority awarded to maintaining macroeconomic stability.

Performance. In spite of fears of an economic crisis as a result of the trade liberalization, the Colombian economy performed surprisingly well in the 1990-95 period. GDP growth increased continuously from 2.0 percent in 1991 to 5.7 percent in 1994 and 5.3 percent in 1995. After falling in real terms in 1991, investment grew at an average real rate of 19.0 percent in the 1992-94 period, spurred by the lower costs of capital goods brought about by tariff reductions, the appreciation of the exchange rate and confidence in the future of the economy. Urban employment increased at a fast pace, offering job opportunities to the growing labour force and reducing the levels of unemployment and informality of employment.

As a result of the appreciation of the exchange rate (discussed below), the fastest growing sectors of the economy were concentrated among non-tradables. Aggregate economic activity was led by growth in construction of urban housing, oil and coal production, public and private services and financial activities. In agriculture, production levels of meats, vegetables, tubers, sugar and oil-palm exhibited the highest rates of growth.

In contrast with the 1985-89 period, the exchange rate appreciated by 13 percent between 1990 and 1994, in response to the increasing inflows of foreign exchange. The causes of this phenomenon have been a subject of heated debate among Colombian economists. Among the factors that seem to have played an important role were an increased confidence about the future of the Colombian economy after the structural reforms, the difference between internal and external yields on short-term investments and the doubling of known oil reserves. This last factor was a result of the massive findings of high-quality crude in the Cusiana and Cupiagua oilfields in 1992, which increased known oil reserves from 1.8 billion to almost 4 billion barrels.

The appreciation of the exchange rate was accompanied by a surge in imports, which grew at real rates of over 40 percent in 1992 and 1993. Export performance suffered from falling profitability and low international prices, particularly in traditional areas such as coffee. As a result, the current account switched from a surplus of 5.6 percent of GDP in 1991 to a deficit of 4.5 percent in 1994.

Policies 1994-1995. In August 1994, the incoming administration reaffirmed its broad commitment to furthering the reforms initiated in 1990, including the trade liberalization. However, a new emphasis was laid on arresting the exchange rate appreciation process and on using growing tax revenues from oil production to raise spending on social programmes and infrastructure. Employment generation is also an important objective, to be promoted by public programmes that foster the development of small private-sector enterprises.

In spite of growing political uncertainties, GDP growth was 5.3 percent in 1995, the result, in great part, of large increases in oil production and government services. The central bank applied a tight monetary policy in order to neutralize inflationary expectations in the context of a more active fiscal policy. Strong signs of an economic slow-down were evident in the second half of the year and growth is expected to decline for 1996.

Sectoral policy changes and performance

The role of agriculture in the economy. In Colombia, agriculture has traditionally accounted for a higher share of GDP than in most economies of the region. This share was about 19.9 percent of GDP in 1980; a result that is associated with the large natural endowment of lands suitable for agricultural cultivation and with the absence of alternative sources of foreign exchange such as oil or other minerals. By 1990, the sector still accounted for nearly 17 percent of GDP, with nearly 25 percent of the population still living in rural areas. About 20 percent of the labour force is employed in the agricultural sector.

As a result of widely differing agro-ecological conditions and land tenure structures, Colombian agriculture is highly heterogeneous. Exportables account for about 30 percent of the value of production and include a smallholder crop, such as coffee, and several plantation crops, such as bananas, flowers, sugar and cotton. Importable crops contribute nearly 35 percent of the value of agricultural production and include those produced by minifundia farmers (barley, wheat, maize) as well as cereals and oilseeds grown in medium- and large-sized farms (sorghum, soybean, oil-palm). Traditional non-tradable items account for about 45 percent of agricultural GDP and include the large-farm dominated livestock sector, as well as vegetables, fruits, tubers and other staples produced in small operations.

The share of GDP accounted for by agriculture has been declining over the past three decades. The sector grew at an average annual rate of only 1.6 percent in the 1980-84 period, as a result of falling prices, an appreciating exchange rate, declining public-sector investments and growing rural violence. However, sectoral growth more than doubled to 3.7 percent from 1985 to 1989, as a result of higher prices, a depreciating exchange rate and policies that protected producer prices by restricting food imports. In particular, the sector benefited from the Plan de Oferta Selectiva (selective supply plan), implemented in 1988 and 1989 to promote production of cereals and oilseeds by guaranteeing high prices to producers.

The growth pattern of Colombian agriculture has entailed more intensive use of land and capital than labour. Employment opportunities in agriculture have not grown significantly since the 1960s, a result of policies oriented towards fostering the subsectors of livestock and mechanized large-farm operations. The bias has been implicit in the pattern of public investment in agriculture, the orientation of the trade regime and the allocation of subsidies.

Apertura measures. Sectoral policies changed dramatically as part of the economywide programme of trade liberalization implemented since mid-1990. The new regime removed the emphasis from the need for sectoral policies, focusing instead on establishing a neutral macroeconomic environment that would allow sectors with comparative advantage to flourish. It was argued that agriculture would benefit because of the overwhelming resource advantage and the removal of the traditional policy bias in favour of manufacturing.

The largest policy shift came in trade-related policies. Import restrictions were eliminated, including the government monopoly on imports of most grains and oilseeds. Tariffs on farm goods were reduced sharply from an average of 31 percent in 1991 to 15 percent in 1992. In the same period, tariffs for agricultural inputs fell from 15 percent to 2 percent. Some importable crops (rice, maize, sorghum, soybean, wheat, barley and milk) and one exportable (sugar) were granted exceptional treatment through a variable tariff system linked to a price band system. This system was designed to filter out large swings in international prices, providing only medium- and long-term market signals to local producers.

The direct intervention activities of the public agency in charge of agricultural marketing, IDEMA, were sharply curtailed. Purchases were restricted to marginal areas where farmers faced severe difficulties in taking their crop to market. Public stocks of grains were drawn down. Guaranteed producer prices for grains and oilseeds were replaced by minimum prices set according to recent world market trends. These measures were complemented by the elimination of all consumer price controls.

A special programme for the modernization and diversification of lagging sectors was designed in 1991. The aim of the programme was to cushion the blow of external competition and help accommodate required resource shifts in certain crops where local farmers were especially uncompetitive. The programme focused on four smallholder crops (wheat, barley, dark tobacco and fique, a type of jute). It included technical assistance, temporary price supports and the encouragement of alternative crops. In practice, implementation of several key components of the programme was delayed and this was later blamed for some of the difficulties faced by farmers in 1992.

Special attention was given to opening new markets for Colombian crops through trade agreements. Many non-traditional agricultural exports benefited from the trade preferences obtained from the United States and the EU. The enhanced integration with Andean Pact nations opened new possibilities for farmers because Colombia enjoyed greater comparative advantages in agriculture than other Andean partners. Some of the potential gains from greater trade within the Andean Pact, however, were thwarted by the lack of harmonization among member countries in their respective systems of price bands for importable crops.

Agricultural credit reforms initiated in 1989 were aimed at increasing the volume of resources available to farmers by creating a new rediscounting fund, FINAGRO, and increasing market forces in the determination of the cost and destination of credit. FINAGRO sought to supplement the banks' own funds for medium- and long-term investment credit. Starting in 1990, interest rates for medium- and large-scale farmers were increased to market levels. A four-year schedule was announced for the liberalization of interest rates on loans to smallholders. In spite of these measures, credit flows to farmers were severely disrupted from 1991, when accumulated losses of Caja Agraria, the agricultural development bank, paralysed the issuing of new loans.

In the 1990-94 period, a number of significant reforms were also undertaken with respect to key aspects of sectoral policy. A new policy for public support for irrigation investments was designed in 1991 to increase the role of the private sector in building and maintaining irrigation districts. A ten-year plan was adopted to increase public support for irrigation and drainage investments, with emphasis on large-scale projects.

Agricultural research responsibilities were transferred from ICA, a public agency, to CORPOICA, a new corporation created with public and private funds. The aim was to increase private-sector participation in the definition of research priorities and funding. The reform was complemented by the creation of many crop-specific funds, financed by contributions from farm revenues. The main objectives of the funds were to sponsor research and to promote better marketing practices. Responsibilities for extension and technical assistance for small farmers was transferred from central agencies to municipal governments.

Land reform policy underwent a radical change with the approval of legislation to use state funds for direct subsidies to beneficiaries, who are now responsible for selecting the plots of land that they wish to acquire. Participation of the state agency (INCORA) is now limited to selecting beneficiaries, overseeing private negotiations and price levels and providing some technical assistance to beneficiaries. The design of detailed norms to regulate the private negotiation process delayed the application of the new methods until late 1995, when the first direct acquisitions by beneficiaries were announced.

To complement the implementation of the sweeping reforms outlined above, several sectoral agencies underwent radical reforms; these included the irrigation agency (INAT), the research and sanitation control body (ICA), the land reform institute (INCORA), the marketing parastatal (IDEMA) and the integrated rural development fund (DRI). In addition, the Ministry of Agriculture and its natural resources agency (INDERENA) transferred their functions in the protection of natural resources to the newly created Ministry of the Environment in 1993.

Reforms and agricultural performance. Starting in the second half of 1991, production levels for a number of important subsectors of Colombian agriculture, chiefly import crops (cereals and oilseeds), fell precipitously. Depressed prices for export crops also contributed to the crisis, which deepened in 1992 when agricultural GDP fell by 1.5 percent. Many farmers then turned against government policies and discussion about the causes of the crisis generated a national debate. Associations of grain and oilseed producers blamed trade liberalization and the withdrawal of marketing support from IDEMA. The government argued that the crisis was caused by the effects of drought and the collapse of international prices, factors that were out of its control.

While still controversial, it seems that the factors behind the reduced harvests and/or profits of 1991-92 varied depending on the crop under question. For coffee and cotton, collapses in world prices were the critical element (coffee crops rose strongly from 1989 to 1993), perhaps compounded by the early stages of the appreciation of the exchange rate. Falling producer revenues for wheat, barley, rice, maize, soybean, oil-palm and sorghum seem to have been the combined result of the effect of the marketing reforms on producer prices and poor harvests caused by the most intense drought in three decades, which affected most of the country in late 1991 and 1992. Real producer prices fell in response to the combination of falling world prices, an appreciating exchange rate and increases in protection that were not sufficient to counteract the above factors. The shortfall in production caused by the drought seems to have been the determinant factor of the reduction in farmer income for vegetables, fruits and tubers. The only major production line that showed excellent conditions of production and profitability throughout 1990-95 was sugar. As a consequence of the crisis, aggregate rural incomes fell by 15 percent between 1990 and 1992.

Using general equilibrium analysis, it has been estimated that the decline in world prices and the relaxation of domestic agricultural price supports explained 70 percent of the observed deterioration in rural incomes. By contrast, trade liberalization benefited both rural and urban populations, raising farm revenues and promoting a more equitable income distribution.

The developments of 1991 and 1992 took a heavy toll on the living standards of the rural population. The share of the rural population living in absolute poverty increased from 26.7 percent in 1991 to 31.2 percent in 1992. The difference between rural and urban wages, which had been declining almost uninterruptedly since the early 1970s, increased substantially. After growing by 4.1 percent annually between 1988 and 1991, rural employment fell by 3.7 percent in 1992, representing a loss of some 200 000 jobs. Overall unemployment rates did not change considerably, because there was a decrease in participation rates combined with an increase in migration to urban centres, where the construction sector offered employment opportunities to displaced rural workers.

Agricultural trade patterns were greatly affected by trends in the exchange rate and international prices. Exports, excluding coffee, reduced their rapid expansion rate of the late 1980s, growing in value by 15.7 percent annually between 1990 and 1992. By contrast, the removal of import restrictions and the rapid growth of domestic demand resulted in accelerating agricultural imports, which grew at a rate of nearly 30 percent per year between 1990 and 1992.

Reactivation measures: 1993-1995. The extent and magnitude of the deterioration of rural incomes in 1992 exacerbated tensions between some farmer groups and the government. Producers of crops most affected by the crisis demanded an end to all trade liberalization measures and the provision of direct subsidies. Others supported the reforms but called for temporary measures to alleviate the effects of the crisis.

Starting in mid-1992, the government adopted ad hoc emergency measures that were consolidated into a reactivation plan by early 1993. This plan included a number of emergency trade-related measures, such as modifications to the price band scheme to increase protection levels moderately. Purchases of grains and oilseeds by IDEMA at above-market prices were resumed. An emergency employment programme was implemented, focused on areas where job opportunities had been most dramatically reduced. Regions receiving the most attention were those infested with coffee-borer and those where cotton plantations had been replaced by livestock grazing operations. Emergency credit measures were adopted to refinance overdue debts in crops affected by the crisis and provide government funds to an insolvent Caja Agraria. Public investment levels in agricultural agencies were also increased sharply.

In late 1993, tensions between the government and farmer groups led to the passage of a new General Agricultural Development Law by a Congress sympathetic to the interests of producers. Arguing that rural violence justified special treatment for agricultural production, the new legislation supported more active government marketing efforts; stronger countervailing and antidumping duties action to prevent the entry of subsidized food imports; the creation of commodity stabilization funds;

the provision of loans for agriculture at below-market costs; and funding for an agricultural insurance scheme. The law also created a new investment subsidy scheme to support rural capital expenditures by the private sector. A fund (EMPRENDER) was created to stimulate the creation of

new marketing and processing enterprises of special

interest to small producers, in joint venture with the private sector. In spite of the law, in late 1995 only a few selected items included in its provisions had actually been implemented.

Application of the measures outlined in the reactivation plan was continued after the change of administration in August 1994. The new government complemented the measures of 1993 with implementation of the investment subsidies created by the Agricultural Law. Subsidies were authorized for investment in irrigation projects and purchases of new machinery. A new programme to refinance and lower interest costs of overdue debts for small producers was also implemented in 1995.

The government also initiated a temporary programme of absorption agreements, in which processor industries, such as feed manufacturers and oilseed crushers, agree to purchase all domestically produced commodities at specified prices. The programme was complemented by direct subsidies to producers in the purchase of the soybean, cotton and rice harvests. In 1995, the price supports and the restrictions to imports implicit in the scheme increased protection levels for rice by 65 percent, for yellow maize by 25 percent, for white maize by 60 percent and for barley by 25 percent.

Production levels of most of the crops affected by the 1991-92 crisis displayed a slow recovery during the 1993-95 period. A Ministry of Agriculture study found that profit margins started to increase in late 1993, with the fastest rates of growth concentrated among exportable annual crops. Prices of all crops excluding coffee grew by 36 percent in 1994. In the same year, agricultural exports increased by 18 percent (excluding coffee), after falling by 4 percent in 1993. However, the value of imports continued to grow at fast rates, reaching 38 percent in 1994, caused, in great part, by higher prices of grains. The production of cotton displayed a significant recovery, yielding an exportable surplus by 1995, as a consequence of increasing international prices and government supports. Of all exportable crops, only bananas have continued to display stagnant production levels, as a result of global oversupply, the implementation of import quotas in the EU and growing violence in the Urabá region.

In 1995, agricultural production (excluding coffee)

grew by 2.9 percent. Growth was concentrated in perennial crops, while annual crops fell by 0.1 percent as a result

of the lacklustre performance of importables such as sorghum, soybean and maize. Smallholder crops presented high growth rates, particularly in plaintains, yuca and

ñame. For the first time since 1990, agricultural exports grew faster than imports, in large part the result of higher world prices for Colombian exports and a faster rate of devaluation.

The bold economic reforms of 1990-93 yielded positive results for the Colombian economy. In agriculture, however, the record has been mixed. In the short term, the reforms to promote greater market orientation were partially accountable for the crisis of 1991-92 that was faced by most tradable crops. Trade liberalization and the removal of import controls exerted the most damaging influences on profitability for importable grains and oilseeds. The timing of the reforms was unfortunate, however; production levels had been buoyed by high international prices and a devaluating exchange rate in the 1985 to 1990 period. Implementation of the reforms coincided with the onset of a period of extremely low international prices and with a surge in capital inflows that further depressed producer incentives through the appreciation of the exchange rate. The effect of low producer prices was compounded in 1992 by shortfalls in production in many areas of the country that were affected by the most intense drought in three decades.

In spite of the setbacks, emergency measures were taken and most of the sectors that suffered the effects of reduced profitability between 1991 and 1993 have gradually recovered. Some of the measures have implied the abandonment of the free market spirit of the original reforms, as more pragmatic considerations have reigned. However, broad policy goals remain consistent with maintaining an open trade system in agriculture and most support measures implemented since 1993 have been temporary. In spite of the initial difficulties, farmer groups have accepted the basic principles of the new approach and have undertaken actions to improve their competitiveness for the future.

After the remarkable recovery of 1993 to 1995, Colombian agriculture seems poised to pursue a more sustainable growth pattern in the long term. Competition with imports has raised the level of awareness among farmers of the need to increase productivity levels and shift crop mixes towards the demands of the market. As a result, productivity levels are increasing and investments in infrastructure and research are laying the foundations for future growth.

Success for Colombian agriculture will, however, require that some remaining obstacles are overcome. Colombian farmers continue to face extremely high levels of rural violence, a factor that has checked the growth potential of Colombian agriculture for decades. According to a government (National Planning Department) study, farmers lost between 10.6 and 17 percent of agricultural GDP annually during the 1980s as a result of kidnappings, extortions, crop losses, theft and general lack of security. Better growth prospects for agriculture will require that rural violence be sharply reduced.

The oil bonanza that is expected to last until the first half of the next decade may increase pressures on the profitability of tradable agriculture. As oil revenues are absorbed into the economy, the exchange rate is likely to appreciate even further and relative prices will move in favour of non-tradables. Most of the income gains of the boom are expected to be captured by the urban sector. In order to decrease the negative effects on production of tradables, in 1995 the government created an oil stabilization fund to reduce negative impacts, and this is expected to limit the rate of appreciation. For agriculture to reap benefits from the bonanza, public investment will need to be raised in key areas, such as research and transport infrastructure, that might increase the competitiveness of Colombian farmers.

Finally, Colombian agriculture will not take full advantage of its natural potential until measures are taken to improve the pattern of resource use. The intensity with which agricultural land is used continues to vary sharply from region to region; parts of the Andean highlands are overexploited whereas large areas in the Atlantic and Central Magdalena region are underexploited. This pattern of resource allocation will continue to generate significant efficiency, equity and natural resource losses until policy biases that favour large mechanized farming units and livestock operations are removed. This should expand employment opportunities in the countryside and reduce rural poverty as well as the reasons for violent actions.

29 See FAO. 1994. The State of Food and Agriculture 1994. Rome.

![]()

![]()

![]()