![]()

![]()

![]()

Interest in the use of cassava as an animal feed dates to the creation of the European Common Market and its Common Agricultural Policy. This policy, designed to promote and protect member country agriculture, favoured the blending of protein rich feeds, such as soybeans, with energy rich feeds, such as cassava, to produce animal feeds. European feed compounders sought sources of cheap cassava - first in the form of chips and later in the form of pellets. The growth in this market has been impressive (Tables 56 and 57). In 1995 11 countries imported more that 10 000 tonnes of dried cassava (which is basically chips and pellets) and 6 cassavaproducing countries exported more than 10 000 tonnes. The non-European importers have been China, Korea, the U.S.A. and Japan, all of which became cassava importers after 1980.

|

Table 56 |

||||||

|

Country |

1961 |

1965 |

1970 |

1980 |

1990 |

1995 |

|

Netherlands |

141 |

72 093 |

502 166 |

2 491 590 |

4 600 769 |

1 107 308 |

|

Spain |

|

10 939 |

10 707 |

336 |

769 760 |

658 890 |

|

China |

|

|

|

|

703 711 |

457 317 |

|

Bel-lux |

22 185 |

95 925 |

268 423 |

822 330 |

935 324 |

393 371 |

|

Portugal |

10 370 |

10 644 |

2 737 |

595 |

536 962 |

324 244 |

|

Korea Rep. |

|

|

|

|

763 465 |

152 061 |

|

Germany |

37 383 |

387 962 |

587 645 |

1 354 695 |

773 461 |

119 093 |

|

Italy |

|

|

13 948 |

98 970 |

71 834 |

74 489 |

|

France |

26 350 |

17 400 |

11 088 |

365 072 |

468 233 |

68 509 |

|

USA |

|

|

|

|

179 000 |

24 052 |

|

Japan |

8 255 |

2 949 |

|

3 |

220 935 |

16 317 |

|

Total |

104 684 |

597 912 |

1 396 714 |

5 133 591 |

10 023 454 |

3 395 651 |

Over time different European countries have been the lead importers, only one country, Thailand has been the lead exporter. The data in Table 57 also show the sharp decline in the demand for cassava that occurred between 1990 and 1995. Total imports declined by more than 6.6 million tonnes, with European imports declining by 5.4 million tonnes. It is interesting to note that the Thai exports of dried cassava dropped to only 4.3 million tonnes, owing to their ability to find non-European markets for cassava.

Historic and current European cassava imports for animal feed usage have been discussed, in detail, in the Phase I study (Henry, Westby, and Collinson 1998). The latest inside information from major European and Thai cassava pellet and chip traders further emphasizes cassava's bleak future. While 1997 Thai pellet exports to the EU amounted to 3.3 million metric tonnes, valued at 8,394 million baht, the expectations for 1998 are down to 3.0 million metric tonnes for a value of 7,875 million baht (TTTA 1998). This may be somewhat too pessimistic, since the relatively cheaper Baht may offset reduced exports. Nonetheless, cassava pellet imports from Thailand and Indonesia are steadily decreasing. Some of the main reasons for this phenomena are reduced price levels of competing EU feed grains and strong competition for raw materials from domestic (Thai, Indonesian) starch processors. Another reason is the continuing pressure for the reduction of cassava production lands that is further influenced by cassava supply and price cycles.

|

Table 57 |

||||||

|

Country |

1961 |

1965 |

1970 |

1980 |

1990 |

1995 |

|

Thailand |

8 405 |

400 526 |

1 172 100 |

4 970 420 |

7 557 577 |

3 224 191 |

|

Indonesia |

8 719 |

84 210 |

334 227 |

386 055 |

1 271 101 |

481 483 |

|

Netherlands |

4 |

372 |

26 296 |

333 056 |

259 154 |

156 507 |

|

Bel-lux |

13 |

|

1 163 |

201 453 |

58 978 |

75 594 |

|

Costa Rica |

|

2 |

69 |

6 676 |

16 000 |

44 926 |

|

Germany |

42 |

19 |

260 |

18 250 |

46 348 |

38 847 |

|

Viet Nam |

|

|

|

|

28 000 |

30 500 |

|

United Republic of Tanzania |

19 217 |

8 252 |

8 554 |

|

35 000 |

21 000 |

|

Total |

36 400 |

493 381 |

1 542 669 |

5 915 910 |

9 272 158 |

4 073 048 |

Major Dutch pellet traders foresee a 1998 pellet import volume of 1.4-1.6 million metric tonnes into Rotterdam, or approximately 110 000 tonnes per month (personal communications, ATRACO Ltd and IAT, Rotterdam). However, up to five years ago, Holland imported double this volume. Furthermore, while Germany used to import an average 1 million metric tonnes per year, pellet imports this year have nearly been suspended (personal communications, Alfred Toepfer International, Hamburg). The principal cause is the reduced margin between cassava pellet and its EU substitutes. Imports were high when this margin was dfl 60/t or more. In April 1998, the Rotterdam cif pellet price including tax was around dfl 215/tonnes compared to EU maize of dfl 230/tonne, hence a margin of only dfl 15/tonne. If these pellets are shipped further to Germany at a rate of DM 7-8/t, the price advantage of cassava pellet is largely eroded.

Besides significant problems of maintaining a price edge, concerns over deteriorating pellet quality have increased. While EU import regulations specify a minimum pellet starch level of 60 percent, up to the mid-90's, this was not a problem since average pellet starch contents were as high as 70 percent. More recently, Thai cassava pellet imports have been detected with starch contents of 55-57 percent. These fluctuations not only cost money to feed millers, they also cause serious problems in maintaining consistent nutrition levels in the feed formulas. Some feed millers nowadays will pay as much as US$10 per tonne premium, for pellets with a 70 percent (10%+) starch content. The reduction of cassava pellet starch contents seems to be an indication of the increased inclusion of cassava starch processing by-products (bagasse) in the pellets (Personal communications, ATRACO, Rotterdam).

During the last five years, the European imports for Thai cassava pellets has registered a downward trend. Given that EU feed grain intervention prices may be further reduced, or in the best-case scenario, remain at a constant level; it seems most probable that pellet imports will continue to slide in the future. A variable that may somewhat change this bleak picture, is the price of soymeal and the devaluation of the Thai baht. Given large predicted 1998 harvests in the main soybean producing countries, decreasing soymeal prices may somewhat widen the margin between cassava-soy mixtures and EU maize or barley. The devaluation of the Thai baht has also tended to make cassava more competitive.

Constraints

Future European demand for imported cassava pellets and chips is highly dependent on the pig industry growth in the EU. It also depends on the price of substitutes (feed-grains and other grain substitutes) and complements (animal and vegetable proteins). Strict environmental laws have already limited the potential for further increased pig production, especially in North European countries (the principal and traditional consumers of imported cassava). The bottom line is that the only real window of opportunity for cassava pellets to regain some of their lost European market is a significant pellet price reduction. This directly implies the need for reducing per unit, cassava root production costs in Thailand. From the supply side, the major constraint is cassava pellet prices, or rather Thai cassava root prices.

European countries cassava pellet and chip imports from SE Asia, is dated to the 60's, and was principally related to EU policy conditions (CAP import regulations). The subsequent cassava boom was largely managed by various EU policy measurements. Likewise the current downturn of the pellet imports has also been policy-induced. In the future, EU grain intervention prices will continue to be under pressure, further reducing the margins for imported cassava. In the cassava growing countries, a significant shift towards starch manufacturing has occurred, putting further pressure on the pellet industry (competing for the same raw material).

The future for cassava pellet imports depends ultimately to a large extent, on future EU policy developments and the ulterior capacity of the Thai pellet industry to reduce costs. This has to come from higher cassava productivity, stabilisation of prices and improved industry organization.

The European Union feed market for dried cassava is well established. The EU has allocated a quota of 145 000 tonnes to World Trade Organisation members, excluding Thailand, Indonesia and China. This quota has never been reached. But it is noted by traders that the pig-feeding industry in Bretagne could absorb as much as 10 000 metric tonnes per month of chips from West Africa. The chips would of course have to be at appropriate price, quality and supplied throughout the year (Personal communications, IAT, Rotterdam).

In Ghana three local companies (Transport & Commodity General (T&CG), GAFCO and SILTEK Exports) sought to exploit the opportunity offered by the WTO quota. However, by 1998 only T&CG was still involved in the chip market. GATCO and SILTEK Exports had withdrawn from the market for reasons that will become apparent later. This case study focuses on the activities of T&CG.

T&CG entered the cassava chip market in 1993 in partnership with Tranex, a livestock feed brokerage based in Belgium, that supplies feed ingredients to a number of feed millers in Belgium and France. Initial exports were of negligible size but in 1996 the company exported 19,725 tonnes to the EU. During this period the company purchased cassava for US$30 per tonne[23] (farm gate price) and sold cassava chips for anything up to US$152 per tonne. In 1997, however, the average dried cassava price fell to $100/tonne (FAO Food Outlook, November 1997). In the first quarter of 1998 T&CG's input and output prices for dried cassava chips were US$40 and US$70 per tonne respectively.

In the early stages of operations T&CG attempted to establish a centralized processing operation but this proved expensive and inefficient. An improvement on this approach involved creating mobile processing teams to tour the production areas - chipping and drying cassava on site. Ultimately the company settled on farm-level processing as the most effective option. Initially the company provided manually operated chipping machines, but as these proved expensive and unreliable, the company switched to a policy of encouraging farmers to chip by hand using a knife. Individual farmers harvest and wash roots before chipping and then sun dry at the field edge. Some farmers were equipped with concrete drying floors but as this proved expensive, T&CG have been encouraging farmers to use traditional wooden drying screens made from lengths of bamboo. Under normal conditions chips are reported to take about two days to dry.

A general specification for cassava chips intended for export to the European Community for use in livestock feeds is given in Table 58. Chips should be white or near white in colour, free from extraneous matter, moulds, insect infestation and damage and possess no peculiar odours. In addition, shipments of chips must not contain significant amounts of dust, as this is considered unacceptable by European importers.

|

Table 58 |

|

|

Parameter |

Percentage |

|

Moisture (maximum) |

10-14 |

|

Starch (minimum) |

70-82 |

|

Total Ash (maximum) |

1.8-3.0 |

|

Crude fibre (maximum) |

2.1-5.0 |

|

Sand and other extraneous matter (maximum) |

3 |

|

Cyanide (maximum) |

100 mg/kg |

|

Dimensions (maximum in cm) |

Lenght 4-5 cm |

This market opportunity has been mainly influenced by changes in Ghanaian policy and economic factors. But it would be true to say that improvements in the network of major roads linking inland areas of Ghana with the coastal cities and major ports would have made Brong Ahafo a more attractive production area for this purpose.

A number of Districts in Eastern, Volta, Ashanti and Brong-Ahafo Regions produce more than 100 000 tonnes of cassava per annum (Day et al. 1996). However, not all Districts are appropriate as sources of cassava for export as many have good access to fresh markets or competing processed products that command higher prices than cassava chips. In practice T&CG has concentrated on six Districts in Brong Ahafo Region where large amounts of cassava are grown, drying conditions are good but farmers' access to alternative markets is poor. Production is decentralised with four to five production zones per district. Each zone contains a number of farmers organized into groups to supply chips to T&CG, farmers groups are expected to supply a minimum of 25 tonnes of marketable chips per month. Farmers are expected to deliver chips to one of 20 zonal buying agencies that then forward batches of chips to the zonal buying centre, for onward transport by road or lake to the company's warehouses in the port of Tema. When sufficient chips have accumulated, chips are forwarded by ship to the companies feed broker (Tranex) in Europe who take responsibility for distribution of chips to the feed millers.

The major physical bottlenecks associated with T&CG's activities are:

Transport infrastructure. The main production zones have a low level of road infrastructure and lack linkages from field areas to the main roads. In addition there is almost no mechanization of transport from field to road. Dry chips have to be head loaded through the bush to reach the road. This is an activity that increases labour costs and reduces flow of supplies to the collection points.

Equipment. In an attempt to increase production rates, the company introduced a manual-chipping machine. This machine proved costly, inefficient and unreliable under field conditions. Motorized equipment was not considered an option due to unacceptable high capital costs (ibid).

Labour shortages. This is an ongoing problem in rural Ghana. Manual chipping requires a high labour input that is not always readily available.

Farmer confidence. Farmers involved in this venture valued the benefits of regular income and guaranteed market access. The success of the company in 1996 led farmers to have high expectations of market returns and sustainability. However, the collapse of world prices for dry cassava in 1997 (FAO 1997) led to cash flow problems, many farmers lost confidence with the company and switched to other markets for their product.

Expansion difficulties. To create a large supply of chips within two years, T&CG operated a policy of rapid expansion into nine Districts in Brong Ahafo and Northern Regions. In each District the company had to provide extension support to raise awareness among farmers, provide training and establish field-based management systems that could provide the necessary level of quality control. In retrospect, the company recognises that this level of expansion was too rapid, and was partly responsible for failings in quality control.

Quality. The policy of decentralised production can lead to problems with establishing and maintaining consistent quality standards. Farmers can be tempted to increase production at the expense of quality. The most common problems are mould spoilage, contamination with sand, and high moisture contents due to inadequate drying. The dimensions of chips may also fail to meet the importers specification.

Supply problems. Increases in the price of fresh roots and dry cassava chips for local human consumption have made it difficult for T&CG to source enough chips to meet their contractual obligations.

Handling methods and loading rates. Low levels of mechanization at the company's facilities in Tema have resulted in very low loading rates, typically 500 - 1 000 tonnes per day. In contrast a similar company in Thailand would expect to load 20 000 tonnes per day. The problem of bulk handling is a key constraint as it increases shipping costs.

Power supply. Since January 1998 Ghana has been experiencing a national power shortage resulting from a combination of several years of unusually dry weather, increased demand for both water and electricity and problems with the operation of the nations main source of power generation. This is a serious problem that may take several years to resolve.

The initial success of T&CG's operation was influenced by several factors:

Competitiveness of cassava as a feed ingredient. In the period from 1993 to 1996 dry cassava, with a suitable protein supplement, was able to compete in Europe on a price basis with alternative feed ingredients such as barley and maize.

Access to funds to develop the opportunity. It is difficult to put a figure on the cost of developing a market opportunity but T&CG have estimated that a minimum of US$600 000 were required for research and development over a five year period in order to exploit this opportunity. T&CG's European partner Tranex supplied a substantial amount of this money.

Farmers' interest in chip production. In the production zones identified by T&CG farmers faced problems with access to markets for fresh cassava roots and relatively poor prices for dry cassava for local human consumption (kokonte). Although the equivalent fresh root price was three times higher than that offered by T&CG for dry chips (Day et al. 1996), farmers valued the opportunity offered by T&CG. The opportunity promised ease of market access, a regular and guaranteed income stream, payment by weight (which farmers considered to be fairer than volume basis), prompt payments and the possibility of credit from the company.

Positive policy environment. During the early stages of the development of this opportunity, a positive policy environment for cassava development existed in Ghana. Cassava was identified as a first priority crop in the National Research Strategic Plan (NARSP) and Medium Term Agricultural Development Plan (MTADS). The MTADS recognised the importance of adding value to cassava through income generating opportunities, expanded markets and interventions by the private sector.

In 1996 and 1997, demand for dry cassava remained steady. However, in 1997, world cassava prices fell from US$150 to US$100/tonne, causing severe constraints on T&CG. In the same period reductions in set-aside subsidies within the EU depressed the price for barley. In addition the price of soy-meal (protein supplement required for cassava feeds) was very high. To maintain the market competitiveness of cassava, under the above conditions, meant that its prices needed necessarily to be cheaper. Unfortunately this was not a viable option for T&CG, which was facing very high production and transport costs when, compared to major competitors in South-East Asia. At the same time, the problems of the European market affected the company's cash flow and interfered with payments to farmers in the production zones.

In Ghana unusually dry conditions attributed to the El Nino weather system led to increases in prices for both kokonte and fresh cassava for local consumption. Many farmers who were already upset by the uncertainty of payment by T&CG switched to alternative outlets. In three Districts in the Northern Region, kokonte prices increased to US$0.13/kg, while T&CG, could only offer US$0.04/kg; thus was unable to compete and had to withdraw from these areas.

In addition to these problems, the company was burdened with the very high costs associated with transport and handling of the product in Ghana, and by the difficulties in sourcing lines of credit to maintain cash flow through a difficult period.

The case of T&CG provides an example of a complete commodity system, where all the stakeholders have a vital role to play in ensuring the successful exploitation of the opportunity. Farmers are the primary stakeholders in this system, and they have the responsibility for providing a constant supply of chips of consistent quality. If the farmers lose confidence in the market, or fail to pay attention to quality, the system will collapse. T&CG has a key role in providing the farmers with a point of access to the market. T&CG equally has a role in ensuring technical and financial supports to exploit the dry cassava market opportunity, as well as providing a management structure to co-ordinate supplies and maintain quality control. The presence of a large and organized purchasing organization should also help to build the confidence of the farmers as to the sustainability of the opportunity. But if the buying organization fails, then farmers will not be able to access the international market. The European feed broker provides a means of reaching the feed millers in Europe, and this case has also provided an example of a broker's substantial financial commitment. Without the feed broker it seems unlikely that T&CG could have developed the dry cassava market opportunity or accessed the European markets so readily.

As noted above, there is little reason to assume that the EU market for animal feed is going to increase. Of course there is the possibility that the market share of some exporters can increase at the expense of other exporters. There is also the possibility of short-term increases in the market. For example, EU traders are currently taking out future contracts on dried cassava shipments, in the belief that large harvests of soybean predicted for the U.S. and Brazil, will reduce soy-meal prices during 1998 and thus improve the competitiveness of cassava (personal communication Alfred Toepfer Gmbh, Hamburg). However, this must be set against current trends in the prices for barley and maize. During 1998, EU barley prices have remained low and large harvests of maize in Argentina and the U.S. could make maize a strong contender against cassava in the short term.

Lessons from the T&CG experience

To continue to exploit this business opportunity against competition from alternative feed ingredients and markets in Ghana, T&CG needs a high level of capital investment. This would reduce the costs associated with transport and handling of the product and thus reduce the sale price of the product to a more competitive level. In addition, financial backing is required to maintain cash flow and farmer confidence during times of reduced world market prices for dry cassava.

The case of T&CG provides a good example of a commercial company attempting to address the problems of a complete commodity system using a mixture of commercial and developmental techniques. This case provides many useful pointers for the development of any cassava processing option in the future. T&CG concentrated solely on the export market, as this seemed to offer the largest market and maximum opportunity for a good return on initial investment. In retrospect, it is clear that the company would have been wise to consider domestic markets for high quality cassava chips as well, because this would have provided a buffer against fluctuations in the world market price for dry cassava. Within Ghana potential opportunities exist for dry chips in the domestic livestock markets and for the manufacture of industrial adhesives and glue extenders.

Marketing dry cassava internationally appears attractive as a means of adding value, expanding market opportunities and providing a source of foreign exchange. This information coupled with knowledge of the examples provided by Thailand, Indonesia and China could attract many nations growing cassava to try and enter the market. However, prospective entrants need to be aware of the unpredictable nature of the EU cassava market, and must prepare themselves for mixed trading fortunes and stiff competition from South-East Asia. The following factors should be taken into consideration:

|

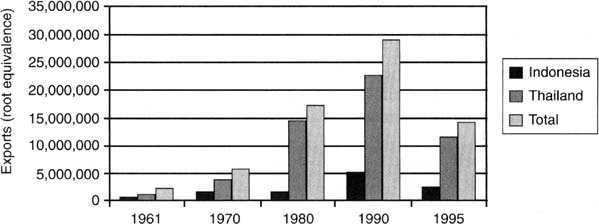

The experience of Thailand, as a leading exporter of cassava products, is instructive to potential exporters in what can be done and what must be done to be successful The objective of this section is to provide an overview of the Thai cassava industry and to identify the key factors that have contributed to the Thai success. As indicated in Figure 22, although 10 other countries export more than 10 000 tonnes of cassava chip (root equivalence), Thailand and Indonesia are the dominant exporters of cassava chip worldwide.

|

Figure 22

|

The development of the cassava industry in Thailand can be divided into 3 phases, each dominated by a partially processed cassava product.

1940s to 1966, Starch: It is believed that cassava was introduced into the Southern region of Thailand from Indonesia. Until the 1940's, cassava was grown in the eastern seaboard of Thailand. During the Second World War, cassava root was processed into starch, using a simple technology, and used to satisfy the domestic demand since Thailand was unable to import starch from abroad. Shortly after the Second World War, modern technologies were imported for processing cassava starch for both domestic consumption and export. This led to the gradual development of the eastern seaboard of Thailand as a cassava starch industrial region directed towards export.

1967 to 1993, Animal feed: In 1962, waste or pulp residuals from cassava starch processing were dried and exported to European countries as a cereal substitute ingredient in animal feed. The highly protected cereal market caused by the EEC's Common Agricultural Policy (CAP) created a market for cereal substitutes in the EEC, and triggered the development of cassava products for animal feed in Thailand. Hammer mills were imported from Germany for producing cassava, or tapioca meal. for export. Concurrently, cassava chips were produced to replace both starch waste and hammer milled cassava exports, which were facing quality problems. Cassava chips however were bulky and freight costs were high. Consequently, cassava pellets, processed from chips by pelleting, were produced using imported pelleting machines from Germany. It did not take long before the local mechanical engineers were able to produce a cheaper pelleting machine than the imported pelleting machines. The local machines produced a relatively softer quality cassava pellets (native pellets) than the imported one. This enabled a rapid expansion in the native pellet industry, all of which was destined to the EEC market.

The quantity of cassava product exported as animal feed increased from 506 000 tonnes of chips and 97 000 tonnes of pellets in 1967 to 487 000 tonnes of chips and 6.7 million tonnes of pellets in 1982. The increase in area of land cultivated and production of cassava was spectacular. At the beginning of the export era in 1967, about 177 000 rais (6.25 rais = 1 hectare) of cassava was planted with a production of 337 000 tonnes. By 1978, cassava area increased to 7.3 million rais with a production of 16.4 million tonnes of roots, and by 1989, the area increased further to 10.1 million rais, with a production of 24.3 million tonnes.

However, in 1996, total cassava cultivated area and volume of production declined to 7.9 million rais and 17.4 million tonnes, respectively (Table 59). This decreasing trend started after 1989. Given the fluctuations in national average yields of 1,969 to 2,281 kg/rai (12.3 to 14.3 tonnes/ha) the increase in root production was gained through area expansion rather than yield improvement[24].

The expansion of the EEC cereal substitute market and the sharp increase of Thai cassava exports into the EEC attracted the attention of EEC's cereal producing countries and the EEC Commission. Eventually, Thailand signed a Voluntary Export Restraint Agreement (VER) or officially called " The Cooperation Agreement between the Kingdom of Thailand and the European Economic Community of Manioc Production, Marketing and Trade" in 1983 for a period of four years. Under the agreement, Thailand accepted to limit its export of cassava to the EEC. In return, the EEC gave Thailand 75 million ECU to assist in the diversification of its production. Since then three such agreements have been signed, the last one was in 1994.

After the implementation of the VER in 1983, the Thai government began to monitor closely cassava products for the animal feed industry, with active intervention through different measures. The Government was particularly concerned about its export quota allocation to the EEC. At least two significant changes took place during this period. One, economies of scale in processing and marketing was gained by the expansion of warehouse facilities, and the adaptation of modern mechanical loading and unloading facilities. Two, dust pollution problems at the port of entry to Europe were solved by the introduction of hard pellets in 1989.

|

Table 59 |

||||||

|

Period |

Production |

Cost and return |

||||

| |

Planted area |

Production |

Yield |

Total cost |

Farm gate |

Return |

|

1978 |

7 281 |

16 358 |

2 246.67 |

0.28 |

0.78 |

0.50 |

|

1979 |

5 286 |

11 101 |

2 100.08 |

0.34 |

0.74 |

0.40 |

|

1980 |

7 250 |

16 540 |

2 281.38 |

0.41 |

0.53 |

0.12 |

|

1981 |

7 940 |

17 744 |

2 234.76 |

0.43 |

0.61 |

0.18 |

|

1982 |

8 418 |

18 764 |

2 229.03 |

0.45 |

0.53 |

0.08 |

|

1983 |

8 552 |

18 989 |

2 220.42 |

0.44 |

0.62 |

0.18 |

|

1984 |

8 780 |

19 985 |

2 276.20 |

0.46 |

0.67 |

0.21 |

|

1985 |

9 230 |

19 263 |

2 087.00 |

0.43 |

0.38 |

-0.05 |

|

1986 |

7 748 |

15 255 |

1 968.90 |

0.44 |

0.74 |

0.30 |

|

1987 |

8 820 |

19 554 |

2 217.01 |

0.41 |

0.91 |

0.50 |

|

1988 |

9 879 |

22 307 |

2 258.02 |

0.41 |

0.61 |

0.20 |

|

1989 |

10 136 |

24 264 |

2 393.84 |

0.39 |

0.55 |

0.16 |

|

1990 |

9 562 |

20 701 |

2 164.92 |

0.45 |

0.67 |

0.22 |

|

1991 |

9 323 |

19 705 |

2 113.59 |

0.49 |

0.76 |

0.27 |

|

1992 |

9 323 |

20 356 |

2 183.42 |

0.56 |

0.76 |

0.20 |

|

1993 |

9 100 |

20 203 |

2 220.11 |

0.59 |

0.67 |

0.08 |

|

1994 |

8 817 |

19 091 |

2 165.25 |

0.60 |

0.59 |

-0.01 |

|

1995 |

8 093 |

16 217 |

2 003.83 |

0.63 |

1.15 |

0.52 |

|

1996 |

7 885 |

17 388 |

2 205.20 |

0.68 |

0.98 |

0.30 |

1994 onward, Starch and modified starch: The first sign - to the cassava industry- that the artificial cereal substitute markets, for cassava products in the EEC, had reached its peak was the signing of the VER. This fact was reinforced by the implementation of the CAP reform in 1994. Understanding these signals, Thai processors and traders of cassava began to diversify or integrate into cassava starch processing. They also began producing modified starches through joint ventures with established developed country firms in the U.S., Japan, and Europe (the Netherlands, Belgium, UK and Finland).

Throughout these phases, cassava remained a profitable crop for the Thai farmer. During the 18 years period, between 1978 and 1996, the computed farmers' returns were negative in only 2 years, 1985 (-0.05 baht/kg) and 1994 (-0.01 baht/kg). As illustrated in Table 59 total production costs of root on average have increased from 0.28 baht/kg in 1978 to 0.68 baht/kg in 1996[25], while farm gate prices have fluctuated in the range of 0.38 to 1.15 baht/kg.

An examination of the marketing channel and price formation of cassava and cassava products is simplified by examining the product flows and price determination of farm price (root price) and the final product (chip, pellet, native starch and modified starch) prices.

In Thailand, cassava roots are sold at the farm directly or through middlemen to two distinct processing factories; chip and pellet factories for feed ingredient processing or native and modified starch factories for starch processing. Processed cassava products are then either further processed into other products or sold through the marketing channel for export and domestic consumption. For example, cassava chips may be sold to pellet factories, exported or used in the domestic market as animal feed. The price for each cassava product is determined by the market at each market level (Figure 23).

Figure 24 illustrates the competitiveness and efficiency of the cassava industry's pricing system, and shows that the price movement of root, chip, pellets and starch are very similar over time. From 1982-1997, the price of fresh root at the factory fluctuated from 630.67 baht/tonne to 1,618.00 baht/tonne. This translates to an average price of 945.29 baht/tonne or approximately $43/tonne. For chips and pellets, an upward trend in prices was observed during 1982-1995. In 1982 the prices of chips and pellets were 2,030.00 baht/tonne and 2,399.20 baht/tonne, respectively, and in 1995 prices increased to 3,011.00 baht/tonne and 3,157.80 baht/tonne, respectively. Similarly, the domestic wholesale price of cassava starch grade A increased from 4,427.08 baht/tonne in 1982 to 8,404.00 baht/tonne in 1995. However, since 1995 prices have been falling. Grade A starch has decreased to 5,987.00 baht/tonne in 1997[26], as well as the domestic wholesale price of chips and hard pellets and fresh root price.

|

Figure 23

|

|

Figure 24

|

Cassava product processing costs are influenced by the size of the factory and the number of operating days per year. The financial crisis has also had a strong impact on processing costs. Traders estimate that in 1997/98 the processing costs of cassava chip were 100 baht/tonne, 250 baht/tonne for pellet and 1,800 baht/tonne for native starch. It is worth noting that these processing costs were estimated for established factories. One would expect that the processing costs for newly established factories would have been much higher.

Transportation costs are an important component of the pricing system. The Thai cassava industry has benefited of late, from the improvement in the efficiency of export handling mechanisms and procedures. For example, the current export cost is 300 baht/tonne, substantially less than the costs in 1992 of 500 baht/tonne. The current average domestic cost to transport cassava product from the major cassava-producing province (Nakhon Ratchasima) to Bangkok is about 250 baht/tonne.

Another important development that has lowered transportation costs has been the improvement of basic infrastructure in Thailand. Statistics obtained from the Ministry of Finance show that the total government budget for transportation and communication programmes increased from US$554 million in 1983 to US$3,548 million in 1997. This is an annual compound growth of 18 percent. The budget allocated to land transportation is the highest at 93%, followed by air transportation and water transportation at 3.2% and 2.9%, respectively. (Table 60).

|

Table 60 |

||||||

|

(US$ millions) |

||||||

| |

Administration |

Transportation |

Total |

|||

| |

|

Land |

Water |

Air |

Telecom |

|

|

1983 |

1.02 |

512.07 |

18.37 |

11.20 |

1.34 |

544.00 |

|

1987 |

1.52 |

448.76 |

20.42 |

12.27 |

1.91 |

484.88 |

|

1992 |

4.67 |

1 132.90 |

31.62 |

69.44 |

3.12 |

1 241.75 |

|

1997 |

8.38 |

3 285.89 |

85.38 |

190.20 |

14.90 |

3 548.75 |

|

Growth rate |

17.65 |

18.06 |

9.72 |

20.54 |

18.29 |

17.88 |

|

Avg. % share |

0.46 |

93.00 |

2.96 |

3.20 |

0.38 |

100.00 |

|

Source: Thai Ministry of Finance |

||||||

The Thai cassava industry developed within a free market price system with little or no government intervention. The industry participants and private firms (both Thai and subsidiaries of trans-national companies) have successfully developed a market-driven demand and a massive cash crop production. They have also successfully solved most of the trade-related problems through negotiation with the trading parties. The one area where the government did intervene in the trade negotiations was in dealing with trade protectionism policies implemented by importing countries.

Since 1982, the export animal feed trade has been closely regulated, with sporadic interventions in the price of roots by concerned government agencies. Intervention in cassava starch processing and trading has occurred only periodically. In general the cassava starch industry has enjoyed a relatively government free market environment.

Although the decision by the government to impose regulations on cassava trade, in the form of export quotas to the EU, was not appreciated by cassava industry stakeholders, after many reformulations, a workable quota allocation method was put in place. Based on the computed average farmers' return, the so-called workable solution has benefited farmers since its establishment in 1982 until 1997. Moreover, the export earnings of cassava products have ranked among the top five commodities in Thailand, making cassava a top strategy crop of Thai agriculture.

Prior to 1970, Thailand was not a major cassava producing country. In two decades (1970s-1980s), Thailand became a major cassava producing country and a leading exporter. The key factors that contributed to that growth and development are identified below:

Food: rice is the major staple, of which Thailand is a major exporter; therefore, cassava is not a staple food in the Thai diet.

Land: degraded forest lands were opened up for cash crop production; the land was suitable for cassava grown under rain fed conditions allowing massive area expansion of cassava root.

Climate: a distinct raining and dry season made sun drying a low cost possibility, especially for cassava chips.

Infrastructure: the government has constantly improved and expanded the road transportation infrastructure, setting the conditions for a viable low cost transport system which has reduced the handling costs of processed cassava products.

Free market environment: Thailand has maintained a free enterprise policy and has encouraged private sector investment. The government has well-established rules and regulations that guarantee private sector property rights.

Technological transfer through joint ventures: Thai private firms and transnational firms have realised the mutual benefit of joint ventures in using low cost comparative advantage to capture export markets and penetrate existing markets.

Processing and handling: Investments in both processing and handling occurred as soon as the industry grew to a viable size. Investors adopted new technologies and gained benefits of economies of scale.

Active entrepreneurs in agricultural sector: An adequate number of entrepreneurs in Thai agriculture allow for a very competitive industry.

Well-organized and co-operative associations: A number of associations exist for producers, processors and traders. These associations are, to a large extent, well established and organized and co-operate among themselves.

Dialogue between public and private sector: Well-established associations enable dialogue between public and private sectors to solve problems faced by the industry and identifying common interests in research and development. Domestic public and private sectors are also connected to international institutions.

As noted already, the catalysts for the development of the Thai cassava export industry was the creation of the European Economic Community and its resulting Common Agricultural Policy (CAP). The CAP opened the market to the importation of cereal substitutes. Although the Europeans promoted the export of cassava from several countries, only Thailand, and to a lesser extent Indonesia, responded to the opportunity. The Thai response was nothing less than spectacular as indicated in the following table.

As noted in the preceding section, numerous natural and man-made factors contributed to the development of the Thai cassava industry. The most impressive fact is how rapidly it grew in the 'sixties and 'seventies. By 1968, Thailand had reached a level of cassava export that only Indonesia had previously been able to achieve. To put Thai export volumes into perspective, Thailand exports 14 000 metric tonnes of processed product on average daily. This is equivalent to a daily fresh root export of approximately 40 000 metric tonnes (Table 61).

|

Table 61 |

||||||

|

Year |

Area |

Production |

Exports |

Number of |

Number |

Export price |

|

1963 |

|

|

483 |

|

|

|

|

1968 |

|

|

875 |

90 |

28 |

50.00 |

|

1978 |

1 164 |

16 350 |

6 275 |

|

|

|

|

1988 |

1 580 |

22 307 |

8 107 |

|

|

|

|

1989 |

1 621 |

24 264 |

9 799 |

|

|

|

|

1996 |

1 262 |

17 388 |

4 500 |

|

|

123.00 |

|

1997 |

1 008 |

16 875 |

5 062 |

|

44 (approx.) |

82.00 |

The export oriented cassava chip and pellet industry is currently facing serious changes. For the past three decades, Thai cassava chips and pellets have been an export-oriented industry. Since the early 1980s and the signing of VER agreements between Thailand and the EEC, the industry has tried to develop alternative export markets. Although these efforts have intensified since CAP reform in 1994 new markets have not materialized. Total exports continue to decline, from 6.7 million tonnes, of which 5.2 million tonnes was exported to the EU, in 1993 to 4.2 million tonnes, of which 3.2 million tonnes was exported to the EU, in 1997. It is hoped that total exports will stabilize soon at about 3 million tonnes per year.

The European market for cassava chips and the resulting benefits for exporters, especially those from Thailand and Indonesia, have spurred an interest in cassava as an export crop. The rapid growth of the market peaked in 1989 and has been in a state of decline ever since. Attempts to restrict Thai exports to Europe began first in the early eighties and were the substance of a 1983 agreement between the EU and Thailand to restrict Thai exports of chips and pellets to Europe.

In principle, the restrictions placed on Thailand's exports, opened the door for other countries to fill the void, but none did. The Ghana case study illustrates one unsuccessful attempt to fill the void.

The Thai success in exporting cassava illustrates what is needed to develop export markets for cassava. The Thai case is also illustrative of many of the factors that are outlined in the Global Strategy for Cassava (Plucknett, Phillips, and Kagbo 1998). One, the EU, owing to the creation of the Common Agricultural Policy, created a growth opportunity based on competition. Two, European importers of animal feed ingredients were both catalysts and champions for the industry in many cassava producing countries. Indonesia and Thailand, however, were the only countries able to seize the opportunity. Three, Thailand was fortunate to have good supporting infrastructure - roads, ports and an entrepreneurial class of agricultural exporters. Four, Thai farmers, who were unfamiliar with the production of cassava, quickly appreciated the commercial benefits of growing cassava, and rapidly expanded the production of the crop. Five, another group of entrepreneurs quickly realised the benefits of drying cassava, and established numerous drying 'plants" in cassava growing areas. Six, the market, especially the processors, adapted to changing market conditions and requirements - producing first chips, then pellets and finally hard pellets. Seven, everyone in the supply chain appeared to understand the need to be competitive and price gouging was not obvious. Finally, industry and government re-invested in the industry as demonstrated by the activities of the Thai Development Research Institute.

While the development of the Thai cassava chip and pellet export industry was not planned, the requisite conditions were in place, or created, to promote the industry. The Thai industry is instructive of what would be needed to develop new markets for cassava whether it is for domestic or export use.

|

[23] Prices throughout this

report have been converted from local currencies to U.S. dollars at the

applicable exchange rate at the time the data refers to. Prices have not been

adjusted for inflation. [24] It is important to note that Thai yields of cassava have been relatively stable in a system that is probably the most intensive in the world. This observation suggests that cassava production is more sustainable than it is sometimes credited to be. [25] Using relevant exchange rates, the farm gate price of cassava roots were approximately US$19 and US$45 per tonne, respectively for the two periods in consideration. [26] The average exchange rates for 1982, 1995 and 1997 were 23.05, 25.60 and 25.39. |

![]()

![]()

![]()