![]()

![]()

![]()

Mr Raymon van Anrooy

Aquaculture

Economist

FAO, Rome,

with assistance from

Mr Nguyen Viet

Ha

Marketing Consultant

Hanoi, Viet Nam

This section of the project summarizes the findings of a study on aspects of vertical chain cooperation conducted in 2002 under the Fish marketing and Credit project in Viet Nam. The subsequent sections focus on general fisheries products marketing issues, domestic consumption of fisheries products and the credit needs of and investment opportunities in fisheries products marketing in Viet Nam.

The rapid increase in fisheries production in Viet Nam over the last decade caused imperfections in the marketing of fisheries products. Fishery[3] product exports increased rapidly and reached 358 000 tonnes in 2001, valued at US$1 777 million, thus providing a substantial contribution to the countries’ total export earnings. The total fishery production was estimated around 2 226 000 tonnes in 2001, which means that only 32 percent of the products were exported. Domestic consumption which accounted for the remaining about 70 percent of the volume is therefore of great importance to the fisheries sector.

Although the volume of fisheries products exported is small compared with domestic consumption, its value was relatively high. The importance of export for the Vietnamese trade balance has meant that in recent years government attention was mainly directed towards export and domestic markets were largely neglected. The increase in per capita consumption fisheries products to almost 18 kg/capita in 2001 and its implications has not received much attention at national level. The only significant study carried out in this field was a domestic market study for the Fisheries Sector Master Plan Project, which was supported by DANIDA and the Institute for Fisheries Economics and Planning (IFEP) of the Ministry of Fisheries (MOFI). The growing concern of domestic consumers on the quality and freshness of the fisheries products, the scarcity of supplies in some areas during certain months of the year, and the lack of information at ministerial level on the marketing of fish has lead to a request from MOFI for donor assistance in this field. In response to this request FAO and the DANIDA FSPS have supported a country-wide research project to address this knowledge gap.

The overall objective of the project was: to improve the livelihoods of the people working in the Vietnamese fisheries sector by the collection and analyses of fisheries products marketing information and the dissemination of the obtained information to all stakeholders in the sector, with particular emphasis on the support for the decision making processes in the Ministry of Fisheries, the sustainable development of the sector, gender roles, the achievement of food security and the alleviation of poverty.

Specific objectives of the project were:

i. to fill the current information gap on the marketing of fish and fishery products in Viet Nam in order to support MOFI, institutions and donors active in the sector to address the needs of the fisheries sector better and support the decision-making processes in the sector;

ii. provide access to clear market information to the actors in the fisheries products-marketing channel (e.g. fishers, middlepersons, processors, market traders and retailers) on the functions of the various actors in the channel, prices and consumer demands in the domestic market and the market structure;

iii. to contribute to the existing knowledge on how to feed the growing population in Asian cities efficiently, with respect to the provision of fisheries products and the main cities in Viet Nam, i.e. Ho Chi Minh City, Hanoi and Danang;

iv. to develop a model, including practical guidelines, that will assist the actors in the Vietnamese fisheries products marketing chain, by focusing on vertical cooperation, to become more competitive on the world - and domestic market and improve the individual as well as chain performance to satisfy better the consumer demands;

v. to contribute to the existing knowledge on how fish production, marketing and processing are being financed at present and on how marketing related financial flows and transactions take place and could be further developed in Viet Nam including the identification of investment requirements and credit needs and channels;

vi. to enable MOFI to forecast, under different assumptions, the future consumption and consumption patterns of Vietnamese fisheries products given different growth rate projections for Viet Nam; and

vii. to strengthen the capacity of MOFI to disseminate the available findings of this project to others interested and identify the needs for possible follow-up activities in the field of fisheries products marketing in Viet Nam.

This section of the report relates to the findings of studies, undertaken to address objective iv above on vertical chain cooperation issues. The main reasons for including this research in the project were the following:

The apparent lack of information at primary producer level (fisherfolk and aquaculturists) about consumer demands in relation to the products forwarded to the sector.

The success of vertical cooperation arrangements in some Western countries such as United Kingdom, Netherlands, United States and Norway in performance improvement of the fisheries products marketing chain.

The opportunities vertical chain cooperation might offers in terms of traceability of fisheries products and quality improvements of the products.

The information reported here was collated from various sources. Desk studies were followed by a large country-wide survey, including interviews with more than 1400 actors in the fishery product chain. In addition, more than 600 people were interviewed in the street on their fish consumption behaviour. To fill the information gaps some in-dept follow-up interviews were arranged with key actors in the chain. All data were collected in a total of 12 provinces (from north to south: Bac Can, Quang Ninh, Hanoi Nghe An, Danang, Khanh Hoa, Dak Lak, Ho Chi Minh city, Ben Tre, An Giang and Ca Mau). Data collection took place between February and June 2002 by staff of the project and of the National Economics University (Hanoi), University of Nha Trang and the University of Can Tho. A database was established and analysis of the data was carried out between July and October 2002 by a team of national consultants, MOFI staff and international FAO staff.

This report consists of four chapters; each dealing with is one of four major outputs from the Fish marketing and Credit in Viet Nam project. Chapter 1 focuses exclusively on the marketing channel of fisheries products. Chapter 2 provides an overview of the current Structure, Conduct and Performance (SCP) of the current marketing chain. The report introduces and discusses the concept of vertical chain cooperation in chapter 3. In chapter 4 the current practices in terms of vertical cooperation in the fisheries products chain are summarised. These findings are analysed as a model for vertical cooperation chapter 5 and resulting guidelines for the practical introduction of improved vertical cooperation and a short conclusions in presented in chapter 6.

The SCP (Structure Conduct and Performance) framework includes the market structure (i.e. the number, size and diversity of participants at different levels), which in turn influences the market conduct (i.e. the reliability or timeliness of activities, control or standardisation of quality, regulatory mechanism). Structure and conduct determine together the performance of the marketing system as a whole (i.e. the technical and allocative efficiency of the market, the degree of market integration, market price and margins, accuracy and adequacy of information flows, etc.).

Market structure is defined as the characteristics of the organization of a market, which seem to influence the nature of competition and pricing behaviour within the market (Bain, 1968). The situation at the consumer market for fisheries products in Viet Nam can generally be described as oligopolistic, as the number of sellers of products is not so large that individual contributions are negligible. Also in many of the other sections of the fisheries products chain the number of sellers at local level is not that high that one could speak of perfect competition. Besides, the products sold are generally not completely homogenous (as quality and species differ), the market knowledge is not perfect and there are sometimes entry barriers.

Section five of the “Fish marketing in Viet Nam: Current Status and perspectives for Development” report showed that horizontal market concentration is high among all actors in the fisheries products marketing chain. Market shares found are, e.g. 79 percent for the highest quintile (the 20 percent largest aquaculturists) of aquaculturists and even over 80 percent for the highest quintiles of wholesalers and processors. In contrast, the lowest quintiles (20 percent smallest actors) present market shares of less than one percent. This large concentration has, of course, its consequences for the competitive behavior at the various market levels.

Market entry barriers were not investigated in detail during the study, but it is clear that especially in the fields of aquaculture, capture fisheries and processing, substantial capital investments are needed. For instance, many of the processing plants were equitized or are in the process of doing so. Those plants processing products for the international market generally had to introduce measures to be able to get HACCP certification. Fisherfolk, dealing with over-exploited inshore fishing areas frequently invested in offshore vessels. Lands suitable for aquaculture gradually became more expensive over the last years. Another entry barrier is the economies of scale related to many wholesale and processing activities, making cost per unit generally lower for larger firms.

Related to the main issue of this report, being vertical cooperation, it is worth mentioning that the current market structure facilitates the establishment and organization of vertical chain cooperation. The high levels of market concentration and the substantial capital costs related to entering different stages of the chain provide some basic conditions that allow vertical chain cooperation to be developed. This is explained in chapter 3.

Market conduct refers to the market coordination mechanisms and the pricing policies used by actors in the chain. In the Vietnamese fisheries products chain one can distinguish some clear marketing channels as was done in elsewhere in this report. It showed that the channel from primary producer (fisherfolk/aquaculturist) via wholesaler to processor is used most often, indicating that wholesalers play an important role in the marketing channel. As far the pricing policies are concerned, negotiation between the actors in the chain was most common (over 40 percent of the cases) and that around 30 percent of the prices are set by looking at the local market prices. In the remaining cases price setting is done by suppliers and/or buyers who make the decision for their business partner. Negotiating power does not seem to increase towards the higher levels in the chain. Nevertheless, a large percentage of processors perceive their power as larger than in other stages of the chain.

With reference to the development of vertical chain cooperation in the Vietnamese fisheries product chain the current market channels provide a valuable departure point. Besides, the common practice of negotiating prices and having frequent personal contacts for this purpose will make it easier to further increase the levels of cooperation between suppliers and buyers.

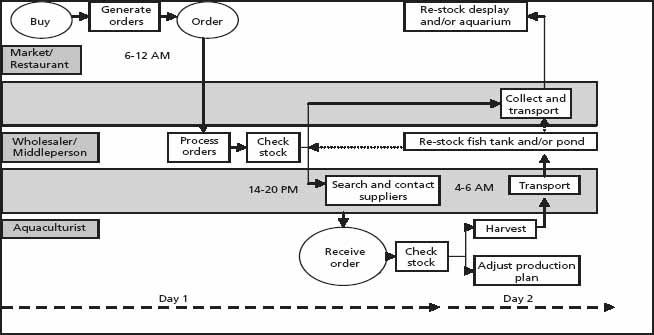

The Event Process Chain (EPC) model (after Kim, 1995) can assist in analysing the market conduct mechanisms and processes in the marketing chain. Its embedded customer orientation and its use of the dimensions time and place make it a useful tool to show the processes in the fisheries product chain. An example is provided here for the aquaculture products marketing situation as was found in the province of Hoa Binh in Northern Viet Nam (Figure 1).

Day 1. At the market place or restaurant the customer/consumer buys an aquaculture product. On the basis of the morning sales at the market, and previous evening and morning sales at the restaurant, orders are generated. Generally, in larger cities, restaurants call their aquaculture/fisheries products wholesaler to place orders; while in the countryside it is common for wholesalers/middlepersons to go themselves or send family members to see how sales are proceeding and ask what should be delivered the next morning.

Orders were compiled by the wholesaler, who checks his stock in the freezer and/or fish tank or pond in the afternoon. If there was sufficient stock he will arrange for transport products to the retailer in the early morning of the subsequent day. When the wholesaler had less stocks they would contact potential aquaculturists to place orders. On their turn the aquaculturists would check their stocks in the same evening or the next morning.

Day 2. Fish were harvested by the aquaculturists and on the basis of stocktaking and harvest; the production schedule was adjusted (less feed inputs, purchase of new fingerlings, etc.). Harvest and transport of produce took place early in the morning, so that retailers at the market or restaurant operators can display fresh (or alive) fish again to customers the same morning. Transport was generally arranged by the wholesalers who restocked their tanks/ponds with the fish obtained from the aquaculturists and transport part of it to the market/restaurants.

Considering the above mechanism certain opportunities for future improvements can be identified, for example:

|

FIGURE 1

|

|

Explanation of the Event Process Chain Model

Branching is conditional splitting of an event-process flow into subflows. Here based on the status of the stocks. |

i. Reduction of the number of events. In the above example the time needed by wholesalers for searching and contacting aquaculturists could for instance be decreased, through working with a number of cooperative and reliable aquaculturists. In addition, direct information provision by the wholesalers on the orders from the market retailers to the aquaculturists could decrease the time requirements for the wholesaler. Probably the re-stocking/stock keeping by the wholesaler can be skipped.

ii. Better agreements on demand and supply between farmer, wholesaler and retailer. This might make it easier to forecast demand and produce species to the specifications desired by the consumers. Orders do not have to be placed anymore for each delivery, but oral or contractual agreements can be made for a longer period; this will decrease the number of events and processes.

iii. Time reduction. The time spend on waiting can be reduced, for instance through the delivery/restock display during the same day in the afternoon/evening. This will allow a decrease in the quantity of fresh fish on the display, shorten the time of fish being displayed and thus make the product reach the consumer in fresher state.

The market performance of the actors in the Vietnamese fisheries products marketing chain can be measured by their returns and their marketing margins. Not surprisingly the study showed that processors generally had much larger annual returns on investment in absolute terms than the other actors in the chain, however, processing companies were often much larger (having sometimes thousands of employees). Of the other actors in the chain aquaculturists generally had on average the largest returns on investment in absolute as well as relative terms. The study also showed that marketing margins for wholesalers and retailers are quite stable over time. Less than half of them frequently changed product sales prices and market margins were generally calculated on basis of the species and the product quality. For instance, the freshwater fish species marketing margin at wholesale and retail levels in inland provinces is generally between 1 000 and 3 000 VND/kg.

There is evidence that long run price integration exists in most fisheries products markets, however, local shortages or over-supplies will cause market prices in one place to differ in the short run from those in other places. Lack of and limited access to market and price information is considered as one of the mayor causes of price differentiation and especially primary producer level actors stress the need for more and accurate information. In chapter 1 of this report this issue of lack of information is discussed further. The importance of vertical cooperation in the fisheries products marketing chain on issues such as price and product information exchange will be made clearer in the next section.

Vertical cooperation is a concept that already as early as in the 1950s appeared in literature on the marketing of agricultural products. In those years the chicken producing sector in the United States went through a period of rapid technological change in breeding, disease control, nutrition and housing (Martinez, 1998). Contractual arrangements between feed suppliers and chicken growers shifted financial and output risks to the feed suppliers. In the period between 1960 and 1985 vertical relationships in agriculture became more and more common. Often farmers, which were not satisfied with their suppliers and buyers, organised themselves in cooperatives to take better care of their own interests. Many cooperatives set up in those days in Europe and the United States still exist, providing member farmers with credit and organising joint marketing for their products. In the fisheries sector cooperative organization models have illustrated their importance. However, globally, a large part of the national fishery sector cooperatives have failed often as a result of a combination of over-emphasis on production, bad management and the individualistic behaviour of fisherfolk general.

At the end of the 1970s and early 1980s transaction costs was a recurrent issue in agri-business. As a result, vertical integration was widely considered as a suitable way to decrease these transaction related costs. Only at the end of the 1980s, under pressure of national and international regulations related to trade and environment, saturated (local) markets and consumer demands for safe foodstuffs, the concept of Supply Chain Management (SCM) was introduced. Many businesses in the agriculture sector (and to a lesser extend in the fisheries sector) and the food industry tried to develop a supply chain for their products, sometimes with great success. A supply chain can be defined as comprising material suppliers, production facilities, distribution services and customers, linked together via a feed forward flow of goods and a feedback flow of information. Especially in the field of logistics, supply chain management has contributed to the performance of individual actors in the chain. As SCM involves an integrated approach to plan and control the flow of goods from raw materials to the final consumer, it does not take adequate account of the fact that chains are being reversed from supply driven to demand led. The latter is especially true for fisheries products as fisheries products are the most internationally traded foodstuffs and consumer demand directs its international trade flows. Moreover, supply chain management involves many other processes (e.g. related to costing, throughput time, fine-tuning of decision making, management, organization, transactions) than only marketing. In view of the fact that it is sometimes difficult to establish a whole supply chain from raw material to consumer in the fisheries sector and as the current reality in the fishery sector should be kept in mind, this report uses the term vertical cooperation, which is widely used in agricultural marketing chains and can be limited to cooperation between just two actors in the chain.

|

FIGURE 2

|

The overall objective of vertical cooperation in the marketing chain is obtaining a larger profit for the participants in this cooperation (Meulenberg and Kool, 1994). Other subordinate objectives may be for instance to increase market share, improve the image of the product, improve product quality and decrease the effects of market failures.

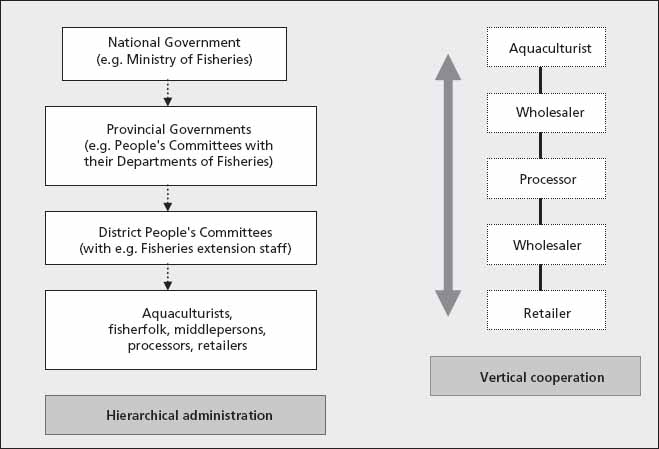

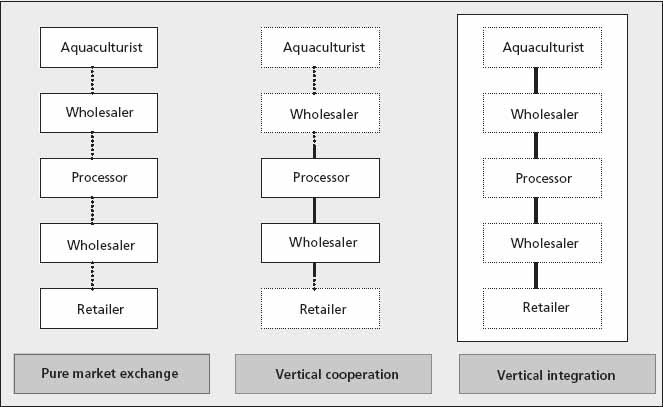

Before continuing it is important to explain that vertical cooperation does not in principle imply any hierarchical relationship or refer to administration of the fishery products channel. Instead, it refers to relationships between actors in the fishery products channel, such as wholesalers, processors and retailers (Figure 2).

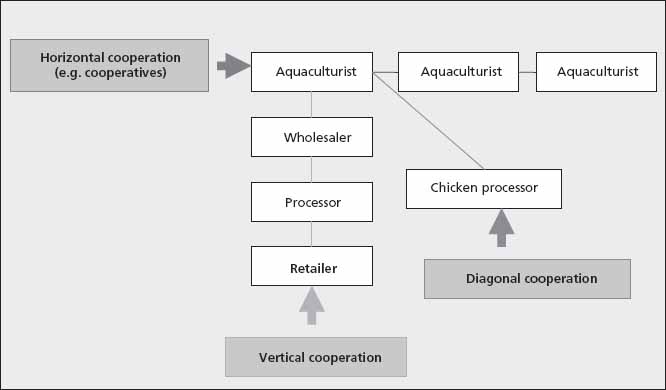

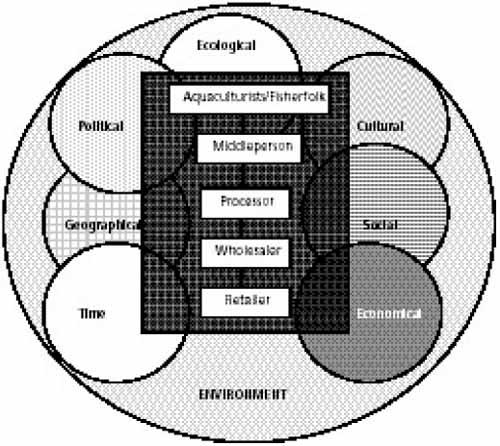

The economic relations in the fisheries products chain were mostly vertical (upor downstream in the chain). However, horizontal and diagonal relations also exist that connect the chain with other chains (Figure 3). A generally used vertical chain is for instance: fish feed industry - aquaculturist - middleperson - fish processor - fish exporter - importer - wholesaler - retailer. Horizontal cooperation is often seen among fisherfolk and aquaculturists, who set up together cooperative style arrangements or establish associations. Examples of diagonal connections were common as well, between channels for different products. One example of diagonal cooperation is for instance the use of chicken slaughter remains from the chicken processing industry as component in the catfish feed used by aquaculturists. Horizontal cooperation relationship can also exist with other product channels, such as between the aquaculture products channel and the chicken channel on issues as the provision of manure from the same level in the chicken (meat) chain to fertilise fishponds as is practised in many VAC (fish/agriculture/livestock) production systems. Other connections exist with research institutes, fisherfolk and aquaculturists associations, banks, etc. Chains were not only connected with other chains but also with other parts of the wider environment (Figure 4). These connections can be considered as integrated part of the wider society (e.g. tax is derived from the sector and used for social services, infrastructure, etc.).

|

FIGURE 3

|

|

FIGURE 4

|

The type of products made by the fishery sector and the demands of the market towards the sector make it essential for close co-ordination between the various links in the fishery chain. As in other agro-food businesses co-ordination within the fisheries products chain is highly relevant. This is caused by the specific characteristics of the market and the production processes used, (Den Ouden et al., 1996) such as:

the perishability and shelf-live of the products,

the variation in quality and quantity caused by genetic differences, seasons, climate, environmental pollution, handling, care for product, etc.,

the variation in production process speed between the processing industry and the aquaculture production,

the scale differences between the various link in the chain, that make vertical integration virtually impossible,

the complementarities of the inputs, what makes it difficult to change the amounts supplied,

the relatively stable demand and consumption of the produce (fish consumption is slowly increasing worldwide),

the increase in consumer consciousness with regard to the product and the production methods influence on health, safety, and the environment,

the intrinsic quality of the fresh products which is highest at the moment of harvest,

the need for capital and knowledge investment that creates some dependence.

The perishability of the fisheries products is key in demanding much of the storage, processing and transport links of the fishery chain (Zuurbier et al., 1996). In addition, the processing of fisheries products for the international market is relatively capital demanding; therefore it is important that continuous supply is guaranteed. Differences in production speed make it difficult to coordinate the various links in the chain and the complementary of products makes it virtually impossible to produce exactly as much as is desired.

The dependency level between the various links in the fisheries products chain is therefore relatively large. By working together it is possible to manufacture those products that are desired by the market, make agreements on their specifications and guarantee quality and quantity of the demanded products (Zuurbier et al., 1996). Transaction costs will be lower in comparison with transactions made via the market. By exchange of information the links in the chain can better anticipate the demands set for the final products, e.g. in the field of availability.

Coordination and cooperation in the fisheries products’ chain can improve the total performance of the chain, especially when taking into consideration the logistical costs, which in the fishery sector often are 50 percent or more of the total value added. In addition, co-operation in the chain can boost product development, as information on consumer demands reaches the lower levels in the chain, and facilitate product differentiation. One can create a more flexible and efficient production process by working together.

Cooperation within the fisheries product chain is increasingly necessary in the light of the following developments:

i. Increasing consumer demand on aspects such as healthiness, food safety, environmentally friendly production processes, biodiversity maintenance, animal welfare, traceability and compliance with international labour laws. In most of the importing countries food security (qualitative and quantitative) at individual level has been achieved and consumers are placing greater emphasis on health and safety of the product. In the beef sector the sudden outbreaks of BSE in cattle, which can cause the deadly Creutzfeldt-Jakob disease in humans, temporarily decreased beef consumption by more than 50 percent in Germany (see www.AD.nl).

Emotional aspects related to food consumption and attention to the way it is produced are gaining importance and consumers are demanding changes in production methods used. Companies exporting to the EU and the United States are required to meet and comply with Hazard Analysis Critical Control Points (HACCP) certification of fish processing to guarantee the quality of the products reaching their people. As controls to obtain the necessary export permits are very strict it is important for processing plants to receive raw products of optimal quality. Vertical cooperation can contribute to the delivery of those fisheries products that are demanded by the consumers.

ii. Rapid technology developments in the fields of products, production processes and information exchange. During the last decade techniques such as Individual Quick Freezing (IQF) and the use of ice slurry in the processing industry have developed rapidly. In aquaculture production the use of genetically modified species has become an issue. New knowledge on fish and shrimp diseases and about organic production processes is changing the opportunities. Reproduction and culture of so-called “new species to aquaculture”, such as groupers is possible only recently. In addition the use of Information and Telecommunication Technologies (ICT) has increased trade possibilities for many.

iii. Increasing capital needs in production and product development. Investments in machinery such as flow freezers and those for IQF requires thousands of dollars but are necessary for modern processing plants to be able to deliver the products desired by the fish consumers. In addition, aquaculturists have to deal with the continuous increase in land (lease) costs; and fisherfolk with the costs of better equipment (e.g. GPS, Fish-finder) to be able to fish offshore as the inshore stocks are over-exploited in many countries. Moreover, processors encounter large capital investment costs for adapting to HACCP standards, while many also consider ISO certification necessary for improving their business.

iv. Increasing diversity in fishery products. To be competitive in the market place for fisheries products and to consolidate or gain market share companies need to diversify in their product range. The diversification in available fisheries products has increased enormously over the last decade, especially through value added production, and an increase in global trade in exotic species (e.g. tilapia, Nile perch, crayfish, prawns).

v. Increasing international competition caused by satisfied markets and trade liberalization. The number of players in the fisheries products market worldwide has increased. Many local traders went international and are increasing the competition. World Trade Organization (WTO), ASEAN and APEC agreements facilitate such international competition. Since information about production and processing techniques is widely available it is attracting many new entrants into the sector who think they are able to make some profit. The newly established fisheries products auctions on the Internet (e.g. PEFA.com, SEAFOOD.com, and GOFISH.com) were a huge success in this respect, attracting already more than 20 percent of the market in some European countries. The recent (2001-2002) trade dispute between the United States and Viet Nam on Basa (Pangasius sp.) catfish exports is just an example of the international competition on the market for aquaculture products It also shows that barriers to trade are still being built and that trade liberalization has positive as well as negative sides.

vi. High risks (e.g. in view of possible detention of products by the EU or the United States customs). As fish is an animal many post harvest biological and chemical processes are taking place in the fish. This implies many potential risks for aquaculturists and fisherfolk that deal with and handle the products. Bad quality products will result in lower prices at the market. In fish and shrimp culture the possibility of disease occurrence implies higher risks. In the year 2001 the mortality rate of the shrimp in Ca Mau province in the Mekong Delta reached 80 percent as a result of diseases. In addition, exporters had to deal with possible detention of the products exported, due to the increasing number of health and safety checks now carried out on fisheries products before they reach the final consumer. Nevertheless, outbreaks of salmonella intoxication, after the consumption of oysters or other fisheries products reach the newspapers every year and damage the image of fish as a healthy product.

vii. High mutual dependency (in view of the specific characteristics of the products). The various actors in the chain of fisheries products have a desire to guarantee supply and demand. Aquaculture and capture fisheries are often seasonal activities and production output levels can vary during the year. One example of mutual dependency is for instance, if the shrimp hatcheries deliver a bad quality Post Larvae (PL) the production of the shrimp farmers will be consequently be lower. On the other side, if shrimp farmers do not manage their ponds well shrimp mortality might be high and that will reflect also on the hatcheries that delivered the product as causes for failure were generally sought elsewhere.

The decision on whether or not to co-operate with other links in the chain depends on the better-anticipated results and performance (Zuurbier et al., 1996). The closeness of objectives between individual actors in the chain is the basis for possible cooperation and will direct the common interests within such a co-operation. Most links or actors in the chain see co-operation on one hand as a necessity but on the other hand as something that will make them more dependent. Mutual benefit is an important reason for cooperation between all actors.

Markets for fisheries products are supposed to bring demand and supply together, in terms of quantity and quality, by means of the pricing system. However, in practice the market is not perfect, especially when considering issues such as competition, information, entry and exit barriers and stability. Uncertainty about demand and supply as a result of a small number of buyers and/or dispersed geographical location of suppliers is fairly common. It is often argued with regard to information that “the larger the number of stages in a chain, and the more geographical dispersed, the more difficult the communication of accurate information will be” (Marion, 1976; Den Ouden et al. 1996). Since the “the modern consumer pays more attention to product quality and origin as well as to the methods of production” (Lehtinen et al., 1998), vertical integration is commonly suggested as a solution to reduce market imperfections and failures.

Vertical integration can be defined as the combination of two or more stages in the production- marketing- chain under a single ownership (Mighell and Jones, 1963; Marion, 1976; De Ouden et al., 1996). There exist important (potential) advantages for fisheries sector companies to vertically integrate. These include:

i. Reduction of transaction costs. Under the Transaction Cost Economics theory, transaction costs can generally be divided in two types: ex ante and ex post (Williamson, 1989; De Mello Brandao Vinholis, 2000). In this respect the ex-ante costs were those that were related to delineation, negotiation and safeguarding agreements, while the ex post costs were those made for monitoring and enforcing agreements. When transaction specific investments need to be made, (e.g. in time, labour and capital), transactions frequently takes place and failures/delays in the transaction are a high risk for the continuance of the production process, it is sometimes advisable to integrate the activity in the own firm (Perry, 1989).

ii. Opportunities for innovations and product differentiation. Such opportunities can be realized through greater control over the increasing number of production stages. “Whereas forward integration gives a firm better or more timely access to market information, allowing a more rapid or specified adjustment of product characteristics, backward integration may allow the firm to obtain specialised inputs through which it may improve or at least distinguish its final product” (Porter, 1980).

iii. Economics of information. The need to collect additional information reduces as information is now available internally (Perry, 1989). The likelihood and duration of exchanges between stages in the chain increases, which decreases the need to invest in collecting and processing information.

iv. Risk reduction. The possibility to control activities in the field of supply decreases uncertainty and makes it possible to keep track of stocks and other inefficiencies (Zuurbier et al., 1996).

v. Improvement of market power. Entry and mobility barriers are elevated through making it necessary for competitors to make higher costs. For instance the fact that there were less suppliers for competitors will make it possible to discriminate with prices and provide quantum discounts. In addition, negotiation power and market power of competitors will be decreased (Zuurbier et al., 1996).

In the Vietnamese Fisheries sector there exist a number of examples of vertical integration. Fish processing companies that have their own fishing fleet and/or carry out aquaculture activities (primarily in shrimp production) were widespread (e.g. Cholimex and Cuulong Seaproducts Company). Vertically integrated companies were often State Owned Enterprises (SOEs), but after equitization many continue with the already developed activities in various stages of the chain. Main reasons for vertical integration are points (iii), (iv) and (v) above. Other vertical integration in the fisheries products chain in Viet Nam is seen in processing when companies go into retail trade (e.g. Seaprodex and Seaspimex) as well (this is called forward integration). These companies have their own wholesale and retail outlets to sell their processed products.

Vertical integration can also lead to disadvantages. These include:

i. High capital investment requirements. “To make vertical integration profitable high investments need to be offset by substantial cost savings, or returns greater than or at least equal to the firm’s opportunity cost of capital” (Buzzell, 1983).

ii. Unbalanced throughput. Unbalanced throughput can result from differences in scale (Den Ouden et al., 1996). The variation in production capacity and production speed will cause that capacity is not always fully used. This means that inefficiencies are to be accepted and that part of the raw materials and partly manufactured products have to be sold purchased/sold elsewhere.

iii. Reduced flexibility. Exiting barriers are elevated as a result of tight technological and design links between the firm’s units and investments in specific processes (Den Ouden et al., 1996). This means that changes in the taste and demand of the final consumer will sometimes require process changes, which will take longer and be more costly to implement than if these were to be incorporated by independent suppliers or buyers.

iv. Increased bureaucratic distortions (Den Ouden et al., 1996). Compared to the markets, which incorporate incentives to restrain bureaucratic distortions, large bureaucratic structures generally lead to less care for new developments.

From the above it is clear that vertical integration has considerable benefits but also implies significant risks and costs. The goal of many companies is to get access to these benefits while minimizing the costs and other disadvantages of vertical integration.

In such cases vertical cooperation, which can be defined as incomplete vertical integration, may be an option. “Vertical cooperation is the alignment of direction and control across segments of a marketing system” (King, 1992) but, in contrast to vertical integration, it does not transfer full ownership and control to other segments in the chain (see Figure 5). While under conditions of pure market exchange control is based at each separate level it is coordinated under vertical cooperation. Under vertical integration control is centrally arranged for all participating stages in the chain. Cooperation generally takes place through better planning, information exchange, quality control, and channel leadership. However, vertical cooperation can have many forms, ranging from cooperation in only one subject to cooperation in almost all activities; which places vertical cooperation somewhere on the continuum between a situation of pure market exchange and vertical integration.

|

FIGURE 5

|

In the fisheries sector in Viet Nam the size differences between often small-scale aquaculturists or fisherfolk and the mainly medium and large scale processing industry means that vertical integration is not often considered an option for improvement of the business. In addition, the high capital investment requires processors and/or wholesalers to become involved in retail (the higher stages in the chain) or fisheries itself (primary production) were generally high. Each stage or segment in the fisheries product chain has its own characteristics and requires specialised technical, managerial and marketing knowledge, thus specialists. It is questionable whether it pays of to hire or obtain all necessary knowledge of the other stages/segments. Vertical cooperation might provide the knowledge and changes needed, decrease costs of information searching, coordinate pricing and make it possible to address the needs of the final consumers better. Use of contracts and other mechanisms, such as franchising, strategic alliances and joint ventures can assist in establishing a fruitful vertical cooperation relationship. Concentrating on certain stages of the chain (e.g. fisherfolk cooperatives and supermarkets) provides a pathway to increase market power and facilitates information transfer from consumer to primary producer and vice versa.

Motives for vertical cooperation may vary among the parties involved in the chain. Primary producers’ motives are generally to secure sales, reduce levels of price variation and decrease risks in production; they generally look for contractual relationships to achieve this. Processors and retailers are likely to be interested in contractual relationships as well; especially because they take higher risks through larger capital investment and require sufficient supply of products (raw materials and processed products) of uniform quality and constant price (Makimatilla and Marttila, 2000).

The number of success stories of vertical cooperation is high and in the agricultural sector these are well documented. Experiences in Netherlands in the dairy, chicken, flowers and meat (Broekmans and Vernooij, 2000) industry, in United States in the pork and broiler industry (Martinez, 1998), in Canada in the swine industry (Srivastava et al, 1998) and in Brazil in the beef industry (De Mello Brandao Vinholis, 1998) all suggest that vertical cooperation can be mutually beneficial for all parties involved. Examples of vertical cooperation within the fisheries and aquaculture sector which can be considered successful are i) The Scottish Salmon Board which executes a comprehensive marketing programme supporting members Quality Approved Scottish salmon, identified by the Tartan Quality Mark in the UK and the Label Rouge in France, ii) the Dutch catfish chain which involves feed producers, farmers, processors, retailers, research institutes and the Dutch fisheries products marketing board, iii) the National Catfish Association in the United States, and the Norwegian chains for salmon and fisheries products.

Alongside success stories there are also various examples of failures of vertical cooperation initiatives. In general, during the process of building up the vertical cooperation parties focus on the economic benefits of working together, such as cost, savings and profits. Understandable as this is, equally important aspects of building and maintaining relationships between the employees of various parties involved often get less attention. Recent studies (Janzen and De Vlieger, 2000; Kumar, 2000) suggest that the importance of social aspects of building vertical cooperation arrangements should not be underestimated. These studies stipulate that trust, information transfer and learning capabilities influence the survival of vertical cooperation to a large extend. While in the start-up phase parties can have similar objectives with the cooperation, these can change with time in a dynamic environment and differences in priorities can make parties decide to stop their vertical cooperation or decrease their level of cooperation. Failures in vertical cooperation arrangements also seem to be caused by i) high and unrealistic expectations of the partners on the benefits/results of the cooperation which often are not met, ii) expectations towards the capabilities and contributions of the partners in the cooperation, iii) partners being competitors at the same time, and 4) threats from the environment (Zuurbier, 1996).

Earlier studies suggest that vertical cooperation arrangements are important because of i) the rapid technological developments in the sector in the fields of production technologies, product development and information, ii) increased demand for capital during the production process, iii) the high competition in fisheries products markets, and iv) the high mutual dependency in the chain.

These issues where also highlighted by the respondents when they were asked about their “main problems encountered in the marketing of their products” and the “areas in which they expect future improvement of their activities”. For example, aquaculturists stressed that low prices (41 percent) and unstable product prices (36 percent) due to high competition, and lack of information on markets and prices (8 percent) were main problems. Main areas where aquaculturists expect improvements were possible are increasing their access to capital, development of suitable aquaculture policies and accessing technological improvements (e.g. breeding, irrigation).

Fish processors stressed the same difficulties in the marketing of their products. Thirty-five percent responded that price fluctuation was their main problem, while 22 percent stressed the unstable supply (thus dependency) and another 22 percent referred to the high levels of competition as the main business related problems. Increasing access to market information (41 percent), accessing capital/credit (27 percent), and increasing the stability of the supply flow (18 percent) were identified as key areas by processors for improving their business

Following aquaculturists and processors, also wholesalers considered low prices for their products (35 percent), high competition (19 percent) and capital shortage (15 percent processors) for improvement of their business as the biggest problems. Wholesalers identified greater access to market information (49 percent) as main area that could improve their business in fisheries products.

In addition, when respondents were asked about the “criteria used for the selection of their suppliers” they frequently mentioned trust, honesty, credibility, friendship, and having good relationships as main criteria for their selection. Frequent communication through visits and by telephone (when distances between partners are large) forms the basis for the development of these relationships. The results highlight that there is a large overlap between what is needed and what vertical cooperation arrangements can offer. Vertical cooperation agreements could partly solve the problems considered as most urgent by the various actors in the fishery marketing chain as well as address some of the areas in which they see opportunities for improvement.

Companies and individuals currently active in the Vietnamese fisheries products chain generally strive to establish and maintain long-term relationships with their business partners. Around 92 percent of the people interviewed (greater than 1300) preferred long-term relationships to short-term market exchange contacts. In addition, commitments to maintaining long-term relationships were similar in the northern, central and southern parts of Viet Nam. Although all the various actors in the fisheries products chain in this study were keen to maintain long-term relationships, wholesalers were most eager to maintain long-term relationships (98 percent) and fisherfolk were least eager (86 percent).

Before going into detail on the reasons behind preferring long term business relationships over short term market exchange contacts it is necessary to get an idea of what activities are currently carried out jointly. Market information exchange is considered important in business relationships and therefore more than three-quarters of the actors interviewed exchange information on markets with their suppliers, buyers or with both. Of the fish processors 98 percent of the respondents in the study mentioned that they exchange market information. Aquaculturists (76 percent) and fisherfolk (89 percent) appear to be a less involved in exchange of market information.

Many actors in the fisheries products marketing chain were also jointly involved in field activities such as handling and grading of products with their suppliers and buyers. Fisherfolk (32 percent) and aquaculturists (38 percent) often do this kind of work jointly with the buyers of their products. As they were primary producers they have fewer responsibilities in this field on the supply side. Fish processors were most cooperative with over 96 percent involved in joint handling and grading of the products (16 percent with suppliers, 20 percent with buyers and 60 percent with both buyers and suppliers). Retailers and wholesalers also jointly carry out activities in this field together with suppliers and buyers (see Annex A).

Storage and transport of fisheries products is generally seen as one of the typical wholesale functions. However, most of the wholesalers do not carry out part of their activities in the field of storage and transport alone, but together with their business partners. Ninety-three percent of the wholesalers said they store and transport products in cooperation with their business partners. In contrast, only 12 percent of the retailers and 6 percent of the processors cooperate with their suppliers in the field of transport and storage. These figures seem to contradict each other, as wholesalers, processors and retailers have direct links and therefore should show less difference here. The difference also shows that cooperation can be regarded differently, depending on the extent of activities carried out and their importance.

The study investigated the exchange of technical instructions and provision of advice on technical issues, as activities, which are usually included in most vertical cooperation relationships. Results showed that wholesalers play an important role in this activity. Ninety percent of the wholesalers stated that they were involved in some kind of exchange of technical instructions and advice with their suppliers and buyers. In contrast, only 13 percent of the aquaculturists and 8 percent of the fisherfolk felt that they were involved in the exchange of such information with the buyers of their products. Although 35 percent of the processors and 84 percent of the wholesalers say they were exchanging technical instructions and advice with their suppliers the perception of the primary producers (who were their main suppliers) was completely different. The latter might mean that the primary producers do not regard the information provided by the buyers as useful, or that the quantity of information provided is not considered significant. In both cases there is a knowledge gap, which should be addressed by buyers as well as suppliers.

Credit is another issue that plays an important role in the vertical cooperation in the Vietnamese fisheries products chain. Fisherfolk and aquaculturists in particular have credit arrangements with their suppliers and/or buyers. As far as aquaculturists concern, 27 percent received credit (mainly in kind) from their suppliers. This credit was mainly provided in the form of fingerlings (for fish) or post larvae (in the case of shrimp). This is generally repaid at the time of harvest. Fifty-three percent of the fisherfolk received credit in kind from their suppliers; such credit generally took the form of fuel, nets or ice. A significant percentage (19 percent) of retailers in fisheries products receive or obtain credit from their suppliers. Generally, retailers only pay for the products supplied by the wholesalers when they were sold to their customers; this means that the suppliers get paid the next time they deliver products to the retailers.

Besides the current levels of cooperation in above fields between actors in the fisheries products chain the study also investigated the reasons for actors getting involved in long-term cooperation. The three main benefits of long-term relationships with their business partners were considered to be i) improved business relationship, ii) increased access to market information, and iii) reduction of costs related to transactions and negotiation, as main reasons for being involved in long term relationships (Table 1). The general importance given to an issue like cost reduction is understandable as well. More importantly access to product quality information and information on quality requirements was considered by aquaculturists, wholesalers, processors and retailers as the main benefit of having a long-term relationship compared with only 9 percent of the fisherfolk. Risk reduction on the other hand was seen by fisherfolk as a very important benefit of long-term relationships with suppliers and buyers.

TABLE 1

Percentage of respondents within the fisheries

products chain that consider benefits as being among of the 3 main advantages of

long-term vertical relationships

|

Benefits |

Fisheries products chain |

||||

|

Aquaculturist |

Fisherfolk |

Wholesaler |

Processors |

Retailer |

|

|

1) Improvement of the existing inter-dependency relationship, with regard to technical information, continuity in supply, financial and social aspects |

61 |

72 |

56 |

49 |

59 |

|

2) The possibility to better respond to consumer demands, e.g. in terms of species, package, size and traceability |

* |

* |

38 |

52 |

35 |

|

3) Increase in access to market information |

50 |

47 |

51 |

61 |

45 |

|

4) Reduction in costs related to transaction, negotiation, time and labour |

47 |

55 |

53 |

48 |

32 |

|

5) Increase in access to product quality information/requirements |

44 |

9 |

48 |

44 |

46 |

|

6) Risk reduction including sharing of risks related to quality of the product, food safety and securing demand and supply |

9 |

36 |

25 |

19 |

32 |

|

7) Increase in access to credit |

28 |

29 |

13 |

7 |

8 |

* as a result of structure of the interviews there no data are available on this issue.

Reasons for not being involved in long-tern relationships were also sought. The main reasons given were: i) the preference of being independent and not wanting to get involved in any dependency relationship, ii) the expected lack of benefits resulting from long-term relationships, and iii) maintaining such a relationship can be time consuming.

A number of issues are important in establishing and maintaining vertical cooperation in the fisheries products chain. Respondents were asked to mark the three issues they consider most important in making vertical cooperation successful. Fair and clear financial accounting of the partners in the chain and responsible behaviour of these partners were considered very important (Table 2). Related to the issue of “good reputation and responsible behaviour” it is noteworthy that much emphasis was placed on trust. Actors in the fisheries products marketing chain search for other actors who they can trust, especially in terms of supplying good quality products. The latter is extremely important for retailers, processors and wholesalers as their reputation is linked to the stable quality of their products and any failure to deliver the demanded quality has its impact on the level of trust. Suppliers generally were eager to take back products delivered that were of bad quality, to keep the relationship with their buyers good.

Almost as important as the above was the timely payment for the services and goods delivered. The results might indicate a problem with current behaviour of the partners in the chain especially in the field of fair accounting and timely payment. Table 2 shows that partners in vertical cooperation consider the provision of mutual financial assistance as important. About a quarter of the processors consider the use of clear contracts and agreements vital, while other chain partners give less priority to this. The latter can lead to problems when starting up vertical cooperation, as some want to use contracts and others might refuse to do so.

TABLE 2

Percentage of respondents within the fisheries

products chain that considers issues below as being among the three most vital

issues for making vertical cooperation in the chain successful

|

Issues |

Fisheries products chain |

||||

|

Aquaculturist |

Fisherfolk |

Wholesaler |

Processors |

Retailer |

|

|

1) Fair and clear financial accounting |

88 |

83 |

86 |

85 |

78 |

|

2) Good reputation and responsible behaviour of chain partners |

81 |

85 |

86 |

93 |

78 |

|

3) Timely payment of debts/quick payments for services delivered |

80 |

72 |

80 |

74 |

75 |

|

4) Provision of mutual financial assistance whenever needed |

24 |

28 |

17 |

11 |

32 |

|

5) Having well defined problem solving arrangements |

13 |

16 |

15 |

10 |

8 |

|

6) Use of clear contracts and agreements |

11 |

10 |

10 |

26 |

8 |

Obstacles to establish and maintain vertical cooperation in the fisheries products chain were also investigated. Main obstacles considered were the unclear identification of costs and benefits for each partner and delays in payment (Table 3). There was a general agreement by all respondents’ on the importance of each of these obstacles.

TABLE 3

Percentage of respondents within the fisheries

products chain that considers issues as being among the three main obstacles in

the establishment and maintenance of the vertical cooperation in the

chain

|

Issues |

Fisheries products chain |

||||

|

Aquaculturist |

Fisherfolk |

Wholesaler |

Processors |

Retailer |

|

|

1) Unclear identification of costs and benefits for each partner |

92 |

89 |

89 |

93 |

85 |

|

2) Delays in payment for services and/or goods delivered |

68 |

69 |

75 |

90 |

68 |

|

3) Insufficient risks and information sharing |

45 |

41 |

33 |

46 |

39 |

|

4) Too much trust in friendship and good relations with partners |

42 |

45 |

35 |

16 |

35 |

|

5) Underestimation of the necessary changes to be made for good cooperation |

38 |

32 |

41 |

41 |

32 |

These findings were not typical just for the Vietnamese fisheries products chain; similar emphasis is also placed in other countries, The study by Skytte and Blunch (1998 analysed the retail buying behaviour in Denmark, Germany, United Kingdom, France and Spain and found that retailers of fisheries products generally place great emphasis on being engaged in long-term relationships and were particularly focusing on obtaining sufficient quantities of product to guarantee that their shelves were full. Suppliers that cannot meet the demand were highly unlikely to trade with a supermarket chain or large retailer. Another interesting finding was that fisheries products retailers highly prefer to do business with suppliers in their own country and that they were attracted by suppliers that offer traceability of the product. The quality of the fisheries products, as it is already expected to be good, was only considered fifth most important by retailers in doing business with their suppliers.

Studies (Lawrence and Hayenga, 2002; Neves et al. 1998) indicate that the use of contracts in many rural sectors has increased dramatically in recent years. Such arrangements have paid dividends, especially in the field of quality and supply assurance. Also, in the fisheries products chain in Viet Nam contracts and other sales and purchase agreements are used in the trade of products between the various actors. Chapter four of the “Fish marketing in Viet Nam: current status and perspectives for Development” report showed that fisherfolk were less used to sales agreements than for instance aquaculturists, processors and wholesalers.

Table 4 shows the percentages of actors in the fisheries products marketing chain using various types of agreements. Verbal sales agreements were most common in the fisheries products marketing chain. More than 70 percent of the aquaculturists and 35 percent of the fisherfolk use such agreements. Such agreements were also common among wholesalers and processors (Table 4). The use of legalized contracts is not widespread; only 5 percent of the aquaculturists and 16 percent of the processors work with legalized contracts.

TABLE 4

Percentage of actors in the fisheries products

marketing chain using various types of sales agreements

|

Marketing chain |

Types of sales agreements |

|||

|

Verbal contract |

Written contract |

Legalized contract |

No contract |

|

|

Aquaculturists |

70 |

1 |

5 |

24 |

|

Fisherfolk |

35 |

1 |

0 |

64 |

|

Wholesalers |

70 (+1*) |

2 |

2 |

25 |

|

Processors |

39 (+11*) |

2 |

16 |

32 |

* Verbal contracts made via telephone.

Apart from sales agreements the use of purchase agreements was also investigated. Similarly, the use of verbal agreements to purchase their products was most common with 68 percent and 21 percent of the wholesalers and processors, respectively, using such arrangements. Legal contracts were used by 3 percent of the wholesalers and 51 percent of the processors in the purchase of their inputs, indicating that processors consider a stable supply of good quality products as very important and want to guarantee this through legal contracts.

TABLE 5

Preferences of respondents (%) for institutions

that should initiate vertical cooperation in the fisheries products

chain

|

Institutions |

Fisheries products chain |

||||

|

Aquaculturist |

Fisherfolk |

Wholesaler |

Processor |

Retailer |

|

|

District extension services |

5 |

3 |

4 |

1 |

9 |

|

Ministry of Fisheries/Provincial Departments of Fisheries (MOFI/DOFI) |

25 |

23 |

8 |

11 |

2 |

|

Fisheries products processors |

6 |

5 |

9 |

8 |

7 |

|

Wholesalers |

21 |

19 |

14 |

9 |

35 |

|

Universities/research institutes |

0 |

0 |

0 |

0 |

0 |

|

Viet Nam Association of Seafood Exporters and Processors (VASEP) |

1 |

0 |

0 |

21 |

0 |

|

VAC VINA |

2 |

0 |

0 |

0 |

1 |

|

VINAFISH |

0 |

0 |

1 |

5 |

0 |

|

Others |

3 |

1 |

2 |

4 |

0 |

|

No idea |

37 |

49 |

62 |

41 |

46 |

|

Total |

100 |

100 |

100 |

100 |

100 |

A number of wholesalers and processors interviewed stressed that they would prefer to have legalized contracts with their domestic suppliers. However, having such contracts would imply that taxation would be easier for the government. Many of them nowadays get visits by the tax inspectors who generally underestimate the current trade (as no evidence of the size of the trade flow is available) and thus the resulting taxation is lower. Another reason for not using written or legalized contracts is that they were often made for a longer term. Current markets (especially the world market, but also the domestic market) for internationally traded fisheries products (e.g. shrimp and catfish) were relatively volatile, at least more than a decade ago. This creates higher risks for wholesalers and processors to sign contracts detailing prices and quantities of supply.

Considering the identified need for vertical cooperation in the fisheries product chain this study examined “who should initiate vertical cooperation activities in the fisheries products chain?” Table 5 shows that MOFI/DOFI, wholesalers and VASEP were considered to be the most appropriate institutions to start such cooperation. Obvious is that a large part of the respondents do not know who should start this cooperation. Moreover, VASEP is only considered by a number of processors as institution to start vertical cooperation; the latter probably due to unfamiliarity with the association outside its target group. Retailers were not mentioned as initiators of vertical cooperation, which is surprising, as they know best the gaps between demand and supply in terms of quantity and quality of fisheries products.

|

FIGURE 6

|

Wholesalers were generally mentioned most as a result of the fact that they were playing a key role in the marketing of fisheries products in Viet Nam. Chapter four of the “Fish marketing in Viet Nam: current status and perspectives for development” report detailed already that most wholesalers were carrying out a large number of functions. They were multifunctional and often collect the products from the primary producers at the farm gate or landing place, carry out the transport, arrange for ice when needed, provide credit to their suppliers, keep up to date on market prices and store and grade the products whenever needed. Having such a diverse range of functions in the chain, and relationships with many actors, it is understandable that wholesalers were considered appropriate initiators of vertical chain cooperation.

As far as the identification of leadership in the chain concerns, it is common practice to look at the price setting mechanism. The current situation in the fisheries products marketing chain in Viet Nam shows that most of the price setting was carried out by negotiation (around 40 percent of the cases). At retail, processor and wholesaler levels price setting by negotiation was the most common practised. Current market prices were also used as a baseline for price setting between various actors in the chain; around one-third of the price setting decision was made based upon market prices. In lower levels of the chain (the primary producer) it is fairly common for decision on prices to be made by the buyer only. This indicates that market power is a bit lower at the primary producer level than at the high levels.

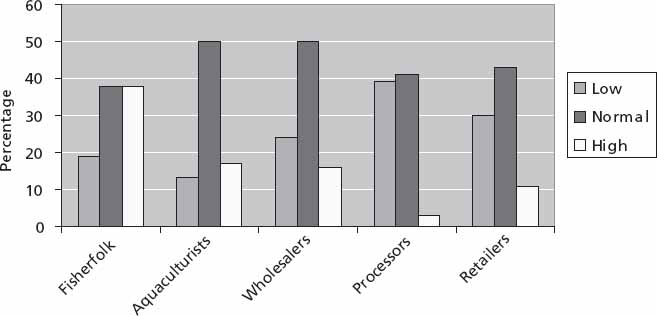

This finding was further confirmed by the “perceived dependency on others in the chain” investigated during the study (Figure 6). This showed that fisherfolk feel significantly more dependent on other actors in the chain than other actors. Thirtyeight percent of the fisherfolk consider themselves highly dependent on others in the chain, while of the processors only two percent does so. Again this indicates that higher levels in the chain, especially processors and retailers, were less dependent and might be considered as relatively more powerful.

Vertical chain cooperation does not necessarily have to change the power structure in the chain; however it often does so. It is difficult to forecast what will happen within the Vietnamese fisheries products marketing chain if vertical cooperation increases. First of all, it will depend on who will take the lead in initiating new initiatives in this field, which will join and who not, and to what extent cooperation is sought. Chain leadership will bring responsibilities and plights next to its advantages; issues as power and levels of investments in the cooperation were to be taken into consideration.

Due to the requirements for communication (time, manpower and money) it is often considered suitable that larger sized actors (such as processors, wholesalers and retailers) take the initiative of starting vertical cooperation.

During the study it was found that vertical cooperation between actors in the Vietnamese fisheries products chain has already taken place; often in an informal way, based on trust and friendship. However, it was also found that there still exists a need for further cooperation. This suggests that current cooperation levels and issues considered were insufficiently in addressing their needs. Causes of the gap between considered needs and the current situation might be partly linked to cultural and traditional aspects. Some relevant aspects are the following:

Fisherfolk in Viet Nam, and in many other countries, appreciate their independence and were generally quite individualistic in their behaviour. This is one of the reasons why fisherfolk cooperatives often fail. It also means that fisherfolk hesitate to get involved in dependency relationships. Besides, past negative experiences of fisherfolk with wholesalers and processors have often made them less confident in establishing better coordination or cooperation, as they fear they would be cheated or be worse off by doing so.

Moreover, information on freshness, quality, technologies, quantity of product available, markets and prices is considered as the basis of power. Instead of exchanging information it is often hidden and only used when one can directly benefit from it. Therefore much of the information available at both ends of the fisheries products marketing chain never flow the other end.

The development of a model for vertical chain cooperation in the fisheries products chain was one of the aims of the study. Theory generally stresses that cooperation in the chain will benefit the actors involved. Based for this conclusion various theories may arise such as:

i. Transaction cost theory that stipulates that advantages can be obtained by limiting the time and costs involved in transactions between actors in the chain. Cooperation can create synergies (Williamson, 1989).

ii. Game theory which shows that all actors will benefit from cooperation as long as they adhere to their mutual agreements, but will be worse of as well when agreements are harassed (Bandyopadhyay and Divakar, 1999).

iii. Competition theory that stresses the use of cooperation in improving own competitiveness and decreasing the competitiveness of others. A chain can be used as tool for the construction of entrance barriers (Zuurbier et al., 1996).

iv. Network theory focusing on the reciprocity within relationships, stressing the fact that one actor is dependent on resources controlled by another and that there are possibilities for gains by pooling of resources (Powell, 1990; Omta et al., 2002).

v. Competency theory which states that actors have to focus on those activities in which they have competitive advantages/knowledge and should contract out all activities in which they are less competent (Zuurbier et al, 1996).

vi. Information theory that emphasises that markets fail in delivering quality information to the various actors in the chain as well as to the final consumers. Imperfect and asymmetric information can be (largely) solved by cooperation in the chain (Kola et al, 2002).

Willingness to become engaged in vertical cooperation generally relates to the above issues. However, the sort of vertical cooperation can differ to a great extent. Contents, solidity and form of the cooperation depend on the goals, priorities, means, strategies and knowledge available among the partners involved in the vertical cooperation.

Generally, the desire to increase cooperation in the chain starts with one actor who tries to interest other actors for such cooperation. In the Vietnamese fisheries sector this often happens in a fairly unstructured way, using informal approaches and focusing on just a few of aspects that could be included in this cooperation. This approach can work, but chances of failure might be larger. In the following paragraphs a stepwise approach is proposed that could lead to higher chances of success. This approach starts with an internal preparatory phase and ends with the establishment of the chain (after Zuurbier, 1996).

Phase A: Internal preparatory phase

A1. Goals, strategies and benefits

Before approaching partners an internal preparatory phase is needed to clearly define what benefits the actor wants to get from cooperation. Questions should be asked such as: What are the goals and strategy? Why does the actor want to engage in chain cooperation? and are there sufficient means available, and will they be made available, for the preparation of chain cooperation?

A2. Setting up an internal preparatory team

Once the actors have got answers to above questions an internal preparatory team for cooperation can be established. In this case it is assumed that the actor interested has various persons working for him/her. For instance, if the actor were a fisheries products processor it would be advisable to include people from various disciplines in the team (e.g. marketing, R&D, quality control, management). Researchers, and those working on promotional activities should also be on the team. The people joining the team should be competent and have the support from management as otherwise efforts are doomed to fail. Instead, VASEP should take up the role of initiator to manage chain cooperation staff. Additionally, considering the number of staff of many fisheries products wholesales team will normally be very small and might consist of just two people.

A3. Investigating the internal and external support

The preparatory team should then investigate the internal and external support for cooperation. Internally, people whose jobs might be under threat when getting engaged in vertical cooperation will probably be adversaries to the team. Identification of the main stakeholders for future cooperation is necessary. These stakeholders should be informed of the activities of the team. Consequently, those stakeholders who are not convinced of the need for cooperation need to be persuaded. In larger companies it is important that the team sets up communication lines; these lines should be used to raise awareness among stakeholders and motivate them to support vertical cooperation activities.

A4. Planning for and by the preparatory team

Management should make sure that planning for and by the preparatory team is realistic, in terms of time, quality, budget available and the expected results. The team will try to produce a preliminary plan of chain cooperation and anticipate the formation of a vertical chain cooperation team with other actors in the chain.

Phase B: Situational assessment

B1. Clarity strategies and goals of potential partners

Before a potential partner in the chain cooperation is approached it is important to investigate whether the overlap with those of their own company. Questions should be raised, such as ”How do competences of potential partners contribute to the own organization? and “Is there relative dependence between partners? The potential partner’s competences should be complementary to the actors’ own activities. Related to the “strategy” issue, differences between partners are for instance: a focus on domestic -export markets, wide range of customers-niche market, low quality-high quality products, etc.

B2. Compatibility of company cultures

In addition, one should think about the partners’ company culture. Are the cultures similar? The latter is quite important, as culture differences between State Owned Enterprises (SOEs) and equitized companies can be large; especially when companies are foreign owned and have foreign management. Japanese management cultures are substantially different from those in the US or Europe and also Vietnamese managers have their own style. To make vertical cooperation successful cultures of partners should fit, or at least not be very different.

Phase C: Search for and selection of partners

C1. Identification of appropriate partners

Having carried out the general assessment it is important to actually start searching for the right partner. Generally the actor willing to initiate the vertical cooperation has some ideas of possible partners, through earlier or current trade experiences, but parts of the necessary information on the potential partners’ capacity and willingness to join in the initiative are lacking. Some of this information might be obtained from external sources, such as MOFI, VASEP, databases and Chambers of Commerce. Before contacting external sources and potential partners it might be useful to produce a checklist of questions to be answered and information to be collected. The ultimate goal here is to use the information for the development of potential partner profiles, which can be used during the search.

C2. Criteria for selecting partners

In addition, one should define the criteria on which selection will take place. The above seems obvious, but a number of vertical chain cooperation initiatives have failed because companies only looked at those actors in the chain they had already a relationship with; ignoring the fact that other actors might be more appropriate for such cooperation. On the other hand, joint norms and values, trustworthiness, reliability and responsibility of potential partners are very important and should be considered as such among the criteria for selection.

C3. Complexity of vertical chain

Vertical chain cooperation does not necessarily need to involve all stages in the chain from primary producer retailer. It could be limited to just two stages. Although it seems most interesting to have the complete chain included it is important to be realistic; thus not trying to include stages/partners that are not ready (yet) for such cooperation. As discussed before, size and capacity of the potential partners does significantly impact the functioning of the chain to be established. It might be easier to start with a few partners and approach others at a later stage when the established cooperation has proven its success.

C4. Involvement of partners in the chain

When having selected one or more partners, they should be approached in the most appropriate way and their willingness to join and commitment to vertical cooperation has to be discussed. Informal ways of approaching potential partners are used most and as a number of partners in the Vietnamese fisheries products chain are relatively small sized (e.g. aquaculturist, wholesalers) it may be easy to use existing relationships/friendships.

Phase D: Establishment of the chain

D1. Organization and structure of the chain

Assuming that the partner(s) agree and like the idea of getting involved in or strengthening their vertical cooperation it is important to define together the organization and structure of the chain. Therefore a chain cooperation team is generally used. Such a team consists of competent staff of each of the partners and starts with identifying the criteria that are seen as important by the partners. Issues as commitment from each of the partners, the task to be carried out, timeframe and approach to be followed, leadership and procedures for communication will have to be discussed.