Sisal and henequen: a marked recovery in prices in 1993

World output of sisal and henequen fell below 350 000 tonnes following the decline of 1992. This continued the long term decline to the lowest level for decades. The contraction reflected a drought in Brazil which reduced production by 23 percent to 150 000 tonnes in 1993. In Africa, the other major sisal producing region, producers responded to the more remunerative prices of 1993, and their output rose 13 percent to 87 000 tonnes in 1993. Kenya and Tanzania increased their production by close to 20 percent. Expansion in China was reported, and production may now be around 40 000 tonnes annually. In Mexico. the henequen industry continues to be affected by the cessation of subsidy payments and production remained static.

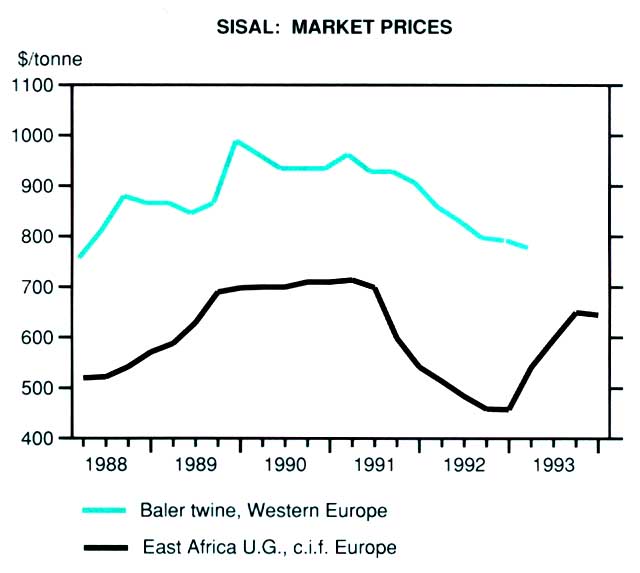

Reduced production, evident from late 1992, was reflected in international prices for sisal fibre which rose in 1993 to levels close to those of 1991. Between October 1992 and mid-1993 quotations for East African 3L fibre rose from $470 to $690 per tonne and for UG from $440 to $620 per tonne. There was, however, some decline later in the year. Brazilian fibre, likewise, increased in price from as low as $314 per tonne in October 1992 to around $500 per tonne late in 1993. In contrast, sisal baler twine prices declined even further in 1993, especially in the United States which had previously paid prices above those in Europe. In both the United States and Europe, sisal baler twine sold at prices notably below $16 per bale. This reflected strong competition with polypropylene twine. Overcapacity, prevalent in polypropylene manufacturing for some years, drove down the price of polypropylene resin in Europe from Dm 1.5 in 1990 to as little as Dm 1 per kg during most of 1993.

The lift in prices for fibre in 1993 reflected shortfalls in production rather than increased demand. Import demand for fibre and for manufactures by most countries remained depressed. In particular, there were virtually no sales to countries of the former USSR in 1992 or 1993. and sales to other countries have been affected by continuation of economic recession. In addition, each year less and less sisal is used in haymaking. In Europe in particular, even in 1991 and 1992 when the total consumption of harvest twine expanded, sales of sisal twine continued to decline while polypropylene gained.

In 1993, global exports of fibre recovered by 11 percent and manufactures 3 percent despite the decline in production. In Brazil, stocks were drawn down and shipments of fibre expanded by 30 percent, although shipments of cordage declined a little under the continuing impact of a 25 percent duty on imports into the EC. Export availability in East Africa increased with production, and while Tanzania's sales of both fibre and manufactures expanded, Kenya's remained static. As a result of the expansion in the volume of world trade coupled with revived prices for fibre, the value of the fibre traded increased by 13 percent to $35 million. The value of sisal and henequen manufactures traded, however, declined by 7 percent to $88 million.

Sisal fibre prices likely to decline with enlarged volumes in 1994

The recovery in prices evident in 1993 stimulated producers in Tanzania and Kenya to expand production. Further recovery in production was expected once Brazil recovers from the drought of 1993. Any such increase in the supply of fibre on world markets would lead to falling prices in the absence of growth in demand. However, at the start of the 1993/94 twine season fibre prices were considerably higher than 12 months earlier putting upward pressure on those for twine. Yet, the price increases for sisal twine would be constrained by the depressed price of polypropylene raw materials and twine and the long-term shrinkage of the market for sisal harvest twine.

The volume of fibre traded was likely to increase further in 1994. However, the impact on the value of exports would be reduced by a likely decline in prices. The longer term outlook for exports of sisal is for continuing decline in the market for harvest twine. Any growth is expected to be limited to nontraditional outlets including, perhaps most notably, papermaking. It is, however, likely to be some years before growth in these areas will more than offset the depression in long standing applications.

Abaca: prices remain relatively high

Production of abaca in the major producing country, the Philippines, expanded as producing regions recovered from drought, but this was partly offset by a decline in production in Ecuador. Some further expansion is expected in global abaca production in 1994, in response to continuation of remunerative prices, and as new plantations in the Philippines come into production.

Growth in global demand for abaca for tea bag production and other specialty uses continued in 1993, despite slow economic growth in many major consuming countries. However, total shipments remained static at 49 000 tonnes, constrained by availability. Trade in fibre continued to be displaced by that in pulp. Shipments of pulp from the Philippines to Germany, in particular, have increased in the early 1990s. This trend is likely to continue as costs in the Philippines are lower than in the consuming countries and the government encourages domestic processing. Exports of cordage increased in 1993, but it is not expected that the long term downward decline in the cordage trade will be reversed.

The price increases obtained in 1991 and 1992 were maintained in 1993 reflecting a continuation of increased demand and producers' difficulties in expanding production. However, in the second half of the year prices declined somewhat following a depreciation of the Philippines peso. The global value of exports of abaca fibre and manufactures increased by 6 percent to $87 million in 1993, the result of an increase in the value of products being partly offset by a decline in the value of fibre traded. Should attempts to increase production in the Philippines in 1994 be successful, prices were expected to move downwards and allay producers' fears that synthetics may encroach on the market. The increased level of demand was likely to be maintained.

Coir

World production of brown coir fibre expanded by a further 4 percent in 1993 as a result of diverse trends in the major producing countries. India's production increased by 12 percent, while Sri Lanka's contracted. This continued the pattern of recent years when growing domestic demand sustained India's industry while foreign demand for Sri Lanka's export-dominated production declined. India's production is expected to increase further in 1994.

The decline in exports of coir fibre, mainly from Sri Lanka, continued and was 7 percent in 1993. However, some recovery in prices of twisted and mattress fibre in 1993 offset the lower volume traded and maintained export earnings.

World output of coir yarn increased steadily over recent years to reach 174 000 tonnes in 1993, with an increasing proportion made from decorticated fibre. India's production of retted white fibre yarn has remained stable at around 127 000 tonnes for a number of years, most of it for domestic use. Exports of yarn from India declined markedly in 1992 and fell further in 1993, while those of Sri Lanka, which also fell in 1992, expanded a little in 1993. In total there was little change in the volume and value of exports of yarn. By contrast, the volume and value of exports of coir mats, mattings and rugs from India, expanded further in 1993, following a recovery in 1992. Nevertheless, coir continued to face strong competition from synthetics in its traditional uses. The only long term expansion of demand was likely to come from the expansion of new uses such as geo-textiles or from a revival of demand for traditional products based on the environmental appeal of natural fibres.

Production

| 1988-90 Average | 1991 | 1992 | 1993 | ||

| ‘000 tonnes | |||||

| Fibres | |||||

| Sisal and henequen | 416 | 418 | 371 | 334 | |

| Brazil | 225 | 220 | 195 | 150 | |

| Kenya | 38 | 40 | 34 | 40 | |

| Tanzania | 33 | 36 | 24 | 30 | |

| Abaca | 73 | 75 | 72 | 73 | |

| Coir fibre (brown) | 166 | 179 | 189 | 196 | |

| India | 74 | 93 | 102 | 112 | |

| Sri Lanka | 81 | 76 | 78 | 75 | |

| Coir yarn1 | 124 | 152 | 162 | 174 | |

1 Including yarn from brown fibre.

Value of exports

| 1988-90 Average | 1991 | 1992 | 1993 | ||

| Million $ | |||||

| Fibres and products | 286 | 270 | 260 | 264 | |

| Fibres | |||||

| Total | 118 | 90 | 80 | 82 | |

| Sisal and henequen | 62 | 41 | 31 | 35 | |

| Brazil | 35 | 18 | 9 | 11 | |

| Kenya | 15 | 12 | 11 | 12 | |

| Tanzania | 4 | 2 | 3 | 5 | |

| Abaca | 26 | 26 | 26 | 25 | |

| Coir fibre | 19 | 12 | 15 | 15 | |

| Coir yarn1 | 12 | 11 | 8 | 7 | |

| Products2 | |||||

| Total | 168 | 180 | 180 | 182 | |

| Sisal and henequen | 103 | 108 | 95 | 88 | |

| Brazil | 64 | 70 | 62 | 54 | |

| Tanzania | 10 | 8 | 10 | 11 | |

| Abaca | 42 | 45 | 56 | 62 | |

| Coir | 23 | 27 | 29 | 32 | |

1 Including yarn from decorticated fibre.

2 From fibre-producing countries.

Exports

| 1988-90 Average | 1991 | 1992 | 1993 | ||

| '000 tonnes | |||||

| Fibres | |||||

| Sisal and henequen | 139 | 87 | 78 | 87 | |

| Brazil | 83 | 45 | 31 | 40 | |

| Kenya | 31 | 24 | 31 | 30 | |

| Tanzania | 8 | 4 | 4 | 5 | |

| Abaca | 34 | 31 | 27 | 25 | |

| Coir fibre | 76 | 69 | 71 | 66 | |

| Sri Lanka | 66 | 60 | 62 | 58 | |

| Coir yarn1 | 18 | 19 | 15 | 15 | |

| Products2 | |||||

| Sisal and henequen | 133 | 124 | 112 | 115 | |

| Brazil | 80 | 78 | 70 | 68 | |

| Tanzania | 15 | 17 | 14 | 19 | |

| Abaca | 21 | 22 | 23 | 24 | |

| Coir | 13 | 14 | 14 | 17 | |

1 Including yarn from decorticated fibre.

2 From fibre-producing countries.

Prices: fibres1

| 1988-90 Average | 1991 | 1992 | 19932 | |

| $/tonne | ||||

| Sisal | ||||

| East African UG | 632 | 639 | 479 | 570 |

| East African 3L | 696 | 667 | 509 | 625 |

| Brazil N.3 | 511 | 400 | 370 | 450 |

| Abaca | ||||

| S2 | 1 253 | 1 407 | 1748 | 1 860 |

| G | 1 023 | 1 123 | 1583 | 1 640 |

| JK | 840 | 875 | 1052 | 1 240 |

| Coir | ||||

| Omat. twisted | 497 | 460 | 400 | 450 |

| Mattress, f.a.q. | 237 | 266 | 250 | 300 |

1 C.i.t. European ports.

2 January to July.

{kind=link}