![]()

![]()

![]()

Scope of the study

Data and Assumptions

Synthesis of Scenario Results

The Asia-Pacific region is being rapidly transformed by fast economic development and population growth. Patterns of forest resource utilization and the manufacture and trade of forest products have changed dramatically in recent years, and will continue to evolve in response to these economic and social forces.

This report examines the evolution of the solid-wood industries of the forest sector of the Asia-Pacific region from 1995 to 2010. Three scenarios are considered: a base case scenario reflects the current supply and demand conditions of the region, and the current industry structure and trading relationships; a second scenario examines conditions of scarcity of supply from the natural forest; and the third scenario combines scarcity conditions with stronger end-product demand.

These scenarios are analyzed with the International Tropical Timber Organization Asia-Pacific Tropical Timber Trade Model. The major ITTO producing countries of the region are represented in the model: Indonesia, Malaysia (Peninsular Malaysia, Sabah, Sarawak), Myanmar, Papua New Guinea, and the Philippines. The model also includes the ITTO consuming countries: Japan, Republic of Korea, People's Republic of China, Taiwan Province of China, and Thailand. Cambodia, Laos, Vietnam, and the Solomon Islands are also included on the producer side of the model, while Hong Kong and Singapore are included as consumers. Other countries normally considered to be in the Asia-Pacific region - such as India, Pakistan, and Bangladesh - are not included in this study.

The scope of the study with respect to forest products is limited to the current capabilities of the trade model. Only logs, sawnwood, and panel products are considered. Plywood and veneer are aggregated in the model and the ensuing analysis. Pulp, paper, and remanufactured products are not included. Secondary manufacturing and reconstituted panels (particle board, medium-density fibreboard, and oriented-strand board) are considered only in the projection of demand, and are not represented explicitly in the model.

Data sources

The primary data sources for this study are the reports documenting the development of the ITTO Trade Model and its attendant database (ITTO 1993, 1995), and the most recent annual statistical review of the ITTO (ITTO 1996b).

Log supply

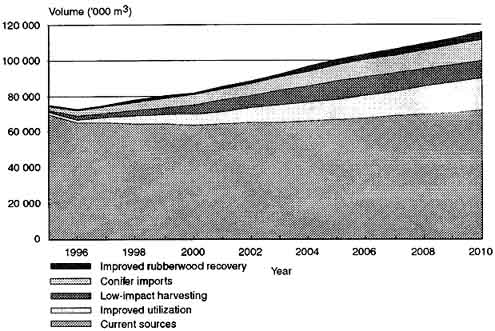

Short-term tropical log supply is represented as a supply curve for each supply region, with four "incremental log" supply sources: improved roundwood utilization, non-conventional harvesting regimes, improved recovery of estate crops, and imported conifer logs. Figure El charts the maximum potential timber harvest from each supply source from 1995 to 2010.

Product demand

Demand curves are also defined for each demand region and demand growth is estimated separately for each demand region in the study (Table El); the aggregate annual growth rate estimated for the Asia-Pacific region is 2.8%.

Product and technological substitution

Substitution of different products (e.g., reconstituted panels for plywood) or technological substitution at the consumer level (e.g., acceptance of building technologies that use wood more efficiently) will dampen demand growth for tropical lumber and plywood in the region. This study assumes that product substitution will replace the consumption of 30.5 roundwood equivalent (RWE) million m3 of plywood and 11.7 RWE million m3 of sawnwood over the study period.

Figure E1 - Potential supply levels to 2010 under the Base Case scenario

Table E1 Average annual growth of consumption to 2010

|

Group |

Category |

Country |

Growth Rate to 2010 (%) |

|

I |

Less developed, importers |

China, Hong Kong, Philippines, Singapore Thailand |

4.4 |

|

II |

Less developed, exporters |

Cambodia, Indonesia, Laos, Malaysia, Myanmar, PNG, Solomon Islands, Vietna |

4.0 |

|

IV |

More developed, importers |

Japan, Korea, Taiwan Province of China |

1.1 |

Country assignments as per Jacques (1996). No category III countries (more developed, exporters) are located in the region.

Natural forest log scarcity will be offset

Although harvest forecasts from current sources may be optimistic, sufficient incremental log supply will become available to avoid scarcity through improved utilization of current log sources, low-impact harvesting of sensitive sites, and the importing of conifer logs.

Hardwood log trade will decline

Hardwood log trade will decline across the region, and several more ITTO producer countries will become net importers by 2010.

Malaysia becomes an importer of logs

The volume of trade in hardwood logs will decline as Sarawak and Sabah progressively curtail log exports. However, Malaysia, principally Peninsular Malaysia, is already an importer of hardwood logs. This trade will grow over the study period, with most of the processing meeting demand for domestic consumption or further processing as value-added products.

Indonesia becomes a net log importer

Indonesia discourages log exports and is considering log imports from Vietnam, Myanmar, and the Solomon Islands to offset declining log supplies. Log imports are likely to increase during the study period.

Papua New Guinea will probably continue to export logs

Papua New Guinea's current policy is to reduce log exports by 10% each year for the period 1995-2000, and ban log exports thereafter. However, the domestic processing industry is generally non-competitive relative to other exporters of the region, and may be unable to absorb a significant increase in log supply. Consequently, log exports will likely persist well past 2000 and may even expand. Log exports from Papua New Guinea will compete with highly competitive log and product substitutes; significant price increase is unlikely.

Myanmar and Vietnam have an export opportunity

Myanmar and Vietnam have an opportunity to expand their log exports in the short term as the major exporters curtail their trade.

Conifer logs imports will expand

The region will import substantial volumes of conifer logs to provide substitutes to tropical logs in the manufacture of sawnwood and plywood, and the raw material for manufacture of substitute products such as reconstituted boards and panels.

Manufacturing will relocate to producer countries

Relocation of manufacturing capacity away from the consumer countries to the producers has been underway for some time, and will continue throughout the study period. This shift is due partly to normal market forces: the higher cost of manufacturing in consumer countries makes the producer countries more competitive and the manufacturing capacity in the producer countries is becoming more efficient. Relocation will also be accelerated by policies, such as constraints or bans on the export of tropical logs, or slowed by import tariffs and non-tariff barriers.

Sawnwood manufacturing will increase

Sawnwood manufacturing will increase in the producer countries, largely in response to growth in domestic demand and the development of secondary manufacturing for export. The same economic fundamentals will result in the manufacture of conifer sawnwood in the producer countries, making hardwood sawlogs available for manufacturing products for export.

If sawnwood manufacturing is to increase in consumer countries, it will be based on imported conifer logs, at least for lower-end products.

Plywood manufacturing will decline

Plywood manufacture will decline across the region as the supply of peeler-quality logs declines and consumers adopt reconstituted panels.

Manufacture of substitute products will expand

While substitute products will be imported from outside the region, new capacity will also develop within the region to manufacture substitutes, especially reconstituted boards and panels. The increasing supply of conifer logs and small logs resulting from intensive utilization of current log sources are attractive sources of raw material. New capacity to manufacture substitute products from underutilized fibre from current sources will most likely be established near their source of supply in the producer countries. However, new capacity based on conifer logs may be established in producer or consumer countries.

Sawnwood and plywood trade decline

Although processing capacity will shift to the producer countries, the overall trade in sawnwood and plywood will decline.

Substitute products trade increases

With new manufacturing capacity for substitute products being established in the producer countries, the trade in substitute products will expand in the region.

Prices will remain stable

Although demand will continue to be strong in the region and the harvest from the natural forest is at, or above, its long-term sustainable level, this analysis demonstrates that product and technological substitution could cause real prices to remain stable, or even decline, over the study period. This result is sensitive to the rate of product substitution accepted by consumers and the rate of growth in demand for tropical timber solid-wood products.

![]()

![]()

![]()

{kind=link}