No.5  December 2008 December 2008 | ||

|

Crop Prospects and Food Situation | |

|

National food price review1/

International cereal prices have fallen sharply from their record levels reached in mid-2008 but in many developing countries they remain high and continue to increase despite the various policy measures taken by governments to limit the impact of high international prices on domestic markets. In countries where prices have declined the reductions have been modest compared to those in export markets and, generally, national cereal prices remain above their levels of a year earlier. Persistent high food prices in the developing world continue to affect access to food of large numbers of vulnerable population in both urban and rural areas. Given the precarious food security situation in many countries because of the sharp increase in food prices in 2008, continued monitoring of prices of staple foods in national and local markets is needed in 2009.

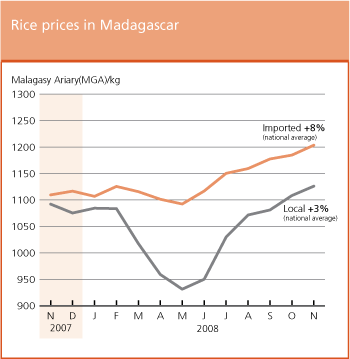

Prices of maize, the main staple food in the subregion have continued their upward trend in most importing countries, such as Mozambique and Zimbabwe, in spite of the stable or declining trend in South Africa, the regions main exporter. Prices in South Africa are following the international price pattern and have declines since July 2008. The decline is steeper in US dollar terms with significant devaluation of the Rand than in local currency. In most importing countries of the subregion the demand for maize on markets is high during this lean period when farmers own stocks and supplies are being depleted. The slower pace of imports, compared to last year, may also be a contributing factor to the high domestic prices in these countries. Elsewhere, prices have stabilized in the past months in countries that have reached self-sufficiency in maize in marketing year 2008/09 (April/March), such as Malawi and Mozambique; however by November 2008 in markets of these countries capital cities prices of maize remained 107 and 73 percent higher than a year earlier. These increase are higher in local currency terms. In Madagascar prices of rice, the main staple food, need watching carefully as they have been augmenting since the immediate post-harvest period, increasing 22 percent from June to November, and the country is heading into the lean period until the next harvest in May. Further increase of rice prices could result in a critical food situation like last year.

Coarse grains prices have started declining in September, reflecting the arrival of bumper harvests into the markets; however, by November 2008 prices remained well above the levels of a year ago. For example, despite significant decreases in recent months, millet prices in markets of Mali (Bamako), Niger (Niamey) and Burkina Faso (Ouagadougou) were still 23, 15 and 43 percent respectively higher than in November 2007. In general, domestic prices of non tradable crops such as millet and sorghum are driven by national and regional factors and fluctuate according to local supply and demand, greatly influenced by erratic weather conditions. The situation is different for rice prices which are determined by world prices and have exhibited high pass-trough from the international market. In Senegal, Niger and Burkina Faso rice prices continued to increase, being 85 percent higher in Senegal in September and 44 and 65 percent respectively higher in Niger and Burkina Faso than a year earlier. These increases occurred despite a series of measures implemented by governments aimed at offsetting the impact of higher world prices, including waiving of import tariffs and food distributions. In most francophone countries of Western Africa no impact was observed on prices due to the relatively low initial tariff level and the recent depreciation of the CFA (which is pegged to the Euro) against the dollar. By contrast, the Nigerian Government reduced import duty on imported rice from 100 to 2.7 percent for 6 months, up to 31 October 2008, targeting the importation of not less than 500 000 tonnes of milled rice. A significant price decline was observed in markets in Nigeria between May and September 2008 (for example 16 percent in Bodija market, Ibadan) due to the initial level of the tariff and the appreciation of the naira.

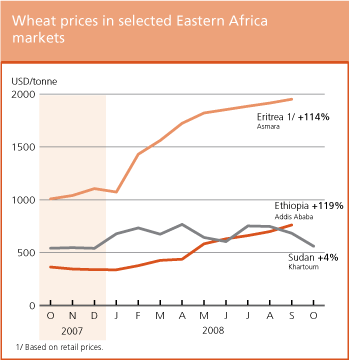

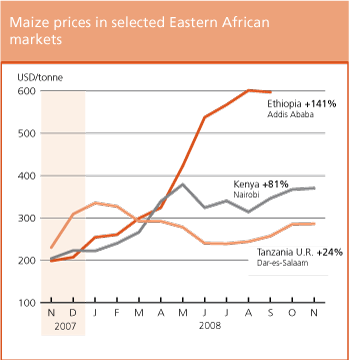

Throughout the region, food prices have generally increased in the past months and are at above-average levels for this time of year. In Eritrea, prices of the main staple wheat in Asmara have been increasing since the beginning of the year and by September had almost doubled the price prevailing a year earlier. In Ethiopia, the price of the main food staple maize in Addis Ababa was quoted at USD 600 per tonne in September 2008, nearly three times higher than its quotation in September 2007. The harvesting season of coarse grains has just begun and some decline in prices is likely to occur. In Sudan, the price of the food staple sorghum in Khartoum was quoted at USD 406 per tonne, which was more than double the price in October 2007. The harvesting season of coarse grains is also underway in Northern Sudan and a decline in prices is expected. In Kenya, the price of maize in November 2008 in the Nairobi market, quoted at USD 370 per tonne, is bouncing back to the peak of USD 379 reached in May 2008 and is 81 percent higher than in November 2007. Similarly, the price of maize in the Mombasa market in October rose back to USD 370 per tonne, exceeding the previous peak of USD 363 per tonne last June. In the United Republic of Tanzania, the price of maize, which began to steadily decline in February/March 2008, following the maize harvest in the southern lowlands, has increased since July. In November, the wholesale price of maize in Dar-es-Salaam averaged at USD 286 per tonne, registering an increase of 11 percent on the September level and of 24 percent compared to November 2007. In Uganda, despite an average main season crop, the retail price of maize in Kampala, after a decline in July to USD 259 per tonne, has increased steadily to USD 353 per tonne in November 2008.

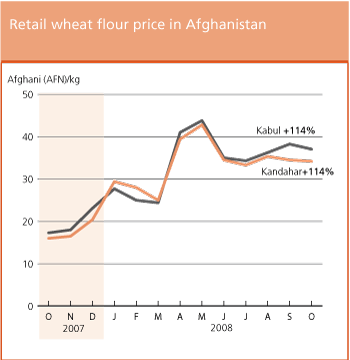

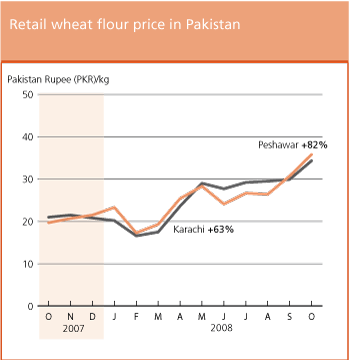

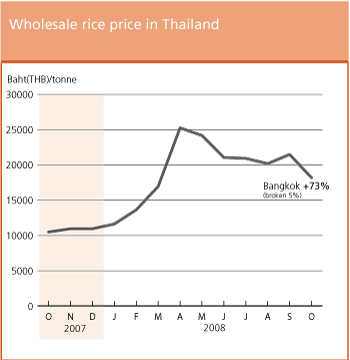

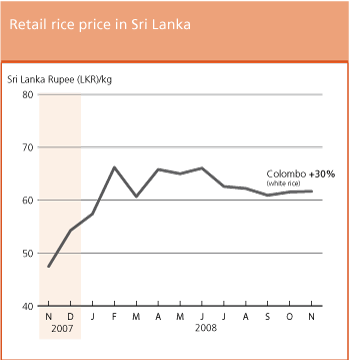

Prices of rice and wheat continue to increase in several countries of the region. In Afghanistan, quotations of the main staple wheat flour by October 2008 were more than twice their levels of a year earlier, following a sharply drought-reduced cereal crop this year. In Pakistan, despite substantial wheat imports by the Government, prices in October were well above their levels of a year earlier reflecting substantial crossborder trade with Afghanistan where quotations of wheat flour in US dollar terms, are about 70 to 100 percent higher than in neighbouring Pakistan. In Thailand, wholesale prices of rice in Bangkok have declined from their peak in April reflecting prospects for another record production this year; however, in October they remained 73 percent higher than a year ago. In Sri Lanka, prices have generally been on the increase since the beginning of the year, and despite another bumper crop recently gathered, in November 2008 they were one-third higher in November 2007. Similarly, in India despite a good 2008 crop and continuing export restrictions, prices of rice have increased since the beginning of the year and by November 2008 had reached 22 rupee per kg, an increase of 38 percent from a year ago. In the Philippines, prices of rice have declined since July but in November, the quotation for the most popular variety (well milled rice), was still 36 percent higher than the previous years level.

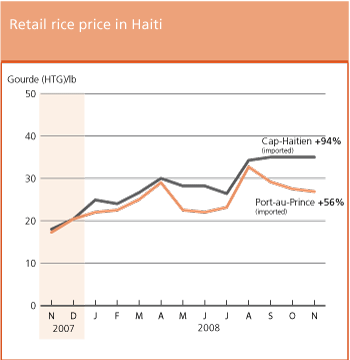

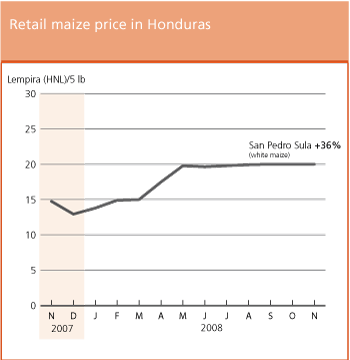

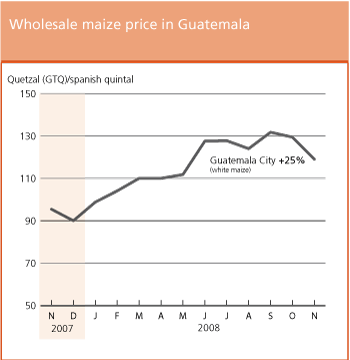

Prices of basic staples maize and rice remain well above their levels of a year ago. In Guatemala and Honduras, the retail price of maize in November 2008 was between one-quarter and one-third higher than at the same time last year. Prices of mostly imported rice have been increasing since the beginning of the year in most countries of the subregion and in November in Haiti (Cap-Haitien) and Nicaragua (Managua) were 94 and 54 percent respectively higher than a year ago.

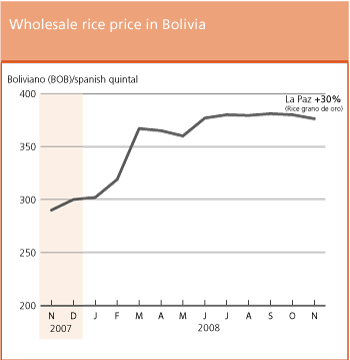

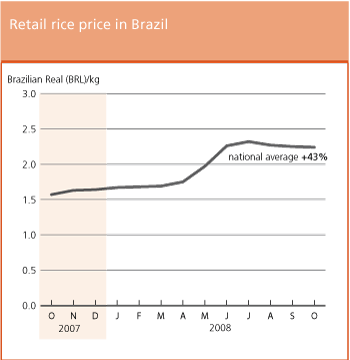

Prices of rice, one of the basic foods in the subregion have shown an upward trend in the past year and in October/November 2008 were one to two-thirds higher than a year earlier in Bolivia, Colombia, Brazil and Peru. Similarly, prices of bread, another main staple in these countries, have increased by about one-quarter from the levels of one year ago and well above the general inflation rates.

1. The percentage figures displayed on all charts refer to the price change from one year earlier. |

| GIEWS | global information and early warning system on food and agriculture |