![]()

![]()

![]()

Softwood lumber notes

The data available at the time of writing indicate that in most countries production of softwood lumber during the first nine months of 1948 was running equal to or slightly higher than for the corresponding period of 1947.

In most countries the general level of business activity showed an increase over that of the previous year. However, high prices tended to limit effective demand for lumber, bringing demand in closer relationship to the available supplies. Countries which depend upon imports for a great deal of their supplies of softwood lumber have limited demand by exercising import or currency controls. Demand has also been limited by other controls such as rationing and controls over credit, although actual needs continue to be great.

Very many statements have been made that selling prices do not cover the costs of production. On the other hand consumers of lumber in all countries feel that prices are high. This has led to the use of lumber conserving methods in industry and an intensification of the search for substitute building materials. In North America prices of most grades of lumber appear to have reached their peak, barring unforeseen increases in the general cost of living. This may also be true in Europe.

North America

United States of America

According to the United States Department of Commerce, it now seems doubtful whether total 1948 lumber production will have reached 19.2 million standards, as earlier anticipated, although it seems clear that production was sufficient to satisfy current demand.

While the third quarter of 1948 was outstanding for its over-all lumber production volume, it is believed that in the fourth quarter there was a curtailment of, or withdrawal from production of a substantial number of marginal operations in both the West and the South as a result of significant declines in prices for rough green lumber. This tendency may have started earlier in the year, as the increasing total availability of lumber and stronger resistance to high prices for poorly manufactured products, accompanied by continued high levels of stumpage prices, made it difficult for the highest cost operators to continue profitable operations.

The total supply of lumber for the third quarter of 1948 exceeded 10.9 million standards, of which beginning stocks accounted for 5.4 million, production for 5.2 million, and imports 0.3 million. The aggregate supply of lumber has at last caught up with the current effective demand, indicated not only by the generally softening prices which characterized the latter part of 1948, but also by the relationship between production, orders, and stocks. Unfilled orders have shown a strong declining trend and increased proportions of current production have gone into inventory accumulations at the mill level. Retail stocks apparently reflect a strong inclination on the part of retailers to avoid further expansion of stocks.

Softwood Lumber Production

Figures collected by the National Lumber Manufacturers' Association indicate that softwood lumber production in the United States for the first nine months of 1948 was 10.80 million standards or slightly in excess of the 10.77 million standards estimated for the previous year. During the period, output in the Southern Pine region totaled 3.64 million standards (3.94), 3 million in the West Coast region (2.86), 2.75 million in the Western Pine region (2.60) and 1.41 million standards in other regions (1.37). Data in parentheses are for the corresponding months of 1947.

Stocks

At the end of January 1948 stocks of softwood lumber were estimated by the trade to be approximately 1.82 million standards. At the end of the first quarter the volume fell to 1.80 million standards. Thereafter stocks increased and at the end of the second quarter totaled 2.01 million standards; the increase continued to the end of the third quarter when stocks reached 2.32 million standards. This expansion in stocks enabled lumber yards, for the first time in many years, to obtain nearly balanced inventories to meet the requirements of their customers.

Retail lumber dealers are reported as desiring not to increase stock levels further until price and demand uncertainties become more clear. The high capital investment required contributed to their decision to await further developments. While figures are not available, it is said that the increase in stock levels has been disproportionately high in the lower grades, supplies in the upper grades in general being still subnormal.

Consumption

Total new construction activity in 1948 reached almost $18,000 million, a record in terms of value and an increase of 26 percent over the previous high figure for 1947. However, the physical volume of construction does not seem to have exceeded the peak levels reached in the nineteen twenties nor the level attained in 1942. Residential construction was the largest single component of new construction and amounted to 40 percent of the total.

In 1947 the amount of completed construction was held down by the lack of balanced supplies of all types of building materials. The supply situation for most building materials improved in 1948 and this materially assisted construction.

The U. S. Department of Commerce reports that for 1949 it is expected that the supply of building materials will continue the improvement shown in 1948. Basic construction items such as lumber, brick, concrete blocks, asphalt roofing and building boards will be in ample supply. No shortages of lath and gypsum board are anticipated.

Because the number of residential buildings started has dropped, it is expected that the number of completed buildings during 1949 will be smaller than for 1948.

U. S. WHOLESALE PRICE INDICES (1939=100)

|

Item |

1948 |

||||

|

Jan. |

April |

June |

Sept. |

Nov. |

|

|

All Douglas fir lumber |

359 |

367 |

391 |

390 |

386 |

|

All Southern pine lumber |

361 |

356 |

341 |

339 |

331 |

|

All Western pine lumber |

303 |

314 |

333 |

355 |

348 |

|

All lumber |

330 |

332 |

336 |

340 |

333 |

|

All other building materials |

214 |

216 |

218 |

225 |

224 |

Source: U. S. Department of Commerce, Office of Domestic Commerce Lumber Industry Report (Washington, D. C.).

Prices

The level of all lumber prices appears to be higher than the relative level of prices for all other building materials. On the whole, during the first nine months of the year prices rose steadily although a leveling-off tendency appeared evident in July and August and declines were small, but definite in September. Indices of wholesale lumber prices declined definitely during October and November, although this may not have been true of all items.

Trade

Exports of softwood lumber (exclusive of box-boards) during the first nine months of 1948 were 190 thousand standards, considerably below the 382 thousand standards exported during the same period of 1947. Of the total 1948 Jan.-Sept. exports, Douglas fir accounted for 139 thousand standards, southern pine 37 thousand, ponderosa pine, sugar pine, and white pine 7 thousand standards, hemlock, redwood, cedar, cypress and spruce together 5 thousand standards, and other softwood 0.5 thousand standards.

The 1948 export trade is said to have been clearly subnormal. High prices and dollar shortages may have substantially contributed to the low level. In some parts of the softwood lumber industry, the present level of exports is causing a production problem

Whereas U. S. softwood lumber exports decreased over the first nine months of 1948, lumber imports at 647 thousand standards stood far higher than the corresponding 1947 figures of 360 thousand standards. The chief species imported were spruce 302 thousand standards, fir and hemlock 174 thousand standards, and pine 123 thousand standards. Other grades accounted for 47 thousand standards.

Softwood lumber accounted for 84 percent of all lumber exports, and for 89 percent of all lumber imports during this period.

Of the total softwood lumber exports during January-September 1948, those directed to Latin America accounted for 29 percent, to Europe 27 percent, to Africa 18 percent, to North America 5 percent, and to all other destinations 21 percent. The distribution of softwood exports for the full year of 1947 was as follows: Latin America 23 percent; Europe 39 percent; Africa 8 percent; North America 7 percent; other destinations 23 percent.

Exports to the nine countries indicated below accounted for 78 percent of the total exports during the first nine months of 1948.

|

Destination |

1000 stds. |

|

United Kingdom |

45.5 |

|

Union of S. Africa |

26.8 |

|

Cuba |

15.5 |

|

Australia |

15.5 |

|

Argentina |

12.6 |

|

China |

8.8 |

|

Canada |

8.2 |

|

Peru |

7.4 |

|

Mozambique |

6.9 |

Canada

Production

The softwood lumber output of 2,019,000 standards during the first nine months of 1948 was 36,000 standards higher than the corresponding figure of 1,983,000 standards for 1947.

The lumber industry in British Columbia is the source of nearly one-half of the total Canadian output. In this province 93 percent of the softwood production consisted of Douglas fir, hemlock, red cedar and spruce. Total production of softwoods at the end of September was running almost 3 percent higher than in 1947.

In the other eight provinces of Canada reports from the larger mills indicate that 65 percent of the softwood lumber produced was made from spruce and balsam fir, 15 percent from white pine, and 11 percent from Jack pine.

Stocks

At the end of March stocks in the hands of manufacturers totaled 372,000 standards, or approximately the level of 1947 for the same date. At the end of June stocks rose to 399,000 standards, a figure 39,000 standards greater than the year before. At the end of September stocks rose to 458,000 standards which was 20,000 standards greater than the previous year's figure.

Trade

Exports of softwood lumber for the first three quarters of 1948 total 902,000 standards, a decrease of 8,000 standards as compared with the same period in 1947.

The shift in the destination of exports is of considerable interest. For the nine month period, exports to the U. S. A. rose from 308,000 standards to 580,000 standards. This increase was offset by the decrease in exports to other destinations as shown below.

|

Destination |

Exports |

||

|

Jan.-Sept. |

Increase + |

||

|

1948 |

1947 |

Decrease - |

|

|

(Thousand standards) |

|

||

|

U. S. A. |

580 |

308 |

+272 |

|

United Kingdom |

219 |

363 |

- 144 |

|

Union of South Africa |

30 |

43 |

- 13 |

|

Netherlands |

6 |

42 |

- 37 |

|

Australia |

18 |

42 |

- 24 |

|

Argentina |

2 |

4 |

- 2 |

Europe

Towards the end of 1948 it seemed that effective demand for softwood lumber had been more or less brought into line with available supplies.

Through 1948, the European economic position, and in particular the timber situation, was influenced by two significant factors:

1. The measures taken in various countries to prevent a further rise in prices, and against the inflationary tendencies which became increasingly apparent in 1947.2. The lack of foreign exchange, particularly dollars, for international trade.

Measures against inflation were not applied simultaneously in the various countries and their effects varied, therefore, according to the nature of the economic situation at the time of application. This uneven development led to considerable price difficulties in the timber trade. Discrepancies in price movements were further increased by the fact that full employment and higher wages in other manufacturing industries exercised a strong drawing power for forest and timber workers in important production areas. Timber industries were forced to adjust wages for lumbering and transport work toward the levels obtained elsewhere, thus increasing production costs.

In some countries efforts to combat inflationary tendencies, through the limitation of credits and rent control led to a fairly considerable decline in investment. In Italy, Belgium, and to some extent in France, this resulted in a big reduction in building activity, and therefore also in the demand for timber, a tendency which was strengthened by the reduced demand on the part of industry. In Europe all payments between countries are made through a payment agreements system, i.e., mainly through bilateral clearing arrangements. It is in the nature of such settlements that export and import values must be balanced against each other. The establishment of this equilibrium often meets with great difficulties. As a result, timber imports have either to be reduced or paid for in hard convertible currency. Until recently various countries were drawing to a large extent on currency reserves for essential timber imports. Many countries have now covered their most urgent reconstruction needs in respect to timber, and they need to budget their currency reserves more stringently. Consequently, fewer dollars, or hard convertible currency, are being made available for the purchase of timber. The covering of clearing balances which may arise from timber imports thus becomes increasingly difficult.

There is a parallel tendency to limit purchases in the dollar countries themselves, Canada and the U. S. A., as far as possible.

The interests of European importing and exporting countries in the matter of prices resulting from this position are exactly opposite. For importing countries every increase in timber prices means a reduction in the volume of timber or of other important products imported; while for timber exporting countries any decrease in prices means a proportionate reduction in other imports.

Stocks continue to be at relatively low levels. The collapse of prices which has occurred at various times in exporting countries, and to a large extent in the retail trade in importing countries, e.g. Italy, is a warning to importers and holders of stocks that they must adopt a cautious attitude.

Considerable progress has been made in the last few years in the economical use of timber as a building and construction material. As a result of this technical progress, timber consumption may continue lower compared with pre-war even after the present period of acute shortage is over.

Exporting countries

Austria

In 1947 timber, in the form of both round wood and sawn wood, was widely regarded as a capital investment, and accordingly stored and held in large amounts. After the currency reform had become effective, all branches of production and trade attempted to realize on their stocks, as a means of increasing their liquid assets. Hence in 1948 demand, which remained at about the same level as in the previous year, was confronted with an increased supply, with the result that prices paid in the internal market, in the case of low grade lumber, actually dropped below the prescribed maximum prices, to between 30 and 50 percent of the amounts paid in the previous year.

Requirements in respect to grades have become more exacting. Thus, unlike 1947, the 1948 timber market in Austria was in a state of equilibrium. In view of this, there has been an appreciable relaxation of controls.

Production

Although an improvement is to be noted, production has continued to meet with great difficulties. These were chiefly connected with the haulage of round wood from the forest to the open road, and from there to the saw mills. The feeding of forestry workers and supplies of fodder for horses improved considerably, but the scarcity of forestry and transport workers had not yet been overcome. The position was improving from month to month, so that it is hoped to carry out the full permitted cut in the winter of 1948/49. However, in order to make up for the overcutting before and during the war, this winter's fellings have been reduced by 24 percent.

When estimating future timber availabilities the considerably improved supply position of Austria in respect to coal and liquid fuel should be noted. It is well known that from the 1946/47 and 1947/48 fellings, large amounts of wood suitable for industrial uses and papermaking had to be used as fuel. Reduced consumption of wood for fuel will have a favorable effect on supplies of industrial timber and pulpwood.

Trade

The countries which constitute the main markets for Austrian timber are Italy, Switzerland, the Netherlands, Hungary and Greece. In general, the export trade in 1948 had to contend with bringing timber grades up to the higher standards required by foreign countries, and with competitive prices. In spite of these obstacles, Austria was able to export some 308,000 m³ (s) between January and September 1948, as compared with 112,000 m³ (s) in the corresponding period of the previous year.

Czechoslovakia

Production

The fellings of 1947/48 winter were heavily hampered by the lack of snow, which did not permit transport to the sawmills in time. This plus the shortage of labor in the forests made it impossible to reach the felling targets set for 1948.

Production of the sawmills, however, exceeded planned production by 17 percent. This was made possible by drawing on stocks of logs, which have consequently been greatly decreased.

Trade

Final export figures for 1948 are expected to be much lower than those of 1947, when a total of 125,000 standards was exported.

During the first six months of 1948 only 38,300 standards were exported, the principal destinations being:

|

Netherlands |

15,400 standards |

|

France |

7,900 standards |

|

Hungary |

2,600 standards |

|

Italy |

7,200 standards |

Smaller quantities were sold to Belgium, Denmark, Greece, Poland, Switzerland, United Kingdom and the Near East and North Africa.

The considerable decrease in the export figures for the first half of 1948 against the 1947 figures has been explained partly because the prices for Czechoslovakian timber are considered to be rather high compared with its quality, and partly because of a slight increase in Czechoslovakia's home consumption.

Finland

Production

Lumber production, which has been steadily increasing, was expected in 1948 to reach levels 10 percent above 1947. As production approached the prewar level, the more difficult it has been to increase it, owing to the lack of power, replacement parts, new equipment, and manpower. Stocks of logs were generally adequate. However, during the next few years the permissible cut in the forests will not be sufficient to elevate economic activity to normal without resorting to over-cutting of accessible forests. This is due to the exceptionally great need of fuelwood and partly to the increased local consumption of timber during years. Overcutting is expected gradually to decrease, chiefly owing to increased coal imports, and the extension of fellings to unexploited forest areas.

Trade

Total timber exports during the first three quarters of 1948 amounted to 60 percent of the 1935 level. At the end of September 1948 total exports of sawn timber amounted to 315,200 standards, showing an increase of about 20,000 standards compared with the same period in 1947.

The principal destinations were:

|

|

Jan-Sept 1948 |

Jan-Sept 1947 |

|

Belgium |

20,100 stds |

15,200 stds |

|

Denmark |

43,000 stds |

27,400 stds |

|

Netherlands |

21,000 stds |

7,700 stds |

|

United Kingdom |

109,800 stds |

126,900 stds |

|

U.S.S.R. |

78,300 stds |

68,900 stds |

Besides sawn timber, Finland exported during the first three quarters of 1948, 208,000 m³ ® of softwood sawlogs as compared with 121,000 m³ ® for the same period in the previous year.

The future prospects of timber exports have been considerably affected by the sudden reduction by 50 percent of Finland's war indemnities to Russia. As these indemnities covered principally finished products, it can be expected that larger quantities should be available for export during the next season.

Prices

The great problem in the Finnish export trade in 1948 was the question of prices, which like prices elsewhere have been rising due to increased cost of logs, wages, and transport. As buyers have become more and more unwilling to pay higher prices, foreign sales have been more difficult, and sawmills have been obliged to restrict production. The price development of Finnish timber, e.g. for the British market, has been as follows:

|

1939 |

£11. 5s. 0d |

|

1940 |

£19. 2s. 6d. |

|

1942 |

£21. 2s. 6d. |

|

1943 |

£25. 5s. 0d. |

|

1944 |

£27. 5s. 0d. |

|

1945 |

£23. 0s. 0d. |

|

1946 |

£28. 10s. 0d. |

|

1947 |

£39. 0s. 0d. |

|

1948 |

£41. 17s. 6d. |

(f.o.b. per standard for 2 ½ in. x 7 in. u/s redwood.)

As the index of the cost of living has reached 839 while the index for timber prices has only reached 372 (1939 = 100), the difficulties of the Finnish timber exporters can easily be understood.

It is estimated that the great differences between export prices obtainable and the Finnish costs of production will cause a decrease in the exports of sawn timber, roundwood and prefabricated houses, but on the other hand the exports of other products such as paper, pulp, cardboard, etc. should increase.

Norway

Production

Fellings, which have shown considerable increases over the low levels of the years of the occupation, are still below normal. The comparatively low rate of fellings was due to lack of manpower. For the season 1948/49 fellings of 8 million m³ ® are envisaged and prospects seem to be good, the manpower situation having improved considerably.

The country's wood-working industry which was working up to 50 percent of its capacity during 1947 reached 75 percent of capacity during 1948.

Norway's softwood lumber requirements for home consumption are considerable and will remain so for many years ahead. Annual consumption of sawn softwoods amounted to about 300,000 standards in 1947.

Now production exceeds domestic needs and stocks of sawn lumber are increasing. Sawn lumber is, however, rationed and its use without permit prohibited for house-building or even repairing.

Trade

Exports of sawn softwood, which amounted to only 2,000 standards during the first half of 1947, reached 4,600 standards during the same period in 1948 and 6,900 standards during the first three quarters of 1948. Exports consisted chiefly of flooring and box-boards. The principal destinations were:

|

|

January-September |

|

|

1948 |

1947 |

|

|

(Standards) |

||

|

Australia |

2200 |

- |

|

South Africa |

1500 |

1200 |

|

Denmark |

700 |

1900 |

|

Palestine |

800 |

- |

|

U. K. |

100 |

100 |

Softwood imports for Jan-Sept 1948 were reported to amount to 11,000 standards, compared with 16,000 standards in 1947.

Prices

The domestic prices of sawn timber have been fixed at a very low level. The wholesale price basis for floorings is 535 Norwegian kroner per standard, but export prices followed general tendencies of the world timber market, reaching an f.o.b. price of £50 per standard (less 2.5 percent) for red and white floorings, and an exchange guarantee was fixed at 20 NKr per pound sterling. Boxboard prices ranged from £70 to £75 per actual standard f.o.b. for average specifications.

Poland

The cession of the best forest areas in the east to Russia has greatly decreased the country's resources of raw materials and caused a strict rationing of timber supplies. Because of this loss, Poland, one of prewar Europe's principal timber exporting countries, will probably not export any great quantity of lumber.

The need for timber in Poland is enormous; according to estimates, about 762,000 houses were destroyed during the years of war. Reconstruction requirements are estimated at 32 million m³ (s).

Production

During the first three quarters of 1948 production increased to 372,000 standards against 292,000 standards in 1947. Stocks, which on 1 October 1947 amounted to 70,000 standards, increased to 94,000 standards by 1 October 1948.

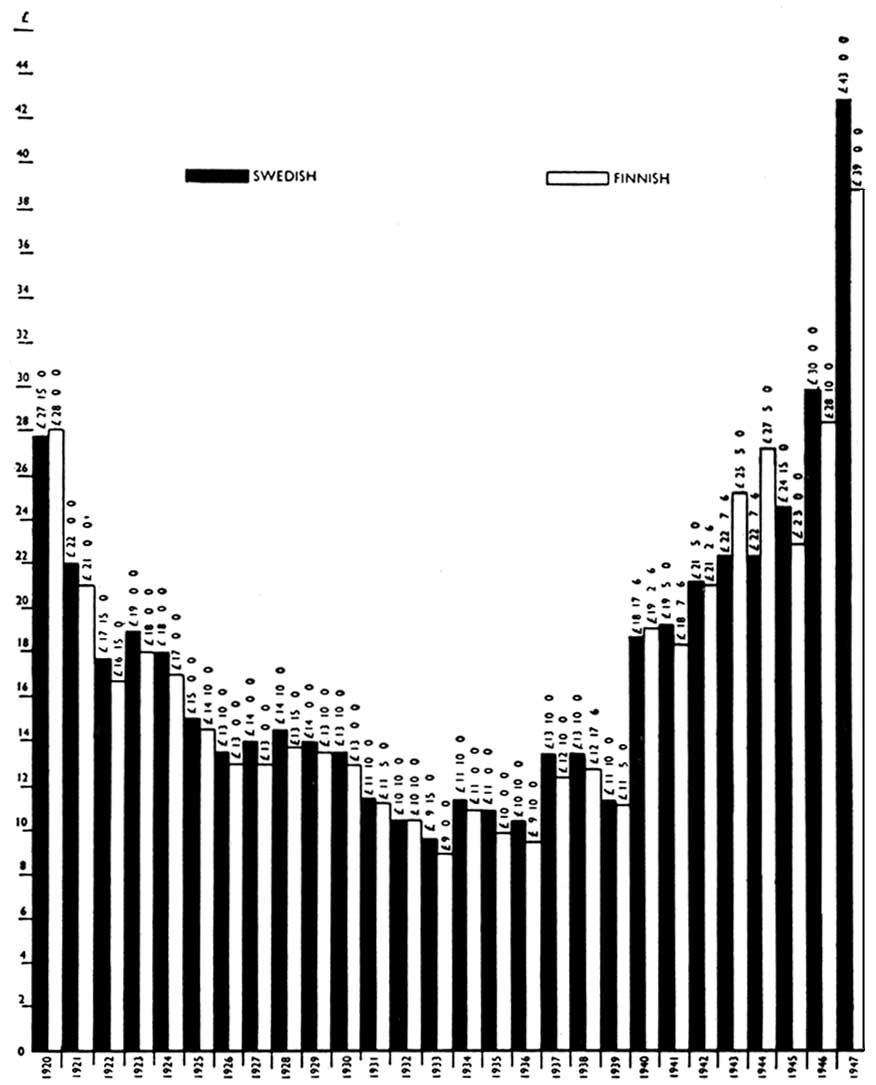

FINNISH & SWEDISH TIMBER PRICES, 1920-1947

Annual opening, f.o.b. prices per standard (of 165 cubic feet), for 7 inch unsorted redwood bettens, destined for the United Kingdom (except years 1940 - 1944 inclusive), from South Finnish ports end the Härnösand district of Sweden. Finnish timber is price group IV.

|

Prepared by TIMBER DEVELOPMENT ASSOCIATION LTD. STATISTICS & INFORMATION DEPT. 75., CANNON STREET, LONDON, E.C.4. L. G. JENNINGS, F.S.S. |

Source: Finnish Sawmill Owners' Association, Helsinki, Finland; Sweden Wood Exporters' Association. Stockholm, Sweden; J. Bulkeley. Churchill & Sim Ltd., London.

Trade

Exports, which averaged some 373,000 standards of sawn timber and 176,000 standards of saw logs during the pre-war years, reached 17,300 standards during the period January-September 1948. The United Kingdom, Belgium, and Netherlands were the principal destinations.

Prices

Prices have been on the same basis as those for Scandinavian timber. For example, sales to the Netherlands are reported at 466 Dutch guilders per standard (£43.10s.) f.o.b. Danzig.

Sweden

Fellings for the 1947/48 season began rather late in the autumn of 1947, and were hampered by exceptionally unfavorable weather conditions, and by the chronic shortage of labor in the forests. These factors decreased the estimated production by about 150,000 standards. In addition, the exceptional drought in the spring of 1948 partly paralyzed timber floatings and stranded about 100,000 standards of logs.

Consumption

Home consumption in 1947 was about 700,000 standards, compared with 725,000 standards in 1946 and an annual average of about 500,000 standards in the pre-war years 1935-1939. Building activity in 1948, however, was more restricted, and the Government control over construction more severe, so that domestic consumption in 1948 should show much lower figures, making more lumber available for exports.

Trade

The 1948 Swedish export market was opened at the end of March, when the Government released a quantity of 500,000 standards for export. In 1947 Sweden exported 405,570 standards, as compared with 391,932 standards in 1946. At the end of September 1948 exports were 324,000 standards as compared with 229,000 standards at the same time in 1947.

At the end of April 1948 negotiations with the United Kingdom led to an agreement for 162,000 standards at 1947 prices. This agreement did not satisfy the Swedish lumber exporters and was accepted with reluctance. Difficulties in meeting the buyers' offers were still great even when the extra duty of 100 Swedish kronor per standard imposed for exported timber was reduced to SKr 75 per standard.

Sales began exceptionally late, towards the end of May. Towards the middle of June 1948, Sweden had sold about 270,000 standards, but after that date sales decreased and there were only some occasional sales for the Mediterranean and overseas markets. At the same time negotiations with the German authorities of the Bizone led to a preliminary agreement. Prices were fixed on the same basis as the Belgian prices for redwood and the Dutch prices for whitewood.

In the middle of July the Swedish Government released an additional quantity of 88,000 standards for export, out of which 50,000 standards were for the

United Kingdom, and 17,000 standards for the Bizone in Germany. However, the Germans having licenses for not more than 7,000 standards, the remaining 10,000 standards were available for other markets.

Prices

The Swedish home market for lumber faced great difficulties at the beginning of 1948, caused partly by very high sawlog prices and partly by increased wages, costs, etc. Prices were strictly controlled by the Government, and were fixed so low, that it is said that they did not even cover production costs. Consequently traders were unwilling to sell to the home market. This changed somewhat during the spring, but the differences between home and export prices were still great.

The prices obtained on various markets during the year 1948 up to the end of September were as follows:

United Kingdom: £43 net for 7 inch red u/s.Belgium: £47 less 2 ½ % for 7 inch red u/s and £59 for 7 inch red u/s boards with an extra £4 for 100 percent sideboards.

Denmark: £43.10s. and £43.15s. for 7 inch red u/s.

Netherlands: 635 SKr for 7 inch red u/s from Härnösand-Umea district.

Eire: £44.5s. for 7 inch red u/s.

South Africa: £50 for 6 inch red u/s.

Egypt: £52 for 7 inch red u/s and £53 for 6 inch red u/s.

The utskott (sixth or lowest grade exported) quality has proved extremely difficult to sell, as the buyers' demands for better qualities have considerably increased.

Importing countries

Belgium

Demand

In 1947 imports of softwood lumber accounted for 75 percent of estimated Belgian consumption. During 1948, bad business conditions, particularly in some export industries, combined with high prices, forced a reduction in lumber imports and in lumber consumption. Building activity decreased.

Pointing to a general price index of about 390, and a price index for imported lumber of about 500, it has been remarked that imported lumber is much too expensive for many of its previous uses. The use of domestic lumber has increased as has the use of wallboards, plywood, cement, and other building materials.

For the time being the Belgians are buyers of small dimension lumber of good quality from Scandinavian countries and some minor quantities of special lumber from other countries.

Trade

Import demands were estimated at about 210,000 standards, but deliveries are not likely to have reached this figure in 1948. Only about 33,000 standards have been bought from Sweden, instead of the 80,000 foreseen in the commercial agreement, and only 20,000 standards have been bought from Finland. Even a small decrease in import prices owing to a drop in freight rates has not increased effective demand.

There has been a decrease in imports from the U.S.A., Czechoslovakia, and Brazil, claimed to have been due to the inferior quality and the high prices of the timber shipped, which did not always satisfy the Belgian buyers and which made it rather difficult to place it on the domestic market.

|

Prices |

Total import sawngoods (Standards) |

Average price per standard |

|

1945 |

11,980 |

£39. 0. 0 |

|

1946 |

52,700 |

54. 0. 0 |

|

1947 |

100,300 |

54.12. 0 |

|

1948 (Jan.-June) |

26,300 |

54. 0. 0 |

Prices are for 2 in. x 7 in. redwood u/s from Sweden and it is to be noted that freights dropped during 1948 from between 190-210 to 120-140 shillings.

Denmark

To fight increasing import prices, prices have been fixed above which no import licenses were granted. As a result, price negotiations for timber between Denmark and the Northern exporting countries, Sweden and Finland, have been difficult and made exporters unwilling to meet the Danish offers for Swedish lumber, at £44.15s. for 7 inch red u/s battens; f.o.b. North Swedish coast mills, and £44.5s free on car inland mills. This concerns above all the Northern production which has always been most sought after in Denmark.

However, an agreement was made with Finland at £45.2s. per standard for 7 inch red u/s battens; in addition, purchases from Sweden commenced. From the USER, the year's shipments were fixed at 10,000 standards from the White Sea district and 5,000 standards from the Russian Zone in Germany.

Shipments during the two first quarters of 1948 showed an upward trend, but decreased towards the end of the third quarter. Swedish authorities did not always grant export licenses when the Danish import license was already obtained. As a result only a small proportion of the 45,000 standards reserved have been shipped, and those almost without exception from the southern inland mills. On the other hand, Finnish and USSR shipments have continued regularly.

France

Demand

There has been a definite slackness in building activity through 1948 due to various causes. For one thing, the rent regulations in force limit returns from houses; further, since the currency reform, the credits required for completing buildings have been difficult to obtain. There has also been a falling-off in repairs to buildings, largely due to the same causes as the reluctance to construct new buildings.

In addition, the efforts to economize in the use of wood led in France, as in other countries, to a reduction in lumber consumption, as compared with prewar. As a result, the demand for lumber has been slight. These factors, together with the scarcity of liquid assets resulting from the currency reform, caused difficulties amounting to a crisis in the marketing of timber during the first part of 1948. This was apparent in a reduction of some 15 to 20 percent, as compared with 1947, in the amounts actually paid for deals and battens.

The prices for planed products fell below the official maximum prices. At the same time customers' requirements in the matter of grade became more exacting, and could not always be satisfied.

Production

Domestic production was on a normal scale in the 1947-48 season. The exceptionally severe bark-beetle attack among the softwood plantations in the Vosges, however, made additional fellings necessary, amounting to more than 1 million cubic meters. This timber in many cases could not be felled at the proper time owing to lack of labor and, having deteriorated, was an additional burden on a market already overloaded with these varieties.

Stocks of sawn wood were considerably reduced by the end of September. Stocks consist mostly of products of French origin, or from the French Occupation Zone of Germany. Supplies from the Scandinavian countries, which were much in evidence before the war, have almost entirely disappeared from the French market.

Prices

It was expected that it would be relatively difficult to market the roundwood produce of the 1948-49 season. However, the first public sales of roundwood were a great surprise, with increases in price from 80 to 100 percent. At the end of September 1948, logs of 120 to 158 centimeters, over bark, were being soold at prices of 1,800 to 3,000 French francs. To judge by these first sales, taking into account felling, transport and trimming costs, there is a definite lack of proportion between the prices paid for roundwood and those of sawn wood products. This paradoxical development should primarily be ascribed to the need to invest capital still available. This has been possible in spite of the prevailing shortage of capital, because a large proportion of the sales are carried out under easy conditions of payment, i.e. with a relatively small initial payment, and subsequent installments. Market prospects for 1949 are better, since there will presumably be a sharp decline in timber imports from Germany, and in addition hopes are being placed in a revival of the building trade. Measures are now being tried with a view to infusing new life into the construction industry.

Greece

Demand

In Greece, as a result of reconstruction, the requirements of structural timber are very large - they have been estimated at approximately three million cubic meters. Domestic production of sawn softwood is very limited. Purchasing possibilities, on the other hand, are also extremely limited, foreign exchange being lacking. Effective demand was kept to a low level inside the country because of credit restrictions and a general lack of funds. There is approximately the same shortage for all grades of sawn wood, which are immediately absorbed by the market when available. On 1 January 1947 stocks stood at 7,000 standards and on 1 April 1948 at 11,000 standards.

Trade

Post-war imports, though increasing steadily, have not yet attained the 1937 figure of 63,000 standards. Thus in 1946 only 8,500 standards of sawn softwood were imported, rising to 18,800 standards in 1947; while for the first eight months of 1948 they amounted to 29,000 standards (including sawn hardwood). Imports were obtained mainly from Czechoslovakia, Sweden, and Finland in that order.

Prices

Despite the big demand, timber prices are in general stable, native sawn softwoods being sold whole sale at 500,000 drachmas ($50) per cubic meter, and imported sawn softwoods at 800,000 drachmas ($80) per cubic meter. Except that prices are controlled, there exist no other restrictions on sawn goods.

Italy

Demand

The decline in industrial production and building activity in 1948, in conjunction with the shortage of capital, soon affected the demand for timber and in particular for sawn softwood.

In the first six months of 1948, prices in the Italian market fell by some 25 to 30 percent. This slump in prices - the only one since the 1933-34 crisis - came unexpectedly, and disturbed the markets of the countries which are normally Italy's suppliers; as import requirements were considerably reduced, strong pressure was exercised on suppliers in the matter both of price and grade. Importers endeavored above all to reduce stocks, the more so as there was a general need to make assets more liquid.

Trade

Actual imports continued higher than in 1947, due to the fact that long-standing agreements had to be carried out, and also that timber had to be taken by Italian exporters, particularly of fruit and vegetables, as payment in compensation trade. It was frequently pointed out that the imports of timber, which were large in proportion to demand, contributed to the complete collapse of the Italian timber market, because the fruit and vegetable exporters had not the necessary technical knowledge to deal in timber, and tried to dispose of the timber as quickly as possible, even at a loss.

The main supplying countries were Austria and Czechoslovakia. As regards Austria, there were considerable difficulties in carrying out the contracts concluded, because Austrian grades did not always manage to satisfy the more exacting requirements. As all transactions were concluded on a compensation basis with internal price equalization, there is no question of prices being determined by value.

Yugoslavia, which supplied a considerable proportion of Italy's requirements before the war, has been unable to establish a footing in the Italian market up to the end of 1948. The quotas laid down by trade treaty, which were to be taken up by Italian importers, could only be drawn on to a small extent, owing to price difficulties. The Italian timber market showed some signs of recovery towards the end of 1948.

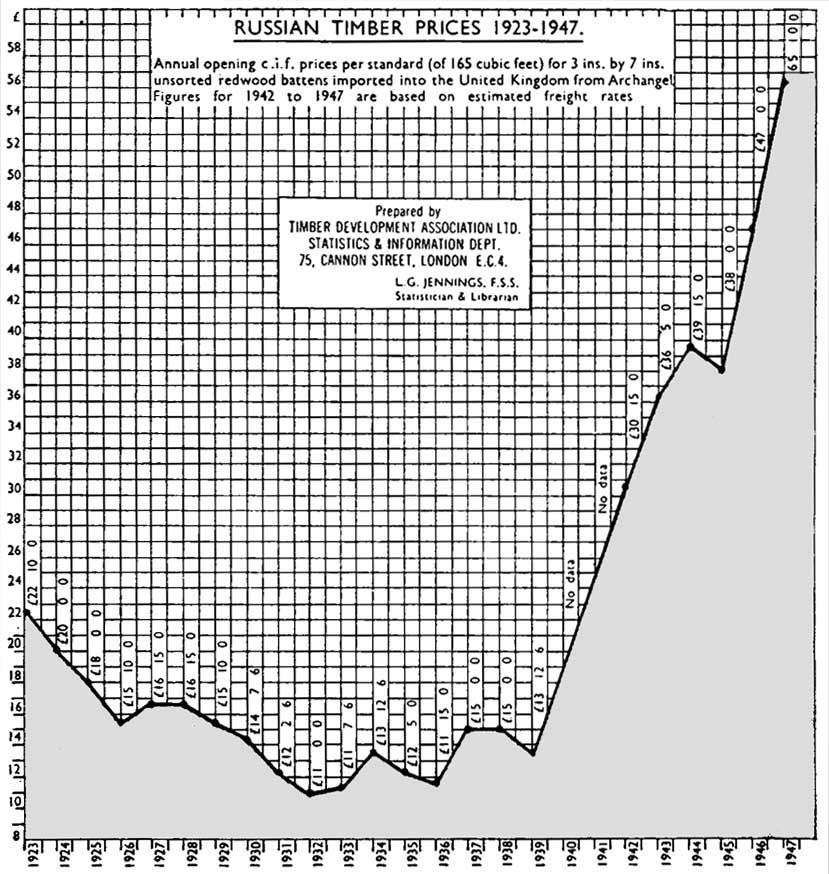

Russian timber prices 1923-1947.

Netherlands

Demand

The demand for timber remained very great through 1948, as in the consumer industries, such as building, furniture manufacture and shipbuilding, business was still very brisk. The building of new houses is assisted by Government credits. As a result of the shortage of foreign exchange, the Netherlands is not yet in a position to cover the demand by importing, so that a strict internal allocations system for softwood is still applied.

Dutch buyers, as far as timber for building and for joinery is concerned, are primarily interested in taking Scandinavian and Russian material. The relatively large imports from Central European countries saturated the market, whereas the demand for Scandinavian products could not be met. In this connection it is significant that the Central European products are expensive in relation to the grades actually delivered.

Stocks are small - since it is not feasible for importers to stock large quantities of timber. Prices have risen eight times as compared with 1935, and three and one-quarter to four times as compared with 1938-39.

Trade

The main supplying countries for the Netherlands, in 1948, were Sweden, Finland, Czechoslovakia, the Bizone of Germany, Yugoslavia, Poland, Austria and the USSR, while France and Rumania played a minor part.

SWEDEN occupies the first place as a supplying country, with 75,000 standards. Imports purchased in this country comprise approximately 13,000 standards of box-making materials, and 12,500 standards of material for making doors; the remainder consists of products for joinery and house building.

FINLAND. The trade agreement with Finland provided for 32,000 standards, about one-third of which is taken up for box-making, the rest being used for building. As compared with Sweden, the Finnish lists are less suited to the Netherlands' requirements.

CZECHOSLOVAKIA. Provision was made for importing from this country some 150,000 m³ (s), i.e. about 32,000 standards. The whole of this quota has been taken up in the form of 70,000 m³ (s) of building timber and approximately 50,000 m³ (s) of box wood.

YUGOSLAVIA. The trade agreement provides for the supply of 80,000 m³ (s) of timber, to comprise 5 to 10,000 m³ (s) of box board and 70 to 75,000 m³ (s) of building timber. In 1947 the Yugoslav production was not satisfactory in the matter of lengths (which were nearly all 4 meters) but it was hoped that in 1948 lengths better graded to suit demand would be supplied.

GERMANY. The agreement between the Netherlands and the American military authorities in Germany provided for the importing of 140,000 m³ (s) of sawn softwood, at a price of $33 per m³ f.o.b. Rhine Port.

POLAND. 40 000 m³ of building timber and box board were purchased and deliveries began in the Autumn of 1948.

USSR. The trade agreement with this country provides for 150,000 m³ - 32,000 standards to come from White Sea ports.

FRANCE. Under a trade agreement, France was to supply 20,000 m³ of "pin des Landes" as box board in lengths of 2 to 3 meters. There are, however, great difficulties connected with selling this product.

RUMANIA. Smallish amounts have been sold to Export-LEMM for the Netherlands. High frieght charges are however, making business difficult.

Prices

The resale prices in the Netherlands are controlled. There is a standard price for all building material. In order to make up the difference in prices for imports as between the various varieties, a price equalization fund has been established to which importers must contribute or, alternatively, from which they receive a contribution, according to the price paid. At the same time the fund acts as an emergency fund, which takes the first shock when there is a change in the market position.

The prices paid for the best Swedish productions of 7-inch battens, f.o.b. varied from 630 to 640 SKr.

While Swedish f.o.b. prices of timber have not been very different from 1947, there was a possible reduction in the case of c.i.f. prices as a result of the lower freight rates. In 1947, rates of £9 per standard from Sweden, and £10 and over from Finland, were normal. In 1948 the rates from Sweden were £5.10s.6d. to £5.17s.6d. i.e. more than £4 under 1947. This difference is large enough to have had an effect on selling prices.

Building material was bought from Finland at list prices, f.o.b. 2 ½ x 7 inches u/s whereby a margin of 7s.6d. up and down was left to sellers and buyers for negotiations.

|

1st group |

£42.17s.6d |

|

2nd group |

£42.12s.6d |

|

3rd group |

£42. 7s.6d |

|

4th group |

£41.17s.6d |

Switzerland

Demand

For the first nine months of 1948 consumption of and demand for softwood remained at a very high level. Yet the proportion of timber used in building and in the packing industry declined sharply in comparison with pre-war years. This decline was more than offset by the increased activity in the industrial field. However, the rapid progress made in the substitution of other materials for timber is generally viewed with concern, since this affects the marketing prospects of Swiss timber, once industrial and building activity has returned to the normal level.

The great demand for first and second grade products, however, could still not be fully met, despite great efforts made to import from Austria, Czechoslovakia and Yugoslavia.

Production

The supply position steadily improved over the first three quarters of 1948. Domestic production of constructional timber in the felling season 1947/48 amounted to roughly 120 percent of the normal figure; large quantities of insect-damaged timber had also to be felled in the spring. In consequence, taken as a whole, home-produced supplies were large in comparison with normal years.

Stocks of sawn timber increased during the first nine months of 1948 from 221,000 m³ (s) as of 1 January to 324,000 m³ (s) as of 31 August, the stocks of roundwood in the same period from 438,000 m³ ® to 510,000 m³ ® in spite of the fact that there is usually a drop in stocks at this period.

Trade

As regards imports, the most important were the deliveries of roundwood from the French Occupation Zone of Germany, totalling 196,000 m³, i.e., about 14 percent of Swiss normal production. Despite the great demand, this flooding of the market with Swiss and German roundwood led in the third quarter to a saturation of the market, as far as wood for building and boxes was concerned, resulting in a recent decline from 10 to 15 percent in the prices of these grades.

In the first nine months of 1948, 34,000 m³ (s) were imported from Austria as against 32,000 m³ (s) in 1947. It is said that the quality of Austrian production did not altogether satisfy the Swiss buyers.

The deliveries from Czechoslovakia, amounting to 3,600 m³ (s), were insignificant. The quantities agreed upon could be traded only up to 15 percent, because of existing price differences and other difficulties.

Prices

The increase of about 10 percent in the price of roundwood which the forestry industry introduced in the autumn of 1947 was reflected, though in lesser degree, in the prices of sawn products. The removal on 1 October 1948 of all control and price regulations for all grades of timber was followed by an agreement in principle between forestry interests and sawmills to maintain 1947 prices for roundwood over the felling period 1948-49. Apparently, however, it is very difficult at present to maintain the corresponding price level for sawn timber in the grades used for building and boxes.

United Kingdom

Demand

At the beginning of 1948, the authorities planned to import a million standards. On the other hand, at the Timber Committee of ECE, an essential need of 1,650,000 standards was announced. In comparison with actual imports of 2,366,000 standards in 1937, consumption has fallen considerably.

The Government's anti-inflation policy had already begun to produce its effects in the first and second quarters of 1948 in the form of a slackening of demand for a large number of consumer goods. The measures adopted also undoubtedly had some effect on the demand for timber, and it is obvious that price considerations are assuming more and more importance. The efforts of the Government to keep down the level of costs over the whole field of industry, including the timber sector, have an added significance in view of the balance of payments. The rise in the volume of exports in the past year was partly offset by import price rises, especially of timber, which have risen much more sharply than those of exports of other commodities.

The main features of the British timber market in the first nine months of 1948 were as follows:

On the whole, demand in the country was steady. It was, however, limited by the Timber Control, which granted consumption licenses averaging about 80,000 standards a month.The demand also varied to some extent as between the different grades. The high grade timber, i.e. joinery qualities, was most sought after, whereas there was a temporary decline in February, March and April in the demand for the big sizes imported chiefly from the U.S.A. and Canada. The demand for the Scandinavian varieties of first class timber was especially marked in those months.

Consumption

The building industry continues to be the chief consumer, the wood being used primarily for house building, where at present authorized use is limited to 1.6 standards of softwood per dwelling. The technical possibilities of saving timber have been systematically developed in this field, both scientists and builders playing their part in achieving this result. Home-produced substitutes for timber, such as cement and steel, are drawn on to the greatest possible extent.

Another important consumer, the box and packing-case industry requires about 300,000 standards a year, i.e. just under a third of the imports planned for 1948. With increased exports of industrial products, requirements in this sector are rising, although here again substitute materials like cardboard (paperboard) are being used to the greatest possible extent.

Production

Domestic production of sawn softwood represents a very small proportion of Great Britain's supplies.

As regard supplies, the position at the beginning of 1948 was considerably better than in January of the previous year. Stocks were as follows:

1 Jan. 1947 215,000 standards of which 205,000 were imported.

1 Jan. 1948 615,000 standards of which 607,000 were imported.

For comparison, imports in 1939 totaled 2,300,000 standards and stocks in January 1939 totaled 880,000 standards.

Trade

IMPORTS OF SAWN AND PLANED SOFTWOOD (excl. boxboards)

|

Year |

Quantity 1000 standards |

Value £1000 |

Value (CIF) per standard |

|

1938 |

1778 |

24 |

£13.13s.6d |

|

1946 |

737 |

31 |

£41.13s. |

|

1947 (Jan-Aug) |

776 |

37 |

£47.16s. |

|

1948 (Jan-Aug) |

562 |

31 |

£55. 3s. |

The increase in the average price per standard between 1947 and 1948 is partly accounted for by differences in the grades of timber imported, since export prices (f.o.b.) in the main exporting countries have shown little or no increase and freight rates are lower than in 1947.

In the early part of 1948, owing to the small shipments, freight rates from the Scandinavian countries showed a sharp downward trend, which continued until the end of the third quarter even after the contracts with Finland and Sweden had been concluded. In comparison with last year the rates from the ports of Central Sweden to London fell by 30 to 40 shillings per standard.

Of outstanding importance were the price negotiations with the Scandinavian countries, Sweden and Finland, imports from which in 1948 were expected to total 162,000 and 140,000 standards respectively. In view of the relatively large stocks at the beginning of the year and the effects of the deflationary policy adopted, price reductions had been hoped for. Exporting countries, however, proposed an increase of about £7 over the 1947 prices.

Negotiations with Sweden which were concluded at the beginning of May led to an agreement on the same basis as 1947, i.e. £43 for 7 inch u/s redwood battens from central Sweden and £47.10s. (f.o.b.) for 3 in. x 9 in. u/s redwood. Subsequent negotiations with Finland led to a slight price increase over 1947, namely, £41.12s 6d. (f.o.b.) for 7 inch u/s redwood Group I, as against £40 in 1947, and £41.2s. 6d. for 7 inch u/s whitewood Group I as against £39.10s. in 1947. The increase in prices of Finnish lumber is explained by the Finnish claim that the prices received in 1947 were too low, particularly in view of prices paid to Sweden.

Purchases were as follows:

|

Time |

From Sweden |

From Finland |

|

to 30 March |

- |

- |

|

to 30 June |

94,000 stds. |

89,500 stds. |

|

to 30 September |

180,200 stds. |

135,500 stds. |

During September new quotas were fixed with Sweden for an additional import of 50,000 standards, but it seemed doubtful whether the whole of this quantity would be utilized, since Swedish stockpiles in the sizes desired were already seriously depleted.

Up to 30 September 1948, 112,000 standards of lumber of which 99,000 were sawn planed softwood had been imported from Sweden and 108,000 standards of lumber of which 107,600 were softwood from Finland.

From the USSR about 32,300 standards had been purchased at the end of September, at the following prices: 7 inch red u/s battens at £43.10s. per standard; 7 inch white u/s at £43 f.o.b. White Sea and Leningrad, German redwood from the Russian Zone is at £40.10s. for u/s and £37.10s. for Group IV f.o.b, for a specification averaging 6 inch, deals, battens and boards. Further sales were expected to bring the total up to about 50,000 standards.

In the first three quarters of 1948, England purchased 100,000 standards from Yugoslavia and 40,000 standards from Poland and 25,000 standards from Rumania. Yugoslavia and Rumania are to supply mainly white wood and Poland mainly redwood.

Shipments from Canada and the U.S.A. during 1948 were being made on 1947 contracts. The quantities covered by new agreements have been drastically reduced, owing to the shortage of currency. Up to the end of September a total of 208,000 standards sawn softwood were imported, including 5,000 standards boxboard from Canada and 63,500 standards from U.S.A.

The 1948 contracts up to 30 September 1948 were 80 000 standards from Canada while no contracts had been concluded with the U.S.A.

Imports of round and sawn wood from Germany played a considerable part in supplying the British market with sawn softwood. In the first nine months of 1948 there had been imported about 133,000 standards (56,000 standards, sawn wood and 77,000 standards in sawn equivalent of German logs). Imports during 1949 will probably fall off considerably or cease altogether.

Near East

General

The sawn softwood market in the Eastern Mediterranean area, in Palestine, Egypt, Syria, Iraq and Iran, has been hampered by prevailing political conditions. The economy of these countries has been affected by the war in Palestine, with all its secondary effects such as increase of prices, lack of credit, little investment activity, and so on. In addition the lack of hard currency also hampered imports very much.

Trade

The Near East played a fairly important role in the central European timber market during the first year after World War II, but now there is a comparatively small demand. Rumania and Yugoslavia take the first place as suppliers, and Portugal and Austria also seem to be interested in certain deliveries. Syria has contracted for 12,000 m³ (s) Syrian quality (= Grade V-VI) at $31 to be delivered in Constanza and 4,000 m³ (s) Yugoslav timber of the same grade at 150 Swiss francs c.i.f., portions of which have already been imported. Palestine imported several shipments of "merchantable" at $270 per standard c.i.f. and "common" at $210 c.i.f. from Canada. It may also have received 10,000 m³ (s) "Alexandriner" at £12 per m³ (s) f.o.b. Constanza. While Iran is able to cover its requirements out of its own production, and does not import to a great extent, Iraq gets supplies from the East.

Egypt, which was a fairly important buyer on the market in pre-war years, shows little demand today. Currency difficulties cause Egypt to try to meet its requirements by barter agreements for cotton. Such agreements may have been made with the USSR and Yugoslavia.

EXCHANGE RATES - Units of National Currency per U.S. Dollar

|

|

1947 |

1948 |

|

Pound sterling |

0.248 |

0.248 |

|

Norwegian krone |

4.97 |

4.97 |

|

Swedish krona |

3.60 |

3.60 |

|

French franc |

119 1 |

207 1 |

|

|

_____2 |

309 2 |

Source: Monthly Bulletin of Statistics, Vol. III, No. 1-2, Jan-Feb 1949 (Statistical Office of the United Nations).

1 Official rate.

2 Free rate.

Fiberboards

A commodity report under this heading, appeared in UNASYLVA, Vol. II, No. 4. The report dealt with commodities which are also classed as "Fiber Building-boards." The editor of The Paper Container, a United Kingdom publication, has pointed out that the use of the term "Fiberboards" in respect to these commodities may be misleading. In the industry fiberboard is properly "a cardboard product made from vegetable fibres," our correspondent states, and the first record of a vegetable fibre being used to form paper or board dates over 200 centuries B.C. when the Egyptians used the tissue-like fibre of papyrus gummed in layers to form a type of paper. In the second century A.D. there is a record of a Chinese invention for making paper from the cellulose fibres of the inner bark of the mulberry tree, and this method of paper manufacture was adopted in Asia and Europe until the fifteenth century, when rags were pulped to make sheets of paper. The first boards of paper were used as bindings for books and were made of sheets of paper pasted together, since when improvement after improvement has taken place until the present product known as fibreboard was produced in an elementary state early in the nineteenth century.

"Fiberboard is not mainly used for building purposes, but as the raw material for containers, an industry which is considerably larger and more important than the building board trade. As for the origination of the fibreboard industry, as it is known today, the Thames Board Mills, Ltd., at Purfleet, Essex, in this country, began the manufacture of such a board in 1903 and made the first containers from this board in 1909, the board being known in the industry as solid fibreboard."

![]()

![]()

![]()

{kind=link}

{kind=link}