![]()

![]()

![]()

Wood pulp

Pitprops

The figures quoted in the text are those available up to 1 March 1950, drawn from official sources, from World Wood Pulp Data (published by the Canadian Pulp and Paper Association and the United States Pulp Producers Association), and from trade journals. Except where otherwise indicated, metric units are used throughout.

In 1948 wood pulp consumption in North America attained new record heights, and consumption by European mills, although still below normal levels, was rapidly increasing. Toward the end of the year, however, a leveling-off of demand in the United States developed into a recession on the world export market, which reached a climax by midsummer of 1949. For the Northern European exporting countries, greatly dependent on pulp exports as a source of dollar exchange, this situation was the more serious when viewed in the light of substantial increases in North American productive capacity.

However, in early September 1949 a renewal of activity became apparent in the U.S. pulp market, and by the turn of the year the United States was back to record-breaking monthly production and consumption. There was also a partial recovery of the earlier drop in Northern European exports to the United States and other destinations. Over-all production for 1949 in North America was lower than for 1948; but the revival in the last months of 1949 promises a possibly higher consumption level in 1950, although the record 1948 figures will probably not be reached. Such a situation in North America should help maintain a firm world pulp market.

Northern European exporters have continued their efforts to sell on the U.S. market. So far, devaluation of currencies has not given rise to underbidding, but it is too early to say how the situation may develop. On the other hand, devaluation has given relief to Northern European producers with relatively high production costs. The trend in the United States is still toward dependence on North American supplies; Europe has maintained its position as the major source of supplies for all continents except North America.

Statistics assembled by the Montreal Pulp Conference organized by FAO in May 1949 indicated that the: 1948 output was slightly in excess of current consumption. Although the apparent world surplus was less than 3 percent of production and may have been due to statistical inaccuracies, it did tend to explain the decline in prices, the accumulated stocks, and of their pulp. The estimates for 1949 and 1950 indicated-a rapid restoration of equilibrium, which appears now to be the actual situation.

World production and trade data for 1949 are summarized in Table 1.

Table 1. - Wood pulp: World production and trade data

|

Region |

1949 Estimates |

||||

|

Production |

Imports |

Exports |

Consumption |

||

|

|

(1,000 metric tons) |

||||

|

TOTAL |

26,822 |

4,654 |

4,864 |

26,612 |

|

|

North America |

17,888 |

1,793 |

1,516 |

18,165 |

|

|

Latin America |

219 |

209 |

- |

428 |

|

|

Europe |

8,086 |

2,550 |

3,348 |

7,288 |

|

|

|

Northern |

5,356 |

13 |

3,247 |

2,122 |

|

|

Eastern |

421 |

66 |

- |

487 |

|

|

Western |

672 |

1,968 |

4 |

2,636 |

|

|

Central |

1,637 |

503 |

97 |

2,043 |

|

South Africa |

15 |

1 |

- |

16 |

|

|

Asia and Pacific |

614 |

101 |

- |

715 |

|

- None.

WOOD PULP PRODUCTION

World pulp production in 1949 (excluding the U.S.S.R.) is estimated at about 27 million tons. This is less than the 1948 output, and less than the volume of production that had been considered possible by the Montreal Pulp Conference in May 1949.

In most European countries steady rehabilitation of the pulp industry continued through 1949, the largest production increase (about 70 percent) having occurred in Western Germany. A few European countries still operate far below capacity, primarily because of pulpwood shortages. But Northern European mills, which had cut production during the first half of 1949, were later reported running close to capacity.

World pulp-producing capacity continues to expand. In North America over 2 million tons of new capacity have come or will soon come into operation. In Europe, Portugal and Norway are planning to erect new mills, and there are also plies for increased capacity in Austria, Czechoslovakia, and Yugoslavia. In Australia and New Zealand new developments are under way, and new pulp mills are projected in Asia and the Far East. At the same time' recent estimates still place the idle pulp capacity of the world at over 5 million tons. Most of this idle capacity is located in Europe, North America, and Japan.

The 1948 and 1949 production figures for North America and Europe are shown, by countries, in Table 2, together with figures on production capacity.

NORTH AMERICA

North American production of all grades of pulp in 1949 totaled approximately 17,900,000 tons, about 950,000 tons less than in 1948.

United States of America

In 1948 wood pulp production in the United States reached an all-time record of nearly 11.7 million tons. In late 1948, however, paper and paperboard production started to decline, following the general economic trend, and this decline was accompanied by a drop in consumption of wood pulp, particularly of market pulp. During the following months, consumers of market pulp drew heavily on inventories that had been acquired in many instances at prices much higher than those currently prevailing.

In 1949 the manufacture of paper and paperboard, at 18.4 million tons, was approximately 1.4 million tons below the 1948 record, and rayon production dropped 12 percent. Total U.S. wood pulp production (11.0 million tons) fell below the 1948 volume by about 6 percent. In August 1949, however, as a result of the general economic situation, confidence began to return throughout the pulp industry, and during the last three months of the year greater tonnages of wood pulp were produced and consumed than in any previous corresponding period.

The brisk demand for pulp continued in January 1950, and it is generally expected that mill requirements will be sustained at high levels, at least during the first part of the year. Inventories, which had dropped to a lower level than at any time since May 1947, are now in process of replenishment.

Canada

In 1948, Canadian (including Newfoundland) mills, operating at capacity, produced nearly 7.2 million tons of all grades of wood pulp (360,000 tons more than in 1947, and almost double the volume of 1937). The decline in U.S. demand during 1949 affected Canadian output of market pulp; and although the final figures for 1949 are not yet available, production and sales are expected to be slightly below the 1948 figures.

The increasing-demand for kraft pulp has led to the construction of three new sulphate pulp mills having a total projected capacity of 145,000 tons annually, to add to the existing Canadian capacity of some 700,000 tons a year; they will come into operation progressively over the next two years.

EUROPE

European pulp production for 1949 is estimated at approximately 8.1 million tons, compared with 7.9 million tons in 1948.

In most European countries rehabilitation and modernization of plants have made further progress, while supplies of raw materials and equipment and availability of manpower have definitely improved as: compared with the immediate postwar years. Many formerly idle mills are getting back into production.

Table 2. - Wood pulp production and consumption, North America and Europe

|

Country |

1948 |

1949 (Estimates) |

||||||

|

Capacity |

Production |

Consumption or new supply |

Capacity |

Production |

New supply |

|||

|

|

(1,000 metric tons) |

|||||||

|

North America |

19,254 |

18,839 |

19,036 |

20,686 |

17,888 |

18,165 |

||

|

|

Canada 1 |

7.397 |

7,161 |

5,470 |

7,900 |

6,863 |

5,492 |

|

|

|

United States |

11,857 |

11,878 |

13,566 |

12,786 |

11,025 |

12,673 |

|

|

Europe |

10,881 |

7,905 |

6,958 |

10,924 |

8,086 |

7,288 |

||

|

|

Northern |

7,376 |

5,407 |

2,439 |

7,352 |

5,356 |

2,122 |

|

|

|

|

Finland |

2,482 |

1,675 |

817 |

2,485 |

1,550 |

652 |

|

|

|

Norway |

1,324 |

823 |

506 |

1,324 |

935 |

493 |

|

|

|

Sweden |

3,570 |

2,969 |

1,116 |

3,543 |

2,871 |

977 |

|

|

Eastern |

443 |

392 |

474 |

483 |

421 |

487 |

|

|

|

|

Hungary |

25 |

6 |

41 |

25 |

6 |

40 |

|

|

|

Poland |

231 |

210 |

255 |

256 |

227 |

250 |

|

|

|

Romania |

148 |

140 |

138 |

157 |

145 |

145 |

|

|

|

Yugoslavia |

39 |

36 |

40 |

45 |

43 |

52 |

|

|

Western |

977 |

674 |

2,395 |

1,004 |

672 |

2,636 |

|

|

|

|

Belgium |

77 |

52 |

212 |

77 |

66 |

183 |

|

|

|

Denmark |

5 |

1 |

76 |

5 |

1 |

74 |

|

|

|

France |

545 |

459 |

771 |

562 |

467 |

830 |

|

|

|

Ireland |

- |

- |

10 |

- |

- |

13 |

|

|

|

Netherlands |

110 |

39 |

193 |

120 |

41 |

41 |

|

|

|

Spain |

82 |

59 |

100 |

82 |

46 |

103 |

|

|

|

United Kingdom |

158 |

64 |

1,033 |

158 |

51 |

1,392 |

|

|

Central |

2,085 |

1,372 |

1,650 |

2,085 |

1,637 |

2,043 |

|

|

|

|

Austria |

385 |

258 |

243 |

385 |

284 |

244 |

|

|

|

Czechoslovakia |

419 |

304 |

281 |

419 |

326 |

286 |

|

|

|

Italy |

240 |

203 |

300 |

240 |

215 |

423 |

|

|

|

Western Germany |

890 |

471 |

619 |

890 |

676 |

895 |

|

|

|

Switzerland |

151 |

136 |

207 |

151 |

136 |

195 |

- None or negligible..

1 Includes Newfoudland.

Northern Europe

Finland. Since the end of the war, Finland has made remarkable progress in restoring the productivity of its mills and improving supplies of raw materials for the pulp industry. Manpower too has been more readily available. In 1948 production of pulp amounted to about 1.7 million tons, approximately 60 percent of total capacity. A leveling-off of exports and production late in 1948 seriously threatened the country's economy. By the spring of 1949 stocks of pulp were more than double the normal, and several manufacturers were compelled to reduce output.

In the fall of 1949, the partial recovery on the U.S. and world markets brought renewed stimulus to Finnish pulp production, and at the end of the year the pulp industry was operating at near capacity. But although the final figures for 1949 are not available at the time of writing, production is expected to have been less than 1.6 million tons. Stocks of chemical market pulp had decreased approximately 50 percent from the levels prevailing in the spring.

Sweden. In 1948 Sweden's production of all grades of pulp amounted to approximately 3 million tons. Production in early 1949 was limited, mainly because of inability to obtain pulpwood. There are, in fact, supplies of pulpwood in southern and central Sweden, but current price levels do not permit the shipping of these supplies to northern Sweden. Germany is reported to have negotiated for pulpwood imports at prices almost twice as high as those paid by Swedish mills.

As was the case with Finland, brisker activity in the fall of 1949 in some degree made up the earlier lag. According to preliminary estimates, the 1949 production of market pulp (including viscose pulp) was over 1.70 million tons, or almost as much as in 1948, when it was just over 1.75 million tons. In this connection it may be recalled that the corresponding figure for the record year 1937 was 2.25 million tons.

Norway. Norwegian production in 1949 is expected to show a slight improvement over the 1948 levels. Confidence in future possibilities is evidenced by the fact that Norway plans, to build a new chemical pulp mill which will replace two old mills. The total annual capacity, therefore, will not be increased, nor is the consumption of pulpwood expected to increase.

Central Europe

Austria. Gradual improvement in Austria's pulp output continued through 1949, and the year's production of all grades of pulp is estimated at 284,000 tons as compared with 258,000 tons in 1948. Production capacity, which is approximately 385,000 tons, could be expanded by modernizing mill equipment, and the present limited supplies of domestic raw material could be increased by carrying out thinnings to provide more pulpwood and by making greater use of sawmill "waste."

Czechoslovakia. As in Austria, pulp output in Czechoslovakia showed gradual improvement in 1949, and production of chemical pulp for the year is estimated at about 325,000 tons, approximately 25,000 tons over the 1948 figure. Production of chemical pulp from hardwoods is now being undertaken by a new mill in the eastern part of the country.

Italy. The chemical pulp industry in Italy is now running close to capacity in an effort to speed the export drive for paper and paperboard. Domestic production of pulp' however, provides barely 30 percent of the paper industry's requirements; the remainder has to be imported. An important event for the Italian paper industry was the granting by ECA of a $1,650,000 loan for the import of American paper-manufacturing machines.

Western Germany. The largest production increase in Central Europe occurred in Western Germany, where output increased from 471,000 tons in 1948 to an estimated 676,000 tons in 1949, a figure equal to 75 percent of existing capacity. This rapid gain was stimulated by Marshall Plan aid and by the cutting-down of pulpwood exports from the French Zone. Towards the end of 1949, pulpwood imports from Sweden to Western Germany were resumed for the first time since the end of the war. Bizone industries contracted for 350,000 cubic meters of Swedish pulpwood, subject to the approval of trade licenses. The price of pulpwood, most of which is obtained from state forests, is much higher in Western Germany than in other countries. As long as this situation remains unchanged, pulpwood imports are likely to be continued.

Eastern Europe

Production figures for Eastern European pulp-producing countries are estimates. For 1949 the combined production of Hungary, Poland, Romania, and Yugoslavia has been set at about 420,000 tons, as compared with 390.000 tons in 1948.

Western Europe

Pulp production in 1949 for Western European countries appears to be about the same as in the previous year. The Netherlands and the United Kingdom are said to be still operating at approximately 30 to 40 percent of capacity. In Portugal, according to recent reports, complete plans for an integrated mill, capable of producing initially 20,000 tons of sulphite pulp and 18,000 tons of paper a year, have been drawn up. The pulp capacity may later be doubled and the paper capacity increased to 28,000 tons. Ultimately this mill, in conjunction with a sulphite mill producing 6,000 tons annually, may be able to supply Portugal's entire requirements and leave a portion of its output for export. The new mill will be located in a heavily forested region which can furnish it with sustained pulpwood supplies. Construction is expected to begin shortly, and the mill may start operations toward the end of 1951.

LATIN AMERICA

Despite some expansion in recent years, pulp production in Latin America still covers only approximately one-third of the region's requirements. Further developments depend largely on the possibilities of using indigenous species' including hardwoods, for the production of pulp at competitive costs.

Recent experiments with tropical and other hard-wood species have been carried out in a number of countries. A significant technical advance has 1 the perfection of the neutral semi-chemical process, which involves both a chemical softening and a' mechanical grinding. In experiments c conducted on an industrial basis, as many as 30 different species have been pulped simultaneously with success. This is an important development in view of the virtual impossibility of segregating at reasonable cost many of the hardwood species, which grow in dense mixed stands. The pulping of tropical woods will probably receive a great impetus during the next two decades. If so, Latin-American pulp production may grow further and make possible an increase in the relatively low level of pulp consumption.

Argentina

At the rate of production prevailing during the first 10 months of 1949, Argentina's production of chemical pulp (including pulp not made from wood) for the whole of 1949 is not expected by the trade to differ materially from 1948 levels, when 25,000 tons of chemical pulp and 12,000 tons of mechanical pulp were produced. Recent studies indicate that, with improvement in transportation, enough pulpwood to double present pulp output could be supplied from the Paraná Delta region. This is important, as straw, reeds, cane, and bagasse, which form an important source of raw material, are now harder to obtain than in the past. New wheat-harvesting machines leave the straw bent or scattered and make its collection more difficult, while cane sugar mills have installed machinery for the use of bagasse as a fuel, since the supply of fuel oil has been uncertain.

Chile

A new sulphate wood pulp plant is projected between the Provinces of Nuble and Concepción in Chile. The capital is being provided by the Chilean Development Corporation and by Compañía Manufacturera de Papeles y Cartones.

Peru

A small pulp and paper mill is under construction near Chiclogo. Capacity is said to be 3,000 tons per years the raw material being bagasse. There is a, second project for a new pulp and paper plant, and a concession has been obtained from the Peruvian Government covering the import duties and certain other taxes for the required machinery, which has been valued at approximately $1,180,000. The Peruvian Amazon Corporation is also said to be investigating the establishment of a pulp mill in eastern Peru.

Uruguay

A new pulp and paper mill has been placed in operation in Uruguay, the raw material used being straw.

OCEANIA

Australia

According to recent reports, Australia's pulp and paper producing capacity is undergoing further expansion. One pulp mill is being expanded from a capacity of 36,000 tons per year to 61,000; at the same time, its capacity for producing bleached pulp is being extended. Four new machines constitute the main features of the first stage of the development program. When these are all in production, the total annual output of paper and paperboard is expected to exceed 180,000 tons.

Plans for the construction of a new mill in Queensland are also reported to be proceeding satisfactorily. The first machine to be installed will produce 13,500 tons of cardboard annually.

New Zealand

Construction has recently begun on New Zealand's first wood pulp mill, and over $500,000 worth of equipment has been ordered. This mill is scheduled to begin production at the end of 1951 with an initial output of 23,000 tons yearly. It will be the key unit in a development planned to have other wood utilization units closely integrated with it. These units will be a kraft paper mill with an annual output of 10,000 tons and a modern Swedish gang-saw mill with a yearly capacity, of 33,000 m³.

Another mill which eventually will have a much greater output is planned by the government, to be located on the east coast of the North Island. Present proposals are for an annual production of 51,000 tons of newsprint, 9,000 tons of printing papers, and 24,600 tons of unbleached pulp for export. The whole installation will include a groundwood mill with an initial pulping capacity of 150 tons a day, a sulphate pulp mill of similar capacity, a bleaching plant, and a sawmill with an annual capacity of 160,000 m³.

SOUTH AND EAST ASIA

Japan

Japan's production of all grades of pulp rose from slightly less than 300,000 tons in 1947 to 410,000 tons in 1948, and preliminary figures for 1949 show another increase to approximately one-half million tons. While mechanical pulp mills are running to capacity, output of chemical pulp amounts to about 54 percent of 1941 production. The: rayon pulp mills have an installed capacity sufficient to produce 180,000 tons per year; their production of 33,000 tons in 1948 and around 54,000 tons in 1949 indicates the present low rate of operation.

The major problem in Japan is inadequate pulpwood supplies. Although imports are anticipated, reforestation is said to be the fundamental long-range solution to the Japanese forest problem. Additional raw material is available in the form of rice, wheat, and barley straws. Over 16 million tons of these straws were available from the-1948 crops; and it has been said that nearly four times the present paper needs of Japan could be produced from such products.

Philippines

Establishment of a pulp mill to supply an existing paper mill was approved in October of last year. It is reported that US$ 600,000 will be made available from the national economic development fund to support this project. The mile is expected to conserve dollar exchange which otherwise would be required for obtaining foreign pulp.

WOOD PULP TRADE

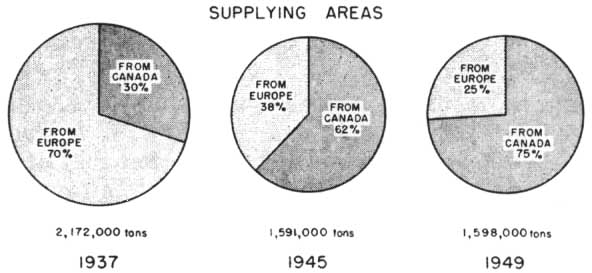

Despite the recovery toward the end of the year, Northern European pulp exports to the United States in 1949 fell 22 percent below the 1948 volume, and Canadian exports about 19 percent. The drop in Canadian exports of market pulp amounted to 27 percent.

The chart below illustrates the marked changes in the pulp supply sources for the United States market which have occurred over a period of thirteen years, and the trend toward increasing dependence on North American sources of supply. The prewar dominance of European suppliers was halted by wartime conditions, and is not likely to revive. In 1945, 62 percent of U.S. imports came from Canada, while the remaining 38 percent originated exclusively from Sweden. By 1949, pulp supplies from all European sources had dropped to 25 percent.

The consequences of the currency devaluations of 1949 are not all clear. The revived interest of American buyers in European pulp was due more to the upswing in business conditions in this U.S. paper industry than to devaluation. European sellers maintained more or less-the same dollar prices after the devaluation as before, and the depreciation of the Canadian dollar did not cause any reduction in Canadian pulp prices. Devaluation helped European exporters cover their relatively high production costs, and sales to the United States became temporarily more profitable than to other nations, whereas before devaluation the contrary was the ease. The difference in price levels has, however, since narrowed as a result of price rises on the European markets.

NORTH AMERICA

United States

In 1948 U.S. imports of market pulp dropped below the 1947 volume by about 400,000 tons. This downward trend continued through October 1949, when imports showed a marked-rise, achieving the highest monthly total since August 1948.

Total pulp imports for 1949 amounted to 1,598,000 tons, one-fifth less than in 1948. The largest declines were registered for Swedish and Finnish pulp (30 percent and 20 percent respectively), while imports from Canada dropped by 18 percent. Shipments from Norway, though quantitatively small, were over 150 percent greater than in 1948.

The types of imports reflected continued demand for the bleached categories. While imports of unbleached grades dropped 40 percent between 1948 and 1949, the bleached sulphite imports for the two periods were at the same level, and bleached kraft even achieved a gain of 40 percent.

Offers of small quantities of unbleached chemical pulps from the U.S.S.R. , as well as trial offers of both bleached and unbleached pulps by Czechoslovakian and Austrian producers, have been reported. Imports from Austria in 1948 were small; in 1949 they amounted to 3,000 tons and imports from Czechoslovakia to 1,000 tons.

In certain segments of the U.S. industry, concern is still felt about possible further effects of the devaluations and about the tariff reductions on certain' pulp products negotiated at Annecy, ranging up to 50 percent on some items.

Canad/I>

During 1948 Canada's pulp exports to the United States increased by about 6 percent over the 1947 volume and were nearly three times the prewar average. Its shipments to the United Kingdom rose by about 39 percent over 1947.

In 1949 pulp exports to the United States were approximately 1,400,000 tons, about 230,000 tons less than in 1948. Their dollar value was about 15 percent below the 1948 level (approximately US$ 177 million, compared with US$ 211 million in 1948).

The decline in shipments to the United States 1949 coincided with a reduction in exports of wood pulp to overseas destinations. Import restrictions and currency troubles are factors responsible for this reaction. Commonwealth countries have been the traditional markets, but they cannot afford the dollars. Canadian producers are eager to retain as much as possible of these markets, because a single market for pulp and paper products makes the Canadian manufacturer particularly vulnerable to fluctuations in the U.S. economy.

EUROPE

Exporting Countries

Finland. The reduction in prices and absorption capacity on world markets had a profound effect ' on Finland's pulp and paper exports. The economy of Finland is largely based on forest products industries: in 1948, for example, over 90 percent of land's total export receipts were derived from forest products; pulp and paper accounted for 51 percent.

During the seller's market of 1944 through 1947, the volume of exports expanded as rapidly as production capacity would permit. When a shift to a buyer's market occurred in the third quarter of 1948, rising production costs: and an unfavorable exchange rate prevented exporters from reducing prices. Exports leveled off late in 1948. Exports to the United States dwindled, aggravating the dollar shortage, and abnormally large stocks forced sizable production cutbacks. I

Similar conditions prevailed in the paper and paperboard industry, where 12 percent of the paper machines had to be shut down. This situation caused the export industries of the country severe losses, and was a major element in the first decision to devalue the Finnish currency in July 1949.

In the late summer, however, the market began to show firmer tendencies, and by November Finland had not only made up for previous export losses but had exceeded corresponding 1948 totals. Total 1949 pulp exports were 920,500 tons, of which sulphite comprised 450,000 tons, sulphate 311,000 tons, and mechanical 160,000 tons. The United Kingdom was the largest buyer. Despite increasing sales outlets in the United Kingdom and elsewhere in Europe, Finland will probably continue efforts to recover a larger share of the U.S. pulp market. At the same time, more Finnish pulp is expected to be converted into paper and board for export.

Sweden. By the beginning of December 1949 the year's production of chemical and mechanical pulp was reported as sold. Total pulp exports for 1949 amounted to 1,894,000 tons, an increase of nearly 214,000 tons over 1948.

Stocks have been reduced considerably, and late in 1949 chemical pulp stocks were scarcely more than half of the 300,000-ton total that existed on 1 January 1949.

In the latter part of 1949 Sweden made great efforts to counterbalance the earlier export losses on the U.S. market. So far as is known now, its exports to the United States in 1949 will amount to about 320,000 tons, or roughly 17,000 tons more than in 1948. Some mills are now reported to be converting substantial tonnages of rayon pulp capacity to the manufacture of paper grades, primarily for the U.S. markets.

Under the new Swedish-British trade agreement, the United Kingdom is prepared to buy increased quantities of pulp and paper from Sweden in 1950, a development foreshadowed at the Montreal Pulp Conference. In comparison with the agreement for 1949, the quantities stipulated mean 25,000 tons more paper pulp, 30,000 tons more mechanical pulp, and 45,000 tons more paper and paperboard.

Norway. Pulp exporters in Norway have no doubt derived advantage from the abolition of three taxes on wood which the industry found particularly burdensome. The saving to the producer through these tax removals is appreciable; for instance, on bleached sulphite nearly $18.75 per ton. In addition, the government has offered to rebate 9 kroner per cubic meter of wood to all firms purchasing more than their original quotas. A plan has also been evolved by the government whereby firms shipping into hard currency countries may retain 10 percent of the dollar exchange to use for imports of capital equipment. A similar principle has been put into practice by Finnish authorities.

Norwegian pulp shipments in 1949 were approximately 36,000 tons greater than in 1948.

Austria. With the slow improvement in the general economic situation, paper supplies on the domestic market have become almost normal, and governmental controls have been abolished during the past year. The Austrian pulp and paper industry is now making great efforts to improve its export prospects in its traditional markets. Exports were restricted to 6,000 tons in 1946 and 9,000 tons in 1947; but in 1948 they went up to 39,000 tons, and they will probably stand at a slightly higher level in 1949. Prewar exports amounted to 175,000 tons. Italy is now Austria's most important customer. The United Kingdom, Switzerland, and Greece are further potential markets.

Czechoslovakia. Czechoslovakia increased its pulp exports from 28,000 tons in 1946 to 38,000 tons in; 1948, a volume representing about 30 percent of the prewar rate. Total pulp exports for 1949 are expected to stand at about the 1948 level. Czechoslovak pulp producers have recently made efforts to extend their exports to the U.S. market.

Importing Countries

With the exception of Belgium, European countries imported somewhat larger quantities of pulp in 1949 than in 1948. The greatest percentage increase is noted for Italy, which doubled its previous pulp imports in order to expand its export trade in paper and paper products.

After a temporary slackening on some European paper markets, there is evidence now of a steadily growing demand, and it can be expected that at least as much pulp will be needed in 1950 by European importers as in 1949.

PRICES

The price decline on the pulp market since the fall of 1948 has been very far-reaching. This is illustrated by the course of Finnish wood pulp prices during 1349 on the United State, markets shown in Table 3.

Table 3. - Finnish wood pulp prices, U.S. market, 1949

|

Grade |

1949 Prices |

|||

|

1st Quarter |

2nd Quarter |

3rd Quarter |

4th Quarter |

|

|

|

(U.S. dollars per short ton ) |

|||

|

Bleached sulphite |

165.00 Dock |

132.50 F.A. |

118.00 F.A. |

118.00 F.A. |

|

Unbleached sulphite |

140.00 Dock |

124.50 F.A. |

100.00 F.A. |

100.00 F.A. |

|

Unbleached sulphate |

127.50 Dock |

112.50 F.A. |

85.00 F.A. |

82.50 F.A. |

|

Groundwood |

85.00 Dock |

75.00 Dock |

65.00 F.A. |

65.00 F.A. |

NOTE: Dock - price on dock, F.A. - cost of inland freight to pun chaser's mill absorbed by the seller.

The reduction in prices in Finnish markkas can also be illustrated as follows: While the volume of sulphite wood pulp exports in 1949 increased 21 percent over 1948, the value in markkas decreased 5 percent; the volume of sulphate wood pulp exports in 1949 decreased 6 percent from 1948, but their value decreased 28 percent.

After the waiving of the export fee in Sweden in September 1948, the Swedish exporters immediately reduced their prices in the United States, but not to the levels of the American domestic prices. The other exporting countries shortly followed suit. However, the attempt to win back American market by a radical price reduction failed, and only resulted in hesitation on the part of buyers in anticipation of further price cuts.

In the spring of 1949, Finnish and Swedish producers reduced their prices further to approximately the American level, without making greater sales. United States and Canadian domestic quotations were reduced at the same time, partly to offset this competition from Europe.

As soon as it was clear that Northern European sales efforts on the U. S. market had failed, quotations in Europe were also lowered; however, prices remained slightly higher than the American prices. At this stage American exports to Western Europe against Marshall Plan dollars, although the quantities involved were very small, contributed to lowering all market prices for pulp to approximately the American level.

At the close of 1949, the steady market for wood pulp in the United States in practically all categories, together with an approximate supply-demand balance in most grades, led to a greater firmness in world wood pulp prices.

Unbleached sulphite sold in late 1949 at $85-$90 per short ton, and unbleached kraft at $75. These figures, however, are an improvement over the minimum levels prevailing immediately after the market uncertainties which followed the currency devaluations. At that time unbleached grades sold at $10-$15 per short ton less.

On the U.S. market, bleached kraft was in the strongest position, while bleached sulphite appeared adequate to current demand. Small tonnages of Austrian bleached sulphites were in the market at $107 $110 per short ton on dock. Unbleached krafts, owing to continuous demand by nonintegrated mills, moved into a strong: position, and Northern krafts were able to command their prices at quoted contract levels. Pulp contract prices on the U.S. market during the first quarter of 1950 are shown in Table 4.

Table 4. - Pulp contract prices on U.S. market, first quarter 19501

|

Grade |

United States |

Canada |

Sweden (on dock Atlantic ports) |

|

|

(Dollars per short ton) | ||

|

Bleached sulphate |

118.00/126.00 |

126.00/- |

125.00/128.00 |

|

Unbleached Northern sulphate |

... |

82.50/105.00 |

82.50/85.00 |

|

Unbleached Southern sulphate |

80.00/82.50 |

... |

... |

|

Bleached sulphite, softwood |

118.00/- |

118.00/- |

118.00/- |

|

Unbleached sulphite |

100.00/- |

100.00/- |

100.00/- |

... - Not available.1 U.S. and Canadian wood pulp delivered prices with varying freight allowances. Full freight allowances are allowed on Northern European pulp. Finnish and Norwegian pulp prices are reported to be competitive with U.S. domestic grades.

Canadian and European producers have so far shown no inclination to lower their prices on the U.S. market under the minimum levels of domestic quotations; and in view of the present strong demand in the United States, there is every indication that prices will remain firm, at least for the immediate future.

Consumption of world pulp supplies

Prices of Swedish pulp on the British market for the fourth quarter of 1949 were agreed upon during September of last year, when the market was still rather weak. Swedish exporters agreed to price reactions, which, for certain categories, were quite considerable.

In recent contracts for delivery in the second quarter of 1950 the prices have been approximately as follows bleached sulphite £43-£44; easy bleaching sulphite £37-£38; strong sulphite £34-£35; unbleached sulphate £28.10.0 to £30 per ton, c.i.f. British ports

Bulk purchasing by the U.K. Government will come to an end on 1 April 1950.

WOOD PULP CONSUMPTION

Since the end of the war, consumption of wood pulp in the United States has shown a great increase, culminating in 1948 in an all-time high of 13.6 million tons for all grades of pulp (almost 65 percent more than in 1939).

However, the decline in paper and paperboard production during the first half of 1949 was reflected in a decreased consumption of wood pulp, and particularly of market pulp. Although pulp consumption during the last three months-of 1949 was tile highest on record, total consumption for the year was about percent (900,000 tons) lower than in 1948.

Consumption of pulp and, pulp products in 1950 will depend upon the aggregate economic and industrial activity of the country as a whole. Recent analyses of the U.S. economy provide promise for a high of activity and consumer expenditures: et least for the first' half of 1960. It is thus reasonable to expect that consumption of pulp and pulp products will continue at the present high levels for the same period.

The influence of economic fluctuations in the United States on the world market retarded Europe's recovering pulp consumption during 1949. There are clearly large unsatisfied demands in many European countries, which will grow with further economic recovery.

Consumption pulp and pulp products in other parts of the world over the next few years will largely depend on the realization of projects for installing new pulping capacity in response to rising effective demand. Technical progress in pulping methods, particularly of tropical hardwoods and other raw materials, holds great promise for the future.

WORLD PAPER TRADE

After the war the tonnage of paper and paper products available for export was considerably below prewar levels, and the requirements of many importing countries could not be satisfied. The paper industry of Central Europe was disrupted, and the Northern European countries were unable to reach their prewar output. Furthermore, their own greatly increased consumption of paper and paper products had considerably reduced the quantities available for export, while the strength of U.S. demand precluded any large North American exports. On the other hand, import demand in many countries was reduced below prewar levels by lowered purchasing power. The largest European importer, the United Kingdom, had restricted its consumption of paper and paper products to a minimum during the war, and many of the governmental controls on imports were continued thereafter. Even now the U.K. import figures are far below those of prewar. In a number of countries, also, the demand for imported paper and paperboard was kept down by the expansion of domestic manufacturing capacity.

However, in most countries effective demand rose more than output during the immediate postwar years. Since 1947 and through 1948 and 1949, although effective demand has still slightly exceeded supply, the situation has become more balanced. This does not mean that balance exists between potential requirements and supply, as UNESCO and FAO have frequently pointed out. International trade, however, is still restricted by numerous impediments, and as long as such conditions prevail, a more even flow of supplies to importing countries is not possible.

Paper prices in general continued to rise up to the end of 1948, when signs of a decline were apparent. During the first half of 1949, order shortages were so pronounced that some Northern European mills had to stop production for short periods.

During the summer of 1949 demand began to pick up. When pulp prices were raised and the effects of devaluation began to influence manufacturing costs, the prices of paper and paperboard had to be increased. This, however, has had no adverse result on effective demand.

NEWSPRINT

Newsprint manufacture accounts for about 28 percent of the world's consumption of wood pulp; and North America uses some three-fifths of the world's newsprint. Newsprint consumption in 1949 in the United States exceeded all previous records with a total of 5,000,000 tons, an increase of 56 percent over the prewar level. This increase has been made possible almost entirely through expansion of Canadian and U.S. output.

United States consumers of newsprint are now obtaining around 80 percent of their supplies from Canadian and Newfoundland mills, compared to 67 percent during 1935-39. The chasm between the dollar and non-dollar countries has been accentuated by devaluation, and the United Kingdom has turned from Canada to Northern Europe for its newsprint supplies.

PRODUCTION

North America. Production of newsprint in North America reached a new high of 5.5 million tons in 1949, an increase of 1.7 million tons over 1939. As compared with 1948, Canadian production increased by 2.8 percent and United States output by 3.5 percent. This record output, reflecting the still increasing United States demand, was made possible by capacity operation at the mills, technical improvements, and installation of faster machines.

Two newsprint mills have recently been built in the United States. A mill using de-inked newspaper as raw ma-serial, recently completed in Indiana, is expected to reach an output of 45 tons daily on a full operating schedule. A plant in Alabama will supply southern newspaper publishers with approximately 270 tons of newsprint daily. The erection of a third mill is proposed in Arkansas.

Europe and U.S.S.R. In 1949 practically all European newsprint-producing countries recorded increases over the preceding year. The most important gain, amounting to more than 140,000 tons, was registered by the United Kingdom; increases for most of the other European countries were on a much more moderate scale.

Despite increases in production of about 300,000 tons between 1947 and 1948, and of over 350,000 tons between 1948 and 1949, there is still much idle capacity; almost 360,000 tons of idle capacity is said to exist in Germany, the United Kingdom, and France, and over 360,000 tons in other European countries, including about 160,000 tons in Northern Europe. The reasons given for this unused capacity are the continued dislocation of world trade, currency difficulties, and shortage of pulpwood.

According to a report dating from the latter part of 1948, the Soviet Government has allocated 400 million rubles for the construction of paper mills in various parts of the Soviet Union. These mills will primarily produce newsprint, of which greatly increased supplies are necessary if the reported goal of 5,600 newspapers, with a circulation of 30 million copies, is to be attained.

DISTRIBUTION

In 1949, 86 percent of: all shipments leaving Canadian newsprint mills went to the United States, 7 percent to other foreign markets, and 7 percent to domestic markets. During 1935-39 the proportions had been 72 percent to the United States, 22 percent to the rest of the world, and 6 percent to domestic purchasers.

The distribution of Canadian shipments, as between the United States and other destinations, is shown in Table 5.

Table 5. - Distribution of Canadian newsprint shipments for export

|

Year |

Destination |

|||||

|

U.S.A. |

Others |

Total shipments |

||||

|

Quantity |

Index |

Quantity |

Index |

Quantity |

Index |

|

|

|

(1,000 metric tons) |

|||||

|

1935-39 Av. |

2,166 |

100 |

667 |

100 |

2,833 |

100 |

|

1940-45 Av. |

2,511 |

116 |

515 |

77 |

3,026 |

107 |

|

1946 |

3,232 |

149 |

621 |

93 |

3,853 |

136 |

|

1947 |

3,535 |

163 |

636 |

95 |

4,171 |

147 |

|

1948 |

3,745 |

173 |

484 |

73 |

4,229 |

149 |

|

1949 |

3,974 |

183 |

408 |

61 |

4,382 |

154 |

SOURCE: Newsprint Association of Canada. All figures have been adjusted to include shipments from Newfoundland.

United States imports reported obtained from Canada have jumped from approximately 2,170,000 tons prewar to nearly 3,980,000 tons in 1949. As compared with 1946, the 1949 actual imports from Canada are greater by 820,000 tons.

Canadian newsprint shipments to all destinations other than the United States averaged 667,000 tons during 1935-39. For 1949 such exports are put at 408,000 tons.

Before the war the United Kingdom was Canada's second largest market, taking an average of 270,000 tons from Canada and Newfoundland together for the years 1935-39. During the war, when it was cut off from Northern European supplies, it had to rely exclusively on Canadian supplies. Later, however, because of dollar shortages, its imports from Canada were cut to 90,000 tons a year, and were at about this level for 1949.

According to the latest reports, the United Kingdom will purchase no newsprint, from Canada during the first six months of 1950. It will then reconsider its further policy in the light of the exchange balances. This decision will release approximately 90,000 tons of newsprint capacity for other markets.

The United Kingdom is able to seek supplies outside the Canadian market because the Northern European producers are delivering newsprint at a competitive price, and are willing to sell for sterling.

The trade figures of other major importing countries also show significantly the shifting from North American to European sources of supply. Australia, for example, where Canada has traditionally been the main source of imports, is taking substantial tonnages from Northern Europe. In Latin America, while total newsprint imports dropped from an estimated 370,000 tons in 1948 to 330,000 tons in 1949, the share of Canadian shipments decreased from 48 to 34 percent, and Northern European shipments increased proportionately. Argentina has completely cut out newsprint imports from Canada. In recent years there has been a tendency for production in North America to be balanced-against the demand within the region. The rift between dollar and non-dollar countries, as regards newsprint distribution, has been widened, leaving the potential requirements of soft currency countries without apparent means of full satisfaction, because Northern European mills and forests cannot indefinitely support the rest of the world, even at its present low levels of consumption.

The distribution of Northern European newsprint exports, prewar and postwar, is shown in Table 6.

CONSUMPTION

Held down by supply shortages during and immediately after the war, consumption of newsprint in the United States has since shown a remarkable sustained rate of increase. As compared with a 1939 volume of 3,220,000 tons, consumption soared to 4,660,000 tons in 1948 and reached an estimated 5,000,000 tons in 1949. At this 1949 level, the increase over the prewar average is nearly 56 percent.

Through the fifteen years preceding the war, the proportion of total world newsprint supplies absorbed by the United States market, as compared with that consumed by other countries steadily declined, falling from over 53 percent of total world consumption in 1925 to 44 percent in 1935-39. Since the war this trend has been completely reversed, and for 1946-50 it-is estimated that the United States will consume 60 percent of the worlds supplies.

Comparing the five postwar years; 1946-50 with the five prewar years 1935-39, newsprint consumption in the United States has increased by over 1,360,000 tons a year, while consumption in the rest of the world has shown a decrease of over 1,134,000 tons per year.

Table 6. - Distribution of Northern European newsprint exports, prewar and postwar

|

Year |

Destination |

|||||||||

|

U.S.A. |

United Kingdom |

Latin America |

Others |

Total |

||||||

|

Quantity |

Index |

Quantity |

Index |

Quantity |

Index |

Quantity |

Index |

Quantity |

Index |

|

|

|

(1,000 metric tons) |

|||||||||

|

1935-39 Av. |

224 |

100 |

121 |

100 |

147 |

100 |

202 |

100 |

694 |

100 |

|

1946 |

25 |

11 |

12 |

10 |

105 |

71 |

285 |

141 |

427 |

62 |

|

1947 |

103 |

46 |

19 |

16 |

159 |

103 |

211 |

104 |

492 |

71 |

|

1948 |

216 |

96 |

29 |

24 |

120 |

82 |

233 |

110 |

588 |

85 |

|

19492 |

197 |

88 |

62 |

51 |

122 |

83 |

290 |

144 |

671 |

97 |

Situation in Europe

Pitprop supplies through 1949 proved adequate to cover the growing needs of European coal mines. In November 1949 this led the Pitprop Working Party of the ECE Coal Committee at Geneva to discontinue the import allocation system which had been in force since the end of the war. Since increased production and larger imports had resulted in bigger stocks in most countries, a situation forecast by the ECE Timber Committee at the beginning of 1949, no further special measures were considered necessary in the interests of consuming countries; substantial quantities of pitprops could be forthcoming, if really needed, from Canada and the United States.

PRODUCTION AND CONSUMPTION

The net pithead production of hard coal again increased in 1949, as shown in Table 1, and consumption of pitprops went up accordingly.

Table 1. - Coal production

|

|

Net pithead production of hard coal |

|||

|

1948 |

1949 |

1950 estimate |

||

|

(1,000 metric tons) |

||||

|

Belgium |

26,700 |

27,800 |

29,000 |

|

|

Czechoslovakia |

17,700 |

17,000 |

17,500 |

|

|

France 1 |

55,900 |

65,500 |

65,800 |

|

|

Germany (Bizone) |

88,600 |

104,800 |

112,000 |

|

|

Italy |

1,000 |

1,100 |

1,200 |

|

|

Netherlands |

11,000 |

11,700 |

11,900 |

|

|

Poland |

70,300 |

73,400 |

77,000 |

|

|

United Kingdom |

2198,900 |

2205,900 |

2214,000 |

|

|

|

TOTAL |

470,100 |

507200 |

531,400 |

SOURCES: Monthly Bulletin of Statistics (Statistical Office of the United Nations) and ECE Coal Committee statistics1 Includes the Saar.

2 Excluding open east.

Some coal-producing countries have stepped up domestic pitprop production in an attempt to confine imports, as far as possible, to dimensions which are unobtainable from their own production. Upon the whole, however, domestic production in pitprop consuming countries showed a declining tendency.

EXPORTS

During 1949, the pitprop exports of the main European exporting countries increased considerably and were in the-aggregate nearly one million m³ or about one-third higher than in 1948. In Northern Europe shipping conditions up to the end of 1949 were favorable, so no difficulties were encountered in carrying out the remaining 1949 deliveries; it is reported that only small quantities, if any, were left lying for the winter in the northern ports.

The most interesting change in the pitprop trade picture as compared with the immediate postwar years is the increase in Sweden's exports. This country, which since the early 1930's had not been a large-scale pitprop exporter, shipped about 660,000 m³ in 1949, compared with 195,000 m³ in 1948. The sudden expansion was mainly attributable to Sweden's difficulties in disposing of its wood pulp during the first half of the year and the resultant smaller demand for pulpwood. Yugoslavia and Portugal also noticeably increased their pitprop exports. It is understood that Romania also increased its exports, mainly to Turkey, although figures are not available.

Exports from the U.S.S.R. and Eastern Germany, on the other hand, remained relatively insignificant and were no doubt far below potential export capacities. Exports from the U.S.S.R. showed an increase over 1948, perhaps foreshadowing larger future exports, and exports from 13 astern Germany (mainly to Western Germany) rose from about 100,00p m³ in 1948 to 141,000 m³ in 1949.

IMPORTS

Reports from importing countries for 1949 reflected the clear improvement in the supply situation. The increased imports brought about a general improvement in the consuming countries' stock position as compared to the previous year.

The 1949 import requirements of the Saar, about 490,000 m³, were filled from German. sources, particularly from the French Zone. Some quantities (40,000 m³) of hardwood pitprops were also delivered by France.

The disastrous forest fires in August 1949 ravaged' 70,000 hectares of forest in the Landes, - Southern France. The quantities of pitprops available as a result of salvage operations were found to be about 900,000 m³. Out of this quantity about 650,000 m³ had been taken up by the French coal mines by the beginning of 1950 and-about 145,000 m³ placed on export markets.

It should be pointed out, moreover, that the latest estimates of timber available as a result of the fires also included about 900,000 m³ of pulpwood, some part of which might be diverted for use as pitprops if circumstances warranted. The Landes fires, however, may not eliminate the need for imports into France ire 1960.

OUTLOOK FOR 1950

As indicated in Table 1, the planned production of hard coal for 1950 in the main producing countries is about 5 percent higher than for 1949. If this goal is attained, consumption of pitprops should increase accordingly.

The estimates made at the sixth session of the ECE Timber Committee actually showed an apparent deficit of 0.4 million m³ in pitprop exports likely to be available in 1950 as compared with import requirements. The deficit was noted as amounting to less than 3 percent of estimated requirements for the year. The Committee, however, pointed out that increases in pitprop stocks in certain consumer countries would tend to offset the apparent import deficit.

Taking all factors into consideration, it is believed that stocks and new supplies in 1950 should be adequate to cover consumption..

EXPORT POSSIBILITIES OF THE MAIN PRODUCING COUNTRIES FOR 1950

Finland and Sweden

These two countries have announced 1950 export availabilities of 1,000,000 m³, viz., Finland 700,000 and Sweden an estimated 300,000 m³. These quantities, however, are likely to be considerably exceeded provided that contracts can be placed with consumer countries. The United Kingdom could take up 525,000 m³ of the Finnish export availabilities and more than the total Swedish forecast.

France

An export availability of 100,000 m³ has been announced. Possible outlets for the supplies made available by the Landes fires, in addition to the United Kingdom and Belgium, are Western Germany, the Ruhr, and Italy. It is felt, however, that a certain portion of the fire-damaged pitwood will have to be sold as pulpwood.

Norway

Norway has announced an export availability of 80,000 m³ for 1950. This quantity, however, may be increased through diversion of pulpwood, as in the other northern exporting countries. The United Kingdom is expected to contract for up to 100,000 m³ for 1950 deliveries.

Central Europe

Austria has announced an export availability of 120,000 m³, Poland 250,000 m³, Switzerland 25,000 m³, and Yugoslavia 175,000 m³ These quantities are likely to be exceeded if more contracts can be placed with consumer countries. The United Kingdom alone could place contracts in 1950 for 250,000 m³ from Poland and 200,000 m³ from Yugoslavia. Furthermore, Belgium is expected to import about 45,000 m³ from Poland.

Portugal

An export availability of 200,000 m³ has been announced, of which 110,000 m³ is supposed to he exported to the United Kingdom.

U.S.S.R. and U.S.S.R. Zone of Germany

An export availability of 1,100,000 m³ from these sources was estimated at the sixth session of the ECE Timber Committee. This figure was based on export arrivals in some of the main consuming countries and on the fact that Poland had to cover its import requirements from these sources. As regards U.S.S.R. proper, speculations have been made regarding greater exports from this source to the main consuming countries in the course of 1950, the United Kingdom for instance expecting around 125,000 m³ It is, however, very difficult to confirm these speculations, as the present Soviet plans for pitprop exports are completely unknown.

Western Germany

An export availability of 300,000 m³ has been announced for 1950. This quantity, however, probably applies to the French Zone only, and is likely to be exported almost entirely to the Saar. The figure quoted seems to include a carry-over of 140,000 m³ from 1949 contracts, but does not include quantities contracted before 1949 which are still undelivered.

OUTLOOK FOR 1951

The ECE Timber Committee has obtained information from countries as to estimated production, import requirements, and export possibilities for 1951. The tentative figures submitted, when totaled, showed a pitprop deficit of slightly over one million m³ in export supplies as contrasted with import requirements. Because of the tentative nature of the figures and the tendency of importing countries to overstate requirements and exporting countries to be cautious, the Timber Committee was not alarmed at the apparent deficit. In addition, it noted that changes in the requirements for pulpwood could have considerable effect on pitprop availabilities.

Personalities

· Harry T. Gisborne, Chief of the Division of Forest Fire Research, Northern Rocky Mountain Forest and Range Experiment Station, died of a heart attack on 9 November 1949 at Gates of the Mountain, Helena National Forest Montana. Mr. Gisborne was internationally known for his pioneer work in measuring and rating weather factors which influence behavior of forest fires. He developed the system of measuring humidity fuel moisture, precipitation, and wind velocity which can be translated into numerical terms of fire danger, and de signed weather instruments now widely used on forest fire weather stations.

· Luang Samarn Varnakij has been appointed Director-General of the Royal Forestry Department, Thailand, on the retirement of Mom Chao Subsuekhswasti Suekhswasti.

· Ingenieur F. W. Malsch has been appointed Director of the State Forest Service in the Netherlands. He succeeds Dr. J. A. van Steijn, who retired on 1 October 1949 after a long and distinguished career in forestry,

· Arthur Upson, Director of the Tropical Region of the U.S. Forest Service and of the Insular Forest Service in Puerto Rico since 1943, has accepted all assignment to do special wood utilization work at the California Forest Experiment Station. He has been succeeded by Henry B. Bosworth, Supervisor of the Texas National Forests.

![]()

![]()

![]()

{kind=link}

{kind=link}