![]()

![]()

![]()

Dr Audun Lem

Fishery Industry Officer

Fishery Industries Division

FAO Fisheries Department

1. INTRODUCTION

This report is based upon the country reports from participating SADC countries and integrated with data from FAO trade and production statistics, FAO GLOBEFISH Research Programme reports as well as material from the FAO Umbrella training programme on the Uruguay Round Agreements. The text of the Code of Conduct for responsible fisheries, article 11 has been consulted as has the text of the various WTO agreements, the SADC Trade Protocol and the SADC Draft Protocol on Fisheries. National legislation on trade has not been consulted.

2. EXECUTIVE SUMMARY

All participating SADC countries are WTO members or WTO observers with the obligation of initiating membership negotiations. As such they are all party to the WTO trade agreements. Observance of the WTO agreements is also embedded in the Code of Conduct for responsible fisheries, in the SADC Trade Protocol and the SADC Draft Protocol on Fisheries. Scope for national or regional deviance from WTO agreements is therefore minimal.

The WTO Enabling Clause opens for preferential access for products from developing countries to developed countries on non-reciprocal basis. The Enabling Clause is the legal basis for regional arrangements among developing countries.

SADC intra-regional trade in fish and fishery products is limited, although formal trade barriers on a regional level have not been reported. Most trade is in exports to the EU and US markets. The main difficulty encountered in exporting to these markets is adhering to requirements on HACCP. As reflected in the country reports, there is a need for most countries to increase national capabilities in HACCP training as well as in fish inspection and laboratory services.

There is also a general need to strengthen national and regional training activities on the WTO agreements. This would include training on WTO member countries’ rights and obligations under the WTO agreements and on the workings of the WTO Dispute Settlement Mechanism. Such training programmes could also prove beneficial in the case of preparing joint SADC positions in international multilateral trade negotiations.

3. SPECIFIC TRADE ISSUES FOR SADC WORKSHOP ON MARINE POLICY ISSUES

Problem area 1 for Trade: Quality/food safety.

Most countries identified in their country reports various problems in adhering to import requirements regarding food safety in major markets, and in particular for exports to the EU. This became a crucial issue after the mandatory introduction of HACCP in 1998 in the EU and the USA.

HACCP introduction proved a true paradigm shift in international food safety and quality standards as they differ fundamentally from previous systems of sampling and control of end product. HACCP systems are recognised by international organizations such as FAO and WHO and have been adopted by the Codex Alimentarius Commission, the body responsible for implementing the Joint FAO/WHO Food Standards Programme.

The responsibility of fulfilling HACCP requirements lies first and foremost with the industry, as it is the industry itself which must implement and continuously maintain the HACCP programs. In many countries, the problem of maintaining quality and safety standards in fish handling or processing is exacerbated by lack of institutional capacity in inspection services and unavailability of laboratory services. This is especially the case for countries on EU list 2 from which only a few companies are exporting to EU markets.

SADC Countries included in the EU lists authorising the import of fishery products for human consumption:

|

Country |

List |

Number of authorised companies for list 1

Countries |

Exports in 1999 |

|

Tanzania |

1 |

38 |

60,202 |

|

Mozambique |

2 |

|

76,861 |

|

South Africa |

1 |

242 |

260,056 |

|

Namibia |

1 |

89 |

344,017 |

|

Angola |

2 |

|

10,043 |

|

Seychelles |

1 |

17 |

12,318 |

|

Mauritius |

1 |

8 |

38,558 |

Whereas it is easy to sympathise with the problems encountered by industry in many developing countries, this is not likely to bring any relief for exporting companies. Food safety issues in major import markets are consumer driven, and political or diplomatic efforts will, at best, only have a minimal effect. In the long run, with increasing trade in food products and rise in third country processing, food safety concerns will probably increase and food safety standards expected to be tightened even further.

On one hand, this gives competitive advantages of producers with good safety records; on the other hand it calls for added investment in processing lines as well as in inspection services.

As reported in the country reports, intra-regional trade is limited with the major export markets being the EU, followed by NAFTA. Formal barriers to intra-regional trade have not been reported.

Possible actions:

Problem area 2 for Trade: Constraints on individual action because of international obligations under WTO and other agreements

All coastal SADC countries are WTO members (Angola, Namibia, South Africa, Mozambique, Tanzania, Mauritius) or observers with the obligation to negotiate membership (Seychelles). They are therefore bound by the specific agreements that are part of the WTO multilateral trade agreements. It is important to underline the fact that fish and fishery products are not covered by the Agreement on Agriculture but are treated as industrial goods in the context of international trade.

The most relevant agreements for fish and fishery products are: the General Agreement on Tariffs and Trade (GATT), the Agreement on the Application of Sanitary and Phytosanitary Measures (SPS), Agreement on Subsidies and Countervailing Measures (Subsidies), Agreement on Implementation of Article VI of the General Agreement on Tariffs and Trade 1994 (antidumping), and the Agreement on Technical Barriers to Trade (TBT). In addition to these, it is expected that the issue of investment (equal treatment of foreign investors) will be highlighted in the new Round of Multilateral Trade Negotiations expected to start later this year. This could have implications for restrictions on foreign ownership in fishing vessels, fish processing or licences for aquaculture production.

In addition to their individual obligations as WTO members, the SADC Trade Protocol also makes specific reference to the WTO agreements, and the various articles in the Protocol have references to their relevant counterpart agreements of the WTO. Further, the SADC Draft Protocol on Fisheries refer to the binding principles of the Code of Conduct for Responsible Fisheries, which states in its article 11.2.1 on Responsible International Trade. The Provisions of this Code should be interpreted and applied in accordance with the principles, rights and obligations established in the World Trade Organization (WTO) Agreement.

The specific reference to the various WTO agreements in the SADC protocol should also preclude national legislation from including barriers to trade. In any case, no country has reported the existence of formal barriers to intra-regional trade in the SADC region.

Conclusion: the actions of SADC countries are bound by their commitments as members of WTO. It is therefore of extreme importance that there is a thorough understanding among member countries of the WTO and the agreements, not only for ensuring that national legislation or procedures are not in conflict with international obligations but also to fully understand their rights of member countries in possible trade disputes and how such disputes can be settled. In addition, a thorough understanding among countries is also needed in order to negotiate effectively in trade negotiations, both as individual countries and as the SADC region.

FAO is offering its member countries technical assistance concerning a wide range of WTO-related issues under the Umbrella training programme. Especially the obligations of WTO members associated with the SPS and TBT Agreements have resulted in a significant upturn in requests for FAO technical assistance. Specific regional workshops on fish trade may also be organised where feasible, as fish and fisheries products are not covered by the Agreement of Agriculture.

The WTO and the EU also offer support and assistance to developing countries on the WTO agreements.

Possible actions:

4. SYNTHESIS OF COUNTRY REPORTS ON TRADE AND MARKETING

The numbering in this section follows the responses as given in the synthesis report.

3.5 Trade in fishery products

3.5.1 Marketing

3.5.1.1 Exports to and imports from SADC countries over the past 5 years

The statistics reported are generally incomplete. As a rule, trade with other SADC countries is only a very small fraction of total trade in fish products. The major export market is the EU. The exceptions given are imports of frozen tuna from SADC countries for tuna canning in Mauritius and some trade in small pelagics and canned fish. Unfortunately, the national report for Namibia, the main exporting country did not report any statistics.

3.5.1.2 Contribution of fishery products to the balance of trade and to foreign exchange earnings

Export earnings from fisheries are generally very important to the SADC countries, especially for the island states (in Seychelles for instance fisheries exports represent around 94% of total exports). Regrettably, statistics for Namibia were not reported but FAO fisheries statistics show total Namibian fish exports in 1999 at 230,000 tonnes with a value of US$344 million.

3.5.1.3 Efforts to promote increased fish consumption, particularly for health reasons

There is a large variation in current consumption of fish in SADC countries and the need for active promotion of fish differs accordingly. Only Tanzania and Namibia report activities to promote increased fish consumption. FAO statistics show that fish consumption in 1997 for SADC varied from 65 kg in the Seychelles and 21 kg in Mauritius to 2 kg in Mozambique[26]

3.5.1.4 Impact of trade controls on fish products

Most reporting countries indicate that trade controls improve quality. Only South Africa certifies that fish exported has been caught legally.

3.5.1.5 Constraints on the international marketing of fish products, especially where due to foreign attitudes towards the environmental acceptability of fishery management or exploitation practices.

Potential problems are related to difficulties in following standards of export markets in general and the EU in particular but they relate to quality, packaging and labelling, and not to environmental issues or sustainability. It was sometimes felt (Tanzania) that embargoes by importing nations were not scientifically motivated.

3.5.1.6 Hidden barriers to the international trade of fish products

Potential problems are related to difficulties in following standards of export markets in general and the EU in particular but relate to quality and food safety. The EU accepts Angolan certificates only for unprocessed fish whilst South Africa is not allowed to export shellfish to the EU due to the lack of adequate water monitoring programmes. Tanzania suffered an EU embargo in 1999, although as mentioned in section 3.5.1.5. the motivation for the embargo is considered unscientific.

3.5.2 Quality and safety assurance

3.5.2.1 Consideration by the fishing sector of the importance of food safety in its harvesting and production.

All countries report the importance of food safety in general and how the following of regulations and standards is necessary in order to export, especially to the EU.

3.5.2.2 Incentives, and current control system, to ensure the nutritional value, quality and safety of fishery products.

The quality and safety of fish products has improved through increased requirements from export markets. Most countries report the use of HACCP systems. It is unclear though how this has been translated into national legislation with subsequent improvements in quality for domestically marketed products.

3.5.2.3 Co-operation between the fishing industry and other relevant actors to define rules and organise the control of quality

There seems to be no formalised co-operation between the fishery sector and other sectors. However, new legislation concerning food safety applying to all food products is forcing closer relationships between sectors, as many of the perceived health hazards are the same for all foods.

3.5.2.4 Availability of trained staff to support the fishing industry in the implementation of quality assurance programmes and to verify their effectiveness

Responses vary between countries. Some countries report adequate personnel levels but most report inadequacies in both numbers and qualifications. All countries report improvements and ongoing training activities.

3.2.5.5 Effectiveness of the application of HACCP principles and the Codex Alimentarius

All countries report the required use of HACCP programmes and most consider the application to be effective. Mozambique and Mauritius report deficiencies in the effective application of HACCP.

3.5.2.6 Certification of shellfish-producing coastal areas

Several countries do not have any production of shellfish; most of those who do report monitoring of water quality.

3.5.2.7 Initiatives on the certification of fish products (as “being produced in an environmentally acceptable manner”)

All countries report that the main focus is on food safety and not on environmental issues. Domestic consumers are mostly price oriented.

5. TRADE POLICY IN MARINE FISHERIES FOR SADC COUNTRIES

5.1 SADC and WTO membership

All coastal SADC countries are WTO members or observers committed to start membership negotiations.

The following countries are members of the WTO: Angola, Namibia, South Africa, Mozambique, Tanzania, and Mauritius. Seychelles is an observer to the WTO, and as observer must commence negotiations within 5 years of getting observer status.

5.2 SADC and fish trade

SADC countries are net fish exporters. The main potential problem in trade lies in the importing countries and are linked to regulations on food quality and safety, including specific requirements to handling and processing. For this reason, many exporting countries perceive food safety regulations in importing countries as potential trade barriers.

The introduction of HACCP in EU and US in 1998 has accentuated the problem. Today, Namibia, South Africa, Tanzania, Mauritius and the Seychelles are on EU list 1 with a total of almost 400 approved production facilities. Angola and Mozambique are on EU list 2 and imports from these two countries are admitted on a case by case basis.

Based on the national reports, there is clearly a need for upgrading institutional capacity in many countries to comply with new food safety rules in export markets. WTO, FAO and EU can upon request all give assistance on these issues.

International duties applicable to fish and fishery products were reduced as a result of the Uruguay Round and are currently reported to average around 4%. However, the averages hide many tariff peaks as well as the problem of tariff escalation which in many cases can be a significant problem to value addition.

On a general level, duties have ceased to be a major obstacle to international fish trade, also helped by an overall growth in imports in major markets. The result is that regulations covering other aspects of trade such as quality and safety issues take on a growing importance.

5.3 SADC regional trade

SADC intra-regional trade is limited. Formal barriers to intra-regional trade have not been reported, but other export markets such as the EU and NAFTA are able to pay higher prices, despite the longer distance involved. However, one can not exclude a priori a possible lack of efficient regional distribution systems or inadequate infrastructure as partly responsible for the limited regional trade. In several other regions, traditional trade patterns for export products are with international markets only and with little concern given to the development of regional trade links.

Of crucial importance to the development of increased regional trade are of course improved infrastructure and communications, but also stable economies, well-working financial systems and a tranquil political situation.

5.4 Links to WTO trade agreements

SADC countries that are WTO members have to comply with WTO agreements (SPS, TBT, etc). The Protocol of Trade and the Protocol on fisheries seem to take well into account the overriding principles of WTO. In addition, the albeit voluntary Code of Conduct 11.2.1 stresses WTO compliance:

“The provisions of this Code should be interpreted and applied in accordance with the principles, rights and obligations established in the World Trade Organization (WTO) Agreement”.

5.5 Food safety and quality

The country reports are short on trade and marketing issues but this fact probably reflects the design of the questionnaires. Problems with food quality and safety and adherence to import requirements in EU markets are mentioned by several respondents. As a consequence of increased standards in export markets, several respondents report increased levels of food quality and safety also for products to domestic markets. This is in line with FAO experience in other developing countries.

5.6 Fish trade and the WTO agreements

Fish and fishery products are not covered by the WTO Agreement on Agriculture, and fish is, by default, treated as an industrial product.

This has implications for subsidies in fisheries but is probably of limited relevance for fisheries in SADC countries.

The issue of national preferences, whether or not linked to subsidies, could arise with the new round of multilateral trade negotiations, in particular in the discussion of investment. This could have consequences for national policy regarding ownership of fishing vessels, fishing licenses and processing operations.

5.7 SADC as part of ACP (Africa Caribbean Pacific) Countries

With the expiration of the Lomé Convention in 2000, a new Partnership Agreement between the European Community and the African, Caribbean and Pacific (ACP) States was concluded. The agreement will regulate trade between the two groups of countries and define development co-operation strategies. The Partnership agreement applies to all SADC countries except South Africa, which has a separate agreement with the EC.

As the EC-ACP agreement gives preferential treatment for products originating in ACP countries, a waiver has been requested from WTO. This is possible under the so-called Enabling Clause, which gives preferential treatment to products from developing countries.

The Enabling Clause, officially called the “Decision on Differential and More Favourable Treatment, Reciprocity and Fuller Participation of Developing Countries” was adopted under GATT in 1979 and enables developed members to give differential and more favourable treatment to developing countries.

The Enabling Clause is the WTO legal basis for the Generalized System of Preferences (GSP) and the Global System of Trade Preferences (GSTP).

Under the Generalised System of Preferences, developed countries offer non-reciprocal preferential treatment (such as zero or low duties on imports) to products originating in developing countries. Preference-giving countries unilaterally determine which countries and which products are included in their schemes.

Under the Global System of Trade Preferences, developing countries which are members of the Group of 77 exchange trade concessions among themselves. UNCTAD provides technical assistance to beneficiaries and conducts analyses of the various schemes.

The Enabling Clause is the legal basis for regional arrangements among developing countries.

5.8 EU Programme for the least developed countries

The recent EU initiative of giving improved access for the world’s 48 poorest countries would also benefit some SADC member countries. The amendment regarding the gradual duty-free inclusion of certain commodities does not apply to fish and fishery products, which as such, would have immediate quota-free duty-free access to EU markets.

ANNEX I

SADC TRADE IN FISH AND FISHERY PRODUCTS WITH EU AND NAFTA

Source: GLOBEFISH Report on Regional trade agreements, chapter on SADC. (FAO, 2001, in press)

Author: Linn Helland.

The Southern African Development Community (SADC)

General information

Establishment and Member states

The Declaration and Treaty establishing the SADC, which replaced the Southern African Development Co-ordination Conference, was signed in August 1992 with the objective of working towards economic liberation between the member states. The current member states are Angola, Botswana, the Democratic Republic of Congo, Lesotho, Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland, Tanzania, Zambia and Zimbabwe (Underlined countries with marine coastal waters).

Objectives

The Treaty does not only cover economical issues but also functions as a political organization with principles of inter alia equality, solidarity, human rights and democracy. The trade and development contract signed in 1996 seeks to establish a SADC free trade area within eight years, i.e., 2004 and the gradual elimination of tariffs and non-tariff trade barriers to trade in the interim. Originally ratified by five member states, the aim is achievement of free trade by the year 2008. Others are in agreement on a tariff liberalisation program, currently being negotiated, and this program is less ambitious than the one under CBI and COMESA. Also, unlike agreements under the CBI, these trade liberalisation agreements among SADC countries allow for special treatment of sensitive products, agricultural products in particular.

Recent developments

COMESA member states have proposed merging with SADC to avoid duplicating their economic development efforts. SADC might be concentrating on the improvement of the economy through increased trade. According to COMESA members a free trade area in the region will create a wider market for goods produced in the region to the outside world. SADC is also currently involved in an institutional restructuring to meet the challenges of the international environment. An option for SADC is to position itself in a world of accelerating global integration by forming regional blocks to facilitate trade with other regional trade blocks. Mozambique has also proposed the establishment of a Southern Africa Free Trade Zone. This would include liberalisation of trade, of foreign exchange regulations and of the financial sector in general.

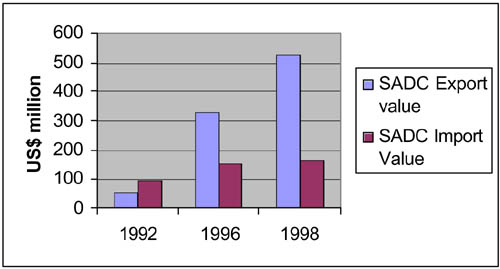

Total trade of fish

The exports from the SADC show the same trend as for COMESA. The exports experienced a large increase after the signing of the agreement in 1992, and an even further increase from 1996 to 1998, exceeding ECU 500 million.

Imports have been relatively stable amounting to ECU 170 million in 1998.

Figure 1: Total value of imports and exports from SADC of fish and fishery products (in US$ million)

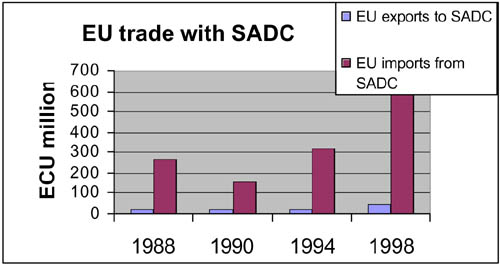

Trade with other regions (EU and NAFTA)

Trade between SADC and the EU has been increasing over the last decade, with an exception for exports to the EU from 1988 to 1990. Imports of fish products to the EU from SADC have been increasing heavily, exceeding ECU 600 million in 1998. This corresponds to a doubling of values every four years and shows the increasing importance of fish trade with the EU for the economies of the SADC countries.

Exports from the EU to SADC have increased as well, although not at the same pace, but remain at low absolute levels.

Figure 2: EU’s trade with SADC in fishery products 1988-1998 (in ECU million)

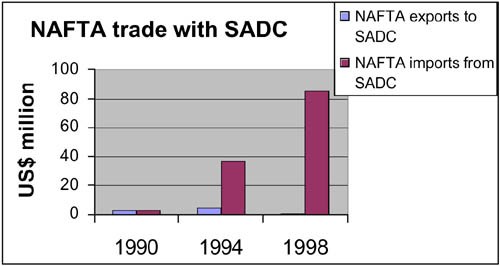

The same trend shows for NAFTA. Exports to Canada and the U.S. from the SADC region have more than doubled every four years, reaching a value of over US$ 80 million in 1998. SADC imports from NAFTA are, however, minimal. This result is similar to the one observed for COMESA and demonstrates the enormous increase in NAFTA’s imports from African countries.

Figure 3: NAFTA’s trade of fishery products with SADC (in US$ million)

ANNEX II

EXPORTS FROM SELECTED SADC COUNTRIES OF FISH AND FISHERY PRODUCTS

|

Tanzania |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

6,383 |

7,922 |

7,024 |

12,775 |

19,118 |

20,381 |

41,344 |

64,691 |

82,221 |

60,202 |

|

Mt |

1,719 |

1,540 |

1,398 |

7,763 |

12,491 |

17,350 |

22,596 |

27,213 |

46,489 |

28,679 |

|

Mozambique |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

50,629 |

63,240 |

66,453 |

70,802 |

59,475 |

65,113 |

68,692 |

85,400 |

71,548 |

76,861 |

|

Mt |

6,336 |

7,841 |

8,610 |

8,699 |

7,990 |

9,672 |

7,767 |

10,367 |

9,382 |

9,549 |

|

South Africa |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

117,393 |

154,559 |

181,239 |

199,030 |

255,996 |

242,284 |

201,620 |

219,054 |

244,248 |

260,056 |

|

Mt |

60,362 |

73,870 |

150,568 |

122,671 |

177,993 |

95,913 |

85,420 |

97,200 |

128,882 |

123,679 |

|

Namibia |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

0 |

0 |

0 |

0 |

270,580 |

291,704 |

200,678 |

238,223 |

300,587 |

344,017 |

|

Mt |

0 |

0 |

0 |

0 |

118,554 |

136,233 |

205,268 |

209,752 |

252,920 |

226,108 |

|

Angola |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

3,490 |

4,830 |

5,657 |

4,932 |

7,165 |

5,768 |

3,922 |

9,273 |

11,618 |

10,043 |

|

Mt |

1,044 |

1,224 |

1,456 |

2,279 |

2,221 |

2,883 |

1,358 |

3,680 |

5,790 |

5,307 |

|

Seychelles |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

13,255 |

16,119 |

17,446 |

14,323 |

21,694 |

22,713 |

39,733 |

33,350 |

27,306 |

12,318 |

|

Mt |

5,727 |

7,627 |

6,644 |

5,189 |

9,066 |

6,846 |

14,625 |

19,482 |

11,414 |

9,200 |

|

Mauritius |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

|

Usd (,000) |

10,772 |

20,217 |

20,106 |

23,108 |

30,391 |

38,137 |

42,613 |

45,416 |

42,793 |

38,558 |

|

Mt |

3,742 |

6,748 |

7,567 |

8,511 |

9,899 |

13,569 |

14,122 |

15,912 |

13,019 |

15,203 |

Source: FAO

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}