![]()

![]()

![]()

Delegation members:

- Mr Ndiaga Gueye, Director of Marine Fisheries, DPM, 1 rue Joris BP289

Tel.: 00 221 821 65 78, email: [email protected]

Mr Boubacar Bâ: Director, Cellule d’études et planification

Tel.: 00 221 821 94 69 email: [email protected]- Mr Aliou Faye, Coordinator, Unité de politique économique, Ministry of Finance

Tel.: 00 221 823 34 27

PREFACE

The present document constitutes the contribution of the the Senegalese delegation to the meeting on fishery tax reform at the FAO in Rome

This document is a detailed account of the situation of Senegalese fishery resources and its current trends. After a brief review on the importance of fishery economy as well as its contribution to the Gross National Product (GNP), it provides policy and strategy solutions to correct for weaknesses and drawbacks, which are major obstacles to the fishery and aquaculture sector's development.

Regarding the tax system, this document provides an overview of the current fiscal fisheries policy. A study is being launched to provide a detailed estimation of whether the current system should be maintained and whether it is beneficial to fisheries or even to the national economy.

As for fishing agreements, a detailed analysis on Senegalese experience, and results of the evaluation of the Senegal-European Community draft agreement from 1997-2001 are provided.

The resulting effects of the European Union Fishing Agreement (Accord de pêche communautaire - APC) and their relevance are clearly brought into view. Likewise for the use of financial compensation resulting frrom this fishing agreements. The beneficial characteristics of such an agreement are clearly brought to the fore, as opposed to the multiple constraints linked to the exploitation of fishing stocks, the balance of public finance and development in general.

LIST OF ABBREVIATIONS

|

MP |

Ministère de la pêche |

|

CEP |

Cellule d’études et de planification |

|

DPCA |

Direction de la pêche continentale et de l’aquaculture |

|

FPE |

Fonds de promotion économique |

|

DPM |

Direction des pêches maritimes |

|

BCPH |

Bureau de contrôle des produits halieutiques |

|

CNCPM |

Conseil national consultatif des pêches maritimes |

|

CNFTPM |

Centre national de formation des techniciens des pêches maritimes |

|

SAGE |

Service de l’administration générale et de l’équipement |

|

CEPIA |

Caisse d’encouragement pour la pêche et les industries annexes |

|

CCIP |

Commission consultative pour les infractions de pêche |

|

DPSP |

Direction de la protection et de la surveillance des pêches |

|

CCAL |

Commission consultative d’attribution des licences de pêche |

|

CLP |

Comités locaux des pêches |

|

CRODT |

Centre de recherches océanographiques de Dakar-Thiaroye |

|

OEPS |

Observatoire économique de la pêche au Sénégal |

|

FENAGIE |

Fédération nationale des GIE de pêche |

|

FNMS |

Fédération nationale des mareyeurs du Sénégal |

|

GAIPES |

Groupement des armateurs et industriels de la pêche au Sénégal |

|

CNPS |

Collectif national des pêcheurs artisans du Sénégal |

Introduction

The marine fishery sector in Senegal plays a major socio-economic role. Compared to other primary sector activities such as agriculture and farming, fisheries has recorded growth which has had a major impact on the improvement of coastal population revenues, as well as on investment and fishery product exports.

After considerable growth, the capture fishery sector in Senegal faced major difficulties due to overexploitation of the most commercially important resources and uncontrolled expansion of fishing, processing and canning capacities.

There was a sustained growth of fishery production until 1985, when landings began to regress. Development of artisanal fishing effort was regular and in the meantime, in the industrial fishery sector, the number of vessels remained stable.

The fall in production and the increase in fishing effort have led to conflict and various voluntary incursions of artisanal fishing crafts or industrial fishing vessels in neighbouring country fishing grounds, without authorization.

At the same time, European Community agreements are still being renewed, even though they pose a serious threat to resources already fully exploited by national artisanal and industrial fleets, this however does not apply to high-sea resources.

It has become an urgent necessity for the Government to maintain or re-establish stocks at economically productive levels. Growth in fishing capacity must also be stopped, and fishing effort control improved.

Due to this situation, fishing authorities have set up a new policy and taken action to improve fishery management. The evaluation of the European Union Fishing Agreement (Accord de pêche communautaire) and the prospect of a fishery sector tax reform to be based on results from a recently launched study, fall within this framework.

After a brief look at the current context of fisheries, and a summary of the sector's recent performances and its key problems, this document aims at setting out the different strategies and policies leading to sustainable development in an appropriate bio-economic, administrative and social environment. It then highlights the fishery tax system and national experience concerning fishing agreements.

1. Current fishery context

1.1 State of fishery resources

Senegal Exclusive Economic Zone (EEZ) is characterized by a great biodiversity. Exploited resources belong to four groups with rather marked bio-ecological and socio-economical differences.

The global exploitable potential has not recently been scientifically evaluated.[13] The most recent information from the “Centre de Recherches Océanographiques de Dakar Thiaroye” (CRODT) shows that:

High-sea pelagic resources, given the highly migratory nature of the main species and their vast distribution area (Atlantic), Senegalese EEZ potential is still difficult to evaluate. The latter was estimated between 25 000 and 30 000 tonnes ay the beginning of the 1990s.

In the last few years the fishing season length was reduced in Senegal and increased in Mauritania, this reflects the above-mentioned downward trend in catch potential.

Many of the main stocks of commercial species (yellowfin tuna, skipjack, bigeye tuna, swordfish, sailfish), are highly to fully exploited in the Atlantic. Small tuna and similar species (little tuna, atlantic bonito, king mackerel, etc.) that are mainly targetted by the artisanal fishery, would have a lower exploitation rate.

Coastal demersal resources, annual capture potential is estimated at 130 000 tonnes[14]. In general, stocks are fully to overexploited in some cases.

Preliminary evaluations, carried out within the sub-regional project SIAP framework (October 2001) confirm overexploitation diagnostics or even severe overexploitation of some stocks (grouper, sea bream, lesser African threadfin, blue spotted sea bream).

Data analysis of five stocks based on the 1981-1999 series, shows an even more alarming situation than before, captures having currently reduced, while fishing effort increased.

Deep demersal resources, the exploitable potential of all species together, is estimated at around 20 000 tonnes of which around 40 to 50% are made up of senegalese hake and 15 to 20% of deep-sea shrimp. These stocks (shrimp and hake) show no signs of over biological overexploitation. Most recent references[15] indicate that despite insufficient biological information and statistics, hake and deep-sea shrimp are not overexploited.

However a freeze on fishing effort was recommended as management measure of deep-sea shrimp stocks. As for hake, a precautionary principle should be observed, in the management of stocks shared with Mauritania.

Coastal pelagic resources, the global potential can be estimated at over 450 000 tonnes based on the average specific biomass in the last five years.

Coastal pelagic biomass in the Senegalese-Gambian zone was estimated at 1 450 000 tonnes in November-December 1999, more than 95% of which were sardinellas.

In general, in the northern part of CECAF region, R/V Fridtjof Nansen surveys show high density levels of sardinellas during the last few years. The most recent evaluations, carried out within a regional framework, show that sardinellas exploitation levels is probably moderate throughout their distribution area, except for Senegal Petite Côte.

As regards horse mackerel, an upward trend in biomass can be observed throughout the whole region, except in the Senegalese-Gambian zone where low levels of atlantic horse mackerel biomass were recorded between 1995 and 1999.

Table 1: State of large pelagic stock and international recommendations for 1993-1997-2000

|

Species |

1993 |

1997 |

2000 |

|

Yellowfin tuna Thunnus albacares (Eastern stock) |

E: In full exploitation or even slightly

over |

E: Effort and production at near optimum

levels |

E: Effort and production at near optimum

levels |

|

Bigeye tuna Thunnus obesus |

E: Stock under-exploited, F < Fmsy. |

E: A surge in catch, biomass in decline;

over-exploitation. |

E: A surge in catch, biomass in decline;

over-exploitation. Mortality higher than MSY level and decline in

stock |

|

Skipjack Katsuwonus pelamis (Eastern stock) |

E: No evaluation carried out since 1984. Record catches

in 1991. |

E: Overexploitation level attained |

E: No new evaluation in 2000 (Overexploitation level

attained in 1997). |

|

Swordfish Xiphias gladius |

E: Concern for stock, particularly in the

south |

E: Stock overexploited and in decline. Current catches

non-sustainable |

E: Stock overexploited and in decline. Current catches

non-sustainable |

Sources: [1] ICCAT/CICTA, 1993. Report on biennal period 1992-93 (Ist part, Annexe 14)

[2] ICCAT/CICTA, 1997. Report on biennal period 1996-97 (Ist part).

[3] ICCAT/CICTA, 2001. Report on biennal period 2000-01 (Ist part, Annexe 9).

Table 2: State of small pelagic and demersal stock and recommendations in 1993 and 1997

|

Species |

1993 |

1997 |

2000 |

|

Sardine |

E: |

E: Variable stock. [4] |

E: Risk of over-exploitation [8] |

|

Sardinella Sardinella (aurita & maderensis) |

E: Moderate rate of exploitation except in Petite

Côte. |

E: Abundant stock. [4] |

E: Exploitation probably moderate (from Morocco to

Senegal) except in the Petite Côte in Senegal [8] |

|

Horse mackerel Trachurus spp. |

E: Moderate rate of exploitation, increase in biomass

after a minimum in 1983. |

E: Variables stock. [7] |

E: Increase in biomass (except in Senegal) with a drop

in 98/99 for horse mackerel. [8] |

|

Senegalese hake Merluccius senegalensis (1) |

E: Insufficient data. [1] |

E: |

E: Non-exploited stock [8] |

|

Sole Cynoglossus spp. (1) |

E: Steady decline since the 1970s. [3] |

E: |

E: |

|

Coastal demersal fish (1) |

E: General decline since 1980, particularly breams,

groupers. [3] |

E: |

E: Global overexploitation and specific:

serranidés (grouper), sparidés (sea bream), lesser African

threadfin [10] |

|

Octopus Octopus vulgaris (1) |

E: Stock in expansion. [3] |

E: |

E: Highly variable stock [11] |

|

Cuttlefish Sepia officinalis (1) |

E: Stock in expansion. [3] |

E: |

E: Variable stock [9] |

|

Deep sea shrimp Parapenaeus longirostris (1) |

E: Insufficient biological data. |

E: Stock fully exploited. [4] |

E: Stock not overexploited [8] |

(1) Only the Senegalese EEZ is concerned with stock diagnostics and recommendations.

Sources of table 2:

[1] FAO, 1990. Rapport du groupe de travail sur les merlus et les crevettes d’eaux profondes dans la zone nord du COPACE. COPACE/PACE Séries 90/51.

[2] FAO, 1993. Groupe de travail ad hoc sur les sardinelles et autres espèces de petits pélagiques côtiers de la zone nord du COPACE. CRODT, 29 novembre-3 décembre 1993. COPACE/PACE Séries 91/58.

[3] Gascuel, D. et Thiam, M. 1993. Evaluation de l’abondance des ressources démersales sénégalaises: estimation par modélisation linéaire des PUE. In: L’évaluation des ressources exploitables par la pêche artisanale sénégalaise. Symposium de Dakar, février 1993. Barry-Gérard, M., T. Diouf et A. Fonteneau (eds.). ORSTOM, Colloques et Séminaires, p. 191-213

[4] FAO, 1998. Questions et tendances du développement des pêcheries dans la région et leur impact sur la sécurité alimentaire. 14e session du COPACE, Nouakchott (Mauritanie), 6-9 septembre 1998. CECAF/XIV/98/4.

[5] FAO, 1995. Rapport de la dixième session du groupe de travail sur l'évaluation des ressources. Accra, Ghana, 10-13 octobre 1994. FAO Fisheries Report FIPL/R511.

[6] FAO, 1993. Evaluation des stocks et des pêcheries mauritaniens. Voies de développement et d’aménagement. Rapport du 3e groupe de travail CNROP, Nouadhibou, Mauritanie, 20-26 novembre 1993. COPACE/PACE Séries 95/60.

[7] FAO, 1998. Questions et tendances du développement des pêcheries dans la région et leur impact sur la sécurité alimentaire. 14e session du COPACE, Nouakchott (Mauritanie), 6-9 septembre 1998. CECAF/XIV/98/4.

[8] FAO, 2000. Etat d’exploitation des stocks halieutiques et aménagement des pêcheries dans la zone COPACE. Première Session du COPACE, Abuja (Nigeria), 30-31 octobre 2000. CECAF/I/2000/Inf.4 F.

[9] CRODT, 2001. Situation des ressources halieutiques sénégalaises et possibilités de pêche. Rapport technique, mars 2001, 9 p. + 8 planches.

[10] Laurans, M.; Barry-Gérard, M. et Gascuel, D. 2001. Diagnostic de cinq stocks sénégalais par l’approche globale (Galeoïdes decadactylus, Pagellus bellottii, Pseudupeneus prayensis, Pagrus caeruleostictus, Epinephelus aeneus). In Document technique No. 2, Rapport de la réunion de Mindelo (Cap Vert), 10-12 octobre 2001.

[11] CRODT, 2000. Rapport du programme de recherches sur les céphalopodes benthiques (poulpes) et leur aménagement

1.2 Recent sector performance

1.2.1 Fishery contribution to the Gross National Product (GNP)

The fishery sector in Senegal is comprised of three different segments of activity: maritime fishery, continental fishery and aquaculture. Most of the activity is in maritime fishery.

Maritime fishery products play an important role in people's diet, providing 75% of animal protein.

During 1990-2000, the fishing sector represented on average 11% of GNP's primary sector. It was also in third position for sectorial GNP contributions after agriculture and farming. In comparison to the economy's total GNP, fishery contribution during this period was on average 2.5 to 2%.

The fishery sector has an even stronger incidence on external balance. During 1990-2000, it provided an average of 37% of exports in terms of value. Making it the largest exporting sector, before groundnut (12%) and oil products (11%).

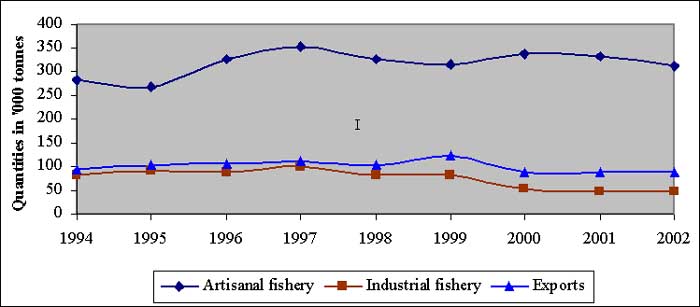

Growth in fishery activity has been spectacular since the middle of the1960s. Landings which totalled 50 000 tonnes in 1965, reached 358 300 tonnes in 2002 (see Figure next page).

Evolution in export and marine fishery landings in Senegal, 1994-2002

In 1999 export turnover from landings and fishery products is estimated at 278 billion FCFA.

The fishing sector's added value is estimated at 199 billion of which 60% from captures and 40% from processing.

From a beneficiary point of view, 25% passes to the State (5% of direct added value and 30% of indirect added value) while the “employees” benefit from 46% of the flow (39% of direct added value and 49% of indirect added value).

Table 3: Synthesis of the added value created by the Senegalese fishing industry (in million FCFA)

|

|

Direct A.V. |

Indirect A.V. |

Total A.V. |

Direct A.V. % |

Total/% A.V. Industry |

|

Industrial fishery |

7 887 |

16 233 |

24 120 |

33% |

12% |

|

Artisanal fishery |

31 958 |

20 690 |

52 648 |

61% |

26.5% |

|

Artisanal processing |

1 049 |

1 912 |

2 961 |

35% |

1.5% |

|

Fish trade - processing units |

6 154 |

85 361 |

91 515 |

7% |

46% |

|

Fish trade - domestic market |

1 396 |

4 481 |

5 877 |

24% |

3% |

|

Fish trade - local consumption |

1 186 |

938 |

2 124 |

56% |

1% |

|

Processing units |

764 |

7 030 |

7 794 |

10% |

4% |

|

Fishmongers |

82 |

876 |

944 |

9% |

0.5% |

|

Canning factories |

3 085 |

5 429 |

8 514 |

36% |

4% |

|

Fishmeal |

746 |

2 163 |

2 909 |

26% |

1.5% |

|

Total |

54 307 |

145 113 |

199 406 |

27% |

100 |

Source: APC evaluation report, 2001

In the fisheries sector as well as in processing and marketing, employment figures are estimated at a total,[16] of 600 000, mostly in artisanal fishery and artisanal processing. The sector's workforce represents 17% of the working population: one out of every six working Senegalese does so in the in the fishery sector.

1.2.2 Key sector problems

Despite the above-mentioned results, the Senegalese fishery sector is faced with overexploitation of coastal demersal resources, national fishery overcapacity and an increasing demand in fishery products.

Taking into account the current situation in fisheries, changing trends both domestic and foreign and policy organization, the different types of problems to resolve are:

(i) problems concerning sustainable management and the reconstruction of fishery resources (reduction of artisanal and industrial fishing effort, adapting industrial processing capacities, etc.);

(ii) the sector's poor governing capacity;

(iii) meeting population, industry and foreign market fishery product demand, without increasing pressure on resources;

(iv) problems concerning optimization of the use of fishery resources;

(v) poor organizational, analytical and decision-making capacities from the sector's operators;

(vi) lack of communication between the sector's operators;

(vii) lack of appropriate financing measures for the different activities.

1.3 Current policies and future reforms

In November 2000 national meetings on fisheries and fish farming were the starting point of the work towards current fishing and fish farming policies in Senegal.

The new sectorial strategy gives priority to the management of access resources, before reinforcing development options. Thus the fisheries institutional framework has been re-examined (decree No. 2000-833 of 16 October 2000) in order to take into consideration this major concern and a plan to review the juridical and statutory framework is in process.

1.3.1 Institutional and legal framework

i) Institutional framework of marine fisheries

The fisheries Minister is in charge of the fisheries department, the latter has extensive power (conferred) by decree. He has an office at his disposal as well as attached services and national director offices.

The Fisheries Ministry’s main institutions

Marine fisheries Department (Direction des pêches maritimes - DPM): The marine fisheries department deals with setting up Government-defined policies within the framework of fisheries resource management and exploitation. The main services which make up the DPM are, the industrial fishery division, the artisanal fishery division, the fishery products control bureau, as well as regional services within each of the seven Senegalese maritime regions.

Continental Fisheries and Aquaculture Department (Diretion de la pêche continentale et de l'aquaculture - DPCA): this is a recently created department. It deals with setting up policies concerning continental fisheries and aquaculture. Due to overexploitation of fishery resources, continental fisheries and aquaculture could be developed in order to contribute towards the diversification and improvement of annual fish, crustacean, mollusc and seaweed production.

Fishery Protection and Surveillance Department (Direction de la protection et de la surveillance des pêches - DPSP): was also recently created, following the decree No. 2000-833 of 16 October 2000. The DPSP's mission is to ensure the protection and surveillance of the EEZ so that fishing regulations are respected. There are three sections to the DPSP (administrative, operational and scientific), as well as coastal stations. It has a permanent staffing as well as contracted observers.

Planning and Study group (Cellule d'études et de planification - CEP): was also recently created and is the result of a merger between the economic research institute and the support group for sustainable fishery development. The CEP is responsible for carrying out prospective and strategic studies, planning coordination within the Department, monitoring and evaluation of projects and programmes, it also deals with the sector's information management.

Centre for Artisanal Fisheries Improvement and Experimentation (Centre de perfectionnement et d'expérimentation pour la pêche artisanale CPEP, ex-CAEP) has been modified in order to adapt his assignments to the new sector's strategic orientations. The CPEP deals with artisanal fishermen training, as well as experimenting and diffusion of artisanal fishery techniques and technology.

National Marine Fishery Training Centre (Centre national de formation des techniciens des pêches maritimes - CNFTPM): deals with training marine fishery technicians. Set up by decree No. 91-1349 of December 1991, the centre has taken over the oceanographical and fishery technicians’ school. It has opened up to other levels of training. The majority of the Ministry civil servants up to category B, have come from this centre.

Other institutions or dialogue groups

Centre for Oceanographical Research: deals with resource and exploitation systems follow-up. It also aids the Fisheries Ministry in scientific assessment and in taking fishery decisions and drawing up policies. The Centre de recherches océanographiques de Dakar Thiaroye - CRODT) is attached to the Ministry of Agriculture. Its financing however is provided by the Fisheries Ministry. Its 2001 budget came to 458 million FCFA, 200 million FCFA of which were provided by the Fisheries Ministry.

Co-management structures: these structures were established by the 1998 Fishing Code. The Conseil national consultatif des pêches maritimes (CNCPM) and local artisanal fishery councils will, in theory, have major fishery management responsibility.

Advisory Commission for fishing licence issuing: it plays a major role in fishery management concerning fishery regulation measures; it examines fishing licence applications and advises the Minister who is the final decision-maker. Professionals are calling for it to be changed to a debating commission.

Professional organizations: have developed and have been increasingly implicated in fishery management in these last few years. The most prominent organizations in the industrial sector are the Groupement des armateurs et industriels de la pêche maritime au Sénégal (GAIPES) and l'Union des pêcheurs et mareyeurs exportateurs du Sénégal (UPAMES). In the artisanal sector they are, la Fédération nationale des groupements d'intérêt économique de pêcheurs (FENAGIE-PÊCHE), la Fédération nationale des groupements d'intérêt économique de mareyeurs du Sénégal (FENAMS), le Collectif national des pêcheurs artisanaux du Sénégal (CNPS), l’Union nationale des GIE de mareyeurs du Sénégal (UNAGIEMS). Such structures often benefit from foreign financial support.

ii) Marine fisheries juridical and statutory framework

A revision in Senegalese marine fishing rights took place in 1998. The basic legislative and juridical framework which governs living marine resources exploitation in the Senegalese EEZ has not evolved with changes or restrictions which have arisen progressively.

The resulting Marine Fishing Code encompasses resource conservation and management fishery measures, which include the following major innovations:

- institutional management mechanisms (introduction of annual and long-term fishery management plans, setting up of a Conseil national consultatif des pêches maritimes and local fishery councils, an advisory commission for fishing licence issuing, etc.);

- indirect control of fishing effort mechanisms;

- coastal zone management measures and a Code of Conduct for responsible fisheries.

However certain aspects of this law need to be improved. The decision-makers in marine fishery management need to have a certain flexibility, as biological, socio-economic, political and technical conditions that influence fishery activities often evolve rapidly.

The 1998 fishing law took this into account, but the current evolution of the sector and constant changes, call for it to be reviewed.

1.3.2 Sustainable development policies and strategies

During the last three years, the Fisheries Ministry has prepared a sector development strategy. This document[17] puts forward a detailed analysis of the sector's problems and defines six objectives:

to ensure sustainable management of marine and continental fisheries, as well as aquaculture while maintaining economic viability;

to satisfy local fish demand;

to modernize artisanal fishery;

to increase added value of fishery products;

to develop an efficient public financing system of private fishery and aquaculture activities;

to strengthen regional and international bilateral cooperation in fisheries.

In order to reach these objectives, the actors concerned identified a global strategy highlighting the following directions:

(i) At resources management level, priority is given to regulation concerning EEZ resource access and to the setting up of artisanal and industrial fishery management plans;

(ii) As for regulations, modern resource management concepts have been introduced: fishery management plans, and dialogue groups between administration and fishery professionals, as well as between-state fishery cooperation.

The law comprises strict measures which could help control expansion of fishing capacity, and stringent conditions for foreign vessels participating in fishing agreements, concerning the exploitation of certain stocks.

It lays down a set of principles leading to more stringent regulation concerning artisanal fishery. Monitoring, control and surveillance of fishing operations are clearly specified and developed, to preserve operators' rights.

It plays an important role in the management of marine ecosystem and marine culture. It redefines conditions, more strictly, of vessels chartering under foreign flags.

However the law is not fully applied and certain aspects need improving in order to adapt to the sector's evolution

(iii) The setting up of an institutional and economic environment which is more adapted to the sector's development needs; in this respect the strategy insists on having an administrative reorganization and a fisheries tax system which would conform to the sectorial policy's new position.

(iv) Fishing agreement cooperation between Senegal and other countries of the region, in order to provide supplementary catch for artisanal and industrial fishery.

1.3.3 The main future reforms

The aim of these reforms is to improve the sector's contribution to the national economy (to generate wealth and employment) and to fight poverty.

Future reforms favour above all, the management of access to resources, before reinforcing development options. The following actions will be given priority:

1° - Opting for a new fishery resources management system

Within this framework, provisional results from the national workgroup to define a fishing rights attribution system in Senegal waters have led to set down the following guidelines:

(i) For industrial fishery, a unique system based on quotas may be adopted, together with delimitation of exclusion zones, so as to protect specific zones for artisanal fishery, reproduction zones and eventually marine parks;

(ii) Artisanal fishery targeting cephalopods and demersal species could initially be controlled through a licensing system which, in future could be associated with an artisanal fishery quota system (according to category in specific zones);

2° - Setting up of a management plan for the industrial fishing fleet

Firstly, the industrial fishing fleet must be reviewed in order to check that conditions granting trawling under the Senegalese flag are respected and evaluate the contribution of fishing companies to the GNP. Once this work is carried out, a master management plan can then be set up.

Within this framework, the fishing fleet audit will enable decisions to be taken, to reduce industrial fishing capacity to match the production capacity of the resource.

3° - Adapting processing capacity to potential of capture

The restructuring of the fishery processing industry, aims to adapt its capacities so that future fish landings may be processed under optimum conditions.

The prerequisite of adapting investment to capture potential, in waters within national jurisdiction, is to set up a master plan for the fishing fleet (see above).

4° - Reducing pressure and on artisanal fishery capacity

Senegalese fishery management will have little hope of succeeding without control or even a freeze in artisanal fishery capacity. Therefore, thought needs to be given to cooperation programmes with United Nations institutions (World Bank and FAO) in order to identify the most effective solutions to reduce and control canoe fishing capacity as well as appropriate support measures.

5° - Institutional adjusting and elimination of governance constraints

Structures and means must be adapted and reorganized in order to strengthen sectorial institutions analytical and decision-making capacities.

Past efforts used in order to tackle the sector in crisis, had largely failed due to socio-political realities (lack of transparency and efficiency, political interference and actions governed by profitability, etc.).

A revival of the sector demands: (i) transparent and clear regulations, (ii) an improvement in regulations and institutions, (iii) changes in behaviour within politics.

In order to do this, a special independent commission will be set up in relation with the Ministry of Economy and Finance and the Fisheries Ministry, which will launch and run a programme for the redeployment of marine fisheries and aquaculture promotion.

6° - Setting up a fisheries restructuring fund

The restructuring of the Senegalese fishing sector will require considerable financial resources. The application of the above-mentioned policies and strategies will result in job losses, a ban on gear and fishing techniques, a redeployment of those concerned, a taxation of non-profit making segments, and tax facilities granted to industries generating sectorial wealth.

The cost of the sector's restructuring will be financed by the State and its development partners within the framework of a restructuring fund. This fund would finance:

- Costs involving the promoting and use of selective fishing techniques;

- Ship owners' reconversion costs, in relation to a reduction in trawl fishing capacity;

- Artisanal fishing reconversion costs in relation to a reduction in artisanal fishing capacity;

- Costs in relation to cuts in vessel operations and land-based industries;

- Subsidy granting to profit making segments.

7° - Information and operators' awareness

In the different fishing practices and policies, communication has always taken a back seat. The success of the fishing sector's restructuring will depend on the results of the communication strategy and policies implemented.

In the past, rehabilitation and rational management policies have been damaged by pressure from industrial and artisanal fishery operators, wanting to maintain a status quo and the threat of social and political measures limiting or even restricting expansion of fishing effort.

The aim here is to set up information and awareness programmes for organizations in the process of restructuring their fishing fleet, processing or canning industry.

The objective is to instil a management culture and the notion of responsible fishery into those concerned via training and awareness programmes.

2. Fisheries tax system reforms and fishery agreements - examples

2.1 The tax system in fisheries

2.1.1 Current tax systems in fisheries

The fishery sector dynamism as well as its economic and social results are due to the States' financial support.

The State has contributed a great deal to the development of the fishery sector via direct or indirect aid to the industrial and artisanal sector. The Senegalese State policy backing capture activity and processing, was mostly based on tax facilitating measures and subsidies.

As far as artisanal fishery is concerned, provision of tax free inputs such as tax free fuel, engines, fishing gear and various imported material is granted. Such aid contributes significantly to the profitability of artisanal fishery.

As for industrial fishery, State intervention concerns tax free fishery input as well as tax facilities granted to export companies through various systems such as: Industrial Free Zone (Zone franche industrielle - ZFI), in Free Points ('Points francs - PF) or within the framework of Free Exporting Enterprise (Entreprise franche à l’exportation - EFE).

Fishing companies benefit from exemption on: VAT, customs rights on local buying, added value, customs administration tax (Timbre douanier), registering tax, Patent and financial contribution.

Table 4: Comparison of tax systems applicable to fishing sector companies

|

System |

Zone franche industrielle de Dakar ZFID |

Points francs |

EFE |

|

Property arrangement system |

Locataire de la ZFID |

Free |

Free |

|

Administrative system |

Administration Spéciale |

Droit commun |

Droit commun avec déclaration préalable |

|

ZFID Tax |

Yes |

Yes |

No |

|

Compulsory amount to be exported |

60% |

60 % |

80 % |

|

Customs system |

Total exemption |

Total exemption |

Total exemption |

|

Customes proceedures |

In ZFID, without guarantee or escort |

Droit commun with escort |

Guarantee and escort exemption |

|

Tax exemption |

Total |

Total |

Total except corporate tax 15% and tax on distributed dividends |

|

Employment subsidies |

Yes but controversial |

Yes in certain cases but controversial |

No |

Source: MP/CEP

The fishery companies are only obliged to declare imports and exports, local buying, local sales and the declaration of accountancy statistics.

Which means that State resources from taxes are not significant (see table above). Fishing companies benefit from a considerable financial income.

An evaluation of the fishery sector's contribution to the State budget will determine precisely the resources generated by fishing activity.

2.1.2 Future fiscal reforms

In general terms, fiscal policy simplification will be implemented in the next three years in order to increase yield. Before the end of June 2003, the government will set up a study to evaluate the effect of a reduction in the marginal taxation rate of direct taxes. Concurrently, action towards a widening of the taxation base will continue, via progressive taxation of unstructured sectors.

As for investment code reforms, the government policy will make sure that they are rational, indiscriminate and that they will preserve public finance viability. The government will also consult the International Monetary Fund concerning the main elements of the fiscal reform, in the first Programme review at the latest.

More particularly, with the fishery sector faced with overfishing and overcapacity, the question of maintaining the tax aid system as we know it, is brought to light. The current tax aid system could be seen as an indirect incentive to overcapacity and overfishing.

Hence the study on the future fishery tax system. As a result of this study, a new tax system will be envisaged for certain non-profit making segments of the sector, which benefit from specific economic regimes

2.2 Senegalese experience regarding fishing agreements

Marine fishery is the most directly concerned by agreements with the European Union. The two vital components of which are artisanal and industrial fishery.

The European Community fishing agreement (Accord de pêche communautaire - APC) as signed by Senegal, specifies the level, conditions of attribution and of use of access rights to Senegalese EEZ fishery resources for European vessels.

2.2.1 National fishery policies and their compatibility with fishing agreements

The first generation of agreements signed with northern countries (bilateral agreements signed with France in September 1974, Italy in January 1975 and Spain in May 1975) were very unbalanced.

These countries granted Senegal loans in exchange for fishing access for an unspecified number of their vessels.

Furthermore, these agreements were ill-defined as to the conditions of the fishery exercise, as well as being long term (4 to 6 years).

During an inter-departmental committee on 21 May 1979, concerning marine fisheries, the Senegalese government laid down new guidelines for fishing agreement negotiations:

nationals are to be given priority to resource exploitation and processing;

the number of foreign vessels to be limited, taking exploitable potential into account;

access fees to be charged in order to obtain fishing licences;

financial compensation to be demanded so as to support national fishery development;

some or all catch to be landed in Senegal in order to supply land-based processing units.

These criteria have since been used as a negotiation base for the application of the different agreements, leading to the following principles:

Senegal is to agree to grant fishing rights to European Community vessels, without reciprocity;

in exchange for these fishing rights, the European Community is to pay the Republic of Senegal a financial compensation, as well as licence fees directly paid by the ship owners.

At the beginning of the 1990s, the agreement completely changed the negotiation's environment, i.e. the terms and beneficiaries of the fishing agreement may influence long-term strategic choices and short-term tactic decisions. They concern:

fishery resources and exploitation in space and time; particularly recent management trends;

sociology, i.e. the relation between local fishing communities reacting to industrial fishery vessel competition;

methods of application of the agreements with the European Union.

Resulting guidelines from national fishery talks (November 2000) state that the negotiation strategy should take into account:

current national fishing capacity;

country's needs of financial resources;

the urgent need of a mutually advantageous agreement based on both parties' aims, for sustainable development in fisheries (conditions, appropriate techniques);

the need to reduce fishing pressure.

The last Senegal/European Union fishery agreement integrated artisanal fishery development with scientific research, fishery surveillance and institutional support.

However, despite well defined actions, the agreements always follow a commercial logic (fishing rights in exchange for financial compensation) and lie in a generally unfavourable fishing context, which is unsustainable and irresponsible.

«Senegalese resource access control is still today a major, unresolved problem concerning fishery management and the development of a national sector».

The fishing agreements themselves should not pose insurmountable problems, beyond geo-strategic stakes outside the fishery sector. They should be seen more as an indication of the management system's weakness and due to this weakness are an aggravating factor in a badly controlled and inefficient system with regard to conservation objectives.[18]

These last two points bring us back to the vital question of the current Senegalese fishery context: fishery resource access (a national heritage) for whom, under which conditions and who is to benefit from the profits?

The Senegal/European Union fishing agreement is currently faced with different problems, the main one is that it is part of commercial arrangements that were favourable to product export, thus inducing pressure on food security and exported ressources.

The fishery environment was not sufficiently taken into account, putting the agreement in an awkward situation facing international regulations which were more restrictive than previously.

Increasing European fleet pressure on resources had an undeniable effect on stock decrease. The question of its reconduction is currently being debated.

The fishery agreement's complementary nature was theoretically the main reason it was concluded. The existing gulf between theory and practice has not stopped widening since.

In the 1980s, the fishing agreement coincided with the development of the of artisanal fishery. From there on, landings of the latter experienced a spectacular increase, from around 150 000 tonnes at the beginning of the 1980s to 250 000 tonnes from 1990 onwards and 358 300 tonnes today.

As for coastal, pelagic and demersal resources, the national fleet seems, not only able to exploit stock almost entirely, but to exploit them fully. If however, pelagic resources are not fully exploited by artisanal fishery, it is more to do with an increase in capital cost, or the growing attraction of export species for the exploitation, than to productivity or capacity problems. According to available scientific data, complementarity would in principle, only concern high-sea resources.

Even if complementarity between national and foreign fisheries exists, both fleets are competing on the same fishing zones. There is generally a double competition: national and foreign industrial fisheries are in opposition, particularly concerning coastal demersal crustaceans and cephalopods, as well as artisanal fishery and industrial fishery (local and foreign).

Conflict between these two types of fisheries has worsened since artisanal fishery development has been put in a situation where it now competes much more in the high sea with industrial fleets. Such overlapping not only result in stock depletion, particularly coastal demersal, but in fishing gear destruction and collisions often costing human lives.

The Senegalese fishery overcapacity, particularly towards demersals, has resulted in resource overexploitation. With artisanal fishery added effort on export species, comes a sharp decline in average size of individuals captured and in national fishery yield, despite a high fishing effort. Hence less fishery products are available in the local market.

The problem could have worsened if the pelagic fishing quotas, granted in the 1997-2001 agreement with the European Union, had been used. More than 80% of artisanal fishery captures are pelagics mostly intended for national consumption. Considering their role in food security, pelagics are extremely sensitive resources.

In general, fishing agreements are aggravating factors to fishery resources, which are already fully exploited by industrial and artisanal national fleets, except for high-sea resources.

Fishing agreements also participate in the gradual opening up of the Senegalese fishing sector, not only directly, by subtracting a certain quantity of the resource from national fishermen, consumers and processors (although the latter have contingents which they must land), but indirectly, by setting up cooperative strategies between national and foreign fisheries, diverting part of the national effort which would satisfy domestic demand.

2.2.2 Impact of the fishery agreement with the European Union

This analysis on the effects of European fleets in Senegal is taken from the evaluation report on the Senegal-European Union agreement 1997-2001.

2.2.2.1 Area competition in fishing zones

There is competition between national and European Union fleets, but also with other foreign fleets targeting the same resources. Competition concerns mostly coastal species exploited on the continental shelf and on the slope.

Such competition can be seen through conflict concerning resource access and between different techniques, resulting in gear destruction or even collisions with artisanal fishery units. These are often badly indicated, and shifting outside their exclusive 6 or 7 mile zone, due to coastal stocks exhaustion.

2.2.2.2 Economic impact from European vessel activity

During this period, average annual European fleet landings in Senegal were of 349 tonnes of demersals used in processing units and 17 042 tonnes of tuna used in canning factories. They generate direct and indirect added value, totalling respectively, 5 579 and 4 881 million FCFA.

Senegalese workers aboard European vessels are fishermen but also observers (80 people). Fishing jobs greatly exceed quotas fixed by the draft agreement due to the good reputation of Senegalese fishermen.

Total expenses for personnel (Fishermen's salaries and State expenditure) concerning European boat activity is on average between 254 and 364 million FCFA annually for an equivalent number of jobs respectively between 240 and 370.

Added value generated by the employment of observers is estimated at 288 million FCFA. Other flows generated by European fleets were valued using data supplied by chartering agents (See Table 5).

Table 5: Incidence of European vessel activity in the fishery sector

|

Expenses |

Total in % |

Expenses |

Total in % |

|

Fishermen's salaries |

47 % |

Provisions and supplies |

5 % |

|

Harbour charges |

5 % |

Maintenance and repairs |

17 % |

|

Handling charges |

4 % |

Consignment charges |

7 % |

|

Security |

0,1 % |

Other charges refacturées |

14 % |

|

|

|

Total |

100% |

Source: OEPS survey using sample of chartering companies

Boat activity incidence on the sector amounts to 10 billion FCFA and show a relative balance between direct added value (53%) and indirect (see Tables 6 and 9)

Table 6: Total annual added value concerning European Union vessel activity (in million FCFA)

|

|

Total added value |

Of which direct AV |

Salaries |

State |

%/total |

|

Landing incidence |

5 086.55 |

1 832 |

1 938.15 |

1 912.32 |

48.6 |

|

Senegalese fishermen employment |

309 |

309 |

266 |

44 |

3.0 |

|

Observer employment |

288 |

288 |

257 |

31 |

2.8 |

|

Stopover incidence |

4 776 |

3151 |

3 335 |

692 |

45.6 |

|

Total |

10 459.55 |

5 580 |

5 796.15 |

2 679.32 |

100 |

2.2.2.3 Impact of fishery agreement on non-market sector

Compensation revenue amounts to 32 billion FCFA, on average 8 billion FCFA per year, 50% of which goes towards strengthening the fishery industry. Trawler licence taxes paid by ship owners should be added: 689 million FCFA and tuna tax: 5.5 million FCFA.

Table 7: Comparison of average annual public budget during the European Fishing Agreement (APC) period (in million FCFA)

|

National budget |

Aid and cooperation |

Fishing agreement |

|||

|

Functioning |

309 |

Japan |

2 423 |

Compensation |

8 000 |

|

B.C.I. |

3 053 |

France |

1 726 |

Trawler taxes |

689 |

|

CEPIA |

634 |

EU |

491 |

Tuna trawler taxes |

5.5 |

|

Total |

3 997 |

Total |

4 640 |

Total |

8 694.5 |

In total the non-market sector gained an annual sum of 8 694.5 million FCFA, which can be compared to public sectorial budgets (see Tables 7 and 9) from which the distribution in the sector can be estimated (see Tables 8 and 9).

Table 8: Public expenditure financed by fishing agreements (in million FCFA)

|

Type of activity |

1998 |

1999 |

2000 |

2001 |

Annual average |

%/total |

|

Aval |

2 518 |

1 250 |

1 380 |

1 804 |

1 738 |

45 % |

|

Research |

250 |

250 |

250 |

200 |

237 |

6 % |

|

Training/accessibility |

985 |

1 100 |

20 |

10 |

529 |

14 % |

|

Institutional support |

246 |

1 150 |

2 000 |

1 103 |

1 125 |

30 % |

|

Financing |

|

250 |

250 |

250 |

188 |

5 % |

|

TOTAL |

4 000 |

4 000 |

3 900 |

3 367 |

3 817 |

100 % |

Source: MP/CEP

The global incidence on market and non-market sectors of the fishing agreements is estimated at 19.2 billion FCFA, representing 9.6% of national added value.

Table 9: Overall synthesis of fishing agreement incidences on commercial and non-commercial (in billion FCFA)

|

(in billion FCFA) |

Average annual flow |

|

Overall incidence on commercial sector |

10.5 |

|

Overall incidence on non-commerciqlal sector |

8.7 |

|

Total incidence of the Fishing Agreement (APC) |

19.2 |

|

Over Overall added value on national fishery sector |

199 |

|

Ratio of APC incidence/national added value |

9.6% |

2.2.2.4 Competition in foreign markets

There is competition from European products in export markets targeted by Senegal, as is the case of Japan for octopus, and the European market (French, Italian, and Greek) for demersal and pelagic species.

General conclusion

The main factors which have led to the Senegalese fishing crisis are: artisanal and industrial overcapacity fishery, targeting overexploited resources, inactive production capacity and low yield, as well as a decrease in productivity.

Nowadays artisanal fishery is no longer able to decently sustain its operators.

The only way out of this situation is to break with old attitudes and behaviour, in order to put sustainable development into action. There is undeniably a socio-political price to pay, which if ignored, will result in a dead end situation for the fishery sector, which in ten years time could lead to the sector's total collapse.

|

[13] Despite this, the master

plan relies on estimation which define Senegalese EEZ exploitable potential in

the range of 450 000 tonnes, close to current level of production. [14] This evaluation corresponds to the maximum sustainable yield obtained by fitting a global production model to capture series (corrected for freezing vessels discards) and standardized effort of a 150 GRT ice trawler. [15] It is worth noting that despite fluctuations in biomass observed in Senegalese waters in 1995-1999, artisanal and industrial captures have remained stable at around 350 000 tonnes despite a sharp fall (-38%) in artisanal fishing from 1996 to 1999. A marked rise in exploited stock density (especially sardinellas) on the coastal fringe - not covered by scientific evaluation - may explain the high level of catches observed. Industrial catches were on average 40 000 tonnes during this period, with a steep rise in 1999 (+54%) due to an increase in global biomass in 1999 and in industrial effort (the number of Russian vessels went from 8 to 11 in 1999).] [16] Sectorial study, reference year 1996, op. cit. [17] - Diagnostic, stratégie et plan d’action de développement durable de la pêche et de l’aquaculture; Note de synthèse, août 2001. - Pêche maritime et continentale, aquaculture; analyse descriptive et diagnostic, Tome I. - Stratégie de développement durable de la pêche et de l’aquaculture, Tome II. - Plan d’action à moyen terme de développement durable de la pêche et de l’aquaculture, 2001-2007, Tome III. [18] MGP-IDRA: Report on the evaluation study of the Senegal-European Community draft agreement |

![]()

![]()

![]()