![]()

![]()

![]()

by

Itamar de Paiva Rocha

ABCC - Brazilian Shrimp Farmers Association

Recife, PE, Brazil

[email protected].

1. Introduction

The Brazilian fishing industry, if one considers the country's potential for ocean and freshwater catch and aquaculture production, at the present time displays development perspectives that vary significantly between its two main components: ocean and freshwater catch show signs of stagnation while aquaculture is vigorously expanding. At the same time, within each of these components there are specific productive segments with considerable variations in performance, which, in general terms, makes it difficult to establish a clear global vision of the real mid and long term perspectives of the national fishing industry as a whole.

With a coastline of 8.5 thousand kilometers, which encompasses an Exclusive Economic Zone (EEZ) of 4.3 million km2, with 12 percent of the earth's freshwater reserves and more than 2 million hectares of flooded land, and with very favorable climatic conditions, Brazil has yet to reach its great potential for seafood production, specially where marine and freshwater aquaculture and ocean catch are concerned. The value generated by the Brazilian fishing sector at its primary level represents only 0.4 percent of the national GNP.

The evolution of the components that make up the fishing industry in Brazil is shown in the numbers listed below:

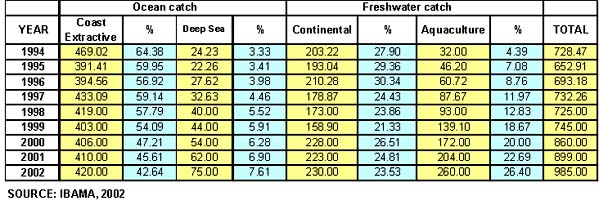

The supply of seafood from catch and aquaculture production increased just 35.2 percent in the 1994-2002 period which definitely has not contributed to improve the per capita comsumption in Brazil, which is very low (Table 1).

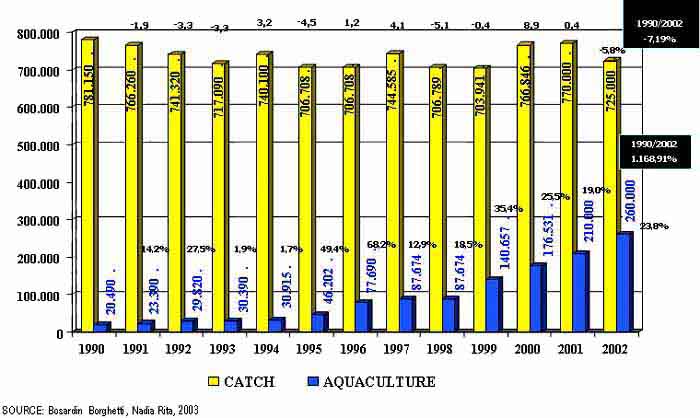

In global terms, the supply derived from catch (ocean and freshwater) showed a 7.2 percent decline in the 1990-2002 period (Graph 1).

The volume of production from Brazilian deep sea catch, with a share of only 7.6 percent of total seafood production in 2002 increased 209.53 percent in the 1994-2002 period (Table1).

Aquaculture, on the other hand, shows an extraordinary growth of 712.5 percent in the 1994-2002 period, increasing its participation in total seafood production in Brazil from 4.39 percent in 1994 to 26.4 percent in 2002 (Table 1).

2. Brazilian seafood exports

Brazilian seafood exports in 2001 represented only 0.33 percent of global exports (US$56.3 billion) that year. Marine shrimp, lobster and tuna are the main products exported by Brazil. National export data is presented below:

Total exported volume related to total seafood production increased from 3.3 percent in 1998 to 9.0 percent in 2002 (Table 2, Graph 1).

Tuna exports decreased 6.5 percent in volume and increased 28.3 percent in value in the 1998-2002 period (Tables 2 and 3).

Lobster exports increased 52.31 percent in volume and 70.21 percent in value in the 1998-2002 period (Tables 2 and 3).

Shrimp is now the main source of seafood export earnings in Brazil, with a 44.63 percent share of the total value exported by Brazil in 2002 and a 75.80 percent share for the Jan/Oct 2003 period (Table 3).

There is some controversy between ocean catch specialists in Brazil about the real mid and long term growth perspectives for this sector of the fishing industry. It is argued that over 80 percent of the fishing stocks along the coastline are either being fully explored, are being explored above the sustainability level, or are in a depletion phase.

During the 1990s, consecutive deficits were registered by the fishing sector's trade balance, reaching a low figure of US$353 million in 1998. This situation, however, was reverted in 2001 with a small superavit of US$22.6 million. This superavit has been increasing since then due basically to shrimp exports, which are mainly composed of farmed shrimp as will be shown later. In 2002 the superavit was US$129 million and in the Jan/Oct period in 2003 the sector's superavit had already reached the value of US$190 million.

3. Aquaculture

The main restrictions that limit ocean catch in Brazil, outside natural stocks limitations, are related to the lack of modern boats that are adequate for the needs of the country, to licensing restrictions for leased boats, to the deficiencies in the support infrastructure for the sector, and to the lack of support and incentive policies for the fishing sector.

On the other hand, there is a national consensus that Brazil offers ample and varied alternatives for the vigorous development of its marine and freshwater aquaculture potential. At the present time, farmed marine shrimp represents the main segment of Brazilian aquaculture in commercial terms with a 2002 production of 60 128 tonnes directed mainly to the export market. Tilapia production comes next with a production of 45 000 tonnes destined basically for the national market, followed by oyster and mussel production in the state of Santa Catarina with an annual production of 1.1 million dozens of oyster and 11 000 tonnes of mussels which are consumed domestically.

The challenges faced by tilapia for expanding production in Brazil are related to production costs that need to be lowered so that it can have a stronger presence both in the national and international markets. In the case of the Northeast region of the country, the greatest limitation is related to the difficulties that exist for environmental licensing in public waters.

The current efforts for expanding oyster and mussel production in Santa Catarina, an activity with considerable potential, are concentrated in techniques for capturing mussel seeds in the natural environment and in quality management and certification for oysters. There is also some promising preliminary work being done for the commercial production of scallops.

4. Farmed shrimp

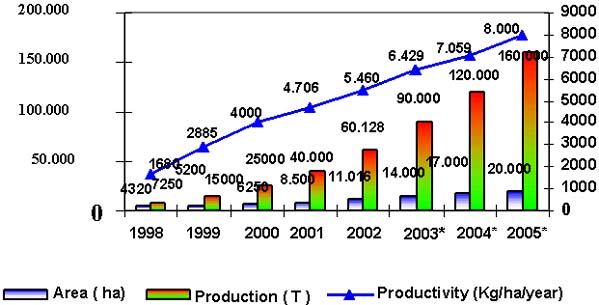

The performance of farmed marine shrimp in the 1998-2002 period reveals extraordinary growth figures. Average national productivity increased from 1 680 kg/ha in 1998 to 5 548 kg/ha in 2002, placing Brazil in first place amongst all producing countries in this technological efficiency indicator. Graph 2 shows not only the figures for 1998-2002 but also projections up to 2005 when Brazil is expected to reach a productivity of 8 000 kg/ha/year. The Brazilian model is characterized by the use of a semi-intensive production system with limited use of natural resources such as water and soil, and technology geared towards productivity and environmental sustainability.

There are two important characteristics linked to the growth of marine shrimp farming in Brazil: the strong participation of small producers in this activity representing 75 percent of all shrimp farmers and the generation of 3.75 direct and indirect jobs per hectare under production according to a study conducted by the Economics Department of the Federal University of Pernambuco. This job generating figure places shrimp farming as the most important activity in the agrobusiness sector of the region, overtaking irrigated grape growing (2.14 jobs/ha) which up to then was the most dynamic job generating segment of the Northeast region of Brazil.

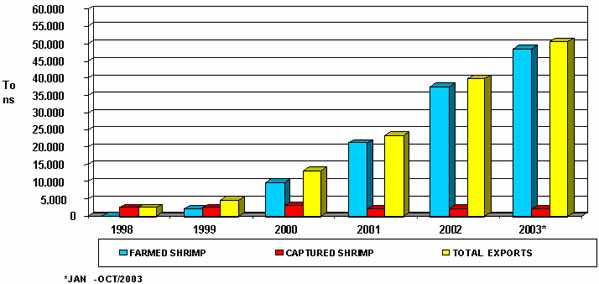

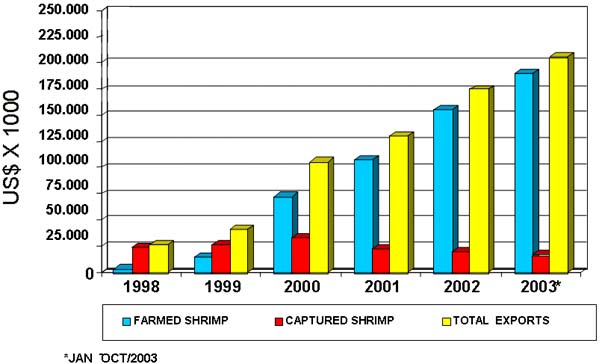

Graphs 3 and 4, which show annual export volume and earnings for shrimp, highlight the participation of farmed shrimp, increasing from 400 tonnes and US$2.8 million in 1998 when first exported to 37 800 tonnes and US$155 million in 2002. In the Jan/Oct 2003 period, exports of farmed shrimp have surpassed the figure of US$190 million from a total of US$205 million of shrimp exports.

The foreign exchange earnings obtained by farmed shrimp exports in 2002 put the product in second place in the list of primary sector exports of the Northeast Region of the country right after the traditional sugar cane sector and ahead of dynamic sectors such as the irrigated fruit growing sector of the region.

Projections for the farmed shrimp sector in 2003 show expressive numbers in terms of exports, 62 000 tonnes and US$220 million. For 2005, the projected numbers for total production and export earnings are, respectively, 160 000 tonnes and US$500 million.

The main restrictions for the development of marine shrimp farming in Brazil are basically:

Export of the product as raw material with increasing market restrictions for this type of product form.

Lack of scientific and technological investments in the areas of nutrition and disease prevention.

Lack of financial resources for investments and production financing.

Restrictions and deficiencies of public licensing mechanisms.

Antidumping threat.

As far as future mid term perspectives for shrimp farming is concerned, the following elements are in evidence through actions and projects:

Availability of credit lines for investments and production financing.

Quality Seal for Brazilian farmed shrimp.

Value added farmed shrimp product elaboration.

Emphasis on environmental sustainabiltiy and social responsibility programs.

Table 1 - Evolution of brazilian aquaculture and catch by categories - 1000 tonnes

Table 2 - Brazilian seafood exports from 1998 to 2003 in tonnes

Table 3 - Value of Brazilian seafood exports from 1998 to 2003 in US$ mllions

Graph 1 -Evolution of Brazilian aquaculture and catch production 1990-2002

Graph 2 - Evolution and projection of Brazilian farmed shrimp production

Graph 3 - Profile of Brazilian exports of farmed and captured shrimp from 1998 to 2003 in tonnes

Graph 4 - Profile of Brazilian exports of farmed and captured shrimp from 1998 to 2003 in US$ millions

![]()

![]()

![]()