![]()

![]()

![]()

by

Carl-Christian

Schmidt[5]

Head of the Organisation for

Economic Co-operation and Development's (OECD) Fisheries Division

Paris,

France

|

Abstract Globalization is the growing interdependence between markets and in fisheries this happens principally through three channels i.e. trade in fish and fish products, foreign direct investments in harvesting and processing (localization) and through fisheries services, that include both harvesting, processing and fisheries management services. This paper provides an overview of the trade and market situation in fisheries as it has developed over the past decades. Based on the experience with fisheries market liberalization, gained through recent work of the Organisation for Economic Co-operation and Development's (OECD) Committee for Fisheries, the paper then proceeds to discus the potential opportunities and challenges that may be expected for developed countries in the process of globalization. |

1. Background

Globalization is not new to fisheries. In fact, the process of globalizations i.e. the increasing interdependence of markets and fisheries has been occurring for decades if not centuries. Just take cod fisheries that already from the mastering of drying by the Vikings made it possible to fish the Northern hemisphere for a market in other parts of Europe.

Later, from the fifteenth century onwards, the development of salting techniques made it possible for Basque and Portuguese fishers to explore the rich banks off the Newfoundland area to satisfy a domestic market craving for salted cod, or "bachalao".[6]

Fishing also has some unique characteristics that underpins an important interdependence among fish markets; fishing vessels (capital) are mobile and can fish all over the world; fish have for many years been able to enter a global market due to advances in processing technology most notably salting, canning and freezing. And many of the fisheries resources do not respect national boundaries and can be caught by fleets of more than one nationality.

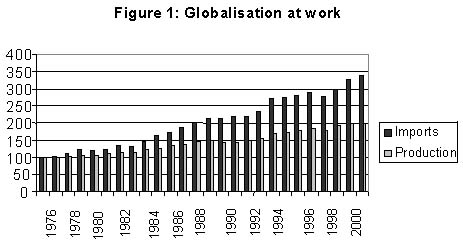

One way of capturing the globalization process has been captured in Table 1 giving an index of respectively world production and world imports (both based on quantities). What is evident form the graphic representation is that trade has increased more rapidly than production thus suggesting that markets have become more intertwined.

What makes fisheries an interesting case in terms of globalization is that several events have helped enhance and support the interdependence of markets and resources.

The common extension of EEZs to 200 miles as from 1977 led to an important redistribution of fishing possibilities but without, at least immediately, to a change on the demand side. Hence, as a consequence two important changes took place i.e. an increase in trade in fish and fish products and an increase in trade in fishing (access) rights.[7]

|

Box 1: Excerpts from the World Summit on Sustainable Development (WSSD) political declaration 11. We recognize that poverty eradication, changing consumption and production patterns and protecting and managing the natural resource base for economic and social development are overarching objectives of and essential requirements for sustainable development. 14. Globalization has added a new dimension to these challenges. The rapid integration of markets, mobility of capital and significant increases in investment flows around the world have opened new challenges and opportunities for the pursuit of sustainable development. But the benefits and costs of globalization are unevenly distributed, with developing countries facing special difficulties in meeting this challenge. |

Furthermore, the extension of the EEZs led to a development of fisheries in developing countries that hitherto had not shown major interests in an "industrialization" of the fishing industry. Besides, artisanal fisheries in many developing countries were not able to technically exploit the distant water fishing ground that became national with the introduction of 200 miles EEZs.

Finally, during the last decade the increasing over-exploitation of resources in the developed world has, once again, added fuel to the globalization process. While consumers in OECD markets have been told that eating fish is healthy, their domestic resources have been dwindling. Consequently, fisheries resources in developing countries in particular, and aquaculture, have come to play increasingly important roles in satisfying global demand for fish and fish products.

The problems and issues that the globalization process gives rise to in the case of natural resources was indeed also recognized by the Johannesburg World Summit on Sustainable Development meeting in 2002; an excerpt in Box 1 from the WSSD political declaration highlights this point. This statement has added increasing awareness to the problems and perhaps a political will to address the issues.

The following section will outline some basic facts about the latest development in trade in fish and fish products. This will help us understand some of the driving forces that underpin the globalization process, the present industry structure and the trade flows that have resulted.

2. Overview of the structural changes in the world fisheries markets

International trade in fish and fish products has increased substantially over the past decades. There is an important trade flow from developing countries to the OECD countries that constitute the principle market for fish. Many different species and products are traded although the lion's share of international trade is made up of groundfish, tuna and shrimp.

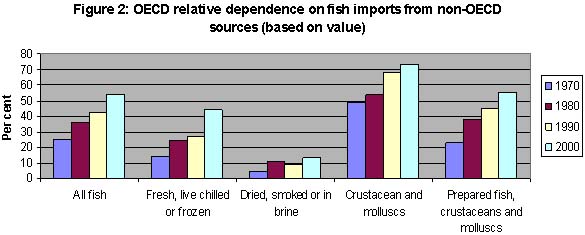

The following Figure 2 highlights the dependence of OECD countries on imports from the non-OECD (mostly developing) countries. The very high dependence on imports of crustaceans and molluscs is caused by shrimps and prawns and this group, because of its relative high unit values, has pushed up the overall dependence.

In the meantime, it is also noted that with regard to imports of fresh, live, chilled and frozen fish (mostly for further processing), the reliance has increased three fold over the thirty years covered.

Source: OECD foreign trade statistics, detailed statistics are provided in Annex 3

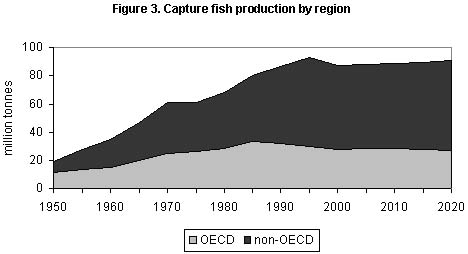

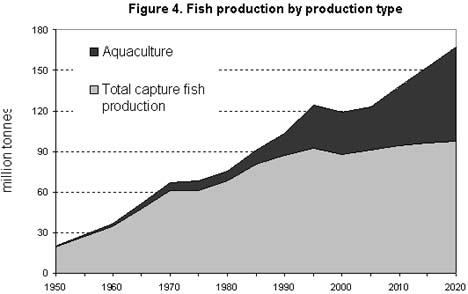

Fish products are from both capture fisheries and aquaculture origins with aquaculture increasing in relative importance as many fish stocks have reached or exceeded their maximum sustainable yields. Figures 3 and 4 depict these trends with regard to the origin of capture fisheries and the increasing role played by aquaculture in the overall supply of fish.

Source: OECD

Source: OECD Environmental Outlook

Insofar as the future demand for fish products is concerned, population growth and changes in economic conditions are two key determining factors. With regard to population growth, FAO calculates that with present day fish consumption patterns, an additional three million tonnes of fish is needed annually to satisfy the demands.[8] Demand is likely also to continue to increase as income levels within the OECD area rise and due to an increased consumer awareness of the health benefits of fish consumption.

Among OECD countries, Japan, the United States, Norway and Iceland are the largest producers. Their combined output amounts to just over half of the OECD total. The EU also accounts for a substantial part of the production (almost a quarter of the OECD total).

While the total production of the OECD countries has been fairly stable during the past decade (at around 32 million tonnes), there have been some significant changes in the composition of production. As with countries outside the OECD, the role of aquaculture has increased but for OECD countries production has concentrated on high valued species (e.g. salmon, sea bream, sea bass, and eel). Concurrently OECD production from capture fisheries has tended to decline or has at best remained stable. This situation and its causes have been documented by the OECD's work on fisheries management.[9]

The importance of these "structural" changes in production and demand should not be underestimated. They have caused major changes in trade flows to compensate for shortfalls in domestic supplies and changes in species composition. Moreover, with general levels of wealth increasing in developing nations over the decades to come a similar "demand explosion" may take place. Hence, a couple of key questions remain to be answered:

Can existing resources be fished more i.e. to what extent do we have underexploited resources?

Can overexploited resources be rebuilt to provide more fish?

Can aquaculture production help on supplies?

What effect will the various combinations of the above have on price developments?

Some answers to these questions have largely been dealt with in the paper for this Expert Consultation by Erhard Ruckes and more generally in the "The State of World Fisheries and Aquaculture, 2002" published by the FAO; the table in Annex 2 from the "State of World Fisheries and Aquaculture" sums up the issues and provides a scenario for the likely developments towards 2030. Three major future developments should in particular be noted. First, the importance of China in the overall picture and for the future developments in particular as regards aquaculture. Secondly, and this is in particular a sourcing issue, the positive future trend noted for net exports from China, Latin America and the Caribbean as well as for the Near East Asia. Third, with minor exceptions, consumption of fish is expected to increase in all major market areas of the world, in developed on developing countries alike.

The important conclusion from the work by the FAO is the increasing globalization and market interdependence that will continue to take place unabated through trade and possibly through other means such as access to resources, foreign direct investments and through services. This will be the case for both fish from aquaculture and from capture fisheries production.

3. Globalization and trade liberalization: who benefits?

The fisheries globalization process has not happened in a vacuum. Fisheries policy or trade instruments have been used to a varying degree to face up to the "pressures" of the globalization process. For example, in the 1980's, trade negotiations on the basis of the notion of "access to markets for access to resources" were in response to the pressures created by the 200 mile EEZ introduction.[10]

A recent OECD publication[11] (see Box 2) revealed that tariff rates and structures applied by OECD countries are complex with a wide variety of duty levels ranging from relatively low rates to levels well above what are considered to be high tariffs. There is also an extensive use of preferential tariff arrangements and a number of non-tariff barriers are in place in addition to technical import requirements and sanitary regulations. Of concern for fisheries trade and investments, in particular vis-à-vis developing countries are:

Tariff protection for fish is still in place albeit at a much lower level than other food products.

There is a major issue of tariff escalation among OECD countries. This has an impact on location of processing industry and on developing countries' ability to export value added products.

On some products tariff peaks are still high

Rules regarding investments and services which are restrictive

Two markets (the EU and Japan) in particular actively use tariff suspensions and the opening of tariff quotas as a way to "manage" the supplies to the domestic processing industry faced with domestic supply constraints. For example, in the case of the EU, autonomous tariff quotas "are opened on an erga omnes basis in order to ensure adequate supply to satisfy user industries. They concern raw material that are intended for the use of the processing industry and for which there is a temporary shortage in Community production." [12]The same applies to the autonomous tariff suspensions in the EU.

In Japan, the study by the OECD notes that "With a view to avoiding adverse effects of disorderly trade on the domestic supply and demand as well as stock status of the principal fish species that are targeted by Japanese coastal and offshore fishermen, certain fish are subject to the Import Quota System."[13]

It is generally recognized that trade liberalization is beneficial. This is also the general case in fisheries. However, as fish is a renewable natural resource, particular attention to the state of the resource and the fisheries management regime is warranted. This observation is an important departure from the trade in other food products, and from aquaculture, whose production systems are generally homogenous across countries and not subject to management system as in capture fisheries.

Normally, relaxing barriers will bring about gains to both exporters and importers alike. However, in fisheries the fisheries management system and the level of fishing will determine the extent to which supplies of fish to the market can change. When contemplating market liberalization, it is therefore important that the policy instruments are analysed taking into account the specific fisheries situation, including the fisheries management framework, resource exploitation level, import and export situation.

|

Box 2: "Liberalizing fisheries markets: scope and effects" The Study "Liberalizing Fisheries Markets: Scope and Effects", undertaken by the OECD's Committee for Fisheries, reviews the significant changes that the world fisheries sector has undergone over the past 50 years, from the growth in fishing technology and capacity, to the stagnation of capture fisheries production, to the surge in world trade in fisheries products. Secondly, the Study focuses on fisheries trade and market issues. While the Uruguay Round of WTO negotiations was successful in addressing a number of trade concerns key, issues remain that need to be tackled. The Study by the OECD's Committee for Fisheries was launched to gain a better understanding of the trade and resource impacts of various market measures applied in the fisheries sectors of OECD countries. The Study also explores the links between trade liberalization and fisheries resources sustainability. The theoretical framework for the research suggests that the outcome of market liberalization, and hence impacts on resource and trade, depends on whether or not the fish supplies respond to price changes flowing from market liberalisation. The ability of producers to increase supplies of fish to the world market depends on both the current level of fishing and the fisheries management regime in place. The Study offers the general conclusion that market liberalization (including improving fisheries subsidies disciplines) is not likely to have a major impact on resources in countries that use fisheries management tools that impose an upper limit on the amount of fish that can be harvested. However, in countries where management is ineffective and the high seas, where open access may still be the norm, market liberalization could exacerbate resource exploitation problems. Importantly, however, this may lead to lower fish supply in the long run. In the meantime, these linkages, in a setting of diverse fisheries management regimes, make it difficult to predict the trade outcome of market liberalization. |

The full benefits of market liberalization and globalization in general will only be achieved, without compromising sustainability, if proper fisheries management regimes are in place. To maximize welfare gains, policies should target market liberalization and improvements in fisheries management concurrently. The OECD analysis has identified aquaculture, shared stocks and high seas fisheries not subject to management, fisheries under bilateral access agreements, under exploited fisheries and multi-species fisheries to be the areas where the effects on trade and resources of market liberalization may be of particular concern. This will also be an outcome of the globalization process which, when market demand increases, may exercise renewed pressure on the resource base. In the meantime, as both developed and developing countries exhibit a variety of fisheries policy frameworks, the effects will vary considerably between fisheries and countries and could be subject to more in-depth analysis.

4. Globalization: opportunities and challenges for OECD countries

While the above has highlighted the importance of the regulatory framework that is in place with regard to trade and fisheries management, the following will identify the major opportunities and challenges that the globalization process may give rise to for OECD countries.

Before doing so however, it is useful to recall the key results from "World Fish Trade, Demand Forecast and Regulatory Framework" (by Erhard Ruckes) and the recent work from the International Food Policy Research Institute "Fish to 2020: Supply and Demand in Changing Global Markets".[14] Both sources identify that the key issue in the decades ahead will be to what extent the developing and developed countries alike will be able to manage their fisheries resources in a sustainable and responsible way.

Furthermore, there seem to be some general observations from other authors that:

Developed countries markets will continue to expand; however while doing so the marketing strategies may well have to change.[15]

Developing countries will continue to expand their capture fisheries and at a relative higher pace than in developed countries where additional supplies can only come forth through stock rebuilding.

Aquaculture production will increase substantially.[16]

As developing countries get richer demand will expand and as a consequence more intra-developing nation fish trade will take place.

Price for fish and seafood will increase at a faster pace than prices for other foodstuff.

These changes are by no means of marginal nature. They will profoundly alter the "fish business" in developed countries that increasingly will depend on imported fish from developing nations. By the same token a number of opportunities arise.

Processors in the OECD area will be particularly pressed to explore unknown or lesser known species and test their acceptability, both for processing and for consumption. This will be analogous to the "invention" of the Alaska Pollack which initially was a poor substitute of cod, but which, by now, is widely accepted by consumers. This could also include development of new technologies; e.g. is it possible to neutralize fish colour to "white" fish, change taste to suit established consumer expectations? These are avenues that will need to be explored by processors to avoid being put out of the market due to a squeezed supply of traditional fish.

Label schemes will be an additional opportunity to differentiate the available supplies from ordinary products and increase margins. The Marine Stewardship Council labelling scheme is a case in point and this scheme is now applied in a number of countries to signal that the fish is from a sustainable managed resource. So far it provides the opportunity for increased net-margins but once the "label effect" is exhausted with consumers, this route may not be an opportunity for augment margins. However, the success of such schemes clearly depends on the consumer's willingness to pay for such additional information.

Finally, the supply constraints on capture fisheries, and increasing prices of fish and fish products will turn investors into developing aquaculture systems further. It should however be noted that some countries may have a comparative advantage in the development of aquaculture. This has been the case for certain species e.g. salmon that need a particular marine environment in which to grow. Other factors that could influence the localization of aquaculture production systems include the existence of readily available processing capacity, distance to markets, environmental legislation, technology etc.

Whilst some of the opportunities have been singled out above we will now turn to the challenges of globalization. The following will focus on three key challenges that the public regulatory agencies need to address in the globalization process i.e. deregulation and reform, obstacles to reform and the governance of fisheries resources.

· Pursue deregulation and reform

As mentioned earlier, a key for the future of any fishing industry is to ensure that both the trade (and investment) and fisheries management regimes are constructed to be mutually supportive. This means lowering trade barriers while ensuring that a sustainable and responsible fisheries management system is in place.

As highlighted, a number of trade and investment impediments are in place that makes it difficult for the fishing industry (both harvesting and processing) to reap the full benefits of globalization. In particular with regard to investment and services, many countries do not allow foreign participation (directly or indirectly) in harvesting, albeit foreign participants may have a comparative advantage. But also the traditional trade impediments could be done away with and the industry would do better. This concerns in particular the tariffs and non-tariff barriers that are still in place in the trade in fish and fish products. Also tariff escalation and tariff peaks are important features of the landscape and their removal will benefit trade, localization of processing and in general the consumers.

· Obstacles to reform

Today's fishing industry structures may also be an obstacle to reform and deregulation due to vested interests in keeping status quo. Overcapacity, supported by subsidies and perceptions that the present trading and investment impediments actually help and support the industry may work against the political wish to reform. Adjustment to or the introduction of new management approaches and systems may not be perceived as positive by fishing industry interests either. While necessary for efficiency and resource conservation objectives, management reform has distributional effects that are of concern to fisheries stakeholders who hence may not be supportive of their introduction. Fears of competitiveness from foreign sources are often raised by industry participants and are an obstacle to policy reform on both trade and resource management accounts.

Opening for foreign participation in fish harvesting may also be challenged by existing fishers despite that foreign fleets may have a comparative advantage. As alluded to many impediments to the use of foreign investments or harvesting service are in place in fisheries (see Annex 1) as domestic operators and fisheries management authorities see the fisheries resources as a national endowment that should only be exploited by their own nationals. This is however, contrary to the process of "globalization" where market interdependence and liberalization suggests that the best, most cost effective producer with a comparative advantage undertakes the operation. Much work remains to be done regarding obstacles to policy reform; more transparency and a cost-benefit analysis may help. International institutions like the FAO and OECD are well placed to address this.

Fleet overcapacity in many OECD countries will put pressure on exploring alternative sources of fishing opportunities. This could be for example through access to foreign resources, through exploiting resources that so far have been too costly to exploit and through developing new fishing technologies (e.g. deep-sea fishing). It is likely that increasing pressure will be on seeking opportunities outside domestic waters, i.e. on the high seas and fishing under bilateral access agreements. This may also help explain why some countries are seeking membership of regional fisheries management organizations through which they perhaps can get a stake in a future fishery for their fleet.

· Governance issues

Public governance of the fishing industry i.e. fisheries management, including research, enforcement and surveillance, is a key component to ensure sustainable and responsible fisheries outcomes. Increasingly, however, fisheries governance has come under scrutiny with a view to assess its strengths and ability to deliver fisheries outcomes that are sustainable.[17]

National and international observers have focused on the fisheries outcome i.e. are the stocks over exploited? What's the extent of excess fishing capacity? This is likely to change in the future and much more emphasis will be on the system's resilience and (fisheries management framework) ability to deliver the stated results and objectives. Several ways of building the institutional capacity to ensure sustainable and responsible fisheries have been explored; the main observation is that there is no "one size fit all" way that can ensure the sustainability of fisheries.[18] It is therefore very important that national and international institutions with a fisheries vocation pave the way for the furtherance of more appropriate fisheries governance models that can help ensure sustainable and responsible fisheries.

Management of "international" resources, i.e. resources on the high seas have become increasingly important as evidenced by the growing number of Regional Fisheries Management Organizations (RFMO). This is also a reflection of the globalization process through which fleets have been forced to seek fishing possibilities outside domestic waters. Also in this area there are important governance challenges for developed (and developing) countries in ensuring that those resources are distributed in an equitable manner, and, by the same token ensuring that problems such as Illegal, Unreported and Unregulated fishing (IUU) do not undermine the efficacy of the RFMOs.

The FAO capacity building work in the developing world and the OECD's analytical work on fisheries and fisheries management are important contributions to this end.

5. Concluding remarks

Globalization is the growing interdependence between markets and in fisheries this happens principally through three channels i.e. trade in fish and fish products, foreign direct investments in harvesting and processing (localization) and through offering fisheries services, that includes both harvesting, processing and fisheries management services.

An interesting feature of the fisheries sector is that a "fisheries globalization process" has been underway for decades due to changes in relative resource endowment, changes in consumption patterns and thus demand, technology and available fishing possibilities with consequences for trade flows and access to resources.

Over the last decades, increasing overexploitation of important commercial fisheries resources in the developed countries has possibly accentuated the globalization process. One outcome has been an increasing dependence on supplies from developing countries. The further development of the aquaculture sector also plays an important role and will strongly influence the future supply and demand outcomes.

While fisheries markets have become more open and traditional trade barriers have been reduced significantly, there are still obstacles along the globalization avenue. Among the developed countries, tariff escalation has been singled out as a particular concern.

As for foreign direct investments in harvesting sectors, there are major difficulties for foreigners to participate and take part in fishing operations. Most countries do not allow foreign harvesting presence through company establishment, or only allow minority participation; the same applies to the use of foreign fish harvesting services which is mostly banned. Hence, globalization carries with it a major potential for additional wealth creation through further liberalizing trade in fish and fish products and investments and services in fish harvesting and processing.

Meanwhile, a major challenge is for developed and developing countries alike eliminate the restrictions they have in place in fish harvesting and trade. In this regard, alternative fisheries management arrangements may need to be addressed. The fisheries management service sectors (enforcement, management and surveillance) have been entrusted to the public civil services. But also in this sector a potential exists for wealth generation if those services could be opened to foreign participation and competition. This is happening in other sectors of the economy (in particular education and health care/hospitals/surgery). It may be that a major obstacle lies in the mantra that national fisheries resources are for nationals only.

Although the fisheries sector has gone through a long process of globalization, one integrated market for fish, fish products, harvesting rights and possibilities and management services does not exist. Obstacles on the road to globalization are vested in hard felt traditional views about ownership of fish resources, rights of access to exploitation and the role of public sector and private entrepreneurs. However, the earlier the opportunities and challenges are addressed and positive adjustment paths identified, the more successful the fish harvesting and processing industry will be in adjusting to and reap the benefits from globalization, which, in any way, is going on unabated. These issues should be addressed further and could be a subject for investigation by the FAO as well as the OECD.

ANNEX 1: SCOPE OF MARKET LIBERALIZATION IN FISHERIES

1) Tariffs and tariff measures

Within the context of the Integrated Data Base (IDB) of the World Trade Organization (WTO), WTO members are obliged to notify the applied (or actual) tariff rates in place; this information has been publicly available since 2002. While some OECD countries have set up web sites that provide up to date tariff information, the lack of transparency on applied tariff rates, combined with the complexity of fisheries tariff schedules of some countries, makes detailed tariff analysis and assessment difficult.

Tariffs collected on fish and fish products are in the order of US$1 billion per annum for the OECD countries as a whole. Due to the extensive use of tariff suspensions , preferential tariff arrangements, etc., in practice, applied tariff rates are well below the bound Most Favoured Nation (MFN) tariff rates (which are the ones that are negotiated in the various rounds of Multilateral Trade Negotiations (MTN). In fact, the bound rate is the upper level for any import tariff but a country is free to apply lower rates if it so chooses.

Tariff profiles vary widely among OECD countries, reflecting the particular fishing sector structure and the relative importance of the harvesting and processing sectors. Furthermore, the trade weighted applied tariff average for "raw/unprocessed" fish is much lower at 2.5 percent than for processed products at 6.3 percent. Thus tariff escalation is present across OECD countries. Most OECD countries offer preferential access to products from developing countries. In addition, other preferential trading arrangements among OECD countries exist including many bilateral and regional trading arrangements. The number of tariff peaks and tariff bindings remains an issue in some countries.

The effects of liberalizing trade in unprocessed fish (by lowering tariff levels) may be followed by a reduction of prices for similar fish species in the importing country. Consequently, unless fishers can increase their harvest in the importing country, their average incomes may fall while consumers will benefit from lower prices. Additional quantities from world or domestic fisheries are dependent on the availability of under utilised resources.

The relatively high tariffs on processed products (Harmonized System [HS] groups 1604 and 1605) in major import markets means that exporters are more likely to sell raw material for further processing rather than exporting processed products. In such cases tariff reductions on processed products can have consequences for the location of processing. Finally, it should be noted that general tariff reductions could undermine preferential access and tariff arrangements and ultimately make them valueless for the beneficiary countries.

2) Non-tariff measures, including quantitative restrictions, trade measures for environmental reasons, countervailing, measures, price mechanisms, licensing, trade information systems

Only one OECD country applies quantitative import restrictions in the form of import quotas. Assuming that the quotas are fully used the relaxation of these will lead to lower prices in the importing country and to higher prices for exporters.

Several regional fisheries management organizations have adopted rules for the implementation, by member states, of trade measures to meet environmental or conservation objectives. In certain cases, if countries which are not members of these organizations are found to be fishing (and trading) in contravention of the rules of the organization, they may have trade measures imposed on them. In practice, however, only one organization has required its Member countries to take measures against the imports of swordfish, bigeye and bluefin tuna from a number of non-member countries. If markets for the products from Illegal, Unreported or Unregulated (IUU) fishing can be eliminated or at least limited, such measures may prove beneficial for conservation purposes, as it would render IUU fishing less profitable. Some countries also have provisions for regulating or prohibiting imports of certain species fished under certain conditions. Relaxing such measures can have similar effects as lifting quantitative import restrictions (i.e. higher prices in exporting countries and lower in importing countries). By the time of the completion of the Study two countries had a countervailing and antidumping duty in place for salmon. Due to the structure of the international salmon market it is difficult to predict the influence on prices received by exporters as well as the prices paid by importers and consumers if the countervailing or antidumping duty is reduced or eliminated.

Three OECD countries and the European Union run price mechanism systems, the aims of which are to stabilize market prices. The overall quantity of fish involved is fairly limited. Reducing the minimum prices might increase demand and external suppliers might export more to the market whereas domestic fishers may receive lower prices for their products. However, it should be mentioned that some of the systems also have an "environmental" aspect as they discourage the harvest, through price discrimination, of for example undersized fish, and act as a complement to technical conservation measures. As such, their discontinuation could negatively influence resources and stocks. In countries with catch control or effectively managed fisheries a discontinuation of systems will not give rise to an increase in the quantities traded.

Over the last decade, the number of trade information systems has increased as a partial response to the growing concern about IUU and "Flags of Convenience" (FOC) fishing activities. These trade information systems ensure that products from legal fisheries are properly tracked and monitored. These systems are needed if trade measures are to be placed against products from countries fishing in violation of conservation rules. Such systems can also be used to better inform consumers about the products they purchase. Such systems impose costs on the harvester, as well as to some extent on the importer, corresponding to the costs of having product's paper trail followed from capture to consumption. The increased costs of using trade information systems may be translated into lower returns on fishing for producers in exporting countries. Whether this gives rise to changes in production and trade is a question of the fisheries management system in place.

Two OECD countries have an export measure in place. Both cases only involve limited quantities of fish. The two cases are both in place for monitoring purposes and their discontinuation may cause adverse effects in terms of quota management.

3) Government financial transfers

While it is difficult to assess the nature and overall size of government financial transfers, transfers to the fisheries harvesting sector are estimated to have amounted to US$5 970 million in 1999[19]. This was equal to 20 percent of the (recorded) landed value of the catch. Although the data may be difficult to interpret, figures covering the 1996-1999 period suggest that there may be a general downward trend in total amount of transfers to fisheries.

OECD Government financial transfers

US$

Million

|

|

1996 |

1997 |

1998 |

1999 |

|

TOTAL OECD transfers, of which: |

6 799 |

6 390 |

5 481 |

5 970 |

|

Direct payments |

838 |

725 |

758 |

865 |

|

Cost reducing transfers |

789 |

759 |

772 |

799 |

|

General services |

5 171 (76% of total) |

4 906 (77%) |

3 914 (71%) |

4 263 (71%) |

|

Total landed value |

37 646 |

37 820 |

29 283 |

29 785 |

|

Total transfers as a percentage of landed value |

18% |

17% |

18% |

20% |

Note: Excludes market price support.

Source: Review of Fisheries (several issues) and Transition to Responsible Fisheries (OECD, 2000)

Of the total amount of transfers in 1999, US$4 263 million (71 percent) was used for general services[20], US$799 million (13.4 percent) for cost reducing transfers and US$865 million (14.4 percent) for direct payment to harvesters. A significant proportion of payments for general services is spent on surveillance, enforcement and research and port infrastructure. The relative share of each type of expenditure has remained relatively stable over the years 1996 to 1999.

There are difficulties with respect to assessing accurately the size of government financial transfers. This is due to various factors but relates in particular to the level of government that provides transfers (national, regional or local), that some of the transfers are not posted as expenditure ("un-budgeted" transfers such as tax concessions) or because the amounts of money involved are relatively small. The WTO[21] requires member countries to notify all specific subsidies under WTO provisions to the fisheries sector at all levels of government. However, it appears that notifications do not cover all subsidies programs as the largest part of the notifications have been made by a limited number of WTO Members that notify fisheries subsidies on a regular basis.

Support to the processing sector is mainly due to tariffs on processed products i.e. market price support that is not financed by the governments but by higher prices for consumers; this is estimated to be about US$400 million per year (2000 figure) for the OECD as a whole.[22]

Government Financial Transfers (GFT) to the harvesting industries of OECD countries represent a significant policy intervention. In principle, the reduction or removal of GFTs may not have impacts on resources or trade provided there are management regimes in place which effectively control the amount of fish harvested.

However, there are a number of cases where supply responses could be forthcoming from the provision of GFTs to the sector. Several OECD countries buy access rights using public funds to ensure fishing entitlements for their fleets in other countries; these costs are often not recovered from the fishing industry. A part of the GFTs included in these arrangements cover aspects such as enforcement support, research and control facilities. The inherent value of the "resource rent"[23] is not fully charged to the fleet that benefits from such arrangements and an element of transfer could thus be present as fishing fleets otherwise may not be interested in the venture. The elimination of such payments, while case specific, could have a positive effect on the resources in the host country provided that an effective management regime is in place. Charging the full cost of the fishing rights to users can also increase the efficiency of fishing operations.

GFTs provided to the aquaculture industry may also give rise to supply responses. However more work is needed to provide transparency on this sector; this concerns in particular stocktaking of subsidy types and levels.

There may be other effects of GFTs worth noting. In the absence of effective fleet capacity controls, transfers may attract more resources than necessary to the fishery in the form of capital (vessels and equipment) and/or labour, i.e. excess capacity. As a result, profitability and average incomes in the fisheries sector are likely to be lower than otherwise would be the case as the same amount of fish is exploited at higher costs. Excess capacity may also be exported and may have spill-over effects on other countries (particularly non-OECD countries) and on the high seas. In addition, the provision of GFTs may embed expectations thereby not facilitating capacity contraction and concurrently increase pressure for higher Total Allowable Catches (TACs).

4) Sanitary and hygiene requirements

All OECD countries impose a series of sanitary and hygiene requirements for fish. While few requirements are attached to direct landings, the number and severity of requirements increases with processing stages. Most OECD countries apply Hazard Analysis and Critical Control Point (HACCP) systems and the enforcement of hygiene and sanitary requirements takes place through point inspection, through dedicated/licensed importer or through systems of approval of establishments. In this respect, the purpose of the WTO SPS Agreement and the notification requirement is to ensure a higher degree of transparency.

Sanitary and hygiene regulations translate into higher costs with effects similar to a lower price for producers in the exporting countries. If the application of such measures is unclear or not sufficiently transparent, costs may be imposed on exporters. Clarifications in these rules and increased transparency in their application will therefore increase predictability and transparency for exporters. Whether this subsequently will influence the resources and level of trade will depend on the level of resource exploitation and fisheries management regime.

In general, importers and exporters comply with health and sanitary regulations to protect consumers since, as well as facilitating trade, such regulations are aimed at enhancing consumer confidence. In the meantime, it should be observed that in many countries, sanitary and hygiene regulations and inspections are often a public domain and a general service not provided on full cost recovery basis.

5) Technical import requirements

A number of OECD countries have technical import requirements in place. These concern restrictions on the imports of fish of certain sizes (length of fish, carapace length) and of fish/crustaceans that are egg bearing. Rules are also in place regarding presentation of the fish when landed directly - e.g. whether the fish are gutted and bled. The WTO requires notification of national technical import requirements and regulations with a view to ensure a higher degree of transparency.

The use of such requirements translates into higher costs with effects similar to a lower price for producers. If they are applied only to exporters or are more severe for producers in exporting countries, their removal will benefit exporters. Moreover, technical requirements could have positive effects on the resource in both the exporting and importing country as they usually are in place as a technical measure with a resource conservation objective.

Some countries require that fish are labelled with the origin of catch, whether the fish is from wild fisheries or aquaculture production and the generic marketing name. The use of labelling schemes adds to the costs of production. If applied to both domestic and imported fish, they are unlikely to affect trade. If consumers are responding to the use of such schemes, their use could have a beneficial effect on the resources.

6) Access to ports/joint ventures/over the side sales and direct landings

Most OECD countries have some form of restriction in place on direct landings or over the side sales within their respective Exclusive Economic Zone (EEZ) in part to ensure that conservation efforts are not circumvented. There are also OECD countries that restrict, or at least make it subject to authorization, the access of fishing vessels to their ports in order to seek, for example, supplies, ship repair and crew exchanges.

Restricting access and landings of foreign vessels translate into higher costs and lower prices for producers that wish to have access to ports, over the side sales and direct landings. Concurrently, restrictions on foreign direct landings will deprive the domestic fish processing industry and market of imported fish. Such restrictions maintain higher prices on the domestic market. The domestic industry, and in particular the harvesting sector, is assisted by such restrictions and the assistance can be captured as market price support element.

7) Investments and services

Most OECD countries restrict foreign direct investment in the fish-harvesting sector. Restrictions are of two broad types. One is related to foreign investment rules and most countries have lodged reservations for the fish-harvesting sector with the OECD's Code of Liberalisation of Capital Movements. Another type of regulation concerns domestic rules regarding participation in the fisheries; this includes regulations regarding duration of residence, educational requirements and language skills which, taken together, often render foreign participation difficult. Foreign investment participation in fish processing is largely unrestricted. It has not been possible to calculate the amount of foreign direct investment in fisheries as the national statistical coverage does not allow for details by sectors.

Some OECD countries restrict the use of foreign fishing crafts by domestic harvesters and that the use of foreign fishing services is subject to authorization by competent authorities. The effects on trade and resource sustainability of allowing foreign investment in the fishing industry will depend on the fisheries management regime. In the OECD countries where catch control regimes often are in place, the availability of foreign capital may replace domestic capital but because of the catch controls there will be no effect on resources and trade. An interesting case is if the fishery is characterized by efficient management regimes with the possibility for foreign ownership of quotas. In such cases a more profitable (lower cost) foreign fleet could replace the domestic fleet.

The close relationship between free flows of investments and capacity should be kept in mind; the opening up of foreign investments may be particularly valuable once current over-capacity and IUU fishing problems have been solved. In this regard, the Spanish case study submitted to this study suggests that the introduction of tradable fishing rights at international level, as a complement to globalization of international trade, may help foster economic activities in fisheries when there is an effective control of the effort and catch.

Insofar as fishing services are concerned, very little information is available. The use of fishing services is a means to better use capacity and profit from fleets with comparative advantages in fishing. By the same token domestic fishers may be displaced from the industry. Effects on resources and trade are dependent on the fisheries management regime in place.

ANNEX 2: FAO PREDICTION ON FISH CONSUMPTION, NET EXPORT AND PRODUCTION TRENDS 1997-2030

|

Country group |

Trend in per capita consumption |

Trend in net export |

Increase in capture production(´000 tonnes) |

Increase in aquaculture production (´000 tonnes) |

|

World |

+ |

n.a. |

13 700 |

54 000 |

| |

|

|

Share in world increase |

Share in world increase |

|

Africa |

-/+ |

- |

4% |

1% |

|

China, mainland |

+ |

+ |

5% |

70% |

|

Europe, 28 countries |

/ |

-/+ |

0% |

5% |

|

Former USSR |

-/+ |

No change |

0% |

0% |

|

Japan |

+ |

- |

0% |

1% |

|

Latin America and the Caribbean |

+ |

+ |

57% |

7% |

|

Near East in Asia |

-/+ |

+ |

2% |

2% |

|

Oceania, developed |

+ |

-/+ |

5% |

1% |

|

Oceania, developing |

-/+ |

No change |

0% |

0% |

|

South Asia |

/ |

- |

10% |

8% |

|

United States |

+ |

- |

0% |

1% |

|

Rest of Asia, developing |

+ |

- |

17% |

5% |

|

Rest of Europe, developed |

+ |

No change |

0% |

0% |

|

Rest of Europe, developing |

+ |

No change |

0% |

0% |

|

Rest of North America |

+ |

- |

0% |

0% |

|

Notes: Percentage data were derived from the Global 1 study, supported by all other studies. -/+ indicates that results differed depending on the model used. |

||||

Source: State of the World Fisheries and Aquaculture, 2002

|

[4] This paper was prepared for

the FAO Industry and Expert Consultation on International Trade, Rio de Janeiro,

Brazil, 3-5 December 2003. [5] The views expressed in this paper are those of the author and do not necessarily correspond to those of the OECD or its Member countries. The paper has benefited from comments by Anthony Cox, Senior Analyst, OECD's Fisheries Division. [6] "Cod: A biography of the Fish that Changed the World" by Mark Kurlansky. Jonathan Cape, London, 1997 [7] This was the subject of a study entitled "International Trade in Fish Products: Effects of the 200-mile limit" (OECD, 1982). [8] FAO "The State of World Fisheries and Aquaculture", 2000 Edition [9] See : Towards Sustainable Fisheries (OECD, 1997). The key message from this work is that all other policy measures and outcomes in the fisheries sector takes effects against the background of the management system in place and the level (below, at, or above MSY) the country is fishing the resource base. [10] See "Fisheries Issues: Trade and Access to Resources" (OECD, 1989 [11] The "Liberalisation Fisheries Markets: Scope and Effects" (OECD, 2003) provides an inventory and overview of the trade policies that the OECD countries have in place. An overview of these instruments and their relevance is given in Annex 1. [12] "Liberalisation Fisheries Markets: Scope and Effects" pp 241 [13] op. cit. pp 259 [14] "Fish to 2020: Supply and Demand in Changing Global Markets" by Delgado, Wada, Rosegrant, Meijer and Ahmed and published by the International Food Policy Research Institute, Washington D.C. 2003 [15] See for example " The Market place for Sustainable Seafood: Growing Appetites and Shirking Seas" Sea Food Choices Alliance, June 2003 [16] In this regard, it should be mentioned that while capture fisheries supplies are finite, supplies from aquaculture can expand almost continuously. [17] See for example "The Costs of Managing Fisheries" (OECD, 2003 [18] See "Towards Sustainable Fisheries; Economic Aspects of the Management of Living Marine Resources" (OECD, 1997) which analyses the outcomes (biological, economic, and administrative) of alternative fisheries management models. [19] It should be observed that there are some data gaps. Data sources are the Review of Fisheries and Transition to Responsible Fisheries. [20] General services comprise a range of elements, including management, enforcement, surveillance, port infrastructure, regional development grants and expenditure to promote international fisheries co-operation. A listing of examples is provided in Appendix 5 to the Preliminary Assessment chapter. [21] Article 25 of the Subsidies and Countervailing Measures (SCM) Agreement requires that "Members notify all specific subsidies (at all levels of government and covering all goods sectors, including agriculture) to the SCM Committee". [22] Total tariff revenue collected for the OECD has been calculated as imports multiplied by the trade weighted tariff average; for total imports of fish and fish products this results in an estimate of US$ 1 billion for the year 2000. Imports related to processed products (tariff position 16.04 and 16.05) amounts to roughly US$ 6 billion a year with a trade weighted tariff average of 6.3% which produces roughly US$ 400 million. [23] In the context of natural resource management, the term is commonly used to refer to the difference between the market value of the resource and the costs of attaining a socially efficient level of harvest, including a normal level of profit. |

![]()

![]()

![]()