Roundwood

Mechanical

wood products

Pulp and

paper

World production of roundwood in 1992 rose by 1.5 percent from the depressed level of 1991. Most of this was fuelwood, mainly produced and consumed in developing countries where it is used for cooking and heating. There, the rapid population growth in some countries has led to such a rise in the exploitation of fuelwood resources as to cause a serious degradation of forest vegetation. Industrial roundwood, the other roundwood output, rose by 1 percent mainly because of demand growth in North America and Asia. Elsewhere demand remained static or declined.

Among the industrial roundwoods, world production of coniferous logs, the main wood used for construction in the developed countries, increased slightly in 1992. While felling expanded in North America it was depressed in many parts of Europe. In the countries of the former USSR production of industrial roundwood, mainly coniferous logs. was reported to have decreased 15 percent. The expansion in the United States was mainly due to a rise in domestic demand not exports which were affected by the ban on logs harvested on Federal forests of the Pacific Northwest. In the Spring of 1993 a new Northwest Forest Plan was announced with measures to safeguard the habitat of the northern spotted owl, designated as an endangered species. This Plan, known as Option 9, aims to reduce annual timber sales from public forests, to 2.8 million m3, 25 percent of the annual harvest in the 1980s. In addition, the Plan will require $1 200 million to be spent over 5 years to help the region's forest industry which has been heavily dependent on local timber. A bill was also signed to restore the export ban on logs harvested in Federal forests. Further restrictions on harvesting North American timber are possible as other threatened wildlife species are listed under the Endangered Species Act. All these restrictions are likely to have an impact on future timber supplies and prices on world markets. A study released in mid-1993 foresees a drop by mid-decade of 30 percent in the combined annual harvest from public and private forests.

Trade in coniferous industrial roundwood logs decreased 9 percent in 1992. Trade within Europe was hit by the effects of recession in these economies; in addition fewer logs were available from central Europe as stocks of the 1990 windblown timber had been sharply reduced during the previous year. Exports from countries of the former USSR were reported to have continued their steep decline despite rising demand for them in Asia. This decline was not, however, reflected in official statistics. In contrast there was expansion in exports of round pulpwood from Eastern European countries and the Baltic States to Scandinavia. Markets in the Pacific Rim were strongly affected by the reduced supply of logs from the American Pacific Northwest. Exports from the United States decreased by a further 18 percent to 15.8 million m3, well below the peak of 21 million m3 in 1988. This favoured exports to Asia from New Zealand, up 12 percent to 4 million m3, and Canada, up 100 percent to 2.2 million m3.

In 1993 log exports from the United States declined further and imports and prices in Asia for logs from alternative sources such as New Zealand and Chile, rose to unprecedented levels. In Europe trade returned to levels prior to the 1990 windblow.

Production of non-coniferous logs from the temperate zone declined slightly in 1992 to 118 million m3. Production in Europe, was depressed as were the economies of the major consuming countries. By contrast, production in North America rose markedly due to the increased domestic demand for furniture and the whole range of interior millwork.

Trade in non-coniferous industrial roundwood increased by 7 percent in 1992. A relatively new feature appeared to be the sharp growth of exports of non-coniferous round pulpwood from Eastern Europe and countries of the former USSR to Scandinavia. Exports of non-coniferous logs from France, the world's largest exporter, declined by a further 8 percent to 1.4 million m3. Exports of hardwood logs from Germany declined to the level prior to the 1991 peak caused by the large supply of windblown timber. Exports of American hardwood logs declined, after years of sustained growth reflecting increased domestic demand. In 1993 markets continued to be depressed in Europe but in North America the relatively high level of demand contributed to price increases for logs.

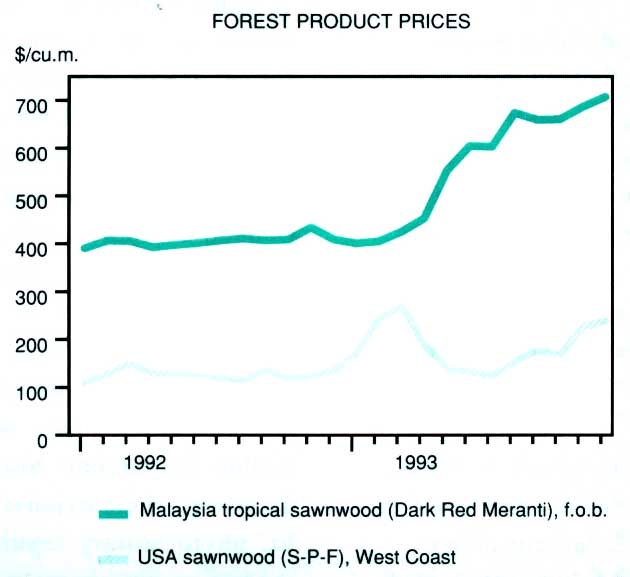

Production of tropical logs was 2 percent up in 1992 to 171 million m3. Trade in tropical logs continued its declining trend and was 3 percent down. Imports by Japan, although rising slightly, remained at a low level and some of the imported logs were only bought to augment the low stocks. Other major consuming countries in Asia, such as the Republic of Korea decreased imports considerably. On the supply side, the State of Sabah decreased its exports by 15 percent and Sarawak by 5 percent. However, there was an upsurge of exports from Papua New Guinea and the Solomon Islands. Exports from Africa went down by 5 percent continuing a steadily declining trend.

During the last part of 1992 and in 1993 supplies for export from countries in the Far East were reduced by further legislation to ban or limit exports of tropical logs. The state of Sarawak suspended log exports during the last quarter of 1992 as felling was running ahead of the reduced level set for harvesting. In January 1993 the state of Sabah imposed a ban on log exports which were later allowed after a lengthy internal discussion. Similarly, in Papua New Guinea new forestry guidelines were put in place to hold exports to the 1992 level. The Government of Myanmar decided not to renew logging concessions to foreign companies, this may result in shipments being cut to only one third of the amount in earlier years. These sudden supply constraints on log supplies, together with the anticipated reduction in supply of coniferous logs from the United States, have pushed up tropical log prices in the Far East to unprecedented levels.

World production of pulpwood increased by one percent in 1992 to 441 million m3. In Europe production recovered slightly, mainly reflecting notable increases in Finland, Poland and France. However, elsewhere in Western Europe demand from the pulp industry was depressed as was the level of production. The further steep decline in pulpwood prices was so severe as to make thinning operations in certain areas unprofitable. In Sweden the national average price for pulpwood fell by a further 8 percent following falls in the two previous years. In contrast, in North America, pulpwood sales expanded with considerable growth of wood pulp production.

Trade in wood chips maintained its previous level in 1992. Exports from the United States grew by 6 percent including an even larger increase for hardwood chips.

Markets for mechanical wood products, in 1992, were characterized by the notable increase in the construction sector, their major market, in North America while in countries of the former USSR there was a further sharp contraction. Housing starts in North America grew by 18 percent to reach 1.4 million units thus leading to a notable recovery in consumption of sawnwood and wood based panels. Demand was also fuelled by the devastation caused by Hurricane Andrew in the southeast of the United States. In Europe the construction sector continued to decline while in Japan it remained at its previous, relatively low, level of activity.

In 1993 construction activity in North America expanded again-, housing starts were 2 percent up favouring a further expansion for mechanical wood products. Construction activity remained depressed in Europe and in Japan.

World production of coniferous sawnwood in 1992, at 36 million m3, was 2 percent above the depressed level of 1991. Major growth took place in the United States, 4 percent up, and in Canada, 9 percent up, but to levels still well below those reached in the late 1980s. Uncertainty about coniferous timber supplies from the Pacific Northwest of the United States drove up the prices of logs during the last quarter of 1992. This led to higher prices for processed products such as coniferous sawnwood. European countries, in general, suffered from depressed domestic markets and output recovered only slightly from the low 1991 level. However, a marked increase in output and exports occurred in the Scandinavian countries. By contrast, production in countries of the former USSR was reported to have fallen by 23 percent. In Japan output continued to decline for the third consecutive year. Increased production was recorded in New Zealand and Chile, reflecting growing exports to the buoyant markets of the Far East.

Trade in coniferous sawnwood increased by 9 percent in 1992 to 80 million m3 recovering from the severe declines in 1990 and 1991. Canada benefited from the high demand in the United States and its exports there increased strongly, despite a 6.5 percent duty imposed by the United States. In Europe exports from the Scandinavian countries continued to expand, by 19 percent for Sweden and by 8 percent for Finland. Scandinavian exports were boosted by their increased competitiveness following the devaluation of their currencies and by the further fall in exports from countries of the former USSR, 35 percent down.

In 1993 demand for coniferous sawnwood remained relatively high in North America and prices escalated to unprecedented levels. Canada's exports, mainly to the United States, grew by a further 3 percent. In Europe, exports from Scandinavian countries continued their strong growth at rising prices. Exports from countries of the former USSR. constrained by production problems, were forecast to fall by a further 28 percent. North American shippers decreased their exports to Europe because of an EC phytosanitary regulation enacted to avoid importing pine nematode on American green lumber. Its impact on the industry in North America was offset by growth in its other markets and by higher prices. Competition for markets in Europe increased with the effects of the 1992 devaluation of Swedish and Finnish currencies, in addition supplies of substitute material from countries in economic transition further disturbed the market. This situation gave rise to a request by some EC member countries for the volume and prices of exports of coniferous sawnwood from Finland and Sweden to the EC to be monitored for three months within the framework of EC procedures.

World production of non-coniferous sawnwood from the temperate zone increased slightly in 1992 to some 60 million m3, recovering part of the decline of 1991. As for many other wood products, markets expanded in North America but were depressed in Western Europe including weakened demand for its furniture. Further. competition from Medium Density Fibreboard (MDF) increased. Production in France declined 6 percent to 3.8 million m3 in 1992. Romania and the former Yugoslavia, previously two major European producers, maintained output at levels well below those achieved in the 1980s. Production in the United States rose 10 percent.

Trade in non-coniferous sawnwood from the temperate zone grew by 10 percent to 6.5 million m3 in 1992. Exports from North America continued to grow with those of the United States 5 percent up and Canada up by 13 percent. Prices rose well above those in previous years fuelled by uncertainty about future supplies of both temperate and tropical timber. Exports from both France and Germany decreased further, penalised by the strength of their currencies. These decreases were partly offset by a notable upsurge of exports from Eastern European countries. The same market situation continued in 1993 with further growth in North America and some signs of recovery in the United Kingdom and in Germany.

Production of tropical sawnwood was down by 1.5 percent to 69 million m3 in 1992. This reflected the policy of major producing countries to favour the expansion of its transformation in their own plywood and veneer industries.

Trade in tropical sawnwood grew by 8 percent in 1992, despite depressed demand in Europe and Japan, and measures introduced in Europe to limit its use. Demand growth in countries of the Pacific Rim, notably China and Thailand, and in some Near East states, offset contraction in other markets. Exports from Malaysia, already the largest in the world, were up by 10 percent and amounted to 5.4 million m3. The states of Sabah and Sarawak increased their sawnwood exports by 9 and 55 percent respectively by diversion of logs from export to domestic sawmills. Peninsular Malaysia, whose export policy also favours further processed products. maintained its previous level of exports at 2.1 million m3. Africa's exports recovered from the low level of 1991 and grew by 10 percent.

In 1993 trade in tropical sawnwood continued to grow, but mainly in the Pacific area. Uncertainty about future timber Supplies, both temperate and tropical, led some Asian countries to increase stocks of tropical sawnwood and prices rose sharply.

World production of plywood grew by 3 percent in 1992 to 48 million m3. The increase in plywood output was mainly clue to recovery in North American markets from the depressed level of 1991. There plywood represents the largest component of wood based panels, some 52 percent of total consumption. Output was, however, still well below that of the late 1980s. In Europe and in the countries of the former USSR, production declined for the third consecutive year. By contrast, in the Far East production of tropical plywood grew strongly reflecting increases in both domestic consumption and exports. Growth of output in Indonesia, the world's largest producer of tropical plywood, was 5 percent and in Malaysia, 25 percent.

Trade in plywood in 1992 rose 3 percent above the depressed level of 1991 to 16 million m3. There was a notable upsurge of trade in North America and the Far East. Exports of plywood, mainly softwood, from the United States grew by 14 percent to reach 1.6 million m3 and from Canada by over 30 percent to 0.4 million m3. These exports went to the EC, Asia and Mexico. Very little plywood is traded between the United States and Canada because of differences in product standards. Exports of tropical plywood from Indonesia grew further by 5 percent to 8.6 million m3, more than 50 percent of total world trade; main markets were: Japan, the United States and developing countries of the Far East. In 1993 there was a notable expansion of consumption, production and trade in the Far East and North America and prices rose considerably.

World production of particleboard in 1992 maintained its previous level of 48 million m3. Production in North America grew strongly reflecting increased activity in housing and, following hurricane Andrew, in the repair and remodelling sector. Oriented Strand Board (OSB), a relatively new panel product mainly produced in North America, gained an increased share of the structural panel market. In Europe, the largest producer of regular particleboard, production and consumption declined for the third consecutive year reflecting the depressed state of the housing and furniture sectors.

Total trade in particleboard increased by 7 percent in 1992 mainly as a result of strong growth of trade in OSB between Canada and the United States. In 1993, a slight recovery in Europe reflected modest increases in consumption in the United Kingdom and Germany.

World production of fibreboard in 1992 remained at 20 million m3. The long established products, fibreboard, hardboard and insulating board, continued to cede market share to Medium Density Fibreboard (MDF). Growth in MDF production strengthened in Europe and in North America. Output in Europe in 1992 was ten times that of 1982. Rapid expansion of MDF production capacity continues as does the number of its uses in the furniture. joinery and construction sector. Trade in MDF, although still relatively small, increased.

{kind=link}