![]()

![]()

![]()

2.1 The forest resources - status and trends

2.2 Environmental initiatives, protected areas and wildlife resources: status and trends

2.3 Wood based industries (including pulp and paper): status, trends and transitions

2.4 Wood energy/fuelwood

2.5 Non-wood forest products

2.6 Services of the forest: status and trends

2.7 Institutions and policies

The Australian continent covers a land area of 768 million hectares. A large portion of the country, particularly the interior, is arid or desert land, however, there is still a large potentially forestable land area. Australia has 156 million hectares of wooded land meeting the FAO definition of forest. Within Australia the word forest is restricted to open and closed forests (>50% crown cover), which cover only 5% of the land area, but are still sufficiently extensive to give Australia the largest forest resource in the South Pacific. An additional 15% of the land is classified as woodlands and mallee (multi-stemmed eucalypts). A portion of the woodlands are also harvested. The vast majority of the Australian forest resource is natural forest, dominated by eucalypts, with the balance being a made up of acacia (Acacia spp), cypress pine (Callitris spp), paperbarks (Melaleuca spp), and tropical rainforest. Natural forests comprise 99.3% of the forest resource. The remaining forest (1.1 million hectares) is plantations. Of this, 73% is softwood (mainly radiata pine) and 26% is native hardwoods. Plantations are being established at a current rate of around 20,000 hectares per year although government policy (Vision 2020) aims to accelerate planting to treble the plantation estate by 2020.

Around 17% of open and closed forest land is reserved for conservation purposes in National Parks and reserves. The remainder is in state forests (27%), private forests (41%) and other Government lands (15%). The state forest resource is generally of considerably higher quality than the private resource and around 60% of the state forest resource is available and accessible for harvest within a multiple use framework. Forests contribute as a focus for tourism and recreation. They also provide fuelwood and a range of non wood forest products. The large area of woodlands are also important for timber, fuelwood and non-wood products. All harvesting on public lands and some private lands is covered by comprehensive codes of forest practice.

Both Commonwealth and State and Territory governments have legislation covering assessment of the environmental impact of forestry proposals and the protection of endangered species and wilderness.

There are numerous State and Territory Acts (legislation) covering conservation issues with implications for forestry including land use planning laws, flora and fauna protection Acts, Acts establishing and governing the administration of National Parks and Acts regulating water rights.

Australia is a party to the Convention for Biological Diversity and the World Heritage Convention and already has a number of World Heritage areas containing significant forest, including the Tasmanian Wilderness World Heritage Area, the Wet Tropics of Queensland, Fraser Island, the Central Eastern Rainforest Reserves (Australia), and Kakadu National Park.

Australia is in the process of establishing a representative system of protected areas including forest conservation reserves.

Wilderness areas are managed with minimal human interference. Conservation reserves are managed primarily to conserve biological diversity and ecosystem processes but also provide valuable tourism and recreational resources. Under the National Forest Policy, Governments have agreed to maintain an extensive and permanent native forest estate and manage that estate in an ecologically sustainable manner so as to conserve the full range of values that forests can provide for current and future generations.

National criteria on the levels of forest to be preserved within RFA areas are as follows:

· 15% of the distribution of each forest ecosystem existing prior to European arrival in Australia

· 60% or more of existing old growth forest

· 60% or more of existing vulnerable forest ecosystems

· 90% or more of high quality wilderness; and

· remaining occurrences of rare and endangered forest ecosystems including old growth.

Within the National Forest Policy framework, specific policies have been developed in relation to nature conservation and wilderness reserves, ecologically sustainable management and codes of practice, data collection and analysis (including continued development of the National Forest Inventory), and the protection of forests from diseases, weeds, pests, chemicals and wildfire.

Australia has a National Strategy for the Conservation of Australia's Biodiversity reliant on community support and community-based actions for its successful implementation.

Further information on the Commonwealth government's environment policies and programmes is available on the internet at:

http://kaos.erin.gov.au/erin.html

Further information on forests policies and programmes is available on the internet at:

http://www.dpie.gov.au/dpie/forestry.html

2.3.1 Sawntimber

2.3.2 Wood panels

2.3.3 Paper and paperboard

2.3.4 Forest products trade prospects

The Australian market for sawntimber in 1994/95 was about 4.7 million m3 of which about 3 million m3 was softwood. Domestic production represented about 3.7 million m3 (79%) (equally divided between softwood and hardwood). Imports were 1 million m3 (mainly softwood) whilst exports were only 500,000 m3.

Sawn timber consumption in Australia fell in 1995-96, reflecting a fall in the number of houses and other dwellings commenced. With commencements expected to remain relatively low in the short term, consumption is expected to fall again in 1996-97. Production is also forecast to fall due to the lower demand for sawn timber and a surplus of stock (see ABARE 1997).

The building industry has historically been the dominant influence on the domestic production and consumption cycles for Australian sawntimber. The building construction cycle is well into a downturn and expectations are that the industry will enter an upward phase in 1997-98 (Neufeld 1997).

The consumption and the production of sawn timber is projected to rise in the medium term as housing activity recovers, new production capacity and plantations are established, and existing softwood plantations mature. An export surplus of softwood sawn timber may emerge in the first decade of the next century (ABARE 1997).

In 1994/95 Australian production of plywood was 145,000 m3, imports 67,000 m3 whilst exports were negligible apparent net consumption (ANC) approximately 212,000 m3. Particleboard production was 864,000 m3, imports 35,000 m3 and exports 71,000 m3 (ANC = 828,000 m3). Medium Density Fibreboard production was 436 000 m3, imports 102,000 m3 and exports 128 000 m3 (ANC = 410,000 m3).

The consumption of wood based panels fell in 1995-96 and is expected to fall further in 1996-97. However, consumption is projected to recover in the medium term. Exports, particularly of medium density fibreboard, are also projected to rise, based on expected higher production from recent and planned additions to capacity (ABARE 1997). Production of medium density fibreboard (MDF) will exceed consumption toward the end of the decade and import substitution and exports will drive the industry (Neufeld 1997).

There is a clearly established trend to increased production, import substitution and increased exports in paper and paperboard (Neufeld 1997). Fixed capital investment rose in the pulp and paper industry by 23.5% during 1995-96 including significant investment in plantations. Sales revenue rose by 9.5% due to increased prices in the early part of the year and a run down of stocks held be retailers. Export sales grew by 4% in 1995-96.

Australian production in 1994/95 was 2.3 million tonnes, imports 1 million tonnes and exports 272 kilotonnes (ANC about 3 million tonnes). The majority of imports were for printing and writing papers (60%) whilst exports were mainly packaging papers (80%).

The balance of trade on pulp and paper products continued to decline going from $1.7 billion in 1994-95 to $1.8 billion in 1995-96 though its decline slowed. The Commonwealth Government considers there is considerable scope for additional investment in the pulp and paper industry including recycling, which could result in import replacement. Import substitution and increased recycling are objectives of both industry and government.

In order to reduce our dependence on imports a new 150 kilotonne paper machine, to produce printing and writing papers is being installed and this is expected to be operational in mid 1998. Feasibility studies are underway for two kraft pulp mills (an unbleached softwood mill and a bleached eucalypt mill). Significant new investment in machinery and plantation establishment is expected in the outlook period.

Australian consumption of printing and writing paper fell in 1995-96 due to high international paper and pulp prices and surplus local stocks. World prices fell in early 1996, however, and printing and writing paper consumption is forecast to recover to some extent in 1996-97. Population growth and rising incomes are expected to increase consumption of paper and paperboard products in the medium term (ABARE 1997).

Australia's wood panel production is expected to exceed domestic requirements in the long term. Prospects for exporting panel products will depend on cost competitiveness with expanding industries in Asia and North America. Prospects to expand export oriented process of pulp and paper products will depend on whether the Japanese price of woodchips remains high, and international cost competitiveness (Cameron 1997 and de Fégely 1997).

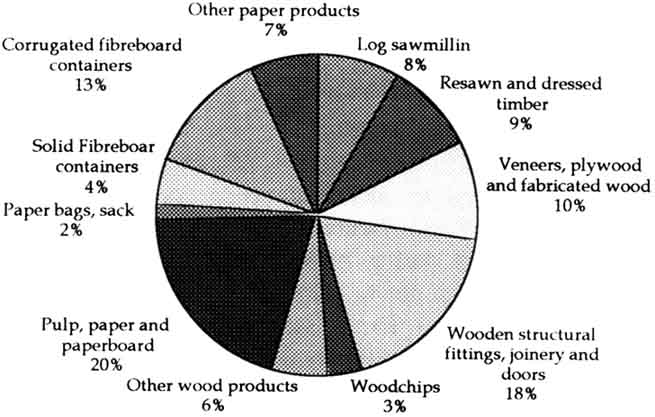

Value of turnover in forest products industries

Residential consumption of fuelwood collected by householders is difficult to measure and is estimated from various assumptions regarding capacity and use. Bush et al. (1997) estimate that around five million tonnes of fuelwood are consumed each year in Australia for residential heating.

Industrial consumption is derived from biennial surveys conducted by ABARE, and is estimated to be around 300,000 tonnes a year. The bulk of this is consumed by the wood, paper and printing industries (Bush, S., Harris, J. and Ho Trieu, L., 1997).

Fuelwood does not constitute a major source of electricity production though there are examples of wood by-products being used to generate electricity in particular industrial plants or regions. Fuelwood collection is not a major source of employment in comparison to employment derived from other forest industries.

One of the most significant non-wood forest product produced from Australia's forests is honey, and native forests comprise an estimated 85% of the industry's resource base (Federal Council of Australian Apiarists Association personal communication 1995). Around 20,000 tonnes of honey are produced annually in Australia (ABS AgStats), with a retail value of around $100 million in 1995. Honey production has been integrated into forest management techniques. Wildflower harvesting from native forests is also a significant industry in some parts of Australia. In Western Australia the wholesale value of the wildflower industry is $50 million annually, half of production is estimated to come from forest land.

There is a small scale industry comprising about 160 firms/individuals harvesting bush foods relying on more than 300 plant species. The industry, worth about A$13 million per annum, supplies a domestic niche market. Oils are produced from a range of eucalypt species and oil production has been successfully integrated with wheat farming in some areas of Western Australia. Some bush foods are being investigated for their potential for wider commercialisation under Australia's Farm Forestry Programme.

Governments are anxious to better educate the public on the complex issues involved in managing forests and the balance to be struck between industry and conservation concerns. Educational materials have been produced by State forestry agencies, industry and conservation groups presenting perspectives on the issues. The governments distribute information concerning their forest policies and consult widely before making policy.

Australia has a number of forestry and forest products research organisations. The Commonwealth Scientific and Industrial Research Organisation's Division of Forestry and Forest Products is the largest national forest industries R & D organisation and undertakes research on species and provenance selection, genetic research including solid wood conversion and processing, composites, pulp and paper and protection of wood in science. The State forest agencies undertake R & D in support of their own forest management and development activities while industry undertakes most of its research in the forest products area.

A Forest and Wood Products Research and Development Corporation was established pursuant to the NFPS. Its purpose is to promote effective research and development which fosters an internationally competitive, sustainable and environmentally responsible forest and wood products industry in Australia. The Corporation has five year research and development plans progressively implemented in annual operational plans. The Corporation's role is to improve the level and relevance of research by identifying priorities and commissioning, administering and subsequently evaluating research into a broad range of issues relating to wood production, extraction, processing, economics and marketing. It is funded by industry levy and by government.

The Farm Forestry Programme aims to increase funding to research activities relevant to farmers and industry. It has funded research concerning the viability of low rainfall agroforestry (species, products, markets); high value timber species, products and markets; non-wood products; improving the availability and coordination of seed, site selection and silvicultural information for farm forestry systems. The Farm Forestry Programme aims to forge stronger links between researchers and the broader farm forestry community.

Tourism is an important and fast growing sector of the Australian economy. Distinctions between ecotourism and 'ordinary tourism' motivated by a desire to experience different ecosystems and see different species are difficult to draw. Australia's unique forests and the species they contain are important in providing industry development opportunities for tourism.

Survey data do not directly measure visits to forests or the extent to which Australian forests or forest dwelling species motivated visits to Australia or particular areas within Australia. Almost half of international tourists to Australia visit a botanical garden or park whilst in Australia and almost half visit a zoo or wildlife sanctuary indicating a high degree of interest in Australian flora and fauna (Preece, N. et al 1995). Domestic interest in ecotourism is strong, a survey concerning holiday plans revealing 53.2% of participants planned to visit a natural attraction or National Park to enjoy nature during their next holiday (Bureau of Tourism Research 1995).

There were estimated to be approximately 600 ecotourism operators in Australia in 1995, employing 6,500 people (equivalent to 4,500 full time jobs) and having a turnover of about A$250 million. The extent to which ecotourism operates in forests varies from region to region. In Tasmania 80% of ecotourist operators conducted activities inside State Reserves many of which comprise forests. The study providing the estimate took the view ecotourism comprised educationally aimed operations designed to teach participants in tours about the environment they were travelling through. These operations which are based in nature experiences comprise a small (total employment in tourism is 130,000 directly and indirectly) but growing segment of Australian tourism. Of course many tourist operations are nature based to the extent they involve looking at or travelling through the natural environment.

Visits to National Parks have generally increased since the early 1990's. In some Parks the number of visits have increased substantially-at over 10% per annum. Visits by people from overseas are a small proportion of visitors-approximately 7% though this may increase due to the strong growth in the number of overseas visitors interested in bushwalking and outback safari tours (both with average annual growth of 11% between 1989-94 compared with annual growth in visitation to Australia of 9%). Over the same period the number of international visitors undertaking bushwalks increased by 66% and the number who undertook outback safari tours increased 70%. The bulk of this growth is comprised by European and Japanese visitors. On average bushwalkers and safari tourers spend more money in Australia than other tourists (58% more and 100% more respectively). A 1993 survey indicated 11% of international tourists go bushwalking. In 1994 13% of the 3.1 million of the over 15 year old inbound tourists went bushwalking. 12% of those in bound tourists also went on rainforest walks and 50% visited National or State Parks or Reserves.

Intergovernmental institutions concerned with the development and coordination of forestry policy include the Ministerial Council on Forestry, Fisheries and Aquaculture (MCFFA) involving Ministers from the Federal. State and Territory Governments and the Standing Committee on Forestry comprising senior officials from those governments. Coordination of major policy commitments occurs through the MCFFA or through the Council of Australian Governments (COAG), a meeting of State Premiers and the Federal Prime Minister.

The NFPS represents the guiding policy document for management of Australian forests and forest industries, supplemented by the WAPIS. Implementation of the NFPS and WAPIS are the priority activities for governments for the foreseeable future. Priorities in advancing implementation of the NFPS and WAPIS are the establishment of RFAs in the major forested regions in Australia, the removal of impediments to industry development contained in planning and tax laws removing export controls on unprocessed timber and wood chips sourced from RFA areas and plantations and providing a sound legal basis for separating ownership of trees from the land to enhance tradability of growing timber as an investment.

Each State has a forestry agency though the institutional arrangements vary considerably between them. There has been a recent trend to combine forestry and agriculture agencies within State Governments. Most State Governments are in the process of privatising or corporatising their plantation operations leading to greater private investment opportunities.

Establishing farm forestry as a self perpetuating part of Australia's agricultural landscape is a major priority. If Australia is to meet its target of trebling its plantation area by 2020 much of the land planted will come from the farm sector. The Commonwealth is fostering a regionally integrated community involvement approach to farm forestry by working in partnership with the States, local government, regional development organisations, industry, landholders, and landcare and community groups. In the outlook period the programme will increase its support for activities in lower rainfall regions, including the development and promotion of wood and non-wood products, especially where these activities address biodiversity and land degradation issues.

![]()

![]()

![]()

{kind=link}