![]()

![]()

![]()

3.1 Assessment of future supply and demand for forest products and services

3.2 Future development and development objectives

3.3 Implications and scenarios

Australia's total exploitable forest area is projected to increase during the outlook period (from 16.6 million hectares to 17.8 million hectares) due to the increase in the plantation estate. The native forest resource in both area available for exploitation and quantities of timber cut are projected to remain static. Removals of all timber are projected to increase from 19.5 million m3 in 1995 to 21.2 million m3 in 2010, the increase made possible by large areas of plantation reaching maturity towards the end of the outlook period and beyond and because of increased regrowth in native forests.

The factors affecting future demand for forest products are discussed in the following section and section 2.3 Wood based industries (including pulp and paper): status, trends and transitions.

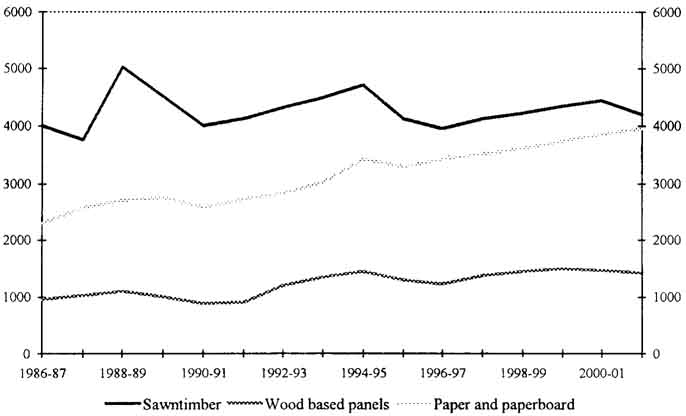

The consumption of sawntimber in Australia is highly cyclical, depending on the housing industry, but also on other end uses and the economy. The average annual level of sawntimber consumption over the next fifteen years is projected to be approximately 4.2-4.3 million cubic metres, consisting of around 1.4 million cubic metres of hardwood, and 2.8 million cubic metres of softwood. By 2006-07, over 30% of timber consumption is expected to be in the alterations and additions sector, compared with 26% in 1994-95, and to exceed consumption in the detached dwelling sector (which accounted for approximately 38% of sawntimber construction in 1994-95). As a result of an increasing availability of plantation radiata pine and a decline in the availability of native hardwood, there is expected to be a shift to a greater proportion of softwood consumption in all end use categories, particularly in residential construction (Neufeld 1997).

Over the longer term, sawntimber production capacity is expected to expand, as a result of maturing softwood plantations and investment by domestic and international investors in new softwood and hardwood plantations and production facilities. Annual average production of sawntimber for the five year period to 2010-11 is expected to total almost 5 million cubic metres, well above the 3.7 million cubic metres produced in 1995. The increase is expected to result mainly from a projected 70% increase in the production of plantation softwood. The production of hardwood sawntimber is projected to remain stagnant over the same period, at around 1.3 million cubic metres a year, mainly because of restrictions on production from native forests (Neufeld 1997).

As a result of increased domestic production, sawntimber imports are expected to decline rapidly over the five years to 2005-06, and in the five years to 2010-11, Australia may have an annual average surplus of sawntimber exceeding 700,000 cubic metres. Because of restrictions on supply, however, the hardwood deficit is expected to remain substantially unchanged for the future (Neufeld 1997).

The longer term outlook for panel products is similar to the outlook for sawntimber. Traditionally, imports constitute a significant proportion of total consumption of panel products. However, Australia now is able to meet its requirements for particleboard and plywood from domestic sources, although softboard is virtually all imported. In future, driven by a rapid expansion in production capacity, the panel industry will become more competitive and export oriented, especially so in the case of medium density fibreboard (MDF) (Neufeld 1997).

The four Australian MDF projects underway will require a substantial lift in exports to secure an adequate market and should result in Australia achieving a positive trade balance for wood based panels (Cameron 1997). As a result of investments in new capacity, annual production capacity of MDF is expected to reach 1 million cubic metres by the year 2000, well beyond Australia's consumption requirements, and annual MDF exports could be as high as 400,000 cubic metres (Neufeld 1997).

Australia's $1.9 billion a year trade deficit in forest products is dominated by net imports of around 550,000 tonnes of printing and writing paper, 280,000 tonnes of newsprint, 40,000 tonnes of packaging and sanitary paper, and 75,000 tonnes of pulp. The 945,000 trade deficit in pulp and paper is equivalent to around 3 million cubic metres of pulpwood. There is potential to reduce or even eliminate this trade deficit if chip exports could be diverted to domestic processing. However, assembling sufficient secure volume within economic haul of new worldscale pulpmills may be a considerable challenge (Cameron 1997).

Removals of logs - broadleaved vs coniferous

Outlook for the consumption of forest products

Sawnwood consumption vs production

The future of the sawnwood and wood based panel industries in Australia will be significantly influenced by changes to Australia's forest estate. While the specific implications of the Regional Forest Agreement process for Australia's native forest industry are yet to emerge, there is increasing availability of plantation softwoods and increasing competition from imports, particularly from New Zealand.

Consumption of sawnwood beyond 1996-97 is projected to increase by an average of 1% a year to reach 4.3 million m3 in 2000-01, while consumption of wood based panels is projected to increase by an average 3.5% a year. Australia has significant areas of plantation softwoods which will reach maturity during the outlook period and are likely to be used to meet these projected increases in consumption and to supply export markets.

The growth in consumption is based on a projected increase in new dwelling construction, and growth in alterations and additions and non-residential construction activity over the outlook period to 2001. However, growth in the consumption of sawnwood and wood based panels is projected to remain subdued in 1996-97, with the residential housing market depressed. A recovery in the residential housing market is predicted for 1997-98.

Australian hardwood sawmillers face a decrease in the availability of high quality hardwood logs over the outlook period. Consequently, domestic supply of hardwood sawnwood, which has remained at around 1.6 million cubic metres a year since 1990-91, is projected to fall over the medium term and keep hardwood prices high relative to softwood prices. State forestry agencies began planting softwood plantations from the 1970's onwards with a long term view to producing timber for house and other construction purposes and to enable hardwood species to be used for higher value uses. Recently hardwood sawmillers have begun diversifying into kiln-dried timber for furniture, flooring, mouldings and other value-added markets as greater volumes of the softwood resource reach maturity. Over the medium term, growth in softwood sawnwood consumption is expected to be largely determined by its price competitiveness, not only against domestically produced hardwoods, but also against imported softwoods from New Zealand and North America.

Over the medium term, consumption of softwood sawnwood is projected to continue to increase, reaching around 70% of total Australian consumption of sawnwood in 2000-01, as logs available for production from plantation forests increase and as softwood timbers displace higher priced imported and domestic hardwood timbers. To facilitate increased softwood production, mill capacity expansions are being organised.

Australian exports of particle board, mainly to South East Asia, reached a record 71 000 m3 in 1994-95, growing by an average 46% a year for the two previous years. Exports, particularly of medium density fibreboard, are projected to rise, based on expected higher production from recent and planned additions to capacity (ABARE 1997). Production of medium density fibreboard (MDF) will exceed consumption toward the end of the decade and import substitution and exports will drive the industry (Neufeld 1997).

Australian producers are able to meet domestic consumption of plywood. The major factors influencing the outlook for plywood industries are the expected growth of the building and construction sector and the availability of high quality veneer logs.

Forest policy in Australia over the outlook period is likely to be driven by the NFPS and WAPIS with focuses on increasing the competitiveness of Australia's wood products industries and ensuring wood based industries are conducted sustainably. Reducing sovereign risk in forest industry investments will result from implementation of these policies. The result for Australia should be decreasing reliance on imports particularly in the pulp and paper sector and in sawn wood and greater employment in regional Australia through greater downstream processing. As a relatively small player on the world market the Australian forest industries are subject to world market influences making precise outcomes difficult to predict.

Reafforestation through farm forestry and plantations will be pursued for forest industry and environmental objectives such as greenhouse benefits. Australia's plantation estate is likely to shift more in the direction of native species (currently only 26% of plantations are eucalypts) though softwood will remain important.

There are likely to be efforts to improve efficiency in other areas of the economy which impact on forestry such as the transport sector, particularly on the waterfront. Export controls are in the process of being removed and are likely to be completely removed during the outlook period. Further efforts will be made to make investment in tree growing more attractive including measures to make the buying and selling of growing trees (as distinct from the land on which they are grown) simpler.

Australia's low population densities, extensive forests and recreation facilities make it likely that it will attract tourists interested in ecotourism or nature based experiences. Forests will continue to contribute to the development of regional tourism based industries.

Research, particularly provenance testing and genetic improvement of Australian species, will continue as will Australia's engagement with the Asia Pacific timber producing countries with a view to improving forest management practices.

It is likely there will be greater opportunities for private investment in forest industries and tree growing. There are large scale private plantations in a number of States, some foreign owned, some domestically owned. Opportunities for further plantation expansion exist in a number of areas to supply the long term needs of domestic industry. Smaller scale plantations on farms are likely to increase bringing environmental and economic benefits to regional Australia.

There should be greater opportunities for downstream processing in Australia particularly in pulp and paper and Medium Density Fibreboard plants. There will be regional variation in the need for investment in additional sawmills influenced in part by the location of plantation resources and Regional Forest Agreement outcomes. Transport infrastructure investment opportunities may arise potentially in railways and port facilities.

Research and development activities are likely to have continued significant government involvement particularly in the forest production sector due to the long term nature of the activity and the level of risk involved though larger plantation owners are expected to engage in significant provenance testing and silvicultural techniques research. Provision of Australian forestry expertise to the Asia Pacific region is likely to increase through consultancy firms involvement in the region and through graduates from Australian universities working in the region. Australian expertise in sustainable forest management and increasing work on criteria and indicators of SFM could be a valuable case study for other countries in the region seeking to improve their own forest management practices.

![]()

![]()

![]()

{kind=link}

{kind=link}

{kind=link}