![]()

![]()

![]()

Valuable hardwood plantations have the potential of satisfying an appreciable proportion of the demand for forest products in addition to reducing the need to exploit the natural forest. However, when deforestation is being driven by demand to open new forest lands for farming, plantations will not help to reduce the pressure.

It has been argued that if plantations supply large amounts of quality timber efficiently, they may undermine the value of natural forest stands and lead to their more rapid destruction. Based on this, it has been suggested that a sensible balance be struck between production from natural forests and plantations where the former exist. Hence, where possible, natural forests and plantations should be managed on a complementary basis (Grainger 1993).

As the fastest growing economic region in the world, the pressures on Asia's forest resources are enormous. Land cleared for agriculture supplies timber on a one-time basis. These loses to the land base will make it very difficult for many of the countries in Asia to maintain their current supply into the next century. It is anticipated that the implementation of sustainable forest management practices will avoid a supply crisis in the region and that supplies from new plantations will start to appear before 2020 (Ministry of British Columbia 1994). However, the latter will only occur if rotations are reduced (Table 5).

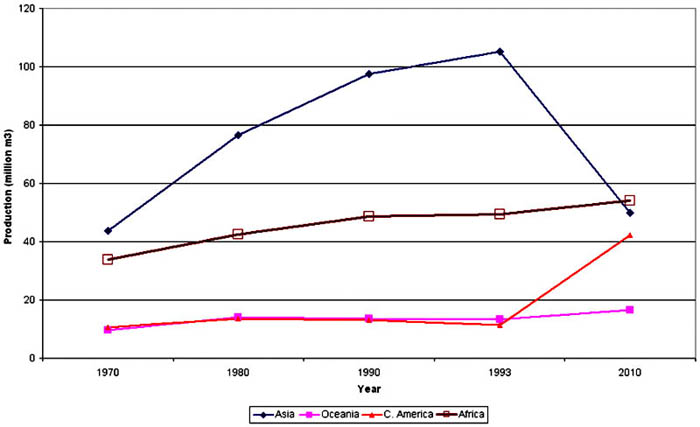

It is estimated that after the year 2000 timber reserves in the natural forests in Asia could become so depleted that exports will decline and supplies would be unable even to meet domestic needs. This trend is demonstrated in Figure 1. Grainger (1993) states that “if the bulk of tropical hardwood is going to come from tropical rainforests in the foreseeable future, it is essential to reverse the bias against natural forest management and direct more resources to make this more sustainable”.

High-grade hardwood plantations account for only 9 percent of the total tropical timber plantation area (FAO 2000) and less than 1 percent of all hardwood production (FAO 1997). That share is unlikely to rise above 5% in the next 30 to 40 years (Grainger 1993). Higher tropical hardwood prices will be needed to encourage a rise in the rate of planting. This is likely as supply shifts occur from low-production-cost natural forests in South East Asia to the higher-production-cost ones in Latin America and Africa.

As discussed earlier, Asia has the largest area of the valuable hardwoods plantations especially with regards to teak. Due to the timing of previous tropical hardwood plantings and the delays caused by the long 70-year rotations of teak plantations established in Asia in the last few decades, overall plantation production could dip in the early part of this century. Any new high-grade hardwood plantation will take at least 40 years to mature. Hence any major initiative to expand their area significantly will not be felt in the next 30 to 40 years.

![]()

![]()

![]()

{kind=link}