|

|

SUGAR

PRICES

|

|

Large global surplus pressures sugar prices to two-year lows

|

|

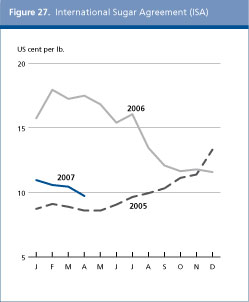

The International Sugar Agreement (ISA) daily price for raw sugar averaged US$ 9.72 cents per pound in April 2007, the lowest level since July 2005 and nearly 80 percent lower than the monthly average for April 2006. Major factors behind the steady decline in prices include the much larger than anticipated crops in Brazil, China, Cuba, the Dominican Republic, Guatemala, India, Pakistan, Thailand and Vietnam. The recent Government of India announcement that it would provide export incentives for white sugar to national sugar mills has resulted in further downward pressure on world refined sugar prices, which fell to US$ 14.28 per pound in April 2007, compared to US$ 21.36 per pound in April 2006.

PRODUCTION

|

|

FAO has revised its 2006/2007 production estimates currently forecast to reach 159.2 million tonnes globally, 3.6 million tonnes more than the estimate released at the end of 2006 and 4.8 percent, or 7.3 million tonnes, above 2005/06. Last year, at this time, global sugar markets were struggling with the third consecutive year of supply deficit, with prices hitting 25-year highs in early 2006. Producers in many countries planted more area to sugar in response to the record prices, and estimates of global output have been revised upward due to much larger than anticipated output in most cane producing countries, particularly Brazil and India. Sugar output in developing countries for 2006/2007 is estimated to grow by 9.1 percent year-on-year, whereas developed country output is forecast to decline by 6.3 percent.

Record sugar crops lead to larger than expected global surplus

|

|

Countries in Latin America and the Caribbean are expected to account for 53 million tonnes or one-third of total global output in 2006/2007. Brazil may witness another record season, with cane output estimated to increase by 13.2 percent, reaching 33 million tonnes, driven by higher yields and the increased capacity of 25 new mills in the Centre-South region. The increase in ethanol consumption during 2006//2007 was dramatic, in part led by hydrous ethanol consumption, which some sources note to have increased by almost 30 percent to 6.5 billion litres. Ethanol prices have increased significantly in recent months, attributable to a recently introduced (April 2007) Government regulation limiting ethanol trade through distributors to five percent of total turnover, restricting normal trade flow in domestic markets. Currently, 60 percent of flex-fuel vehicles use ethanol, the majority located in Sao Paolo. Expectations are that increased cane availability from this years record crop may exceed the requirements from ethanol demand, potentially resulting in increased volumes of cane converted into sugar. However, less sugar output should be directed to exports in the coming year given expectations of lower prices, and given that the Government is contemplating raising the mandatory blending ratio for ethanol in 2007/2008.

Estimated production in Africa has been revised upward to 10.5 million tonnes up 6 percent from the previous season, with forecast increases for Malawi, Mauritius, Mozambique, Zambia and South Africa. Extremely wet conditions in Kenya constrained delivery of harvested sugarcane to the mills for processing, and also reduced sugar content of this years crop. Plans to expand sugar out-grower schemes are underway in Malawi and Zambia with the support of the private sector. Sugar production in Mozambique continues to grow at a rapid pace, passing from 39 000 tonnes in 1998 to 282 000 tonnes by 2006/2007. The country is to receive US$ six million between 2007 and 2010 from the European Union to adjust its sector to the EU sugar reform. The funding will be directed toward the promotion of small and medium-sized sugarcane farmers. Production in Swaziland is likely to reach 662 000 tonnes, while output for Zimbabwe has been slightly revised downward to 427 000 tonnes. A major factor underpinning expansion decisions in sub-Saharan Africa is the expectation of some gains from the granting of preferential access to the EU market to the Least Developed Countries (LDCs) under the Everything but Arms (EBA) initiative. The estimate for Egypt has been raised to 1.8 million tonnes, roughly two-thirds of which is derived from sugarcane and one third from sugarbeet. Egypt is expanding its sugar industry, particularly sugarbeet. Sugar production is down slightly in the Sudan. Production there is likely to reach nearly 800 000 tonnes in the current year, in line with output levels of the past few years. The Sudanese Government has announced an agreement to establish a US$ 224 million sugar factory that would produce 10 000 tonnes of sugar and 60 000 tonnes of molasses.

Output in Asia up nearly 17 percent

|

|

Estimated production in Asia now stands at 58.4 million tonnes, a nearly 17 percent increase over 2005/2006. Producers in the region responded to higher world sugar prices, resulting in sizeable increases in production. For example, dramatic increases in sugar output were witnessed over last year in the region: Bangladesh up 30 percent, Malaysia up 38 percent, Thailand up 38 percent, Vietnam up 46 percent. Output in India at 25 million tonnes was 20 percent higher than last year and a new record. To support the industry, in April 2007, the India Elections Commission approved a Government proposal to offer export incentives (raw and refined sugar products) to those sugar mills most at risk from the steady decline in international sugar prices, a move, which if implemented, could impact price and trade dynamics for the remainder of this marketing year. Further expansion of the domestic sugar sector in China has resulted in an estimated output of 11.2 million tonnes for 2006/2007 and reduced the quantity of sugar that China may import this year. Indonesia, because of a poorer than expected cane harvest due to very dry weather, has announced plans to import 225 000 tonnes of raw sugar. In Yemen, a group of investors from the country as well as from Spain and Lebanon have announced plans to construct a factory in Hadramout with a production capacity of 600 000 tonnes per year.

Production down nearly 16 percent in the EU

|

|

Significant contraction in European Union sugar output was expected in 2006/2007 as the EU sugar reforms were implemented. FAO currently estimates EU (25) production at 17.1 million tonnes, down some 3.2 million or nearly 16 percent from 2005/2006, the year prior to the implementation of the EU sugar reform. Although output increased slightly in Spain, it was uniformly down in the rest of the Union. The European Commission has proposed to remove all remaining quota and tariff limitations on access to EU markets for African, Caribbean and Pacific (ACP) countries as of 2009, as part of the negotiations related to the Economic Partnership Agreements (EPA). The EU has also approved reduced import tariffs on raw sugar for new member states, Bulgaria and Romania, which will last until 2009.

Estimated output in the Russian Federation has been revised upward, from 3.1 million to 3.3 million tonnes which would be 22 percent above 2005/06. The Government announced that the current raw sugar import tariff will remain at US$ 140 per tonne. Production estimates for the United States, at 7.5 million tonnes, point to a 15 percent increase over the past year, and is comprised of some 4.5 million tonnes of sugarbeet and 3 tonnes of sugarcane. Forecast sugarbeet area is some 5 percent lower than last year, as producers shifted land to maize where feasible, given its currently attractive price and strong and growing demand for ethanol. Sugar production in Australia has been revised downward by 15 percent to 5.1 million tonnes for 2006/2007, given the drought conditions the country faces, whereas production in Fiji is up 25 percent over last year, as the sugar sector seeks ways to add value, potentially focusing on conversions to organic sugar products.

| |

Production |

Consumption | | |

2005/06

estim. |

2006/07

fcast |

2005/06

estim. |

2006/07

fcast | | | | | |

million tonnes, raw value | |

WORLD |

151.9 |

159.2 |

148.9 |

152.3 | |

Developing countries |

109.0 |

118.9 |

100.8 |

104.1 | |

Developed countries |

43.0 |

40.3 |

48.1 |

48.2 | | Asia | 50.0 | 58.4 | 65.9 | 67.8 | | Africa | 9.9 | 10.5 | 14.6 | 15.3 | | Latin America and the Caribbean | 52.0 | 53.0 | 26.4 | 26.9 | | North America | 6.6 | 7.6 | 10.8 | 10.8 | | Europe | 26.8 | 24.1 | 29.7 | 29.8 | | Oceania | 6.6 | 5.6 | 1.5 | 1.6 |

UTILIZATION

|

|

The FAO estimate of world sugar consumption in 2006/07 is currently estimated at 152.3 million tonnes (raw value), representing a 2.3 percent growth from the revised level of 148.9 million tonnes in 2005/2006. Although still below the long term average annual growth rate of 2.4 percent, global offtake has been recovering since prices started their decline from the 25-year highs recorded last year. The previous FAO estimate of sugar utilization in developing countries is now reduced by about 400 000 tonnes to 104.1 million tonnes, representing an absolute increase of 3.3 million tonnes or 3.3 percent up from the previous years estimate of 100.8 million tonnes.

Growth in Asia continues to underpin global utilization estimates

|

|

More than 60 percent of the increased sugar utilization in developing countries is expected to be concentrated in Asia. This reflects a combination of factors, such as large populations, strong demand by the food industry, particularly the bakery, confectionery and soft drinks sectors, and strong GDP growth. Sugar disappearance in India is expected to rise to more than 21 million tonnes, driven by economic growth and falling domestic prices. Domestic consumption of sugar in China is expected to reach 13 million tonnes, almost 2 percent higher than in 2005/06. Population growth and increased industrial use of sugar in processed foods will continue to underpin sugar disappearance in China, the second largest consuming country in Asia . Sugar consumption in Indonesia may also increase to 4.3 million tonnes, reflecting the upward trend in household consumption and industrial disappearance.

For developing countries in Africa, sugar consumption is estimated at 9.7 million tonnes, almost 400 000 tonnes more than last year, primarily due to increased consumption in Egypt and the Sudan, largely driven by population growth. Sugar offtake may reach 26.9 million tonnes in Latin America and the Caribbean, although growth rates are expected to slow, reflecting the relative saturation of markets and, in the case of Mexico, competition from alternative sweeteners that has intensified following the elimination of the 20 percent tax the government had imposed on beverages containing high-fructose-corn syrup (HFCS). Uncertainties remain in regard to the impact of the full implementation of the North American Free Trade Agreement (NAFTA) and the ability of the industry to satisfy internal demand and at the same time compete for market opportunities in the rest of North America once all three NAFTA markets are fully integrated in 2008.

Sugar consumption in developed countries in the current year is not expected to experience any substantial change, due to long-term and sustained underlying factors, such as a fully saturated market, growing dietary and health-related concerns and low price elasticities of demand. Consumption in developed countries is thus likely to remain at an estimated 48.1 million tonnes. Demand is expected to remain flat in the EU (25) and the United States, at 17.9 million and 9.5 million tonnes, respectively. Marginal increases are expected in the Russian Federation, where steady growth in industrial offtake should continue to more than offset declines in sugar consumption at the household level.

|

June 2007

June 2007