November 2007 November 2007 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

WHEAT

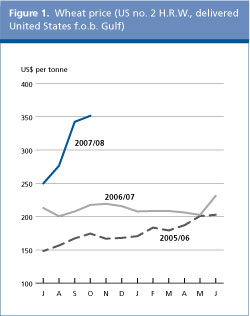

While in recent weeks international wheat prices have lost some ground from their record highs registered in late September, they are still 50 to 65 percent (depending on the type and origin) above last year. Low wheat stocks, compounded by repeated downward revisions of this years production forecast in major exporting countries, most notably in Australia, have kept wheat prices at elevated levels. In addition, stronger trade activity in the early months of the season and developments in currency markets, also provided support. The current high prices have been accompanied by extreme volatility (refer to Special Feature on Agricultural Commodity Prices) mostly as a result of low world stocks and stretched export supplies. In October, the United States hard wheat (HRW, No. 2, f.o.b.) averaged US$352 per tonne, up US$100 per tonne from its already high level at the start of the season and 60 percent more than last year. Recent weeks witnessed increases also in wheat export prices from other major origins.

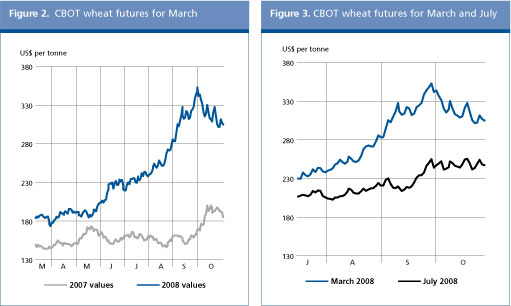

The wheat futures prices for December delivery on the Chicago Board of Trade (CBOT) hit a record of US$350 per tonne on 28 September, mainly in reaction to a further reduction of the forecast for this years Australian crop and the strong pace of export sales from the United States. However, by late October, wheat futures lost some of their earlier gains with prices for March 2008 delivery at the CBOT down to US$299 per tonne, albeit still 60 percent more than in the corresponding period last year. Most prices for nearby delivery remain high but favourable growing conditions in Argentina and generally higher winter plantings, helped also by the suspension of the 10 percent set-aside in the European Union, are likely to improve the supply situation in the coming months and result in lower prices by the middle of next year. In fact, wheat futures for July 2008 delivery are currently quoted at US$248 per tonne, already well below the delivery prices for December 2007 and even March 2008.

Table 2. World wheat market at a glance

FAOs latest forecast for world wheat output in 2007 stands at 602 million tonnes, significantly below earlier expectations and representing an increase of just 1 percent from 2006. The forecast has been reduced since June on account of poorer results than earlier expected in some northern hemisphere countries and the deterioration of prospects for the seasons still to be concluded in the southern hemisphere. Of the crops already harvested, the largest deviation from expectation has been in Europe, where the latest estimates point to a 1.3 percent decline in production, contrasting with the early season prospect of a sizeable increase. The worst losses were encountered in the eastern parts of the region where several weeks of exceptionally hot and dry weather severely compromised yields. However, in some major producing northern countries, a combination of early summer dryness followed by excessively wet conditions also led to poorer results than earlier forecast. In North America, a downward revision has also been made in the latest estimate of this years output in the United States; although the harvest is still good and sharply up from the previous year. A more substantial downward revision was made for Canada, where hot and dry conditions compounded the impact of reduced area. The latest estimate of the aggregate 2007 wheat output in Asia points to a good performance of the sector, exceeding that of last year despite a slight downward revision for Pakistan where, nevertheless, a bumper crop was harvested. Elsewhere in the northern hemisphere, drought devastated this years wheat crop in Morocco. Despite about-average harvests elsewhere in North Africa, the subregions aggregate output is sharply down from last year as well as from the average of the past five years. In the southern hemisphere, the bulk of the major 2007 wheat crops is yet to be harvested between now and the end of the year. In South America, aggregate output is forecast to increase by over 10 percent from 2006, with a recovery in Brazil, and contrary to earlier expectations, also a small increase now envisaged for Argentina. In Oceania, prospects for the wheat crop in Australia have deteriorated significantly over the growing season because of hot and dry weather, which set-in after planting in the major producing areas. Forecasts now point to a production level that is less than half of the amount expected at planting time.

In many parts of the northern hemisphere the winter wheat crops for harvest in 2008 are already being planted, and with world wheat prices at high levels, a significant expansion in area is expected. In North America, conditions have been generally favourable in the United States and all indications point to a record area. Although no official decision has been made regarding an early release of land from the Conservation Reserve Programme (CRP), contracts on some 800 000 hectares of land have already reached their normal expiration date and therefore could be put back into production over the new season. In Canada, a significant increase in the relatively small winter wheat crop area has been reported, and early indications already point to a substantial increase in the main spring plantings next year, reversing the significant shift to oilseeds in 2007. In Europe, weather permitting, a large increase in the winter wheat area is also likely. The European Union suspension of its 10 percent obligatory set-aside requirement for the 2007/08 season could bring an estimated 3 million hectares of arable land back into production. Early indications from the large producing areas in eastern Europe also suggest that farmers intend to plant larger wheat areas if weather and inputs allow.

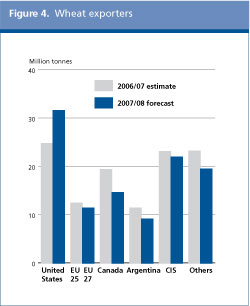

World trade in wheat in 2007/08 (July/June) is forecast to reach 107.5 million tonnes, down 6 million tonnes from the estimated record volume in 2006/07 and 1.5 million tonnes lower than FAOs first 2007/08 forecast published in the June report. The reductions from the previous season as well as the cut in the forecast are primarily driven by the anticipated sharp decline in wheat imports by India. After importing a record 6.7 million tonnes of wheat in 2006/07, India is forecast to purchase no more than 2 million tonnes from world markets this season, against the initial forecast of 3 million tonnes. The surge in this seasons world prices coupled with improvements in Indias own supply situation, following a strong rebound in production and more comfortable inventory levels, are the reasons for anticipating smaller imports in 2007/08. In October, India also announced a ban on exports of wheat flour while prolonging the ban on wheat exports, already in place since February. On the eve of the new sowing season, the Government also decided to increase the price it pays farmers (the minimum support price) by nearly 18 percent (to 1 000 rupees per 100 kg) to further boost plantings. Among other countries in Asia, wheat purchases by Indonesia are expected to decline significantly by 600 000 tonnes, due to high world prices and reduced supplies in Australia, its main supplier. In contrast, several Asian countries are expected to increase their imports. Most notably, Pakistan, where imports are expected to increase by at least 500 000 tonnes from the previous season, to nearly 1 million tonnes. The Government is also reported to provide PRs 12 billion (around US$198 million) in subsidies on imported wheat to reduce the impact of high world prices. Larger imports are also anticipated for Bangladesh and Yemen, mainly to keep prices under control. Bangladesh suspended a 5 percent import duty on wheat in March to stimulate private imports. In September, Yemen signed a new bilateral agreement with Syria for imports of wheat from that country, which for this season stands at 50 000 tonnes. Slightly higher imports are forecast for China1/ where, based on recent reports, the Government wheat procurement under its minimum purchase programme is down 30 percent from the previous season, at nearly 29 million tonnes. Imports by the Taiwan Province are likely to remain stable following the decision to halve the import tariff on wheat and wheat flour, to 3.25 and 8.75 percent respectively. Total wheat imports in Africa are forecast to increase mainly due to larger needs in Egypt and Morocco. In Egypt, this years small decline in production and the rise in consumption are expected to result in at least 7.5 million tonnes imports, 500 000 tonnes more than in the previous season. To curb the impact of rising world prices, in September the Government also increased its subsidies for bread by almost 52 percent, to 3.7 billion Egyptian Pounds (roughly US$2.47 billion). Imports by drought-stricken Morocco, where production this year fell by 76 percent, are forecast to double to 3.5 million tonnes. In August, the country announced the suspension of customs duties on wheat imports in order to lessen the impact of rising world prices on domestic consumers. As a result of a decline in production, imports by South Africa are also forecast to increase sharply by over 60 percent to 1.3 million tonnes this season. Imports by most countries in Central America are expected to remain unchanged from the previous season. The largest importer, Mexico, is forecast to purchase slightly less wheat from world markets this season due to higher domestic production. In South America, imports by Brazil, the worlds second largest importer after Egypt, are forecast to decline by 1 million tonnes from the previous season to 6.5 million tonnes. This mostly reflects a strong rebound in production from last years poor harvest. Imports by most countries in Europe are likely to remain stable at the previous seasons levels. In the European Union, imports are expected to remain large, at around 6.5 million tonnes, as domestic supplies remain tight, especially for feed. Reflecting the need to ease imports into the European Union, in early October the European Union Commission proposed a temporary suspension of import duties on all grains until June 2008, equivalent to 66.37 per tonne import levy for medium and low quality wheat. The Commission proposal also includes a removal of tariff-rate quotas currently in place for wheat and barley. As high prices already indicate, this seasons export supplies are proving exceptionally tight. Several exporting countries have less to export because of production shortfalls. Even in those instances where harvests and domestic supplies have been favourable, some are limiting exports fearing a rise in domestic prices if too much of their supplies were sold abroad. Among the major exporters, only the United States is forecast to increase its wheat shipments this season. Total exports by the United States are forecast to increase by nearly 7 million tonnes, or 28 percent, which would to some extent compensate reductions in export sales by other exporters. The increase in exports in the United States would be made possible by a strong rebound in domestic wheat production as well as a sharp drawdown on stocks. As of October, that is four months into the season, export sales from the United States already reached 84 percent of the current forecast for the full season. This rapid pace in sales was also driven by a falling US dollar, which made supplies from the United States particularly competitive. The deterioration of crop conditions in Australia, as a result of the prolonged drought, is now expected to curb their exports to no more than 10 million tonnes. This would be at least 1 million tonnes below the previous season, when Australia suffered its worst drought in 100 years, and at least 5 million tonnes below the average annual export level from Australia in previous years. Exports from Argentina are likely to decline by 2 million tonnes to no more than 9 million tonnes on a July/June basis, as the Government has halted export registration for wheat and wheat flour (as well as for several other commodities) since March in response to rising domestic flour and bread prices, on the one hand, and the fast pace in export declarations on the other. By March, the declared export commitments had reached nearly 8.7 million tonnes, of which almost 3.5 million tonnes were destined to Brazil. However, with the new harvests approaching and given the improvements in this years crop prospects, Argentina is expected to resume exports soon. Wheat exports from Canada are forecast to decline by almost 5 million tonnes this season. This would be the lowest level in five years driven mainly by a sharp drop in this years production and very low carryover stocks. In the EU-27, a rundown of inventory levels and a reduction in this years production, mostly driven by unfavourable climatic conditions during the decisive growing months in spring, are expected to result in wheat exports of only 11 million tonnes. This compares to already low exports of just over 12 million tonnes in the previous season from the EU-25. Export supplies in most other exporting countries are also generally hampered by lower production and rising domestic prices. Turkey is forecast to halve its exports to 1 million tonnes, as a result of a severe drought. Also because of drought, exports from Syria are forecast to decline sharply from the previous seasons peak of 1.5 million tonnes to only 300 000 tonnes. According to the Government, most of this years sales to Egypt, Jordan, and Yemen (Syrias main markets) are likely to be drawn from its strategic reserves.

Among the Commonwealth of Independent States (CIS) countries, wheat exports from t he Russian Federation, which has harvested larger crops this year, are expected to match those of last season at around 11 million tonnes. Driven by large export sales during July-September, domestic prices have risen and, in response, the Government is reported to be considering an increase in the current 10 percent tariff on wheat exports. Moreover, large exports amid rising domestic prices have led the Government to announce in October a possible establishment of a state-run corporation, in order to enhance its control over the overall supply situation, especially with regard to exports. Similarly, in Kazakhstan, in spite of another bumper crop this year, exports are likely to remain unchanged, at around 8.5 million tonnes. Also confronted with rising domestic prices, the Government in early October announced that domestic exporters would have to sell 20 percent of their exports on the domestic market. Due to a production shortfall for the second consecutive year and low stocks, Ukraine has imposed prohibitive export quotas since the beginning of the season, recently extended to March 2008. This is expected to limit exports for the season to no more than 1.5 million tonnes; about one-half of the already sharply reduced level in 2006/07.

Global wheat utilization is forecast to reach 619 million tonnes in 2007/08, down marginally (0.4 percent), from the estimated total use level in 2006/07. Tight supplies and high prices are expected to drive down feed utilization of wheat by over 4 million tonnes, or 3.7 percent, to 107 million tonnes, the lowest level since 2003/04. The forecast decline in the use of wheat for animal feed is mostly concentrated in several CIS countries as well as in Australia, Canada and the European Union. Total food consumption of wheat is forecast to reach 448 million tonnes, up by only 4 million tonnes, or just below 1 percent, from 2006/07. As this is less than the anticipated growth in world population, world wheat consumption, on a per caput basis, would also decline slightly, from 68 kg in 2006/07 to 67.8 kg in 2007/08. The high prices, which have caused this situation, this year are expected to reduce consumption, especially among the low income countries. Among all the regions, the negative impact of high prices is expected to be most pronounced in Africa, where several countries are likely to cut their wheat utilization by more than 1 kg. Rising prices are also affecting richer countries such as Japan, the Russian Federation and many countries in Europe. Bread prices in Japan have gone up for the first time in more than two decades. In Japan, the Government is the sole importer of wheat so the recent decision by the Government to increase the price of the imported wheat it sells to millers by 10 percent is seen as the main reason for the recent increases in prices for bread and other wheat products.

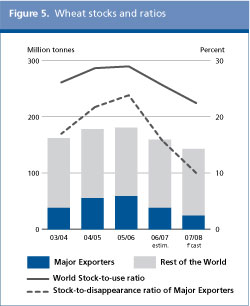

World wheat stocks by the close of the crop seasons in 2008 are forecast to exceed 142 million tonnes, 17 million tonnes, or 10 percent, below the already low opening levels and the smallest since 1982. At this level, world wheat stocks-to-use ratio is forecast to reach 22.5 percent; again below the reduced level in 2006/07 and the lowest since the early 1980s. The drawdown of wheat reserves for the second consecutive season reflects a continuation of strong demand amid insufficient increases in world production. The drawdown is expected to be most pronounced among the major exporting countries, which are also among the leading stock holders. Total wheat stocks held by major exporters are forecast to fall to 25 million tonnes, down around 14 million tonnes from their opening levels. At this level, the ratio of the major exporters stocks-to-disappearance (defined as their anticipated exports plus domestic consumption) would stand at a historical low of only 10 percent. The drop in stocks is expected to prove most significant in the case of Australia, which is suffering from a prolonged drought for the second consecutive year. Reduced inventories are also forecast for Argentina, Canada and the European Union. In spite of a sharp rebound in its production, stocks in the United States would still fall significantly in order to sustain increased export this season. As a result, ending stocks in the United States are forecast at roughly 8 million tonnes, the smallest in more than three decades and 2 million tonnes below the previous low registered in the mid-1990s. At this level, the stocks-to-use ratio in the United States would stand at around 29 percent, the lowest in more than three decades, while its stocks-to-disappearance ratio, would barely exceed 13 percent, the lowest since 1990.

Among other countries, inventories are anticipated to increase in only a few cases, notably in India, sustained by a rise in this years production and large imports before the start of the season, and in China, following a 2.5 percent expansion in domestic production from the previous season. However, sharply lower stocks are forecast for several countries, especially Egypt, Iraq, Kazakhstan, Morocco, the Republic of Serbia and Turkey. Serbia signed a protocol in October with Bosnia and Herzegovina on strengthening cooperation between the two countries with regard to their respective trade and stock policies. Following this years drought reduced production, which has driven down grain stocks, Serbia has agreed to provide its stockpile facilities to Bosnia and the two countries will also cooperate with each other on their procurement activities instead of extending the current imposition of export quotas on wheat and maize. 1. All subsequent references to China also refer to Mainland China, unless otherwise specified. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |