November 2007 November 2007 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

SUGAR

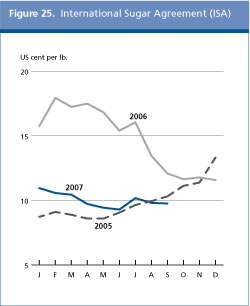

The prospect of a consecutive sugar surplus for 2007/08 weakens international sugar prices World sugar prices fell to United States 9.29 cents per pound in June 2007 which is nearly 52 percent less than the 25-year highs reached in early 2006. After recovering to United States 10.17 cents per pound in July, prices declined to United States 9.81 cents per pound in August and to United States 9.76 cents per pound in September, resulting in a price average for the first nine months (January-September) of 2007 of United States 10.01 cents per pound1/; 37 percent lower than the corresponding price average in 2006. Ample supplies in exporting countries, particularly the return of India from a net importer to a net sugar exporter after two consecutive years of production setbacks, were the key factor behind the price decline. There is a general consensus that the sugar sector over-reacted to the high prices of last year and expanded too much crop area and processing capacity, triggering the price slump The price outlook for 2007/08 has been dimmed by preliminary estimates that indicate world sugar production could surpass consumption by as much as 12 million tonnes, for the second consecutive season. Market price development over the next few months will most likely depend on the actual size of the production surplus in major exporting countries and the expected build up of sugar inventories in consuming countries.

Could sugar prices fall below their current levels? In the midst of this generally negative prospect, there are a few factors that could work to mitigate the price decline. First, at present levels, international sugar prices are too low to cover costs in all major producing countries, with the exception of Brazil. The weakness of the US dollar against the currencies of several exporting countries has accentuated the decline of prices, when expressed in national currencies, to unsustainable levels. India, for instance, has already announced that it will not be exporting sugar below United States 10 cents per pound, a move that would sustain somewhat world prices, despite the large global surplus. Second, as oil prices hit new highs, Brazil, the largest sugar exporter, is expected to process more sugar cane into ethanol, because of better returns, and less into sugar. This shift would remove large quantities of sugar from the world market and hence reduce the downward pressure on prices. Brazil has already announced that, as of 1 September, sugar production in the centre south parts of its territory was down 8.8 percent on the year, while ethanol output rose by 12.6 percent. Finally, rising maize prices raises the production cost of HFCS (high fructose corn syrup), which encourages the use of alternative sweeteners such as sugar. Both sugar and HFCS compete in the sweetener market, but due to the current sugar price advantage over HFCS, the food and beverage industry is expected to substitute more sugar for maize-based sweeteners. All this nurture the belief that despite an easy supply/demand balance, there are some forces of relative support to the global sugar market. These factors are likely to be insufficient to reverse the price decline, especially if crude oil prices drop significantly and the global sugar market imbalance is further exacerbated by greater than expected surplus for the 2007/08 season.

Global sugar production to expand further in 2007/08 World sugar production in 2007/08 (October/September) is estimated by FAO to reach 169 million tonnes (raw sugar equivalent), 2.7 percent more than in the previous year, and about 12 million tonnes higher than the projected world sugar consumption of 157 million tonnes. Virtually all of the growth in output would stem from developing countries, which are forecast to produce 128.5 million tonnes, up from 124.3 million tonnes in 2006/07, led by a record harvest in India. Total production in developed countries is forecast at 40.5 million tonnes, 0.7 percent more than in the previous year, reflecting increases in Australia and the United States. In the Latin American and Caribbeanregion, Brazil is set to produce 32.2 million tonnes in 2007/08, relatively unchanged from 2006/07. This is despite a record level cane harvest, following relatively favourable weather conditions, which boosted yields. Indeed, it is estimated that between 54 and 55 percent of Brazils 2007/08 sugar-cane harvest will be converted into ethanol rather than into sugar. In Mexico, sugar production is forecast at 5.7 million tonnes, a 5.1 percent rise over 2006/07 season that was affected by poor weather in the major producing state of Veracruz. Expectation of growth in 2007/08 reflects a slight increase in planted area and assumes a return to average growing conditions. The challenge facing Mexicos sugar industry is the total liberalization of the sweeteners market with the United States by January 2008, under the North American Free Trade Agreement (NAFTA). Sugar production is expected to be higher in Argentina, as a result of increases in crop plantings and milling capacity, helped by the peso devaluation and attractive sugar returns in 2006. Sugar output is also to expand in Colombia, Ecuador, Guatemala and Peru, while it is anticipated to fall in Cuba, due to foreseen adverse growing conditions. Aggregate sugar production in Africa may reach 10.6 million tonnes in 2007/08, 125 000 tonnes or 1.2 percent above the previous year. While a strong growth is anticipated in South Africa, production may fall in Kenya and Mauritius. In Egypt, production is forecast at 1.8 million tonnes, slightly greater than in 2006/07, with the beet harvest accounting for the bulk of the increase. The Government is keen on promoting beet instead of cane production to mitigate the challenges posed by scarce water and land resources. After two years of extreme drought, sugar production in Swaziland is expected to recover only marginally over last seasons level, due to less than ideal growing conditions. Increases are also forecast for 2007/08 in Mozambique, the Sudan and the United Republic of Tanzania, fuelled by rising expansion plans in anticipation of free access to the European Union market by 2009, under the Everything but Arms (EBA) initiative. Production in Ethiopia is forecast at 360 000 tonnes, relatively unchanged from 2006/07, but the sector may benefit from renewed institutional support. The Government has announced plans to expand sugar production by five fold to 1.52 million tonnes by 2012/13. Sugar output is set to fall in Kenya, as a result of structural difficulties and adverse weather conditions. Domestic production may be further disrupted with the expiration of the safeguard measures provision under the Comesa (Common market for eastern and southern Africa) in 2008, the lifting of which will give full market access to more efficient sugar producing Comesa member countries, such as the Sudan. Table 7. World production and consumption of sugar

Source: FAO

Estimated production in Asia now stands at 68.5 million tonnes for 2007/08, 6.6 percent higher than the 2006/07 level, mainly reflecting strong gains in India, China, and Thailand. In 2007/08, India is expected to surpass Brazil as the largest sugar producer in the world. The anticipated 9.5 percent growth this season comes after the increase recorded over 2006/07 season, when the monsoons provided ample rainfall in the cane growing areas of Karnataka, Gujarat and Uttar Pradesh, the main producing regions. Assuming normal weather conditions, sugar production is expected to reach 32.4 million tonnes in 2007/08 as high cane prices and institutional support from both state and federal governments encouraged cane planting to expand by 200 000 hectares to 4.7 million hectares. In China, production is forecast to reach 13 million tonnes, about 700 000 tonnes more than in the previous year, largely due to better weather conditions and remunerative prices. In Thailand, sugar output is forecast at 7.5 million tonnes, an increase of about 6.8 percent from 2006/07, following a substantial increase in cane plantings. An expansion is also foreseen for Indonesia, Pakistan and Turkey. In Europe, sugar output in the EU-27 is forecast to fall to 16.8 million tonnes, still exceeding by about 0.2 million tonnes the revised production quota for 2007/08. The European Union aims at reducing sugar production by 6 million tonnes over the four years of the restructuring programme. Production is forecast to increase in the Russian Federation, driven by an expansion in beet area and improved crop husbandry practices, while it may fall in Azerbaijan, Belarus and Ukraine. In the rest of the world, sugar production in the United States is forecast to be slightly higher than in 2006/07, reflecting a return to normal growing conditions after hurricane damaged crops in Florida and Louisiana in 2006/07. Similarly, production in Australia is expected to recover from drought and cyclones experienced in 2006/07.

Global sugar consumption in 2007/08 is forecast at 157 million tonnes, 3.5 million tonnes more than in 2006/07, reflecting increases in Asia and in Latin America and the Caribbean . On average, this would raise global per caput availability from 23.5 kg in 2006/07 to 23.8 kg in 2007/08. Current low prices are expected to stimulate some additional demand and also induce some substitution from HFCS to sugar, given high maize prices. Sugar consumption in developing countries is estimated to grow by 2.9 percent to 107.6 million tonnes, sustained by per caput income and population growth. Sugar consumption in China is set to reach 13.5 million tonnes, up 3.7 percent from 2006/07, influenced by a continued expansion of sugar use in the food and beverages industries. Similarly, year-on-year offtake is expected to increase in India, boosted by low prices. Sugar consumption is also expected to rise in Latin America and the Caribbean where it may reach 27.9 million tonnes, up 2.9 percent from 2006/07. Most of the growth will be accounted for by Brazil and Mexico where utilization is estimated at 11.4 million tonnes and 5.6 million tonnes, respectively. Year-on-year sugar offtake is foreseen relatively stable in developed countries, particularly in the European Union, the Republic of Korea and the United States. Growth rates in these markets are limited given already high per caput usage, of nearly 36 kg, slow population growth and dietary concerns.

World sugar trade is forecast to reach 45.4 million tonnes in 2007/08 (October/September), slightly lower than estimated for 2006/07. Trade prospects are highly tentative at this stage as there are still many uncertainties regarding the final outcome of the 2007/08 production cycle. However, the expected slowdown in trade would reflect weaker import demand following rising production in traditional importing countries. In Europe, imports by the Russian Federation, the worlds largest sugar importer, are set to decline by as much as 1.7 percent to 3.5 million tonnes, because a much higher seasonal import duty of US$240 is to be introduced in 2008. Purchases by Belarus and Ukraine are also foreseen to drop, mainly on account of large stock availability, while overall imports to the EU-27 are forecast at 3.2 million tonnes, virtually the same level as imported in 2006/07 by the EU-25. In Asia, due to generally positive production outcome, sugar deliveries to China are expected to decline to 1.2 million tonnes, compared with 2.1 million tonnes in 2006/07. Similarly, shipments to Pakistan and the Republic of Korea are forecast to contract, while those to Indonesia and Malaysia may increase. In the rest of the world, deliveries to the United States are set at 1.9 million tonnes, 135 000 tonnes higher than the previous season, while imports by Africa are projected to expand further on account of strong domestic demand. The depreciation of the US dollar against some local currencies could stimulate imports to the continent as well. Due to larger output in exporting countries, export availabilities are expected to be ample in 2007/08. Competition however, among exporters is likely to be fierce in the light of the weak expected demand by traditional importing countries. In Latin America and the Caribbean, Brazil, the worlds largest exporter, is expected to ship 20.8 million tonnes, about 2.6 percent more than in 2006/07. In Asia, overall exports are foreseen to surpass 13.4 million tonnes, up 37 percent from last year. In India, exports could reach 4.5 million tonnes, driven by ample supply and the recent Government decision to lift all controls on sugar trade, including a ban on export. Strong domestic production may also foster increases in sales by Thailand, with shipments set to reach 4.8 million tonnes, mostly directed to markets in Asia. Given the soaring freights rates, the pattern of trade this year is indeed expected to be very much influenced by the distance between supplier and import markets. 1. US$221 per tonne 2. Sugar production figures refer to centrifugal sugar derived from sugar cane or beet, expressed in raw equivalents. Data relate to the October/September season. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |