![]()

![]()

![]()

ECONOMIC OVERVIEW

SELECTED ISSUES

The economic outlook and prospects for agriculture

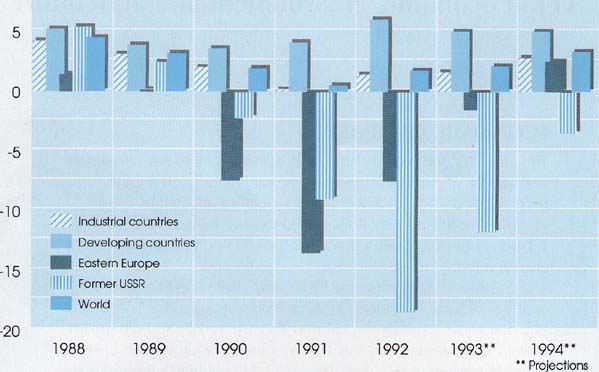

The global economic downturn that started in 1990 has continued into 1993 and prospects for recovery in the near term appear particularly uncertain. After having virtually stagnated in 1991, world economic activity is estimated to have increased by only 1.7 percent in 1992 while forecasts for 1993 point to a 2.2 percent growth rate.1

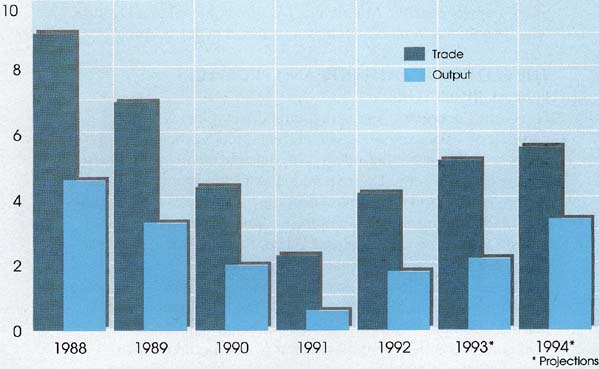

1 Unless otherwise indicated, estimates and forecasts in this section are from IMF. World Economic Outlook, April 1993.The General Agreement on Tariffs and Trade (GATT) estimates world merchandise trade in 1992 to have expanded by 5.5 percent in value and 4.5 percent in volume, the first acceleration in growth since 1988. Current forecasts for 1993 are for trade growth of more than 4.5 percent in volume, although a downside risk is recognized for trade performance.2 In any event, the relatively brisk expansion in world trade is seen as a bright spot in an economic environment that is otherwise characterized by depressed growth and uncertain prospects. Economic growth in the industrial countries, which account for three-quarters of world output, is currently estimated by the Organisation for Economic Cooperation and Development (OECD) to be a mere 1.2 percent in 1993, below the already depressed growth levels of the previous year.

2 GATT world trade estimates are somewhat different from those of the IMF.. According to the IMF, the volume of world trade in 1992 expanded by 4.2 percent and forecasts for 1993 point to a 5.2 percent growth.European countries are facing a particularly difficult situation: economic recession (oddly combined with high real interest rates); high and rising levels of unemployment; widening fiscal deficits; and financial and currency instability which is seriously straining the exchange rate mechanism (ERM) of the EEC and adding to the difficulties of achieving Maastricht objectives.

Japan's growth expectations for 1993 are barely of the order of 1 percent, but recent indications suggest that stimulative fiscal and monetary measures may help recovery to take hold in 1994. With Western Europe and Japan loosing momentum as global growth poles, the United States appears to offer the best prospects for stimulating the world economy in the short and medium term. United States economic growth in 1993 was forecast by the OECD to be 2.6 percent, below previous expectations but still more than twice the average growth for the OECD area. Recovery appears to be gaining momentum although major uncertainties remain, particularly with regard to the large federal budget deficit and the effectiveness of measures to reduce it.

Figure 1 WORLD ECONOMIC OUTPUT* (Percentage change over preceding year)

* Real GDP or real NMPFigure 1 ECONOMIC GROWTH, DEVELOPING COUNTRY REGIONS (Percentage change over preceding year)

Source: IMF

Among the former centrally planned economies, the Czech Republic, Poland and Hungary are showing signs of recovery and reduced inflationary pressure, but they still face difficulties in containing fiscal deficits. The Baltic states are also showing encouraging progress in growth and stabilization.

On the other hand, the process of economic restructuring is encountering major obstacles in most other countries in the former USSR. After catastrophic output losses in the previous two years, real GDP in the former USSR is expected to decline sharply again in 1993. Underlying these dismal performances are extremely high rates of inflation, a collapse of trade flows within and outside the area, inability to compress the fiscal deficit and uncertainties over the process of transformation itself.

Figure 2 WORLD OUTPUT AND VOLUME OF WORLD TRADE (Percentage change over preceding year)

Source: IMF

In marked contrast with the depressed economic performances of developed countries and economies in transition, developing countries as a whole showed robust growth in 1992 (about 6 percent) and are expected to continue growing at a relatively fast, although somewhat slower, rate in 1993. There were wide regional differences, however, and the overall strong growth of developing countries mainly reflected the performances of relatively few dynamic economies. The best performers were again Far East countries, particularly those in eastern Asia. China emerged as possibly the fastest-growing economy in the world, with its production, investment and exports shooting up in 1992 and 1993 - but with growing concern about inflationary pressure. Economic activity also remained reasonably buoyant in Latin America and the Caribbean, a major exception being the Brazilian economy which is crippled by stagflation and a budget deficit representing 40 percent of GDP. Finally, Africa was badly affected by conflicts, drought in southern countries and depressed prices for several of the region's main export products in 1992; an improvement in terms of trade and return to normal weather conditions in southern Africa are expected to strengthen growth somewhat in 1993 (see Part II, Regional review, Sub-Saharan Africa). The darkest side of the global economic picture is the large number of poor countries that continue to see their situation worsen. According to the United Nations Conference on Trade and Development (UNCTAD) the 47 least-developed countries (LDCs) are expected to record a fourth straight year of economic decline in 1993. Only a few of these countries will have avoided the negative trend, namely Malawi, Mauritania, Myanmar, Nepal and Uganda, which benefited in particular from expanded export earnings.

Prospects for developing countries' agriculture

Prospects for economies heavily dependent on agricultural trade

Forecasting economic and agricultural developments is a particularly risky exercise, given current circumstances. A number of events that are still unfolding have introduced an unusually high degree of uncertainty. These include the transformation process in Eastern Europe and the former USSR; the outcome of the Uruguay Round; the timing and extent of the economic recovery in the industrial world; and the unresolved conflicts in Africa, the Near East, the Balkans and other parts of the world.

With all the caution imposed by such uncertainties, most forecasts - in particular those of the World Bank, the IMF and the LINK project - point to the following developments for 1994-95:

· Economic activity in the industrial world should recover somewhat in 1994 and further in 1995, although growth rates will probably remain below 3 percent. The United States is likely to be the main driving force in the recovery.One remarkable feature in these forecasts is that developing countries would continue outpacing the developed countries in growth. It may be generally observed, however, that: i) the dynamism of developing countries' economies would be narrowly based, being chiefly accounted for by East Asian countries (mainly China) and liberalizing countries at an early and still uncertain stage of recovery, mainly in Latin America and the Caribbean; ii) although the growth rate differentials imply some narrowing in the economic gap between industrial and developing countries, the gap remains vast. Average per caput income levels in OECD countries are currently about three times higher than those of the richest developing countries. Even the highest-income and fastest-growing developing countries still have to make up a large difference in per caput income levels3 and, in order to do so, in factor productivity; iii) the North/South growth differential must be seen as a transitory phenomenon rather than a sign of lesser economic interdependence. Indeed, the recent home-based recovery of many developing countries is unlikely to be sustained in the absence of more trade and investment impulses from the industrial world.· Central Europe's economies in transition may resume positive growth in 1994; those in the former USSR are unlikely to do so before 1995 or even later.

· Economic growth in the developing countries as a whole should continue outpacing that in the industrial world, at rates between 5 and 6 percent. The fastest-growing economies should continue to be in East Asia (6 to 7 percent), with China gradually emerging as a "fourth pole" of world growth. Several adjusting countries in Latin America and the Caribbean should consolidate recovery, bringing the region's growth to 5 to 6 percent. At 3 to 4 percent, Africa's economic growth should show some pickup; however, this growth would remain well below the developing country mean and gains would be meagre in per caput terms. Growth in the Near East would slow from the very high rates of 1992, although growth would continue to exceed the rate of past trends.

3 The World Bank estimates that, should China's economy continue growing in the 7 to 8 percent range throughout the 1990s, the size of its GDP by 2002 would be approaching that of the United States. However, China's per caput income would remain about one-fifth that of the United States.

|

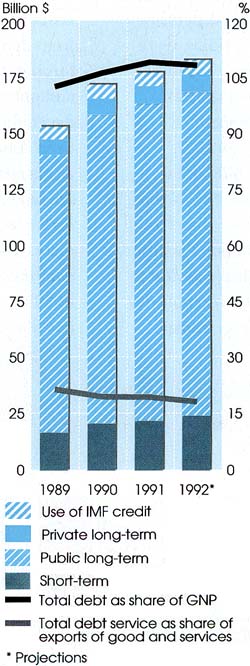

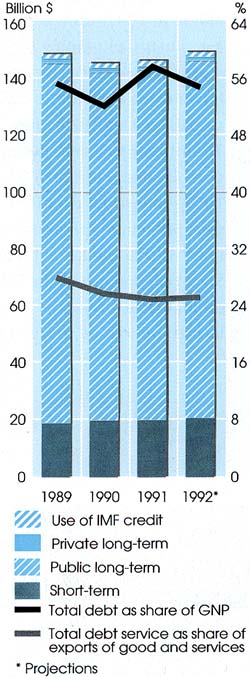

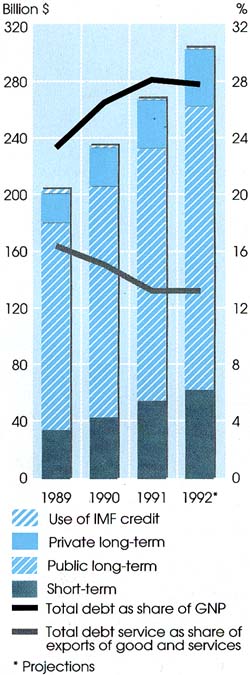

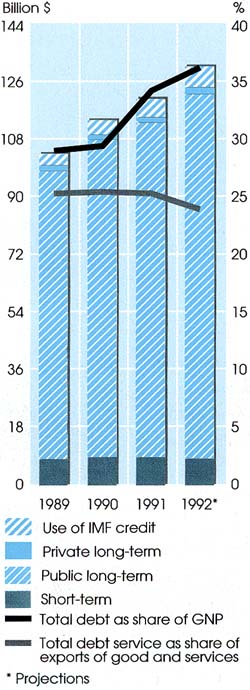

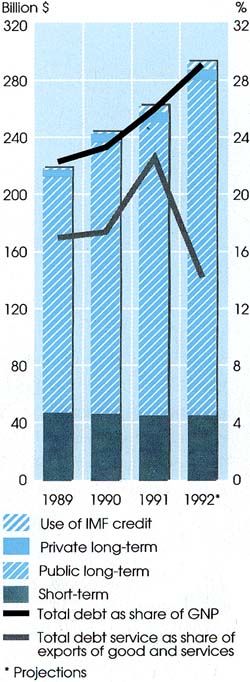

BOX 1 The total external debt of the 116 developing countries reporting to the World Bank's Debtor Reporting System (DRS), estimated to be $1 418 billion at end-1991, was projected to reach $1 510 billion in 1992. For all DRS countries, the debt-to-exports ratio in 1992 was estimated to be 178 percent, about the same as the previous year but much higher than in 1990, when it stood at 167 percent. Yet, from 21 percent in 1991, the ratio of debt service-to-exports is projected to decline slightly to 19 percent in 1992. The debt-to-GNP ratio is expected to remain almost unchanged in 1992 at 37 percent. Regional debt indicators varied widely, as shown in Figure 3. The debt situation in sub-Saharan Africa and Latin America and the Caribbean are discussed in the Regional review of this report. For the group of severely indebted low-income countries, the debt-to-GNP ratio stood at an estimated 113 percent in 1992, down from 117 percent in the previous year. The debt service-to-exports ratio was estimated to be 22 percent, the same level as in 1991. Developing countries' external debt originated from agriculture-related projects was estimated to be $72.2 billion in 1991, representing approximately 6 percent of these countries' total external debt. Overall, this share has remained fairly constant in past years, although variations between regions were significant. These ranged from 4 percent in Latin America and the Caribbean to 8 to 10 percent in the Near East, sub-Saharan Africa and East Asia and 15 percent in South Asia. The low share of agriculture in total debt reflects the fact that external finance to the sector, chiefly provided by official sources, is highly concessional. Net transfers (net flows minus interest payments) related to all debts, which reached a negative $16 billion in 1991, are projected to decrease to negative $3.6 billion in 1992. The long-term component of such transfers, which were a negative $23 billion in 1991, were expected to turn slightly positive in 1992, with negative net transfers to private creditors falling from $27 billion in 1991 to $7 billion in 1992. This was partly due to larger disbursements by private creditors, which rose from $70 billion in 1991 to $84 billion in 1992. Debt reduction operations were estimated to have reduced the debt of all developing countries by $13 billion in 1992, against $9 billion in 1991. Official debt forgiveness accounted for about $6.5 billion. The reduction in private debt was done mainly through officially sponsored operations. Those under the Brady Plan reduced debt by $4.7 billion, market buy-back by $7.9 billion and debt-equity swaps by $1 billion. The Paris Club of developed creditor countries negotiated special agreements under the Houston terms1 with severely indebted lower-middle-income countries, consolidating more than $5 billion in 1992. Conventional restructuring agreements amounting to $13 billion were also negotiated. Twelve severely indebted low-income countries obtained special concessions under the new "enhanced Toronto terms"2 and, during 1992, consolidated more than $2.5 billion. In 1992, only seven countries benefited from debt reduction operations under the "IDA only" World Bank Debt Reduction Facility. Such reduced use of the Facility was due to difficulties experienced by debtor countries in carrying out adjustment programmes. 1 The Houston terms are longer terms of repayment granted by the Paris Club for countries that have a strong adjustment programme and have performed well under previous Paris agreements. These were decided as a follow-up to the July 1990 Houston economic summit.An important financial development in 1992 was the increase in private capital flows to developing countries and the shift from debt to equity financing, particularly through foreign direct investment (FDI) and portfolio equity investment. This development affected more particularly Latin America and the Caribbean and is discussed in the Regional review of this document. Only a few low-income countries have benefited from the increased FDI flows. This group of countries received an estimated $9 billion in 1992, of which $5 billion were invested in China alone. |

Figure 3 COMPOSITION OF DEBT - SUB-SAHARAN AFRICA

Figure 3 COMPOSITION OF DEBT - NEAR EAST AND NORTH AFRICA

Figure 3 COMPOSITION OF DEBT - EAST ASIA AND THE PACIFIC

Figure 3 COMPOSITION OF DEBT - SOUTH ASIA

Figure 3 COMPOSITION OF DEBT - EUROPE AND CENTRAL ASIA**

TABLE 1

Projected growth in agricultural value added, exports and imports for developing regions

|

Region

|

Agricultural value added |

Agricultural exports |

Agricultural imports |

|||

|

1993 |

1994 |

1993 |

1994 |

1993 |

1994 |

|

|

(....................................................%.................................) |

||||||

|

Sub-Saharan Africa |

2.34 |

2.99 |

0.50 |

8.22 |

6.64 |

8.89 |

|

Latin America and Caribbean |

2.58 |

3.54 |

4.50 |

6.81 |

4.44 |

4.65 |

|

Far East and Pacific |

4.98 |

4.20 |

10.29 |

9.10 |

8.22 |

12.29 |

|

Near East and North Africa |

3.64 |

4.03 |

5.33 |

7.12 |

6.69 |

7.20 |

Short-term forecasts for developing countries' agricultural output and trade are shown in Table 1. The projections suggest that:

· The increase in agricultural value added in 1993-94 would be broadly in line with the average trend values of the 1980s, except in Latin America and the Caribbean where projected growth rates would significantly exceed past trends. Growth in agricultural value added would accelerate in 1994 in all regions except Asia and the Pacific, although agricultural growth in this region would remain strong.Two factors will crucially determine developing countries' growth and trade prospects for the sector: i) the extent of the overall economic recovery, which will affect domestic and international demand for agricultural products as well as agricultural supply through its impact on input costs and capital flows; and ii) largely related to the above, the future behaviour of commodity prices -with agricultural commodities accounting for about 10 percent of world trade but a far greater proportion of the export earnings of many developing countries.· Agricultural exports and imports would expand well above the 1980s and more recent trends. For sub-Saharan Africa, 1994 would be a year of strong recovery for agricultural exports. However, imports would expand at an even faster rate, causing the agricultural trade deficit recorded in this region to reach $12 billion in 1994 - nearly twice the deficit recorded in 1991. The agricultural trade deficit record would also increase in the Near East (to $15 billion in 1994, up from $12 billion in 1991).

· The agricultural trade surplus in Latin America and the Caribbean would expand moderately from $24 billion in 1991 to $26 billion in 1994, but that of Asia and the Pacific would fall from $4.9 billion to $2.5 billion during the same period.

As regards the first factor, the current uncertainty regarding the timing and strength of the global recovery makes it hard to assess the impact it will have on agriculture. Bearing in mind the past record of oversanguine forecasts of global recovery, it may be interesting to explore what might happen if, for instance, the recovery does not materialize in the near future. For a specific region, what would be the impact on agricultural exports, imports and total GDP of zero growth in the rest of the world? A simulation exercise can at least attempt to appraise the magnitude of such impacts, given these hypothetical scenarios. In this type of simulation exercise, of which the results for sub-Saharan Africa are summarized in Table 2, such impacts are estimated as percentage deviations from "baseline" projections.4

4 This simulation is based on an econometric model elaborated for FAO by Prof. George P. Zanias, Agricultural University of Athens.The figures indicate that regional agricultural exports in 1993 would expand by 0.5 percentage points less than the "baseline" growth estimate for that year; and by 1.5 percentage points less in 1994, assuming a second year of zero growth in the rest of the world.

In other words, using the baseline projections shown in Table 1, sub-Saharan Africa's agricultural exports would stagnate instead of growing by 0.5 percent in 1993 and would increase by 6.6 percent instead of 8.2 percent in 1994 - the difference between the latter two being about $1.41 billion in actual value terms. This amount is considerable in the African context. Converted at 1992 prices it would represent over 10 percent of sub-Saharan Africa's repayments on all debts, or roughly the total value of estimated FDI into the region that year.

Global economic stagnation would also affect the region's economic activity, which would grow by about 2.9 percent in 1994 instead of the 3.1 percent currently forecast by LINK. While such a loss does not appear dramatic, it represents the difference between catching up with population growth - currently 3.1 percent annually - and recording yet another decline in per caput output for the region.

TABLE 2

Sub-Saharan Africa:1 simulated effects of zero GDP growth on the rest of the world

|

Year |

Agricultural exports |

Non-agricultural exports |

Agricultural imports |

Non-agricultural imports |

GDP |

|

|

|

(............................... % changes over baseline

projections...........................) |

|||||

|

1993 |

-0.50 |

-0.64 |

-0.01 |

-0.04 |

-0.05 |

|

|

1994 |

-1.51 |

-2.06 |

-0.06 |

-0.13 |

-0.17 |

|

1 Excluding Nigeria.As regards commodity prices, most forecasts point to a firming of international quotations from their current, deeply depressed levels, reflecting some increase in demand as global recovery proceeds as well as reductions in supply caused by shifts away from primary production. Thus, the World Bank baseline forecasts predict some increase in food and beverage prices and a continuing long-term decline in the production of perennial crops, especially coffee and cocoa, where production costs often exceed world prices and new plantings have fallen.5

Source: FAO.

5 World Bank. 1993. Global Economic Prospects and the Developing Countries.Project LINK projections for 1994-95 indicate a strong upsurge in coffee and, to a lesser extent, cocoa prices, although this would be insufficient to offset the declines of the previous two years. On the other hand, prices of other commodities, including sugar, banana, beef, cotton and hard fibres, are expected to increase only slightly or, in some cases, even decline. Grain prices are likely to be depressed through and beyond 1993 while, according to FAO projections, a tightening of the global market is not likely until the mid-to late 1990s.

Note must be taken, however, of the high risks involved in commodity forecasting - as well known to market analysts as they are to speculators. Furthermore, while there appears to be a degree of consensus on the general price trends for several commodities, there is disagreement among analysts on the magnitude, and even direction, of forecast changes for several others.

Pursuing the approach introduced in The State of Food and Agriculture 1992, this section reviews the economic and agricultural prospects for two groups of selected developing countries: i) low-income food-deficit countries (LIFDCs) with the lowest capacity to finance food imports; and ii) economies highly dependent on agricultural exports (EDAEs). The countries classed in these groups are shown in Table 3A and 3B.

TABLE 3A

LIFDCs with the lowest capacity to finance food imports

|

Sub-Saharan Africa |

Latin America and Caribbean |

Far East and Pacific |

Near East and North Africa |

|

Cape Verde |

Haiti |

Samoa |

Egypt |

|

Gambia |

Nicaragua |

Bangladesh |

Yemen |

|

Lesotho |

Dominican Rep. |

Cambodia |

Sudan |

|

Djibouti |

|

Afghanistan |

|

|

Mozambique |

|

Nepal |

|

|

Guinea-Bissau |

|

Laos |

|

|

Somalia |

|

Sri Lanka |

|

|

Comoros |

|

Maldives |

|

|

Sierra Leone |

|

|

|

|

Ethiopia |

|

|

|

|

Burkina Faso |

|

|

|

|

Togo |

|

|

|

|

Senegal |

|

|

|

|

Benin |

|

|

|

|

Rwanda |

|

|

|

|

Mali |

|

|

|

|

Mauritania |

|

|

|

Note: The criteria for the definition of these groups are explained in The State of Food and Agriculture 7992.The analysis is based on macroeconomic estimates and short-term forecasts for the two groups of countries, prepared by the IMF for FAO, and on forecasts by the LINK project, prepared in association with FAO, for variables related to agriculture. The time horizon explored is 1993-94.

The broad trends emerging from the analysis confirm the general observations presented in The State of Food and Agriculture 1992, i.e. both country groups are forecast to share in the overall improvement of developing countries in general economic and agricultural performances.

TABLE 3B

Economies highly dependent on agricultural exports

|

Latin America and Caribbean |

Far East and Pacific |

Sub-Saharan Africa |

|

Argentina |

Sri Lanka |

Côte d'Ivoire |

|

Paraguay |

Thailand |

Malawi |

|

Honduras |

Afghanistan |

Zimbabwe |

|

Cuba |

Viet Nam |

Mali |

|

Uruguay |

Malaysia |

Sudan |

|

Brazil |

|

Madagascar |

|

Guatemala |

|

Burundi |

|

Costa Rica |

|

Cameroon |

|

Colombia |

|

Ghana |

|

Saint Vincent and |

|

Liberia |

|

the Grenadines |

|

Uganda |

|

Ecuador |

|

Kenya |

|

Guyana |

|

Ethiopia |

|

Belize |

|

Rwanda |

|

Dominica |

|

Swaziland |

|

Nicaragua |

|

Mauritius |

|

El Salvador |

|

Central African Rep. |

|

Dominican Rep. |

|

Tanzania, United Rep. |

|

Sao Tome and Principe |

|

Chad |

|

|

|

Burkina Faso |

|

|

|

Somalia |

|

|

|

Benin |

|

|

|

Guinea-Bissau |

|

|

|

Gambia |

Note: The criteria for the definition of these groups are explained in The State of Food and Agriculture 1992.However, the improvement for these two groups would be highly uneven and their average GDP growth would continue below that of developing countries as a whole. Beyond those general tendencies, the following salient features emerge from the 1993-94 forecasts:

LIFDCs with the lowest capacity to finance food imports.

· GDP growth would accelerate to about 4 percent in both years, with agricultural value added increasing at a slower pace.Economies heavily dependent on agricultural exports.· Merchandise imports would expand strongly from the deeply depressed levels of 1991 -92. Agricultural imports would also expand significantly, outpacing other merchandise imports in the African countries of this group.

· Agricultural export growth would lag behind that of food imports, so the agricultural trade deficit would more than double from the level of 1991-92.6

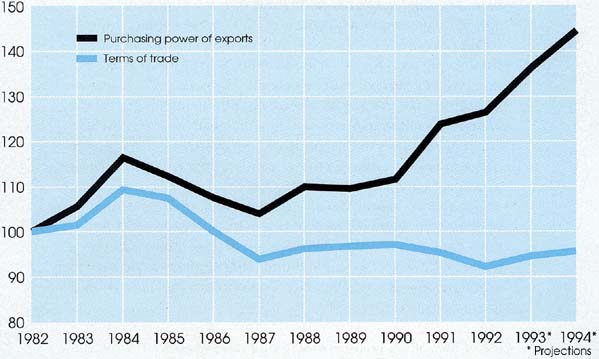

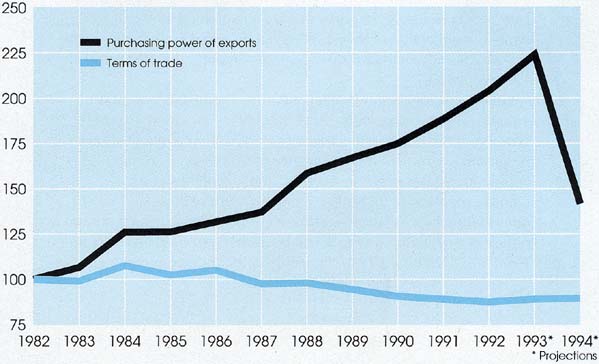

6 Despite their high dependence on food imports, LIFDCs rely heavily on agricultural exports, which account for about 28 percent of their total export earnings.· Despite a strong expansion in export earnings (8 to 9 percent, about twice the rate of the previous two years), the value of imports would still be more than twice that of exports. Nevertheless, unrequited transfers (largely official project and technical assistance, benefiting African countries in particular) would help to bring the current account deficit to less than half the level of 1989-90.· The terms of trade and, more significantly, the purchasing power of exports would show some improvement, thus reversing a negative trend. Gains in purchasing power would arise from a significant expansion in export volumes, since export unit values would rise only moderately.

· GDP growth is expected to accelerate slightly, reaching almost 3 percent in both 1993 and 1994, with agriculture expanding faster than other sectors.Figure 4 REAL GDP GROWTH OF SELECTED COUNTRIES AND ALL DEVELOPING COUNTRIES (Percentage change over preceding year)· Economic activity would be boosted by a significant expansion in total and agricultural exports. For the latter, this would mark a recovery from depressed performances in 1992.

· Along with the strong growth in exports would be a slight improvement in barter terms of trade in both 1993 and 1994, thereby interrupting a long declining trend. From 1981 to 1992, terms of trade have deteriorated virtually every year. The expected firming of commodity prices in the coming years would largely explain the terms of trade improvement forecast for these countries.

· Contrasting with the adverse movements in terms of trade, the purchasing power of exports generally showed positive growth during the past decade as a result of volume increases and they were expected to increase significantly again in 1993-94. Sub-Saharan countries in this group did not share in the favourable trend, however, and only minor gains in their export purchasing power are expected in 1993-94.

· Merchandise imports would expand even faster than exports, widening the trade deficit that began to emerge in 1991 and contributing to a further deterioration in the current account balance; however, the agricultural trade surplus would increase significantly and, consequently, contribute to the alleviation of the financial constraint.

Source: IMF and FAO

Figure 5A LIFDCs WITH THE LOWEST CAPACITY TO FINANCE FOOD IMPORTS (1982 = 100)

Figure 5B ECONOMIES HIGHLY DEPENDENT ON AGRICULTURAL EXPORTS (1982 = 100)

Source: FAO

One of the salient features emerging from the above review is the capacity of both groups of countries to counter adverse terms of trade movements through expanded volumes of exports. In the case of EDAEs, terms of trade deteriorated by a cumulative 27 percent between 1981 and 1992, but the purchasing power of their exports (of which agricultural products typically account for two-thirds) rose by a cumulative 53 percent. This is explained by the fact that, while the unit value of their exports fell by about 5 percent, export volumes increased by nearly 80 percent during the same 12-year period.

General factors behind such a vigorous expansion in export volume- itself a price-depressing influence- included: export promotion measures, often linked to stabilization and adjustment programmes; improvements in factor productivity, leading to competitive gains in world markets; and a general share in the global expansion of trade. The relative weight of these and other contributing factors is a research area of considerable interest from a policy perspective. This issue will be further explored in The State of Food and Agriculture 1994, focusing on the past experience of agricultural export-dependent countries.

|

BOX 2 Economies highly dependent on agricultural exports (EDAEs) specialize in the production and export of agricultural raw materials. To that extent, they could be expected to be in a better position to strengthen their competitiveness in world agricultural markets than those countries for which agricultural exports matter less. Historical evidence refutes this simplistic assumption. Not only have EDAEs lost agricultural market share globally but, in the cases of African and Latin American countries in this group, they have lost in relation to other developing countries with a more diversified export base. While identifying the determinants behind these trends is a matter for further research at the specific country and commodity market levels, one general observation can be made: specializing in agricultural exports - for many countries a fate-determined rather than a chosen course - does not per se guarantee competitiveness. The issue is more related to the overall economic situation of the countries concerned. EDAEs are, with few exceptions, relatively poor countries with a limited capacity for introducing technological improvements, investing and providing financial and technical support. This is likely to reduce their international competitive

position even in those trading activities for which they are better suited - all

the more so, considering the spurious competitive losses they suffer from farm

protectionism practised in many richer countries. |

|

|

1969-71 |

1979-81 |

1989-91 |

|

|

|

(......................%......................) |

|||

|

Share of EDAEs in: |

||||

|

|

- Agricultural exports of all developing countries |

49 |

56 |

51 |

|

- World agricultural exports |

18 |

17 |

14 |

|

|

Share of EDAEs, by region, in agricultural exports of all developing

countries |

||||

|

|

- Africa |

14 |

12 |

9 |

|

- Asia and Pacific |

10 |

13 |

15 |

|

|

- Latin America and Caribbean |

31 |

36 |

28 |

|

Meeting the goals of the International Conference on Nutrition

Decline in agricultural commodity real prices and exporters' earnings

Uruguay Round of multilateral trade negotiations

Current issues in fisheries management

Current issues in forestry

Biotechnology: challenges and opportunities for the 1990s

This section reviews selected issues of current or emerging importance for agriculture. The themes discussed this year concern challenges and achievements in food access and nutrition as a follow-up to the International Conference on Nutrition (ICN); the decline in commodity prices and the current status of the Uruguay Round; forest and forest industries, their status in economies in transition and issues related to forestry trade; high sea fishing and coastal zone fisheries; and opportunities and concerns arising from the development and application of biotechnology in agriculture.

Past achievements and current challenges

Nutrition at the centre of development

Action to improve nutrition

The World Declaration on Nutrition and the Plan of Action for Nutrition were unanimously adopted at the ICN, held in Rome in December 1992. Their adoption was the culmination of more than two years of preparation and collaboration at national, regional and international levels. It also marked the beginning of renewed and vigorous efforts at all levels to reduce global hunger and malnutrition and to improve the nutritional well-being of all populations.

With the adoption of the World Declaration on Nutrition, governments and other concerned parties pledged to make all possible efforts to eliminate before the end of the 1990s: famine and famine-related deaths; starvation and nutritional deficiency diseases in communities affected by natural and human-caused disasters; and major health problems related to iodine and vitamin A deficiencies. They also pledged to reduce substantially starvation and widespread chronic hunger; undernutrition, especially among children, women and the aged; other important micronutrient deficiencies, including iron; diet-related communicable and non-communicable diseases; social and other impediments to optimal breastfeeding; and inadequate sanitation and poor hygiene, including unsafe drinking-water.

The ICN recognized that poverty, social inequality and lack of education are the primary causes of hunger and malnutrition and stressed that improvements in human welfare, including nutritional well-being, must be at the centre of social and economic development efforts. It called for concerted action to direct resources to those most in need in order to raise their productive capacities and social opportunities. It also emphasized the need to protect the nutritional well-being of vulnerable groups through specific short-term actions, when needed, while working for longer-term solutions.

An estimated 20 percent of the people in the developing world are chronically undernourished, consuming too little food to meet even minimal energy needs. 7 Approximately 192 million children under five years of age suffer from acute or chronic protein-energy malnutrition; during seasonal food shortages and in times of famine and social unrest, this average number increases. According to some estimates, every year nearly 13 million children under the age of five die from infections or as a direct or indirect result of hunger and malnutrition. Moreover, more than two billion people, mostly women and children, are deficient in one or more micronutrients: babies continue to be born mentally retarded as a result of iodine deficiency; children go blind and die from vitamin A deficiency; and enormous numbers of women and children are adversely affected by iron deficiency. Hundreds of millions of people also suffer from diseases caused by contaminated food and water.

7 Defined as those people whose estimated daily energy intake over a year falls below that required to maintain body weight and support light activity.At the same time, a number of impressive achievements have been made in food availability, health and social services throughout the world over the last few decades. The estimated number of people in developing regions suffering from chronic malnutrition has declined consistently (from 941 million people to 786 million between 1969-71 and 1988-90), as has the proportion of malnourished people (from 36 percent to 20 percent), even though the world population has increased. In addition, life expectancy in most developing countries is improving steadily, mainly as a result of reduced early deaths from infectious diseases, while mortality rates among children are also declining.

Average per caput food supplies in developing countries increased in the 1970s and 1980s, although the rate is slowing. By the late 1980s, roughly 60 percent of the world's population lived in countries that had more than 2 600 kcal available per caput per day. Global food supplies (if distributed according to individual requirements) were sufficient to provide well over what would have been required to meet energy needs.

Progress in a number of countries indicates that the goals of the ICN, although ambitious, are attainable. In Thailand, for instance, during the past decade the prevalence of protein-energy malnutrition (PEM) among preschoolers was reduced dramatically from 50.8 percent to 17.1 percent, with the almost total elimination of moderate and severe forms. In Indonesia food availability increased from 2 072 to 2 605 kcal per caput between 1971 -73 and 1988-90 and the prevalence of malnutrition is decreasing steadily.

Chile has made remarkable achievements in improving the health and nutritional status of infants and preschoolers over the last three decades. Both infant and child mortality rates have declined from one of the highest to one of the lowest in the region; the prevalence of child malnutrition has declined from 37 to 8.5 percent.

India has completely eliminated famines over the last two decades. In Brazil, national averages of the prevalence of underweight children fell from 18.4 to 7.1 percent between 1975 and 1989. Substantial improvements have been made in the nutritional status of preschoolers in Zimbabwe and infant mortality rates have declined sharply. Botswana, despite current and persistent drought, has eliminated deaths from famine and starvation.

These country examples illustrate that nutritional status can be markedly improved by the commitment of political will and the formulation of well-conceived policies and concerted action at national and international levels. The immediate challenge to the international community is to build on the progress made and accelerate the pace of improvement in the nutritional well-being of all people.

Malnutrition primarily affects the poor and disadvantaged who cannot produce or procure adequate food, who generally live in marginal or unsanitary environments without access to clean water and basic services and who lack access to education and information for improving their nutritional status.

Moreover, poor health related to malnutrition reduces the resources and earning capacities of households that are already poor, thus increasing their social and economic problems. This, in turn, contributes to further declines in future human, economic and social development.

In the poorest countries, nutrition problems cannot be solved through nutrition programmes alone; efforts are needed to improve the overall social and economic conditions in those countries. In all countries, it is imperative to ensure that the benefits of social and economic development are directed to the poor and malnourished. In many instances, the most effective government strategies to reduce malnutrition on a national scale have been those focusing on national income growth with equity.

However, many national planners and policy-makers have often failed to give adequate attention to the nutritional implications of development policies. Consequently, such policies have not achieved the maximum nutritional benefits possible and, in some cases, they have had a negative impact on nutritional well-being. For example, the pursuit of industrialization policies that are biased against the agricultural sector has contributed to nutrition problems in some instances.

Macroeconomic policies that attempt to correct imbalances between aggregate supply and demand but fail to pay adequate attention to the social and nutritional implications can lead to serious nutrition problems, particularly for poor and vulnerable households. While improvements in nutrition may not be among the prime objectives of sector or subsector development policies, the identification of their potential impacts on nutrition should be given particular attention.

One key strategy emerging from the ICN is to promote better nutrition explicitly through a range of agricultural and development policies and programmes by incorporating nutrition objectives into the planning process. Significant improvements in nutrition can result from the incorporation of nutrition considerations into the broader policies of economic growth and development, structural adjustment, food and agricultural production, processing, storage and marketing of food, health care, education and social development.

Properly implemented development policies can improve nutritional status by providing an economic environment conducive to growth (employment and income creation) or by influencing the prices of and access to goods and services, especially food. Sectoral policies can also maintain or enhance the productivity of resources directly through agricultural and environmental policies or indirectly through health policies that enhance labour productivity. Moreover, public sector policies that develop and expand services such as agricultural extension, health clinics, crèches, schools, farm input centres, roads, bridges, wells and potable water supplies can all have beneficial impacts on nutrition.

The agricultural sector presents the greatest opportunity for socio-economic development and consequently offers the greatest potential for achieving sustained improvements in the nutritional status of the rural poor. In many rural areas, the overriding nutrition problems are more closely associated with a shortage of jobs than with a shortage of food. Often, the most pressing need is for employment creation, both on the farm and off, through activities related to agriculture. Agricultural policies can positively affect nutrition through improved food production, availability, processing and marketing as well as through increased employment opportunities.

Agricultural policies also affect time, labour and energy utilization, environmental and living conditions and the nutrient content of food. By taking a more comprehensive approach to development, planners may be able to encourage a more equitable distribution and consumption of food, while increasing the purchasing power of the nutritionally deprived, poor and disadvantaged groups of the population.

To safeguard the nutritional well-being of the poor, it is essential that macroeconomic policies do not discriminate against the food and agricultural sector and rural areas, where the poor often live. Public investment in health care services and public sanitation, including both piped water and sewerage, can significantly improve health and nutrition. Investment in infrastructure to promote effective market functioning, especially roads and transportation, and the communication of market information are also likely to promote equitable access to economic incentives.

A growth-promoting external economic environment also has an essential role to play in improving the nutritional status of the poor. Policies in this domain encompass improving the international trade environment, alleviating the external debt problem and increasing the flow of external resources. At the national level, rapid population growth is a serious barrier to achieving a sustainable improvement in living standards. Consequently, the implications of population policies on nutrition are significant, particularly in food-deficit countries where rapid population growth continues and where urbanization is increasing.

Education provides better opportunities and better living conditions which can result in improved health and nutrition. Maternal education and literacy, in particular, have a significant impact on children's survival, health and nutritional well-being. Education and literacy affect development and income which, in turn, contribute to improved nutrition. Education and the training of people to address food and nutrition concerns at the community and regional level may have a great impact in areas where such skills are lacking.

Environmental policies also have a major role in influencing the nutritional status of the poor. Policies should aim at creating an economic environment in which it is more profitable to manage and conserve natural resources than to destroy them.

Intersectoral dialogue, based on a strong government commitment and political will, is indispensable for encouraging realistic and complementary actions to improve nutrition. At local and regional levels, some structure is needed to identify actions that the various sectors should take to improve nutrition and formulate better operational objectives for such actions; for example, targeting the benefits of development preferentially to those most in need.

Most countries have already made good progress in identifying priority problems, reviewing or preparing plans and establishing intersectoral mechanisms for action. Many countries, including some of the poorest, have taken measures to strengthen food, nutrition, agriculture, education and health and family welfare programmes that have dramatically reduced hunger and malnutrition.

Many have also been successful in improving the nutritional status of their populations through intersectoral committees on food and nutrition and through integrated food, nutrition and health policies. The following country examples are representative of these successes.

Thailand's success is largely attributed to its five-year social, health and food and nutrition plans and, especially, to its Poverty Alleviation Plan (PAP). The PAP, initiated in 1982, is a rural investment programme aimed at improving the quality of life of 7.5 million poor people in the northern, northeastern and southern regions of the country. The plan concentrated on raising the population's living standards from the subsistence level and providing minimum basic services in rural areas with a high concentration of poverty.

The PAP emphasized maximum community participation and low-cost technology that would enable people to do more to take care of themselves. Four key programmes were employed: rural employment creation; village development projects or activities; provision of basic services; and an agricultural production programme. The very strong political support received by the PAP throughout its implementation as well as the emphasis on community participation are considered to have been essential to its success.

Indonesia's long-term development plans focus on food and nutrition policy and programmes as a priority in human development and poverty alleviation. At the national level, policy and planning of food and nutrition programmes are coordinated and approved by the National Development Planning Agency. Rapid and equitable economic growth and increased food availability are responsible for the improvements achieved in nutrition. Indonesia has been self-sufficient in rice since the mid-1980s, for instance.

Chile's remarkable achievements in improving nutritional status have been accomplished through the development of an integrated national food, nutrition and health policy that directly involves specific ministries in different sectors as well as through well-targeted policies and programmes in health, sanitation, education and food production.

Some of the activities implemented include: targeted food interventions for families in extreme poverty; treatment centres for severely malnourished children; nutrition education through the schools and health services; emphasis on elementary education, especially for girls; and a nationwide sanitation programme for the urban population.

Agricultural policies initiated in the mid-1970s have resulted in a complete turnaround in this sector, and food production has increased rapidly. The success of the agricultural sector has led not only to a sharp decline in food imports but also to a substantial increase in rural employment and income and, consequently, to a marked improvement in health and nutrition.

The Botswana Government has shown a clear commitment to improving national and household food security and nutrition and has made impressive achievements in improving the economic, social and nutritional status of its population. The country has established an intersectoral framework for improving food security and nutrition as well as for the overall development programmes.

Botswana copes with the ever-present problem of drought through an effective early warning system and comprehensive relief measures to alleviate the effect of drought conditions on the nutritional status of the population. Relief measures combine direct food supplements with income-earning opportunities for vulnerable households. The goals of the Early Warning Technical Committee are to improve drought monitoring activities, maintain the country in a state of readiness to confront drought and facilitate the response to drought situations.

The complete elimination of famine in India is a major achievement made possible by government policies on food security over the last two decades. The overall growth in food availability, resulting from the green revolution technologies and a substantial reduction in poverty, has eliminated the threat of famine for India's entire population. India's food security interventions, in particular the Public Distribution System and the National Rural Employment Programme, also provide good examples of both the benefit of government interventions to improve nutrition and the need to target such programmes better.

Many other countries have made important achievements that provide useful examples of effective ways to alleviate hunger and malnutrition. However, the resources, needs and problems vary between and within countries and regions of the world. The situation in each country and region needs to be assessed in order to set priorities for formulating specific national and regional plans of action, giving tangible expression to policy-level commitments to improve the nutritional well-being of the population. This should entail considering the nutritional impacts of overall development plans and relevant sectoral development policies.

National plans of action for nutrition need to be initiated or reformulated in accordance with the goals and objectives of the World Declaration on Nutrition and the Plan of Action for Nutrition. These national plans of action should: establish appropriate goals, targets and time frames; identify priority areas for actions and programmes; indicate the technical and financial resources available, as well as those still needed, for programme development and implementation; and foster continued intersectoral cooperation.

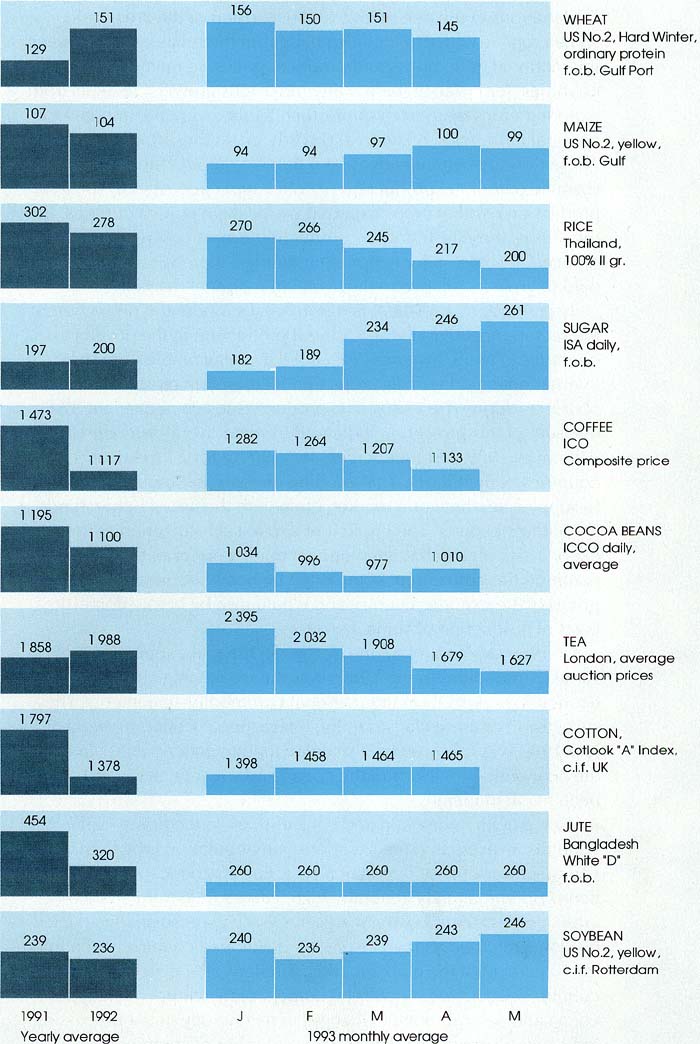

For at least a decade, the prices of agricultural commodities have tended to fall on international markets while those of manufactures have tended to rise. These contrary movements have resulted in a decline in the net barter terms of trade between agricultural commodity exports and the imports of manufactures and crude petroleum. In 1992 the decline was 2 percent. A comparison of the three years 1990-92 with the years 1979-81 shows a decline of 30 percent, that is an average annual rate of 3 percent. The decline was close to 40 percent for the agricultural commodity exports of the developing countries and 20 percent for those of the developed countries.8 Some countries have achieved gains in productivity sufficient to outweigh the decline in real prices (the barter terms of trade) but, for many, the decline has reduced earnings per hectare of land cultivated (the single factor terms of trade). Furthermore, the global decline in prices has been so large that it has generally offset the expansion of production, thus actually reducing overall earnings (the income terms of trade).

8These data are derived from UN world export price indices of primary commodities.Examples of the degree to which increases in crop yields and production have been outweighed by declines in the barter terms of trade are provided in Table 4. Coffee exporters have generally been big losers, as the small increases in yields and production have been far outweighed by a 66 percent decline in the barter terms of trade on the international market. Other commodities showing large losses have been cocoa, natural rubber, sugar, rice and maize.

The rise in production despite major declines in these terms of trade may be partly explained by the survival of plantings and other investments made in earlier and more favourable years. In fact, just prior to the start of the 1980s - by 1977-78 - the barter terms of trade for coffee and cocoa had been more than twice as high as in 1979-81.9 The real price of rubber had peaked in the early 1950s but the plantings spurred by this and the succeeding years of favourable prices caused its production to continue. The level of production incentives in earlier years would also explain growth in the production of oil-palm, which rose substantially in the 1980s.

9 FAO. 1987. instability in the terms of trade of primary commodities 1900-1982. FAO Economic and Social Development Paper No. 64, p. 172. Rome, FAO.TABLE 4

Changes in yield, production and terms of trade for selected commodities, 1990-92

|

Commodity |

Change in yield |

Change in production |

Change in terms of trade |

||

|

|

|

|

Barter |

Single factor |

Income |

|

(...............................................%..........................................) |

|||||

|

ALL COUNTRIES |

|||||

|

Coffee |

3 |

14 |

-66 |

-65 |

-61 |

|

Cocoa |

18 |

42 |

-66 |

-60 |

-52 |

|

Tea |

27 |

36 |

-28 |

-8 |

-2 |

|

Cotton lint |

36 |

34 |

-33 |

-9 |

-10 |

|

Natural rubber |

12 |

34 |

-44 |

-37 |

-25 |

|

Sugar |

10 |

27 |

-55 |

-50 |

-43 |

|

Soybean |

16 |

26 |

-36 |

-26 |

-19 |

|

Rice |

29 |

32 |

-48 |

-33 |

-31 |

|

Wheat |

36 |

29 |

-35 |

-12 |

-16 |

|

Maize |

15 |

18 |

-35 |

-25 |

-23 |

|

DEVELOPING COUNTRIES |

|||||

|

Cotton lint |

53 |

52 |

-33 |

2 |

2 |

|

Sugar |

9 |

43 |

-55 |

-51 |

-36 |

|

Soybean |

21 |

66 |

-36 |

-23 |

7 |

|

Rice |

30 |

34 |

-48 |

-32 |

-30 |

|

Wheat |

44 |

53 |

-35 |

-6 |

-1 |

|

Maize |

28 |

41 |

-35 |

-17 |

-8 |

Note: Barter terms of trade = export prices (of agricultural products) deflated by import prices (of manufactured goods and crude petroleum); income terms of trade = export earnings deflated by import prices; single factor terms of trade = net barter terms of trade adjusted by changes in productivity (yields per hectare).For some commodities there has also been an expansion of production in areas that have the advantage of low-cost production, often achieved by above-average increases in productivity. Explanations of the persistence and expansion of the area under some crops would also include changes in the relationship between international trade prices and producer prices. In many developing countries, for instance, before the mid-1980s growers' receipts from exported crops were often diminished by the overvaluation of their national currencies, taxation and costly marketing arrangements. These restraints on incentives, and thus on output, applied to a sizeable part of the production of coffee and cocoa and to some production of other crops exported by the developing countries. In the 1980s, these restraints on production incentives were greatly reduced in some major exporting countries, thereby raising prices paid to growers relative to those on international markets.Source: FAO.

By contrast, as a result of governmental support and protection of the sector, incentives for agricultural production in the developed countries in many instances exceeded those available from the international market. This protection increased in most developed countries during the 1980s. The producer subsidy equivalent (PSE) measure of this protection increased from an overall average of 30 percent in 1979-81 to 44 percent in 1990-92 for 22 member countries of the OECD. The resulting increase in output was added to supplies on the world market, often with the use of public funds to facilitate exports. The implicit or explicit subsidization of these exports also meant that international market prices of the commodities concerned would often be below domestic producer prices of the exporter country and would also be below domestic costs of production of some importers.

A further explanation of the decline in the real export prices of some commodities in the 1980s was the weakening and removal of economic provisions in international commodity agreements. The suspension of these clauses in the International Coffee Agreement in July 1989 was followed by a steep decline in coffee prices. Earlier, the economic provisions of the cocoa and sugar agreements had been made inoperative.

Slow growth in demand and consumption in the developed countries exacerbated the situation. The population growth in these countries was only 0.7 percent a year. Further, per caput consumption, already generally high, gained little from an income growth of less than 3 percent a year. Coffee was especially affected by slow growth in its markets, as the developed countries accounted for 70 percent of the global market. Similarly, the developed countries accounted for over 60 percent of the global market for cocoa and natural rubber. Changes in technology in the processing industries also reduced demand for a number of commodities, especially natural rubber and sugar. There was, however, considerable growth in the market for animal feeds, which was of importance to oilcakes and oilmeals, non-cereal feeds and, in some cases, grains. This growth has been reduced of late by a squeeze on animal production in both Eastern and Western Europe and in the former USSR.

Figure 6 EXPORT PRICES OF SELECTED COMMODITIES ($ per tonne)

Increases in per caput consumption through price reductions also tend to be relatively small in the developed countries. Thus, for many commodities the volume consumed was persistently below that produced, despite decreases in international commodity prices of up to 66 percent from the beginning of the 1980s. Smaller price decreases in the face of high rates of production increase were recorded for commodities where consumption was more responsive to international prices, for example animal feeds in the developed countries and commodities with major markets in the developing countries, such as tea.

Since early 1992, the GATT multilateral trade negotiations (MTNs) have proceeded on four tracks.10 Under track one, negotiations on market access have taken place bilaterally, plurilaterally and multilaterally. Similarly, on track two, negotiations have been conducted on initial commitments in services. Under the third track, work has taken place on the legal conformity and internal consistency of the draft agreement in the Draft Final Act. Finally, the Trade Negotiations Committee (TNC) has held a number of meetings, thus forming the fourth track.

10 Developments up to early 1992 were covered in The State of Food and Agriculture 1992.Of particular importance to these trade negotiations were the bilateral discussions between the Commission of the European Communities (CEC) and the United States that concluded in the so-called Blair House Accord of November 1992.11 The parties reported achieving progress necessary to assure agreement on the major elements blocking progress in Geneva, notably in agriculture, services and market access. Regarding agriculture, the parties resolved their differences over the main elements of domestic support, export subsidies and market access. They also agreed how to resolve their dispute on oilseeds.

11 GATT document MTN. TNC/W/103 of 20 November 1992.The main differences between the Draft Final Act and the Blair House Accord concern the possibility that subsidized export volumes may be reduced by 21 percent instead of 24 percent and that the 20 percent reduction in the aggregate measure of support would apply not to individual commodities, as envisaged under the Draft Final Act, but to agriculture as a sector. Furthermore, all subsidies decoupled from production would be exempt from reduction. That is, they would be included in the "Green Box" category.

Subsequently, there have been several calls at international meetings, including the FAO Council, for a successful and comprehensive outcome of the Uruguay Round. Further impetus was given by the agreement at the July 1993 meeting of the G-7 leaders of industrialized countries to reduce or eliminate tariffs on a wide range of manufactured goods.

Coastal zone fisheries and local involvement in management

High sea fishing

For many years FAO has been promoting local-level involvement in fisheries management. Although Chapter 17 of UNCED's Agenda 21 takes a broader outlook on the issues, particularly those relating to environmental and habitat protection, the basic principles of community involvement still apply and the following observations and guidelines for fisheries management are quite valid in this broader context.

The devolvement of management responsibility to the local level is often a gradual process, linked to the capacity of the community to manage its own affairs effectively. In this connection, careful attention needs to be given to traditional or customary management systems which may already exist with respect to the management of different resources. The recognition and possible legalization of such systems may provide a solid basis for local-level management.

Clearly defined local property and ownership rights to the resource can facilitate the monitoring and enforcement of regulations, including self-policing, and therefore make management more effective. They can also improve the planning and implementation of specific management measures because of the traditional and indigenous knowledge of the resources, their seasonalities and other characteristics that are available to the resource users.

Many of the most vulnerable resources of coastal areas are characterized by the open access condition. Open access implies that the use of the resources is unpriced, as anybody who wishes can exploit the resources without paying a price for them. This did not create problems in the past when resources were abundant relative to the available exploitation technologies and the demand for the resources. However, population growth and technological progress have changed this situation dramatically, with the result that there is widespread misuse and degradation of open access resources in coastal areas.

The open access condition is often particularly badly felt by local communities whose livelihood may depend on such resources. In the absence of local control, people from outside the communities take advantage of the open access condition and, with superior financial and technical means, are often able to appropriate large parts of the resources to the detriment of local users. This has frequently led to conflict, for example between local artisanal fisheries and national and international industrial fleets. Some countries have taken steps to establish local rights to local resources. An example is in the Philippines, where municipalities have been given exclusive rights over coastal waters up to 15 km from the shore.

Increasing international concern about the sustainable use of the world's fishery resources has focused attention on the manner in which high sea fishing operations are conducted. This matter has been considered in a number of international fora, including the International Conference on Responsible Fishing, UNCED and the FAO Technical Consultation on High Seas Fishing, all of which were held in 1992.

One of the recommendations of UNCED, and in particular of Chapter 17 in Agenda 21, was to convene an intergovernmental conference under the auspices of the UN to consider measures and mechanisms that could be adopted internationally to manage straddling fish stocks and highly migratory fish stocks better. The first session of this conference was held in 1993.

The 1982 United Nations Convention on the Law of the Sea (the 1982 Convention) lacks detailed provisions with respect to high sea fishing. As a consequence, the management of high sea living resources has often been ineffective. Unlike the management of resources falling under coastal state jurisdictions, there is no comprehensive internationally agreed regime for the management of the high seas.

When extended jurisdiction was introduced by most countries in the 1970s, it was anticipated that there would be a significant retrenchment of fleet capacity. This retrenchment did not occur and the capacity of fleets continued to expand. Vessels that could not gain access to the exclusive economic zones (EEZs) of coastal states that had surplus fish stocks were forced to shift their operations to the high seas. Consequently, FAO estimated that, in the 1970s, 5 percent of world fish catches came from areas beyond the 200-mile zones while, in 1990, this share was estimated to have increased to 8 to 10 percent.

As a result of government subsidization policies, many fishing nation fleets targeting high sea resources have expanded since the introduction of extended jurisdiction. These subsidies, estimated to be $54 000 million per year, have enabled fleets to continue operating when, under normal circumstances, such operations would not have been financially viable. Indeed, it is estimated that, to return to the 1970 catch rate per vessel, the removal of at least 30 percent of the existing tonnage in the world's fishing fleet would be required.

The need to secure internationally agreed management mechanisms for the rational exploitation of high sea resources is recognized both by coastal states and distant-water fishing nations. FAO is contributing to the formulation of the Code of Conduct for Responsible Fishing and the Draft Agreement on the Flagging of Vessels Fishing on the High Seas. Such management agreements must necessarily involve consensus on the overall exploitation limits of stocks and resource allocations. For management mechanisms to be effective in securing sustainable resource use, adherence to measures agreed by contracting parties will be critical. There is a risk, furthermore, that the effectiveness of management mechanisms will be eroded by non-contracting parties to conventions.

Recycling in forest industries

Forests and forest industries in countries in economic transition

Trade and sustainable forest management

The recovery and recycling of residues has played a major role in the development of forest industries in the last 50 years. Forms of recycling include the utilization of the residue of logs processed in the sawmill to produce chips for pulp and paper and particleboard; the use of small wood previously left in the forest; the use of bark and other residues for energy production; and the recovery of waste paper for use in paper manufacturing.

More than 95 percent of the industrial wood harvested in developed countries is used in primary or secondary production. About 70 percent enters into the actual fibre composition of the final product and 20 percent is recovered or recycled from final residue into energy generation within the industry. The recovery of wood residues is at a much less advanced stage in developing countries, where only 65 percent of industrial wood harvested is effectively used and 58 percent of wood harvested enters into the actual composition of the product. Thus, there remains a potential equivalent of some 30 percent of industrial wood residues which could be recovered.

As environmental concerns have gained importance, the issue of recycled fibres has increasingly attracted the attention of environmentalist groups and mass media. The paper industry, which has expanded strongly in the last decade, has considerably increased the amount of recycled fibre products utilized. It has also substantially improved the control of effluent and emissions as well as energy efficiency.

Between 1980 and 1991, world consumption of paper and paperboard rose from 170 million to 245 million tonnes, while per caput world consumption rose from 38 to 45 kg per year. To meet the increasing demand for paper, the industry has relied on three major fibre sources: wood pulp, other fibre pulp and waste paper. In the period 1980-1991, wood pulp consumption rose from 126 million tonnes to 155 million tonnes, at a rate close to 2 percent per annum. The consumption of waste paper rose much faster, from 50 million to 88 million tonnes, i.e. at a rate of 5.3 percent per annum. World consumption of other fibre pulp, 16 million tonnes, is concentrated in developing countries, predominantly in China.

Recovered waste paper is today an important raw material for paper manufacturing. Accounting for 40 percent of the fibre input both in developed and developing countries, it totalled 88 million tonnes in 1992. Twelve million tonnes enter international trade, with the United States providing some 50 percent of total exports, mainly directed towards developing countries in Asia.

However, the world disposes of a further 150 million tonnes of used paper, which is a major component of the total 500 million tonnes of solid waste generated each year. Disposal of this massive amount of waste has become a major physical problem for local municipal authorities. Various policy instruments have been considered for reducing the volumes of waste paper to be disposed of, including increase in recycling and the use of incineration for energy production.

The recovery of waste paper for reuse is, under certain conditions, an economically feasible option. When free from contaminants, waste paper may be reused as pulp, thus saving the raw material inputs and the cost of manufacturing paper pulp. Contaminated waste paper requires cleaning, however. In particular, inks, glues, coatings, fillers and additives have to be removed. This process is costly, as it requires special equipment and often produces noxious residues and effluents. This recycling process also results in some deterioration and loss of fibre.

Recycling waste paper is all the more economically viable when the transport distance is limited or the recovered paper is reused in mills in the locality where it is collected. This tends to be the case in densely populated countries with a high per caput paper consumption, such as Germany, Japan, the Netherlands and some other European countries where recovery rates of more than 50 percent have been achieved.

Local and national authorities in some countries are introducing measures to encourage or improve increased recycling. However, policy measures that require paper to have recycled content may lead to the transportation of waste paper to distant mills, making recycling less economical. In addition, mandatory measures may lead to the market being swamped by an oversupply of recovered paper. There is also a risk of forcing the use of excessively costly recycling processes in order to recover low-grade or badly contaminated waste paper. In circumstances of high recycling costs, the incineration of waste paper as well as other urban waste for energy production may be more economical and beneficial to the environment.

In general, recycling is a component of a more efficient utilization of basic raw materials and it contributes to the reduction of urban waste. Its future growth will lead to a change in the demand for wood raw materials from forests and induce adjustments in forest management. In fact, a lower demand for small logs, mainly used by the pulp industry, poses a particular problem because it reduces the market for products of intermediate cutting (thinning), which is necessary to improve the quality of the final harvest.

Market-oriented reforms in Eastern Europe and the former USSR have initially led to considerable reductions in their production, trade and consumption of forest products. The output of forest products fell from the peak years of the mid-1980s to 1991 by percentages of about 30 to 40 percent for mechanical wood products and more than 45 percent in the case of paper production.

The collapse of the former marketing and distribution system and the replacement of its predetermined production and price levels with market-determined prices resulted in a very sharp increase in real prices of wood products and lower levels of domestic demand. In Poland, real prices of wood products rose by 50 percent between 1987 and 1991, while the per caput consumption of sawnwood, already well below West European levels, fell by 60 percent. Similar declines in per caput consumption of forest products took place in Bulgaria and Romania.

Trade in forest products among these countries was also hampered by the collapse of the Council for Mutual Economic Assistance (CMEA) trading arrangements and the introduction of pricing in convertible currencies. Exports to other areas suffered as well, reflecting the problems of quality and competitiveness faced on Western markets as well as uncertainties resulting from changes in long-established trading arrangements. Thus, total exports of sawnwood from countries in Eastern Europe and the former USSR dropped from 10.5 million m3 in 1987 to 6.4 million m3 in 1991.

The paper industry, which relies heavily on energy and chemicals, suffered severely from the dismantling of intraregional trade in inputs and products as well as from the inadequacy and obsolescence of equipment. In Estonia difficulties with energy imports from the Russian Federation and the need to pay for raw materials in hard currency have practically brought the paper industry to a standstill. The obsolescence of equipment and inadequate pollution controls have forced the virtual closure of the wood pulp industry in the former German Democratic Republic.

By 1993, conditions for the wood industries appeared more favourable in the Czech Republic, Hungary, Poland and Slovakia. In these countries, the first signs of economic recovery have begun to stimulate investments in residential activities using wood. The other countries, less advanced in the process of economic transformation, are seeing a continuation of falling output, trade and consumption of forest products. Production of coniferous sawnwood in the Russian Federation in 1993 is expected to continue to decline because of financial problems experienced by producers and trading organizations and because of uncertainty about forest legislation.

The privatization of property and enterprises is regarded as an important step to speed up the transition process. Given the complexity of the political, legal and administrative problems concerning landownership, the privatization of forest land has tended to be slow and uneven among countries. In Hungary it is expected that 60 percent of forest land will remain in state ownership while some 30 percent will be transformed into private ownership or into joint forest property associations. In the Czech Republic, joint stock companies are expected to be founded to assume ownership of state forests, while in Slovakia publicly owned forest enterprises, financed from the state budget, will be the norm. In Poland the state forests will still provide the basic potential both in economic and ecological terms, but previous owners, whose forest land was nationalized, will be compensated financially. Under the Romanian Land Law of 1992, the state is expected to return to previous owners 300 000 ha of forest land out of a total forest area of 6 million ha. In Estonia only 55 000 ha of forest land have so far been privatized since 1991, but up to half of the total forest land of 1.8 million ha may be privatized in the future.

Some notable progress has been achieved in the important area of forest industry privatization. In Hungary, where the process is most advanced, some 55 percent of the total capital of the pulp and paper industry had been privatized by the end of 1991, with 23 percent of participation being foreign capital. The decentralization of the forest industry in the Czech Republic and Slovakia is expected to be followed by the privatization of the most efficient wood enterprises and the formation of small private companies. In Poland some of the smaller sawmills have been privatized, but this process is complicated by claims from previous owners; the Polish wood-based panel industry, the largest in Eastern Europe, has seen the privatization of eight mills out of a total of 30 while, in the pulp and paper sector, private joint ventures with foreign capital have included seven large enterprises. Important developments have also taken place in some of the Baltic republics. In 1993, Estonia launched a massive privatization programme of state property, open to foreign capital, which included the offer for sale of 11 forest industry complexes comprising three pulp and paper mills. In some countries, such as Romania, the privatization of the sector is still proceeding very slowly; in 1992, for example, only 100 000 m3 of wood, out of a total of 2 million m3 harvested, were purchased by private operators. In the future, however, harvesting operations in Romania may be taken over by contractors and wood enterprises may be transformed into commercial societies with state, mixed and private capital.

It is generally agreed that every effort should be made to ensure that forests are sustainably managed so as to permit their survival, but there is less agreement on how to achieve this objective.

It is clear, however, that trade is not a major cause of deforestation and, as such, trade policies alone cannot ensure sustainable management of the forests. Only a minor proportion of the wood harvested actually enters world trade and the linkages between trade policies and forest management are very indirect. In the case of tropical forests, only about 6 percent of the wood harvested enters international trade in any product form and only one-third of the tropical timber produced (logs, sawnwood and solid wood panels) is sold on international markets.