![]()

![]()

![]()

SUB-SAHARAN AFRICA

ASIA AND THE PACIFIC

LATIN AMERICA AND THE CARIBBEAN

NEAR EAST AND NORTH AFRICA

The following review examines recent economic and agricultural performances in the four developing country regions and highlights the main policy developments affecting their agricultural sectors during 1992 and 1993. Following the customary approach, the review then focuses more specifically on the experience of selected countries in each region: Ethiopia in Africa; Bangladesh and Sri Lanka in Asia; Mexico in Latin America and the Caribbean; and Egypt and the Syrian Arab Republic in the Near East.

Regional overview

Ethiopia

The economic performance of sub-Saharan Africa was dismal yet again in 1992. The average growth rate of the region (excluding Nigeria) was 0.9 percent, a slight recovery from the meagre 0.2 percent achieved in 1991.1 However, these averages mask a great diversity among individual countries. According to the African Development Bank (AfDB),2 more countries (16) experienced negative growth rates in 1992 than in the previous year (13) and fewer countries (19) experienced growth rates of more than 2.5 percent than in 1991 (23). Moreover, economic growth fell far short of population growth. Consequently, in per caput terms, output shrank by 1.1 percent in 1992, meaning the sixth successive year of decline. Overall, the picture is that of worsening economic and social conditions.

1 UN. 1993. Economic Recovery, 6(4).

2 AfDB. African Development Report 1993.

The UN Economic Commission for Africa (ECA) estimates output growth to be about 3 percent in 1993 (for Africa as a whole).3 That growth rate, if achieved, would merely keep abreast with the projected population growth rates.

3ECA. Economic Report for Africa 1993. UN.The causes of the gloomy performance of sub-Saharan African countries include: i) the negative effects of the depressed global environment on trade and capital flows; ii) the continuing decline in terms of trade for primary exports which represent the bulk of foreign exchange earnings for most countries in the region; iii) the undiminishing debt burden that continued to frustrate the process of recovery and structural adjustment in many countries (see Box 3); iv) the declining inflow of external resources from both official and private sources; v) civil strife in parts of the region; and vi) low agricultural production as a result of drought.

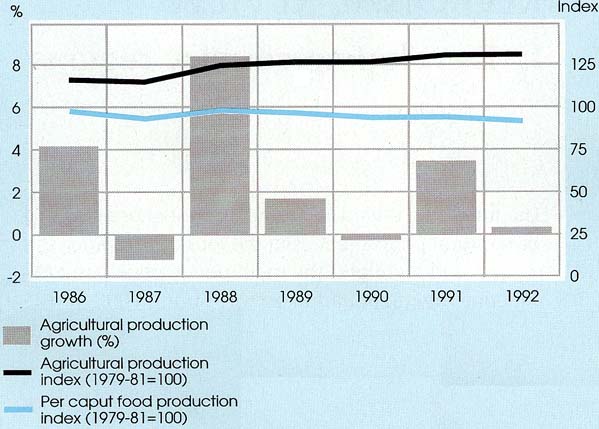

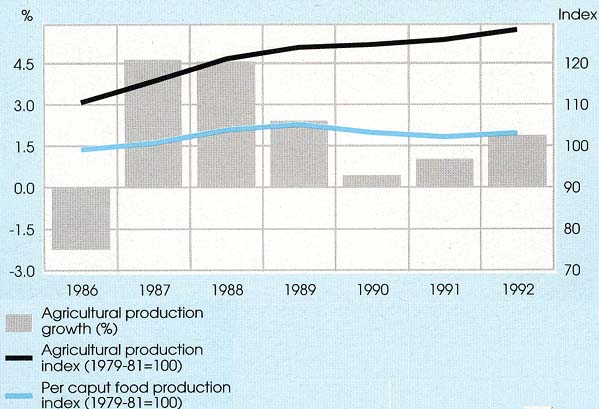

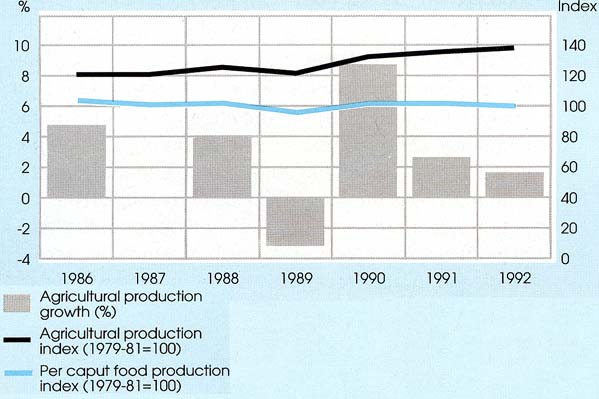

Figure 7 SUB-SAHARAN AFRICA - AGRICULTURAL AND PER CAPUT FOOD PRODUCTION

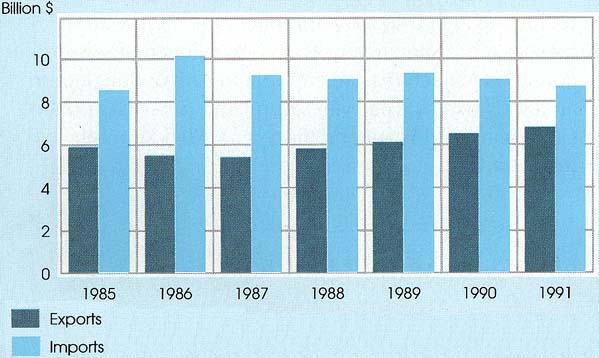

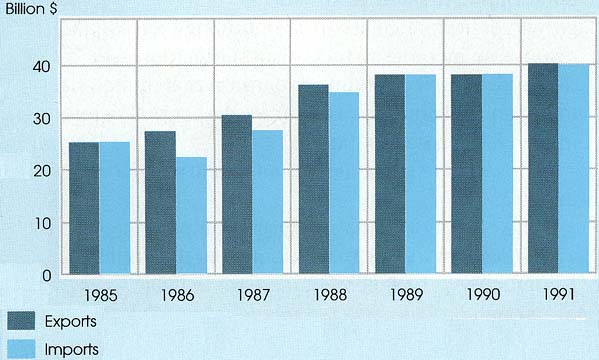

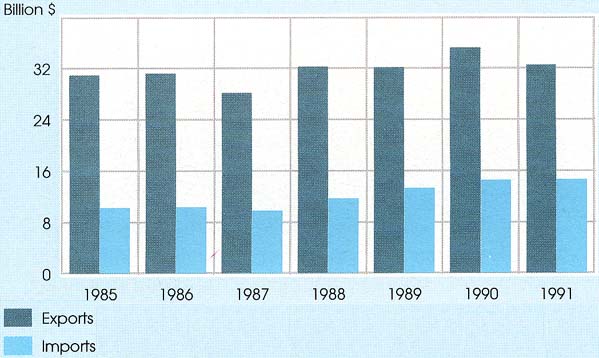

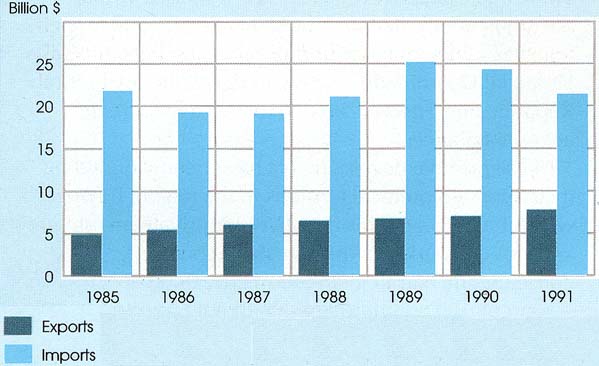

Figure 7 SUB-SAHARAN AFRICA - AGRICULTURAL TRADE

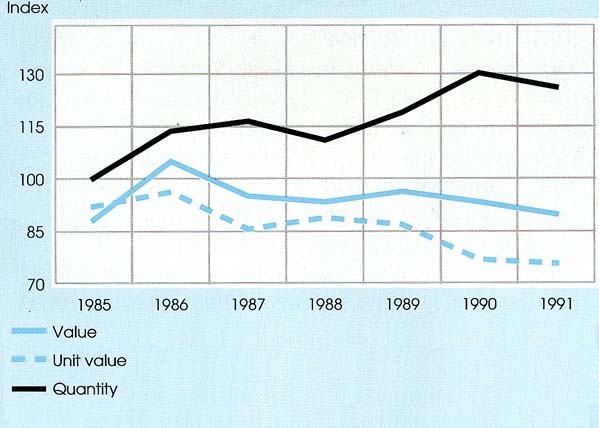

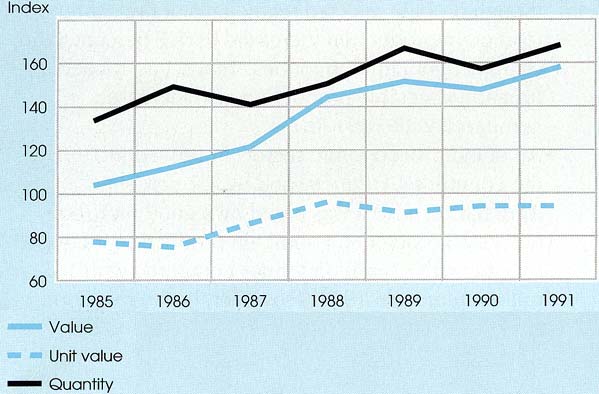

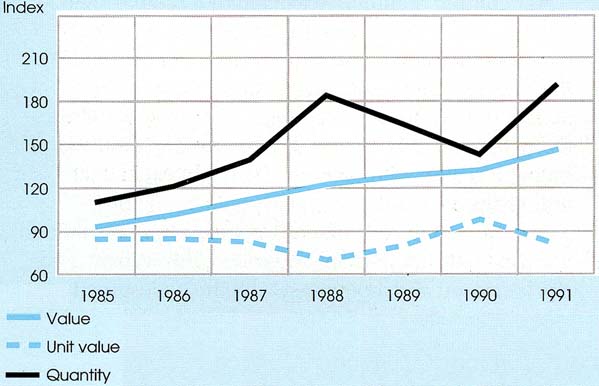

Figure 7 SUB-SAHARAN AFRICA - AGRICULTURAL EXPORTS (Index 1979-81 = 100)

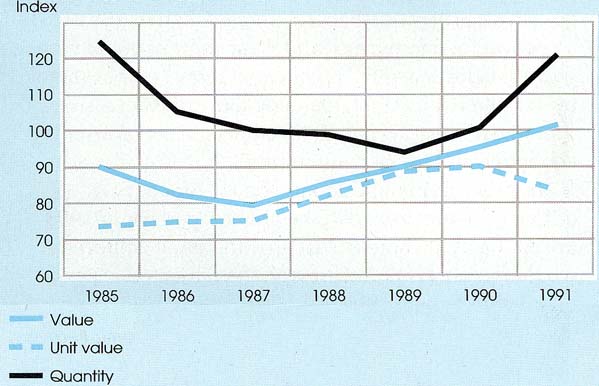

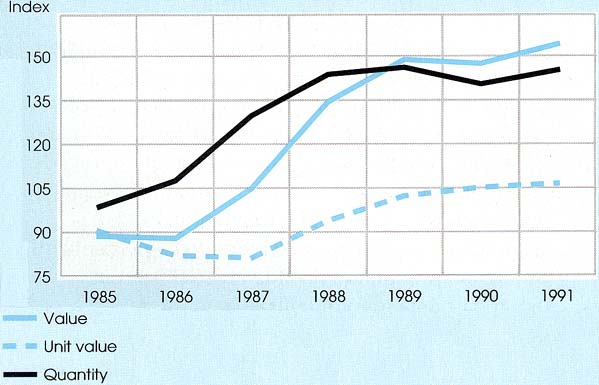

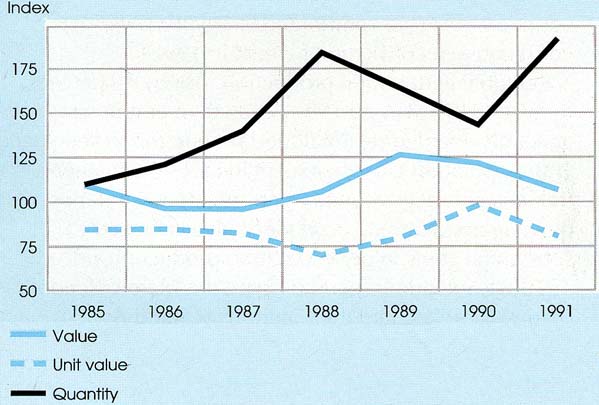

Figure 7 SUB-SAHARAN AFRICA - AGRICULTURAL IMPORTS (Index 1979-81 = 100)

The slow growth (1.7 percent) in the combined output of industrialized countries constrained demand for developing country imports and capital flows to the developing world. Moreover, the demand for primary commodities remained weak and their prices declined in spite of a small recovery in world trade during the year.

Terms of trade for sub-Saharan exports deteriorated further in 1992. Despite lower inflation in the industrialized countries, the main trading partners of sub-Saharan Africa, import prices rose by 3.2 percent during 1992. Meanwhile, prices of exports fell, albeit less pronouncedly than in 1991. Among the main agricultural commodities exported by the region, only logs, tea and sugar registered higher export prices in 1992 than in 1991. Cocoa and coffee recorded their eighth and sixth consecutive years, respectively, of falling prices. Prices of almost all metal and mineral exports from sub-Saharan Africa fell during the year. Moreover, in 1993, improvements are expected only in aluminium and diamond prices.

With continuing poor prospects for export earnings relative to the value of imports, sub-Saharan Africa requires an increasingly large volume of external resource flows. However, foreign direct private investment in the region has traditionally been small ($1.7 billion in 1991) and can be expected to remain so, particularly as private resource flows to countries labelled as bad debtors are rare. The hope that structural adjustment programmes would accelerate the flow of foreign private finance seems to have been misplaced.

Unfortunately for sub-Saharan Africa, which has traditionally depended on official resource flows, the flows of Official Development Assistance (ODA) to the region have actually declined of late. ODA net disbursements, which amounted to $11.5 billion in 1990, were down by about $1 billion (in real terms) in 1991. Meanwhile, at $6 billion, total multilateral net disbursements remained the same in 1991 as in the previous year.

|

BOX 3 Total debt for sub-Saharan Africa was more than $183 billion in 1992, up from about $178 billion in the previous year. At that level, the debt stock exceeded the 1992 annual regional GDP by 6 percent. Interest arrears on long-term external debt alone were a staggering $14 billion. Nearly one-fifth of hard-earned export revenue was used to service debt in 1992. Although that figure signifies a third consecutive year of decline, the debt-service ratio remains stubbornly high. A significant share (some 10 percent on average between 1985 and 1991) of total debt originates from loans for projects in the agricultural sector. In 1991, the latest year for which data are available, outstanding agricultural long-term external debt was just over $13 billion, up from about $12.5 billion in the previous year. For 1991 alone, net long-term flows on debt (or net lending) to agriculture, at $727 million, were the lowest since 1985; nevertheless, they represented 23 percent of total net flows on debt. Despite years of efforts to reduce the sub-Saharan African debt burden through rescheduling and debt forgiveness, only a small amount of debt has so far been affected. In 1991, only $3.8 billion of Africa's debt (mostly in sub-Saharan Africa) was cancelled. During 1992, only nine countries secured the "enhanced Toronto terms", which allow for a cancellation of or reduction in the interest charges offered by some creditor countries. The amount of debt involved is significantly less than it would have been with the cancellation of two-thirds of the entire stock of eligible debt, as envisaged under the "Trinidad terms". Furthermore, only two countries had recourse in 1992 to the IDA Debt Reduction Facility, which is oriented towards reducing commercial debt, because of the creditors' reluctance and debtor countries' domestic constraints as well as debtors' failure at times to comply with structural adjustment conditionality. Multilateral debt, rather than commercial or official

bilateral debt, is fast becoming the major problem in sub-Saharan Africa. During

the 1980s, most countries were lured away from contracting commercial market

debt by the prestructural adjustment experience, commercial banks' reluctance to

lend to debt-burdened countries and donor persuasion, and they consequently

resorted to heavier borrowing from multilateral financial institutions. Almost

40 percent of total sub-Saharan Africa's official long-term debt in 1992 was

owed to multilateral institutions from which the debtors can not expect debt

rescheduling or cancellation. |

Wars and civil strife, notably in Angola, Liberia, Mozambique, Somalia and the Sudan, contributed significantly to the overall economic decline in 1992, as did the sometimes chaotic political situations in such countries as Togo and Zaire where looting and rioting destroyed the infrastructure required for economic development.

The level of agricultural production in 1992 remained virtually unchanged over that of 1991, the major cause being the drought that affected East and southern Africa. As a whole, the latter experienced a decline of 7.7 percent over the previous year and accounted for 16 million of the 40 million people estimated by FAO to be facing food shortages in sub-Saharan Africa. Elsewhere in Africa, growth was slow; in central Africa, agricultural output grew by 1.4 percent and, in West Africa, the growth rate was 2.9 percent. Civil strife exacerbated the already disastrous food supply and access problems in Mozambique and Somalia.

Cereal production fell by more than 5 percent for the region as a whole. In southern Africa, where cereals are the main staple, output fell to less than one-half of the 1991 level. Thanks to less dramatic changes in cereal and non-cereal food items elsewhere in the region, notably in Ethiopia, the Sudan and in West and central African countries, the aggregate food production sector increased slightly - by nearly 1 percent - over the previous year. The output of non-food agricultural commodities, on the other hand, fell by about 5.7 percent.

Over a longer period, sub-Saharan Africa has, contrary to popular belief, maintained trend growth rates in agricultural production comparable to other regions of the world.4 In fact, from 1981 to 1992, aggregate production increased at a rate of 3 percent per year, with slight declines in 1982, 1986 and 1990. The problem in the region has always been the population growth rate which has outstripped growth in production, thus resulting in a declining per caput output. For instance, although agricultural output increased marginally (0.3 percent) in 1992, per caput production declined by nearly 2.8 percent. The prospects of a reversal of this trend depend on both the region's ability to slow population growth as well as its capacity, assuming more benevolent weather conditions and fewer wars and civil disruption, to increase production through sustainable and intensive agriculture.

4 UN. 1992. Economic Recovery, 6(3).With the return of favourable weather conditions for the 1992/93 growing season, a rebound of agricultural output in countries affected by drought in 1992 is expected in 1993.

With respect to policy developments, structural adjustment programmes with emphasis on short-term objectives continued to guide policy reforms in most countries in the region. The pursuit of adjustment with transformation and the harmonization of short-term policy goals with medium- and long-term development objectives were hardly in evidence. The latter were the objectives of the African Alternative Framework to Structural Adjustment Programmes for Socio-Economic Transformation (AAF-SAP) adopted recently by the Organization of African Unity (OAU).

Fiscal reform played a central role in efforts to strengthen domestic economic management. The success rate in reducing budget imbalances varied considerably, however. Benin and the Gambia, for instance, were able to reduce their budget deficits as a proportion of GDP, but many other countries failed to do so.

Monetary policy emphasized a tight control of money supply as well as adjustments of interest rates. Going against the grain, however, Zaire embarked on a course of monetary expansion, and its inflation rate reached huge proportions. Interest rate adjustments were an important plank of monetary policy and real interest rates were raised by several countries, including Cape Verde, Comoros, Côte d'Ivoire, Djibouti, the Gambia, Guinea-Bissau, Kenya, Malawi, Mali, Mauritania, Tunisia, the United Republic of Tanzania, Zambia and Zimbabwe. Ghana and Mauritius adjusted their nominal bank rates downwards but they remained positive in real terms.

The move towards market-determined exchange rates continued in many sub-Saharan countries in 1992 either through outright devaluation of national currencies (e.g. Ethiopia, Malawi, Mauritania and Rwanda) or by flotation (Nigeria) and foreign exchange liberalization (e.g. Algeria, Uganda, the United Republic of Tanzania and Zambia).

Public sector reforms, which have included trimming the size of the civil service and curtailing government consumption, were a continuing feature of the reform programme. Privatization also played a major role in public sector reforms of such countries as Chad, Côte d'Ivoire, Ghana, Mozambique, Nigeria, the Sudan, Uganda and Zambia.

Policy reforms in agriculture continued in most countries, often within the overall framework of structural adjustment programmes negotiated with the World Bank and the IMF. Market liberalization remained an important component of agricultural policy reforms, with agricultural parastatals being dismantled, privatized or restructured in countries such as Burundi, Côte d'Ivoire and Mozambique. In some other countries (e.g. Ethiopia, Kenya, Malawi, Mali, Uganda, the United Republic of Tanzania, Zambia and Zimbabwe), some or total decontrol of agricultural marketing has been effected. Agricultural market liberalization has also been planned for implementation in other countries, including Lesotho and the Central African Republic.

Some countries have embarked on a policy of diversifying the agricultural export base, moving away from a reliance on one or few export crops, as international prices for traditional exports continue to crumble. For example, Benin is promoting the production of palm oil, coconut and groundnuts as well as pineapple and exotic fruits and vegetables, along with the traditional export, cotton. Uganda is planning to diversify into sesame, tobacco, hides and skins, spices and fish after regaining a market share in its traditional exports: cotton, tea and coffee. Typically, the fisheries sector has featured prominently in the drive towards diversification. Mozambique, Namibia, Nigeria and Sierra Leone are just four of the countries that have embarked on aggressive fish farming campaigns.

The drought in southern Africa has led to the region's agricultural development policies being focused mainly on drought relief, increased food production and diversification within the food sector. In Malawi, in addition to supporting maize production (the main staple for most of the population), the government is promoting the production of cassava - a drought-resistant crop - as a security crop, as well as promoting local production of vegetable seeds. Zambia is encouraging the production of sorghum, millet and cassava in its food crop diversification strategy to reduce dependence on maize. In Zimbabwe, price and non-price incentives have been provided to farmers to ensure an increase in grain production. Other countries in the region have followed similar trends.

Food security has also been a major preoccupation elsewhere in the region. Nigeria's five-year ban on wheat imports (lifted temporarily at the end of 1992) was designed to promote domestic production and was a partial success. Senegal has launched a programme intended to achieve an 80 percent self-sufficiency in food. In Burkina Faso, a project to prevent seasonal hunger and malnutrition has been launched; and in Djibouti, efforts are under way within the broad arena of food security to encourage greater consumption of local products, including food.

The drought in the southern part of the region has been a catalyst in the reorientation of agricultural policies towards a more efficient exploitation of irrigation potential in the region; Malawi is one of the countries that are actively addressing this issue.

Environmental protection has also received some attention within the context of agricultural policies. The Global Coalition for Africa, in its first annual report, contends that four-fifths of the cropland and pasture land in sub-Saharan Africa is at least partly degraded; and that deforestation might have been a cause of the significant decline in rainfall in the Sahel, in coastal areas along the Gulf of Guinea, in Cameroon, northern Nigeria and East Africa.5 Environmental concerns have led, for example, to a government ban on the felling of some tree species in Zaire and to a ban on the exportation of 18 log species in Ghana. Several other countries have outlined strategies to develop forests and rationalize the exploitation of fisheries resources.

5 The Global Coalition for Africa. 1992. African Social and Development Trends. Annual Report, p. 11.In addition to desertification, which was Africa's primary concern at the United Nations Conference on Environment and Development (UNCED) in 1992, the countries in the region have given priority to the issues of increased finance and technology transfers during the UNCED follow-up discussions. In doing so, they are echoing the thoughts of part of the donor community. The World Bank, for example, has made it clear that environmental issues are at the top of the priority list of the Bank's concessional lending arm - the International Development Association (IDA).

Although policy emphasis was heavily weighted towards national concerns in 1992, intra-African trade, in particular, but also economic and political integration, generally, received a boost through a number of important decisions.

The Preferential Trade Area for Eastern and Southern African States (PTA) amended the PTA Rules of Origin: all goods originating from member states, regardless of the nationality of the producers, are now subject to preferential tariffs.

In August 1992, the Southern African Development Coordination Conference (SADCC) was renamed the Southern African Development Community (SADC) in anticipation of the potential accession of post-apartheid South Africa.6

6 The prospects of a settlement of the political quagmire in South Africa have been enhanced by the announcement of a tentative date (April 1994) when the country will hold multiracial elections.The year also witnessed ratification by a few more countries of the 1991 Abuja Treaty establishing the Pan-African Economic Community (PAEC).

The apparently renewed commitment to economic integration results from the recognition that the region's future may lie in collective self-reliance as the international economic environment becomes increasingly hostile, thereby threatening accelerated growth in the small, often fragmented, individual economies of sub-Saharan Africa. Self-reliance was one of the themes of the international conference, held in Dakar from 16 to 18 November 1992, entitled "Trampling the Grass: Is Africa's Growing Marginalization in the Newly Emerging International Order Reversible?" The conference was hosted by the African Centre for Development and Strategic Studies (ACDESS), a major new African think-tank.

The country: general characteristics

The economy

Economic policies affecting agriculture

Agricultural sector policies

The impact of policies on agriculture

Current issues in agricultural development

Situated in northeastern Africa, Ethiopia constitutes the largest part of the Horn of Africa.7 It spans an area of 1 223 600 km2 (one of the largest countries in Africa) and has an altitude ranging from 100 m below sea level to more than 4 000 m above sea level. The second most populous African country after Nigeria, Ethiopia has a population of 55.1 million.8

7 Eritrea, officially independent since May 1993, is included in most of the reported data because of insufficient information to permit systematic reporting on Ethiopia only.The main characteristic of the climate is its erratic rainfall patterns. The southwest highlands receive the highest average rainfall, while precipitation decreases towards the northeast and the east. Even in areas with a high mean annual rainfall, the variations can be extreme. Chronically drought-prone areas cover almost 50 percent of the country's total area and affect about 20 million people.981992 estimates.

9T. Desta. Disaster management in Ethiopia: past efforts and future directions. Presented to the United Nations Sudano-Sahelian Office (UNSO) Workshop on Drought Preparedness and Mitigation. Early Warning and Planning Services Relief and Rehabilitation Commission, Addis Ababa, May 1993.Drought was at the root of at least ten famine episodes in the last 40 years which have affected large areas and significant portions of the population. In the last 20 years, the most serious droughts in terms of human suffering were those of 1972-73 and 1984-85.10

10 For more information, see T. Desta, op. cit., footnote 9.

Ethiopia is one of the poorest countries in the world, with a per caput GDP of $120 and 60 percent of its population living below the poverty line.

Agriculture accounts for 50 percent of the country's GDP and 90 percent of exports. In terms of area under cultivation, cereals (teff, maize, barley, wheat) are the major crop category, followed by pulses (horse beans, chickpeas, haricot beans) and oilseeds (mainly neug and linseed). Coffee is the main export (accounting for 57.3 percent of total agricultural exports), followed by hides and skins (28 percent), live animals (3.3 percent) and vegetables.11 About 78 percent of the total value of production from manufacturing industries is based on the processing of agricultural products (food processing, beverages and textiles).

11 AGROSTAT data for 1990.The smallholder sector accounts for 90 percent of the country's agricultural output. The average farm size is estimated to be between 1 and 1.5 ha.

The overall growth of GDP during the 1970s and 1980s (1.9 and 1.6 percent, respectively) closely follows the trends in the growth of agricultural production (0.7 and 0.3 percent, respectively) and both magnitudes are well below the population growth rate (estimated to be 3 percent).

The search for proximate causes of both agricultural and general economic stagnation in Ethiopia since the mid-1970s leads to a set of interrelated structural constraints and policy factors. In addition to the harsh agroclimatic conditions, inadequate and poorly maintained infrastructure, environmental degradation and inadequate technology have contributed to the decline of agriculture.

At the policy level, macroeconomic and sector-specific policies have contributed to the creation of a negative environment for agricultural growth. The rise to power of the revolutionary government in 1974 marked the beginning of an era of tight direct government controls on the production and distribution systems. A brief description of the policies implemented as well as their effects help explain the nature and magnitude of the problems facing Ethiopia today.

Macroeconomic policy: a deceptive internal balance. In Ethiopia, macroeconomic policies have traditionally been characterized by prudent fiscal management. The fiscal deficit was kept at an average of 7 percent of GDP for most years between 1975 and 1989, with the exception of drought years.

Relatively low deficits were achieved despite increasing public expenditure (from about 17 percent of GDP in fiscal 1974/75 to 47 percent in 1988/89). An aggressive policy of fiscal receipts prevented the deficits from ballooning. The budgetary effects of external shocks were mitigated by foreign disaster-relief flows. In general, foreign flows of grants and loans left about half the deficit to be financed internally. As the government avoided recourse to inflationary financing, average inflation was kept close to 9 percent during the 17 years ending in 1991.12

12 For details, see World Bank. 1990. Ethiopia's economy in the 1980s and framework for accelerated growth, Washington, DC.While a macroeconomic balance and price stability are necessary for growth, Ethiopia is an example of how these two factors may not be sufficient. Public fixed investment expenditure grew by almost 16 percent annually after 1975, while recurrent expenditure grew by 5 percent. It was chiefly channelled towards directly productive activities (mainly in manufacturing and public utilities), which often had questionable efficiency performances. During the 1980s, 30 percent of real capital outlays were devoted to agriculture (including state farms and land settlement) and only 15 percent to infrastructure (transport and communications).13 Of the recurrent expenditures, approximately 2.2 percent were devoted to agriculture and settlements while close to 55 percent were spent on security and defence.

13 For detailed Ministry of Finance data, see A. Teferra. 1993. Ethiopia: the agricultural sector - an overview, Vol. II - statistical annex. Paper prepared for the Policy Analysis Division, FAO.An aggressive revenue policy brought total fiscal revenues from 20 to 29 percent of GDP in the 1980s. Tax collection was divided evenly among domestic indirect taxes, business profit taxes and taxes on foreign trade. Taxes on coffee exports amounted to 30 to 40 percent of the f.o.b. coffee export values. Profits made by the lucrative state enterprises (mainly airways, mining and shipping) constituted an increasing share of total revenues. Occasionally, emergency levies and surcharges were imposed.

Institutional constraints on private business activity, for example a ceiling of 0.5 million birr (br) of fixed assets per manufacturing enterprise and a lack of investment opportunities and consumer items increased the amount of deposits (demand and savings) made by households and private businesses. High levels of deposits could be attracted at low interest rates (forced savings) and they were, in turn, mobilized for financing the domestic deficit. As a result, 85 to 90 percent of domestic financing came from the banking system.14

14 See footnote 12.On the expenditure side, the relative neglect of infrastructure and less than optimum public investment allocation in agriculture weakened the overall productivity of the economy. Likewise, the emphasis on security in the recurrent budget and the maintenance of uneconomical projects further aggravated the situation. Furthermore, non-inflationary financing of the budget deficit was achieved at the expense of private investment opportunities. Thus, overall domestic balance was achieved but basic sources of productivity and growth were neglected or suppressed.

Between 1974 and 1993, the agricultural policy environment as well as that of the economy as a whole can be divided in three periods:

· 1974 to 1988, when "command economy" measures were implemented and consolidated;Given the country's variable agroclimatic conditions, three sets of interdependent factors shaped the environment for agricultural growth: the institutional framework; pricing and marketing policies; and the distribution of budgetary allocations.· 1988 to 1991, when a number of previous measures were abandoned and reforms were made towards a more liberal economy;

· the post-1991 period (the revolutionary regime collapsed in 1991), during which several of the 1988-1990 reforms were consolidated and additional measures were taken to liberalize the economy.

The pre-1988 situation. In March 1975, the government announced sweeping changes in the structure of land tenure and labour relations in rural areas. The major elements of the law (Proclamation 31 of 1975) were: i) the nationalization of land and the abolition of private landownership; ii) a ban on tenancy contracts; iii) the prohibition of hired rural labour in private farming; iv) guaranteed access to cultivable land for all households.

Individual farm units were organized in peasant associations (PAs) which allocated and reallocated land among households, collected taxes and production quotas and organized voluntary labour for public works. The PAs, in turn, formed service cooperatives (SCs) which carried out supply, marketing and extension functions. Producers' cooperatives (PCs) were composed of individual households which commonly managed their consolidated farms. A number of large state farms were also established. By 1989, there were 17 000 PAs and 3 700 SCs, while the socialized sector (PCs and state farms) comprised 3 300 PCs with a total of 290 000 members.

Despite efforts directed towards the "socialization" of agriculture, the structure of production basically remained private because peasants strongly resisted integration in PCs. By 1988, the share of individual peasant holdings in total cultivated land was around 94 percent, with the remainder divided between PCs (2.5 percent) and state farms (3.5 percent). The allocation of public resources between the socialized and the non-socialized sectors was not proportionate to their importance, with the bulk of financial resources, modern inputs and extension personnel allocated to the socialized sector whose productivity performance often did not justify this disproportionate allocation.

"Villagization" (the grouping of the population in designated villages) became national policy in 1985. By 1989, one-third of the rural population had been transferred to villages. In 1985, in the wake of the drought, the campaign to resettle peasants from drought-stricken areas to uncultivated lands was intensified. Poor organization and settler selection transformed the scheme into an extremely costly project which required continuous subsidies in order to survive.

Pricing and marketing policies also reflected the tendency towards heavy state control. The Agricultural Marketing Corporation (AMC) was responsible for wholesale domestic procurement of grains, oilseeds and pulses and for cereal imports. The AMC was responsible for collecting all the marketable produce from PCs and state farms and required individual farms to deliver a quota based on their assessed capacity to produce a marketable surplus. From 1980, a pan-territorial pricing system was in effect for the quotas, with procurement prices remaining fixed until 1988 when they were increased by 7.7 percent.

Even after their increase in 1988, procurement prices for teff, wheat and barley were, respectively, 37, 61 and 45 percent of free market prices. There were intermittent bans on private trading in major producing regions until 1988. In addition, private traders were obliged to sell the AMC a share of their purchases (ranging between 50 to 100 percent) at br 4 to br 5 more than the price paid to farmers. AMC procurement was not particularly successful and its share of grain purchases reached a peak of 11 percent of the total grain crop in 1986/87, as both individual farmers and traders had strong reason to evade controls.

The functioning of the public procurement system created a market "dualism". On one side, there was the public distribution system which delivered to mills, hospitals, urban associations (kebeles), educational institutions and the army. On the other, there were (poorly integrated) free markets where grains and pulses were sold at substantially higher prices.

Exports of pulses and oilseeds, coffee and livestock were also handled by parastatals. Livestock products for export were procured at market prices while domestic trade was free. Coffee farmgate prices have been kept low (at 35 to 45 percent of their f.o.b. value) even under the overvalued official exchange rate.

The reforms of 1988. Faced with economic stagnation and mounting social problems, in 1988 the government initiated a programme of economic reforms aimed at liberalizing the economic system. The government pointed to the following causes for the economic stagnation:15 i) the negative effects of suppressing private economic activity; ii) the unbalanced allocations of investment in peasant agriculture in favour of the low-performance socialized sector; and iii) neglect of market forces and the private sector in favour of central planning that led to resource underutilization and inefficient investment.

15 Presidential Address to the Ninth Plenary Session of the Central Committee of the Workers's Party of Ethiopia, November 1988.In response to the diagnosis above, the government endorsed and started implementing a series of measures, including increases in price incentives as well as institutional reforms. Official procurement prices were increased and crop quotas for delivery to the AMC were reduced. Price incentives for coffee were improved substantially. The number of licensed traders was increased, interregional restrictions on the movement of agricultural produce was abolished. Participation in PCs became voluntary and, by the end of 1989, 95 percent of these cooperatives had disintegrated. Several PAs also disappeared.

Another set of reforms was introduced in 1990, liberalizing the foreign investment code, while plans existed to allow the hiring of rural labour. As the country plunged increasingly into civil strife, political instability and institutional disintegration, those policies were not put into effect.

The post-1991 economic environment. In May 1991, the Transitional Government of Ethiopia (TGE) assumed power. It faced an economy that was devastated by the long period of civil strife, with low living standards and deteriorating infrastructure and social conditions. In addition to the deep-rooted problems of poverty in the country, there was the challenge of providing a livelihood for 350 000 demobilized soldiers and their families as well as for a large number of war refugees and displaced civilians.

Along with measures to establish peace and security in the country, a wide-ranging programme of economic and social reforms was introduced by the government with support from the donor community.

On the macroeconomic side, the government devalued the birr from br 2.07 to br 5 per US dollar and, in May 1993, a limited exchange rate auction system was established for essential items.

In agriculture, the government guaranteed use, lease and inheritance rights to land. In the transition period, land redistribution has stopped and the hiring of rural labour is now allowed. The TGE has announced that an elected government should handle the land tenure issue by referendum. The AMC lost its monopoly power so most grain is now marketed by private traders and the quota system has been abolished. Since January 1993, all export taxes have been abolished, with the exception of the coffee export tax. A 15 percent subsidy on fertilizer has been instituted as partial compensation for the effects of the devaluation. In the transport sector, trucking has been liberalized and there are plans to parcel and sell the government trucking company.

The effects of the policies (both macroeconomic and sector-specific) followed from 1974 to 1991, especially those applied before 1988, created an overall negative environment for agricultural growth, thereby contributing to the virtual stagnation of agricultural output.

Institutional changes with respect to land caused a drastic reduction in the size of farms which often were not sufficient to support a household. Tenure uncertainty had serious environmental implications while the small size of the holdings and the lack of timely distribution of fertilizers and seeds (exclusively distributed by the public sector) have contributed to the stagnation of yields.16

16 Average cereal yields are about 1.2 tonnes per hectare for the smallholder sector, two-thirds as high as those in Kenya for comparable soil fertility and climatic conditions. For pulses and oilseeds (at 0.65 tonnes and 0.5 tonnes per hectare, respectively), yields are among the lowest in the world.There has been insufficient research on appropriate technologies and inputs (seeds and fertilizers) adapted to the agroclimatic conditions of the country. The Ethiopian Seed Corporation distributed about half of the 40 000 tonnes of seeds that were estimated to be needed by the traditional farm sector. The erratic distribution of seeds and a lack of extension services caused many farmers to rely on traditional seeds and refuse new varieties.

Although the land actually controlled by PCs and state farms was only a small percentage of the total land area cultivated, according to the Ten-Year Perspective Plan 1982/83-1993/94, most individual farmers were to be organized into PCs. The final objective was for 44 percent of the cultivated land to be allocated to individual farms, 49 percent to PCs and 7 percent to state farms. Although the plan was never implemented, its provisions - along with the uncertain land tenure system and the frequent land reallocations within PAs - created great uncertainty among individual farm households and acted as a disincentive to long-term investments by farmers as well as to sustainable farm practices.

Furthermore, the marketing system was not conducive to the production of a marketing surplus, as low prices were paid for quota deliveries. Restrictions on interregional movements prevented the integration of deficit and surplus areas, a situation that was exacerbated by the poor condition of rural roads, tight controls on the transport and hauling system and the long distance of the majority of small peasant holdings from all-weather roads. The relative neglect of rural infrastructure greatly reduced overall investment efficiency.

It is difficult to single out the impact of the liberalization measures taken between 1988 and 1990, as their effects are clouded by the severe disruption of markets caused by the war. There is evidence of a reduction of spatial price dispersion and increased market integration for cereals following liberalization, despite the worsening security situation.

Thus far, the response of the economy and agriculture to the post-1991 reforms is encouraging, although it is difficult to establish with precision a correspondence between policies and performance. Exogenous factors (favourable weather) and non-economic factors (increased peace and security) have played a positive role in expanding economic activity.

On the macroeconomic side, after a reduction of 5.2 percent in 1991/92, real GDP is expected to grow by 7.5 percent in 1992/93, one percentage point above the government target. Inflation fell from 45 percent in the period June 1990/June 1991 to 14 percent in the corresponding period 1991/92. It is believed that the country had already absorbed the effects of the devaluation, as a large number of foreign exchange transactions were taking place on the parallel market at br 7 per US dollar.

The projected strong performance of real GDP is linked to the agricultural sector's continuous strong performance during the last three years. Cereal production showed a strong recovery, with a total production of 7.3 million tonnes in 1990/91 (a record crop), followed by a near-record crop in 1991/92 of 7.1 million tonnes and a projected 7.7 million tonnes in 1992/93.17

17Sources: For 1990/91, Central Statistical Authority data; for 1991/92, Ethiopian Ministry of Agriculture estimates; for 1992/93, FAO. 1993. Food-supply situation and crop prospects in sub-Saharan Africa. Rome. Note: Data include non-food uses.The variations reflect changes in weather patterns and localized droughts. The peasant sector accounted for most of the increase in output, while state farm production was static. Fertilizer consumption was 30 percent higher in 1992 and cropped land area expanded in response to strong cereal prices. Increased deliveries of coffee have been observed in the Addis Ababa market during the first months of 1993.

Recent policy reforms constitute the beginning of deep structural changes needed to set the Ethiopian economy on a sustainable development path. Ethiopia is, and will stay for some time, an economy in transition between two different economic development models. Among the numerous issues currently facing Ethiopian policy-makers, two are analysed more extensively in this report: i) food security and poverty alleviation; and ii) natural resource degradation.

Poverty and food insecurity. The extent of the problem and its root causes. Food insecurity (defined in its most basic form as a situation where the food needed for a healthy life is not accessible to all people at all times) is both a chronic and a transitory phenomenon in Ethiopia. It is estimated that 50 percent of the country's total population (between 23 million and 26 million people) are subject to food insecurity. More than 20 million of these people live in rural areas. In cases of consecutive periods of natural and human-caused calamities, poor households sell their assets, deplete their food stocks and become highly vulnerable or destitute and in need of continuous flows of food assistance to survive. Over the last two decades, transitory food insecurity has manifested itself in the famines following the droughts of 1972-73 and 1984-85.18 In Ethiopia, refugees and people displaced by the civil war are highly vulnerable groups requiring assistance.

18 Similar consequences were averted in the 1987 drought because of early warning and adequate preparation.With respect to chronic food insecurity, data show that even in normal periods (i.e. not characterized by abnormal climatic or socio-economic conditions)19 the average national level of food intake was 14 percent below the minimum daily requirement of 500 g of cereal equivalent per caput. "Average" data may be misleading because they mask differences in the ability of people to gain access to available food supplies. Data from the Ministry of Agriculture show that, in 1982/83, average incomes per household in the low-income areas were less than one-third of those in higher-income regions. Poor regions were also food-deficit areas and, given the lack of market integration, grain prices were much higher in those areas, thus further exacerbating the access problem.20 It is estimated that, although food aid has prevented the average food availability from falling dramatically, acute malnutrition during periods of drought and civil disturbances has affected 8 percent of the population.21 FAO has estimated that the current level of food production (including grains, pulses, vegetables, fruits and livestock products) could provide a total of 1 600 to 1 700 kcal per caput per day. Food aid and imports increase total per caput caloric intake to 1 800 to 1 900 per day which is below the minimum recommended 2 100 kcal per day.

19 For instance, the period 1979-1984.Poverty is at the root of the problem of access to food supplies.22 In the rural sector, the poor have limited productive assets, mostly of low quality (small farm size, poor soil quality, variable rainfall, a small number of livestock); limited opportunities for alternative employment; poor access to social services; and they use traditional production techniques. The poor also spend a large part of their incomes on food and energy, while a minimal amount is saved.23 Thus, they are highly vulnerable when emergencies occur. Urban poverty is the result of high unemployment and wages fixed at low levels. The problem has been aggravated recently by the influx of demobilized soldiers and displaced people and by increases in food prices on the free market.20 For more information, see IFAD. 1989. IFAD: Special Programming Mission to Ethiopia. Working Papers Nos 1 (Macro-economic performance and trends) and 7 (The dynamics of rural poverty). Rome.

21 Ethiopian National Institute data. See I. Loerbroks. Statement on the occasion of World Food Day 1992, 16 October, Addis Ababa, Ethiopia.

22 In addition to the level of per caput income, access to social services is another dimension of poverty. Such access, if it exists, can compensate for some of the consequences of low income. In this report, only the elements of poverty directly affecting access to food are examined. For a detailed analysis of the different dimensions of poverty in Ethiopia, see The social dimensions of adjustment in Ethiopia: a study on poverty alleviation. Addis Ababa, Ministry of Planning and Economic Development. May 1992.Policies for alleviating poverty and food insecurity. Broad-based economic development is essential for a long-term sustainable improvement in the lives of the poor. For Ethiopia, the role of agriculture is critical in this respect. Agricultural growth will address the supply side of the food security issue (i.e. increasing food production and foreign exchange for food imports) as well as the access side, through employment creation and income opportunities. On the other hand, policies that promote growth are often slow to work and it may take several years of growth to absorb productively the unemployed and underemployed labour force and raise the living standards of the most needy groups.24 As a major restructuring of the economic system is taking place, some of the short-term adjustments (especially food price increases) will negatively affect the most vulnerable parts of the population.23 Using 1982/83 survey data, IFAD estimated that only 5 percent of rural income was saved.

24 According to the World Bank, assuming 5 percent real GDP growth and 3 percent population growth, it will take 35 years for the per caput GDP of Ethiopia (of $120) to double.Thus, in addition to policy reforms aimed at growth, urgent targeted measures must be taken to deal with poverty in the short and medium term. Issues related to emergency (drought) preparedness and relief as well as to the most appropriate use of the (substantial) food aid flowing into the country need to be examined in the light of the changing economic conditions. Following are some of the issues and actions being taken by the government.

Safety net measures. Past policies for poverty alleviation emphasized untargeted commodity subsidies administered mainly through the public distribution system. Beneficiaries of the subsidies were members of the kebeles, PCs and cooperatives who were issued rations of subsidized food and other commodities (soap, salt and kerosene). Families had access to the same rations irrespective of income, the intention being (especially in the urban areas) the creation of a self-targeted system where the more privileged households would not be willing to queue in the kebele shops to obtain lower-quality items. The problems with the system of generalized commodity programmes were: i) it had a strong urban bias, i.e. urban consumers, representing 15 percent of the population, were receiving about 60 percent of the subsidies; ii) although it provided significant relief to poor households, it benefited disproportionately the middle- and higher-income ones, as very poor households could not afford to buy their ratio at subsidized prices; and iii) the economic costs of those programmes (i.e. using border prices at equilibrium exchange rates) were extremely high. As prices were liberalized and the exchange rate was devalued, the programmes became unworkable.25

25 World Bank calculations show that, at the shadow exchange rate of br 5 per US dollar (which, after 1991, became the actual exchange rate), the benefits to the poorest 30 percent of the urban population amounted to about 16 percent of the total cost of the urban commodity subsidies. For the rural sector the share was 5 percent (after adding the cost of the fertilizer subsidy). The total weighted share (urban plus rural) was about 12 percent.In the wake of the complete liberalization of commodity markets in 1991, the TGE instituted a programme to mitigate the effects of food price increases on the poor. The programme contained a number of safety net features, including a limited public sector wage adjustment to cover food price increases; severance pay and retraining for employees of abolished public enterprises; and a food/kerosene voucher scheme to assist the poorest groups in the urban areas. The scheme uses the kebele administrative infrastructure to target the poorest households which, depending on their income, receive a voucher either free or in exchange for community service or public works. This targeted income transfer scheme is more efficient than the previous system of untargeted commodity subsidies. In the rural areas, a programme to provide fertilizer and other input vouchers for poor farmers is under consideration, as is a rural public works programme to help generate income for unemployed rural workers.

Food aid for development. Food aid increased from about 3.5 percent of total food availability in the first half of the 1980s (up to 1984) to 17.2 percent during the second half, reflecting the effects of the 1984-85 drought.26 The TGE has taken a clear position against free food distribution in its programming of food aid resources. This position is based on the belief that free food distribution is ineffective in arresting or reversing the trend towards impoverishment and that it could destroy the survival mechanisms of the poor. Thus, a number of proposals exist for the use of food aid as a development tool through employment-generating public works programmes. The basic elements of these proposals are: i) selection of labour-intensive projects, mainly in the rural areas, based on food-for-work or cash-for-work compensation - the latter being funded with proceeds from monetized food aid; ii) a self-targeting mechanism by which the cash or food-equivalent wage is set below the market wage, thus attracting only the truly poor and vulnerable.

26 See footnote.The extent to which such a programme can be implemented will depend on the capacities of the line ministries, the Early Warning and Planning Services Relief and Rehabilitation Commission, NGOs and the regional governments to resolve a number of issues, including the following:

· a system for setting the appropriate wage level has to be established;Natural resource degradation.27 Degradation of natural resources constitutes one of the major constraints to increasing agricultural production in Ethiopia. According to FAO, about half of the highlands (270 000 km2) are already significantly eroded; of this, 140 000 km2 are seriously eroded and have been left with relatively shallow soils. Close to 20 000 km2 of agricultural lands are so badly eroded that they are unlikely to sustain cropping in the future. About 1 900 million tonnes of soil are being eroded annually, of which about 10 percent is carried away by rivers and cannot be retrieved, while the rest is redeposited as sediment within the highlands but mostly in places that cannot be of much agricultural use. If the trend continues, land covered by soil with a depth of less than 10 cm will constitute 18 percent of the highland area by the year 2010. This implies a dramatic fall in yields, frequent crop failures and a high probability of famines, especially in the low-potential cropping areas (LPCs) of the highlands. In addition to on-site agricultural production losses, erosion reduces the effective lives of dams and reservoirs through siltation as well as increasing the extent and intensity of droughts and flooding.· the main orientation of the projects must be decided, i.e. whether projects will be selected strictly in terms of economic cost-benefit criteria or whether such economic efficiency will be compromised in favour of projects that make a significant difference in the level of employment (putting more emphasis on the project's social safety net features).

27 This section is derived for the most part from FAO. 1985. Ethiopian Highlands Reclamation Study. Project report. Rome.Soil erosion is not a necessary consequence of cropping but rather a result of inappropriate cropping practices. Factors contributing to high erosion rates are the removal of natural vegetation for cropping, fuel, grazing and building; short, intense storms in the rainy season; high erodibility resulting from deforestation; and highly sloped topography. In the Ethiopian highlands, population pressures forced the cultivation of increasingly steeper slopes and progressively shortened the fallow between periods of annual cropping. It is estimated that four-fifths of the erosion in the highlands occurs from the overexploitation of croplands, while most of the remainder is caused by the overgrazing of grasslands and deforested areas.

Deforestation constitutes another serious environmental problem. In less than a century, the country's forest and woodland cover has been reduced from 40 percent of the total area to 16 percent in the 1950s and an estimated 4 percent at present.

Past policies concerning the agricultural sector amplified the adverse resource degradation and depletion effects of agroclimatic parameters. Villagization schemes placed an excessive demand on forest resources for building material. No effort was made to explore and introduce new energy sources in the rural sector, so wood and dung remained the only sources of energy. As the demand for such resources grew with population, deforestation and the deprivation of land from valuable nutrients increased. Uncertainty about land tenure acted as a disincentive to investments in soil conservation. Inadequate funding for agriculture and its disproportionate distribution in favour of state farms and cooperatives resulted in a shortage of funds for research on appropriate peasant technologies. In general, the policy environment discouraged the integration of conservation activities into the farming practices of peasants. The situation was exacerbated by a lack of appropriate land-use and forest policies. While the resettlement of rural populations may be, in principle, an efficient method of addressing imbalances between patterns of human settlement and available resources, the way it was implemented in the past in Ethiopia made it ineffective.

In its 1985 Ethiopian Highlands Reclamation Study, FAO recognized that isolated conservation measures are bound to be both highly costly and ineffective. The study suggested a broad-based development strategy (conservation-based development strategy or CDS) so that conservation measures are integrated into mainstream agricultural development activities at all levels (farm, agricultural, national).28

28 "The term Conservation-based Development implies not only the allocation of more resources for conservation but, even more importantly, ... the integration into agricultural and rural development objectives and criteria of improved land-using systems. This could result in a significant reduction, if not the removal, of absolute poverty." Executive Summary, p. 12, in FAO. 1985. Ethiopian Highlands Reclamation Study. Rome.Within the agricultural sector, the strategy identified proper farming and livestock management systems and practices to be promoted in each agro-ecological zone in the highlands. Emphasis was given to the provision of proper incentives for conservation and to proper relocation practices. The strategy recognized that agriculture cannot by itself solve all factors associated with degradation (such as low growth and poverty). It suggested that the links of agriculture with other sectors and complementary activities (small-scale industry, agroforestry, energy generation) be exploited to generate alternative income sources, especially in low-potential areas. At the national level, increased overall spending for agriculture was recommended in favour of the peasant sector; the need for an increased capacity of the ministries to carry out conservation programmes; and the full utilization of the capacities and skills of the private sector.

A number of policies included in the recommendations of the Ethiopian Highlands Reclamation Study have already been implemented (more secure tenure, more freedom for the private sector, voluntary resettlement and better incentives to farmers) but much more needs to be done. Land-use and forest resource policies are necessary prerequisites for a successful environmental resource conservation strategy. Accordingly, a forestry action plan is an important component of the national conservation strategy that the Ethiopian Government plans to complete by April 1994. Within a well-established set of rules for forest management and conservation, a greater role will be allowed for private sector participation in wood harvesting and processing. Incentives will be given to farmers and rural communities for reforestation and tree planting.

Regional overview

Bangladesh

Sri Lanka

Growing intraregional trade and investment flows

The challenges of economic transition

The environment and sustainable agriculture

Sectoral policies following macroeconomic and structural reforms

Asian and Pacific countries continued to show strong and steady economic growth in 1992. The Asian Development Bank (AsDB) estimates the average annual GDP growth rate for the region to be 7 percent in 1992, up from 6.3 percent in 1991. Despite the prolonged global recession, the AsDB expects regional GDP to increase by 7.2 percent in 1993. Three significant factors contributing to the region's ability to maintain this solid growth performance are: i) a continuing increase in disposable incomes, which is sustaining domestic demand; ii) the continuing expansion of intraregional trade; and iii) positive results from earlier policy reforms in many Asian economies.

Following are some individual country experiences in 1992:

· The output of China's industrial output increased by 20 percent in 1992, contributing to the country's impressive 12.8 percent increase in GDP. Even though drought affected many parts of the country, total grain production increased by 1.7 percent to an estimated 443 million tonnes. Tea, sugar, tobacco, fruit and vegetable production also increased compared with 1991 levels.Figure 7 ASIA AND THE PACIFIC - AGRICULTURAL AND PER CAPUT FOOD PRODUCTION· All of India's economic sectors improved in 1992 -the country's GDP increased by 4.2 percent. Agriculture, which was aided by a good monsoon, grew by 3.5 percent. Foodgrain production increased to a record 177 million tonnes compared with 167 million tonnes in 1991. However, heavy monsoon rains and floods in July 1993 are likely to have serious implications for this year's grain production.

· In Pakistan, a 30 percent increase in cotton production spurred agricultural GDP to a 6.4 percent increase in 1992. The large cotton crop is attributed to higher farmgate prices, a wider use of improved seeds and favourable weather. In contrast, Nepal experienced unfavourable weather in 1992. Its agricultural GDP increased by only 0.5 percent and foodgrain production declined by 6.5 percent.

· Southeast Asia reported mixed agricultural performances. Agricultural GDP increased by 3.5 percent in Thailand and 1.2 percent in Malaysia, but fell by 1 percent in the Philippines. In Malaysia, the production of palm oil, sawlogs, livestock and fish increased, while rubber and cocoa declined. In the Philippines, a severe drought reduced corn and rice production while the logging ban and related conservation measures curtailed forestry production in 1992.

· Viet Nam produced a record rice crop of 21.1 million tonnes, 1.2 million tonnes more than 1991. Total food production increased by 9 percent and agricultural GDP increased by 6.3 percent in 1992. Wide access to inputs and agricultural policy reforms are credited with improving yields and expanding area under cultivation. Laos' agricultural sector also recorded an outstanding year in 1992. Its agricultural GDP increased by 8.3 percent, with rice production growing by more than 20 percent.

Figure 7 ASIA AND THE PACIFIC - AGRICULTURAL TRADE

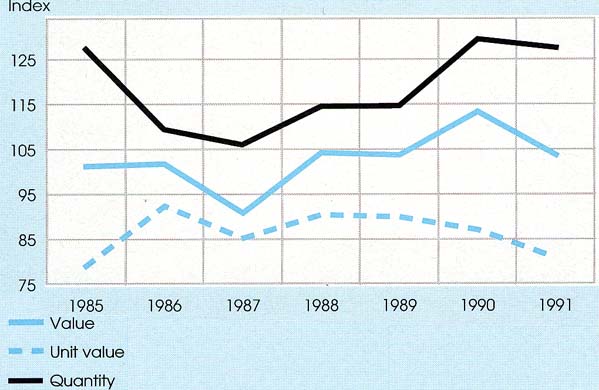

Figure 7 ASIA AND THE PACIFIC - AGRICULTURAL EXPORTS (Index 1979-81 = 100)

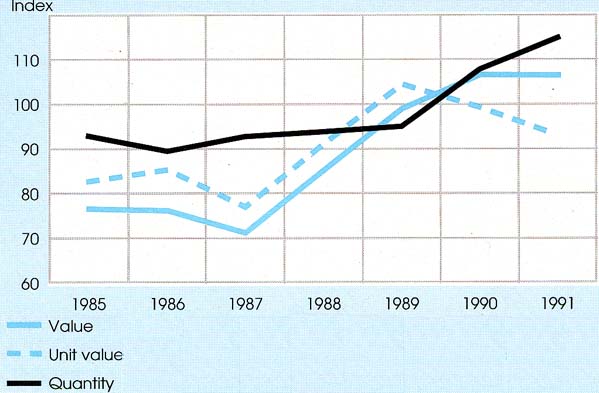

Figure 7 ASIA AND THE PACIFIC - AGRICULTURAL IMPORTS (Index 1979-81 = 100)

Despite a slow-down in the world economy in 1992, the international trade performance of the developing countries of the Asia and Pacific Region continued to be buoyant. Exports rose by 13 percent as a result of improvement in production efficiency, low inflation rates and favourable impacts of the policy reforms initiated in recent years.

One key factor sheltering the Asian economies from the global recession was the significant growth in intraregional trade and investment. In 1991, intraregional trade expanded by 23 percent compared with a 15 percent increase in exports to the rest of the world. This development is strongly supported by the ongoing regional division of labour, specialization and the relocation of production within the region in response to the opportunities offered by the various countries' relative factor endowments, macroeconomic policy environments and resulting comparative advantages.

In addition to large inflows of direct foreign investment, substantial flows of investment capital from Japan and newly industrialized Asian economies to the developing countries within the region continued. In particular, vast investment opportunities and the spectacular rate of growth in China attracted millions of dollars of investment by overseas Chinese.

The outcome of the ongoing Uruguay Round of multilateral trade negotiations (MTNs) is keenly awaited in view of its influence in shaping the application of the principles of non-discrimination and market access for exports from the region. The emergence of the North American Free Trade Association (NAFTA) is, however, viewed with some wariness because of the likely diversion of direct foreign investments from Asian countries.

Against the backdrop of these changes in the external environment, Asian countries have moved ahead with the creation and promotion of subregional trade arrangements. The member states of the Association of Southeast Asian Nations have launched the ASEAN Free Trade Area (AFTA) with a goal to remove tariffs on most commodities traded within the region in the course of the next 15 years. Likewise, the South Asian Association for Regional Cooperation (SAARC) summit in Dhaka earlier this year adopted a resolution to create a South Asian Free Trade Area (SAFTA). However, because of differences in size and the state of economic development between member nations, many difficult issues need to be resolved before these regional arrangements can emerge as an effective means for coordinated action.

During the past two years, the number of Asian countries undergoing transition from a centrally planned to a market-oriented economy more than doubled when six former Soviet Asian republics (Azerbaijan, Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan) joined China, Laos, Mongolia and Viet Nam in this process. There is considerable variation among these countries in terms of the problems of transition, approaches followed and the degree of success achieved. Most of them require structural transformation which can only be achieved over a number of years through persistent and consistent efforts. There are also problems of short-term stabilization and macroeconomic management as well as the need to create and strengthen institutions necessary for a market economy. Both problems seem to be more acute in the case of former Soviet Asian republics than others.

While, initially, all countries undergoing transition faced high inflation, unemployment and underemployment, China, Viet Nam and to some extent Laos have been able to reduce these by stimulating agricultural production, private investment and foreign direct investment. Mongolia and the former Soviet Asian republics, on the other hand, are facing severe shocks of transition.

For example, in 1992, in contrast to the economic growth of 12.8 percent and an inflation rate of 6.4 percent in China, Mongolia's real GDP fell by 7.6 percent and the inflation rate spiral led to 320 percent. In China and Viet Nam, the rural communities - whose production systems are based on the household unit and are equipped with labour-intensive technologies -responded well to market signals. In contrast, farming communities in Mongolia and the former Soviet Asian republics, which have a longer tradition of communal farming using heavy equipment and depending on input supplies from state enterprises, face more difficulties in adapting to the new situation. It also appears that, in the latter group of countries, price liberalization did not bring about the expected supply response because of a monopolistic control over inputs and the tendency of the monopolistic enterprises to curtail production and raise prices.

Judging by the experience of some countries in transition (China and Viet Nam), which suffered initially from short-term macroeconomic instability and inflation, it appears that an appropriate institutional structure is equally as crucial as macroeconomic stability for a successful transition. The transition process requires the public sector and foreign donors to have an active supporting role in creating and consolidating a favourable policy framework and institutional environment that will enable the efficient functioning of a market economy.

In addition, improvements are essential in the government's capacity to deliver public goods (research, extension, transport and communications infrastructure, health, education and other social services), which remain in the domain of the public sector even in a highly developed market system.

Rapidly increasing population pressure, urbanization, the excessive use of chemicals in production processes and the unsustainable use of natural resources are contributing to serious water and air pollution, deforestation, soil erosion, desertification and flooding throughout the region.

While the improved seed and fertilizer technology, complemented with a vast expansion in irrigation facilities, removed the spectre of hunger from many populous Asian countries, in some cases it also added to environmental degradation. Moreover, maintaining or raising the present yield levels demands a more intensive use of natural resources, which has adverse environmental consequences. For the Pacific countries, global warming and the resulting rise in sea level are the most serious, although uncertain, environmental threats. The externalities involved with these types of environmental issues require concerted group actions by the international community.

Developing Asian countries have realized the close connection between rural poverty and environmental degradation. Increasing population pressure on agriculture, the result of inadequate growth in off-farm employment opportunities and a lack of access to yield-improving technologies, is forcing many Asian farmers to cultivate marginal lands and overuse other natural resources for their immediate survival. In many Asian countries that are striving for equitable and sustainable development, poverty alleviation is a core element of the national development plan.

Many countries are grappling with the complex task of achieving poverty alleviation and environmental protection goals within a somewhat conflicting framework, containing socio-political commitments to achieving equity as well as market liberalization policies aimed at resolving macroeconomic imbalances. It is argued that market-based policy instruments emphasizing the removal of input subsidies, output support prices and protective tariffs may act as a two-edged sword. While tending to discourage uneconomical and unsustainable input use, with positive effects on the environment and the evolution of sustainable farming practices, these policies tend to increase food prices, consequently having negative income effects on the poor, who often are net buyers of food, and thus mitigating the achievement of poverty alleviation goals in the short term. Policy formulation in such situations may call for a compromise between economic efficiency and a pragmatic understanding of the short-term socio-economic political situation.

Finally, the cost of reversing environmental degradation is very high. For most developing Asian countries, investing in such activities would entail drawing resources away from other important development projects. It has also been realized that preventing environmental damage costs less than restoring the loss. Thus, there is an increasing emphasis on the incorporation of environmental considerations in policy formulation as well as in development project selection and the evolution of appropriate production systems.

Having established a growth-oriented macroeconomic policy framework in the course of implementing stabilization and structural adjustment programmes, a number of market-oriented Asian countries, such as Bangladesh, Indonesia and the Philippines, have moved on to sectoral reforms. It is realized that the macroeconomic policy reforms cannot be fully effective in improving efficiency and unleashing the farmers' production potential unless sectoral constraints on growth are tackled.

A comprehensive package of agricultural sectoral policy reforms generally consists of the withdrawal of input subsidies, the dismantling of expensive public food distribution systems and the removal of subsidized credit and protective tariffs as well as other barriers. It also entails freeing import restrictions, encouraging private sector participation and investing in infrastructure to promote the efficient operation of market mechanisms.

The task of designing efficiency-oriented equitable agriculture sector policies is not easy, however. Among other things, policy-makers have to take into account the differential impacts of sector policy changes on various sections of society as well as dealing with diverse coalitions and interest groups who react differently to policy changes. These reforms are therefore being carried out selectively and in sequence, with due consideration given to the socio-political realities of the countries concerned. For example, in some cases fertilizer subsidies have been gradually reduced (in India and Indonesia) while an active public sector role in foodgrain procurement, distribution and buffer stock management has been maintained.

In some Asian countries, the reluctance to carry out agricultural sectoral policy reforms seems to have been reinforced by the delayed finalization of the Uruguay Round of GATT negotiations as well as by protective trade policies and trade blocks outside the region.

The agricultural sector

Rice and foodgrain policies

With an estimated per caput GNP of $225 in 1992, Bangladesh is among the poorest countries in the world. Moreover, with approximately 115 million inhabitants and 149 000 km2, the country is three times more densely populated than India and seven times more than China. This intense population pressure on a relatively narrow resource base, together with the frequent natural disasters suffered, present formidable challenges to poverty alleviation efforts in Bangladesh.

Over the years, floods, droughts and cyclones have undermined progress and hampered the country's efforts to stimulate growth and reduce poverty. Cyclones and resulting storm surges are particularly destructive. The Bay of Bengal is the most cyclone-prone area in the world, having been hit by 15 cyclones during the past 25 years. These natural disasters cause immeasurable human suffering, devastate large crop areas and destroy property and infrastructure. The government estimates that the cyclone of April 1991 killed approximately 140 000 people. Such disasters impede economic and social progress by diverting attention and resources away from development programmes and towards crisis management.

Despite all these obstacles, Bangladesh has made significant economic progress over the past decade. The country has reduced external and internal deficits, stabilized the inflation rate, promoted non-traditional exports and achieved a modest growth rate. Stabilization policies have helped lower the budget deficit from about 8 percent in 1990 to 5 percent in 1992. The inflation rate fell to around 5 percent in 1992, the lowest rate in more than ten years. Real GDP growth during the period 1990-92 has been in the range of 3.5 to 6.5 percent and is forecast to be 5 percent in 1993.

Bangladesh has also initiated a number of structural reforms in the industrial and financial sectors, public enterprises and trade and exchange rate policy. Financial sector reforms include abolishing credit ceilings and increasing reliance on cash and liquid asset reserve requirements to regulate liquidity. Public enterprises are being given more administrative and managerial autonomy. Trade policy is shifting from import substitution to export promotion; a tariff system is replacing prohibitions and quantitative restrictions on imports.

Perhaps even more important to the overall economy are the agricultural policies, programmes and projects that have expanded the use of high-yielding variety (HYV) rice seeds, fertilizers and shallow tube wells for irrigation. As a result, rice production has increased by more than 40 percent in the past ten years. Today, Bangladesh is close to self-sufficiency in rice and, for the first time in the country's history, the government is discussing the possibility of exporting rice.

In addition to the stabilization programme and economic policy reforms, human resource development and poverty alleviation remain top priorities. Public spending on health care, primary education and family planning increased in real terms in 1992. Food distribution programmes aimed at vulnerable groups and the poor are being overhauled to reduce costs, increase efficiency and improve coverage.

Many human development programmes have proved successful in Bangladesh. For example, family planning efforts have resulted in a lower population growth rate which is currently down to 2.1 percent. At the same time, the country still has a low literacy rate (around 35 percent), a low primary school enrolment rate (72 percent) and a low life expectancy (56 years). Moreover, half of total mortality is due to child death below the age of five years, of which more than half is due directly or indirectly to malnutrition. Household food security is another persistent problem; half the households in Bangladesh cannot afford an adequate diet and an estimated 22 to 30 percent of the population lives in dire poverty (less than 1 805 kcal per caput per day).

The agricultural sector is Bangladesh's largest source of income, employment, savings and investment. Agriculture accounts for about 40 percent of GDP and more than 60 percent of employment. Rice not only dominates all other agricultural products, it also dominates all other economic activities. Production, trade, processing and transportation of rice amount to more than 25 percent of the country's GDP. Rice represents 75 percent of the cropped area, 95 percent of foodgrain production, about 80 percent of caloric intake, 60 percent of protein intake and about 30 percent of total household expenditures - the weight of rice in the consumer price index (CPI) is about 60 percent. For these reasons, policies that affect rice production, trade and consumption have a profound impact on Bangladesh's entire population.

Over the past two decades, rice production and distribution policies have adjusted with changing economic circumstances and pressures. The growth in rice production is attributed primarily to policies that encouraged wider use of new irrigation technology, HYVs and mineral fertilizers. The introduction of tube well irrigation, particularly low-cost shallow tube wells, is the main reason for the rapid expansion of total irrigated area and the shift away from traditional irrigation methods.

Rice production. During the 1980s, the area under shallow tube well irrigation expanded annually by nearly 30 percent, increasing from 227 000 ha in 1981 to 1.8 million ha in 1991. Today, tube wells account for 55 percent of the 3.3 million ha under irrigation, compared with 14 percent in 1980. Moreover, tube well irrigation has encouraged more rice production in the dry season and less in the early monsoon season. In 1992, irrigated dry season rice accounted for 37 percent of the record harvest (18.25 million tonnes) compared with 20 percent in the early 1980s. In contrast, the total area planted to rice during the early monsoon season declined from 3.2 million ha in 1982 to 1.9 million ha in 1992.

Initially, government policies encouraged rice production through the direct provision of irrigation equipment. During the 1970s and 1980s, the Bangladesh Agricultural Development Corporation (BADC) monopolized imports and domestic distribution (sales and rentals) of all irrigation equipment. An increasing number of procedural difficulties, however, led to a series of policy changes in 1989. These changes included: restructuring the BADC's tube well sales practices; allowing the private sector to import and market tube wells; and eliminating licensing requirements for shallow tube wells (many restrictions still apply to deep tube wells).

The resulting increase in access to and availability of irrigation equipment, combined with lower prices, contributed to a rapid expansion in tube well irrigation. Half of the 40 000 units sold in 1989 came from the private sector. In the three-year period from 1989 to 1991, the irrigated area expanded by almost 700 000 ha, which is more than the total irrigated area added during the previous eight years.

Other production policies provided a guaranteed floor price as well as subsidized inputs, including HYV seeds, credit, pesticides and fertilizers. In recent years, the government has removed subsidies on fertilizers and allowed private sector imports and sales of mineral fertilizers, even though it remains the sole domestic producer of most types of fertilizers.

Rice and foodgrain distribution. To ensure an affordable food supply for poor consumers, the government manages a variety of food distribution programmes and open market sales operations to help stabilize foodgrain prices. Public food distribution programmes provide approximately 13 percent of all foodgrains consumed in the country.

Past policy measures aimed at foodgrain distribution and prices include: a ban on exports; a monopoly on imports; restrictions on the movement and storage of rice; prohibitions against extending bank credit for rice storage; open market sales of wheat and rice at predetermined ceilings during times of price peaks; and public sector procurement at predetermined floor prices in the postharvest season. The objectives of price stabilization policies are to protect poor consumers from sharp price increases, protect poor farmers from a postharvest price collapse and achieve foodgrain self-sufficiency.

The public food distribution programmes include disaster and famine relief, seasonal food-for-work development projects and year-round rationing. Many food distribution programmes and food policies have recently been restructured, reformed or eliminated. For example, in August 1992, the government allowed private sector imports of foodgrains for the first time. Private traders responded by importing more than 300 000 tonnes of wheat by the end of the year.