CEREALS

Tight supplies keep prices high but improved production prospects could lead to lower prices

|

|

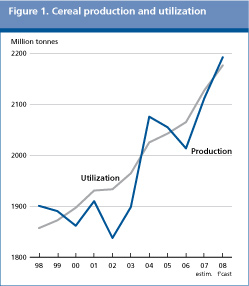

FAO's latest forecast for world cereal production in 2008 points to a record output, now put at nearly 2 192 million tonnes (including rice in milled terms), up 3.8 percent from 2007. Unlike in the previous year when maize accounted for most of the increase in world cereal production, wheat is expected to be the main protagonist this season with its production expanding by as much as 8.7 percent. High wheat prices during the 2007/08 season have boosted plantings, which combined with generally favourable weather conditions, are the main factors for an expected record wheat crop this year.

In spite of the strong growth in world cereal production in 2008, total cereal supplies in 2008/09 are likely to remain tight given the critically depleted levels of carryover stocks combined with continued strong demand. Total cereal utilization in 2008/09 is forecast to rise by 2.3 percent from 2007/08 to 2 176 million tonnes, which would be nearly 2 percent above the ten-year trend. The increase in world cereal utilization reflects a sustained growth in food, feed and industrial utilization of cereals. Maize-based ethanol production is likely to continue its strong growth in the new season, accounting for almost 20 million tonnes, or nearly one-half of the overall anticipated increase in total cereal utilization in 2008/09.

In 2008/09 world cereal production is forecast to exceed total utilization for the first time in three seasons, and because of this, some recovery in global stock levels is possible. World end-of-season cereal stocks for crop years closing in 2009 are currently forecast to increase by 3 percent (or 12.5 million tonnes) from their 30-year low opening level, to 421 million tonnes. As a result of this modest recovery, world cereal stocks-to-use ratio in 2008/09 would reach 19.5 percent, slightly up from the 2007/08 low.

International trade in cereals in 2008/09 is forecast to fall to close to 252 million tonnes in 2008/09. This represents a sharp decline (10 million tonnes, or 4 percent) from the record in 2007/08. Lower trade in maize accounts for most of the contraction while trade may recover in the case of rice and increase slightly in the case of wheat.

The FAO Cereal Price Index averaged 284 in April 2008, up 20 percent since January and 92 percent more than in April 2007. While wheat prices have demonstrated some signs of weakness in recent weeks, in the maize market, prices have received support from strong demand and concerns about this year's crop in the United States. International rice prices have increased sharply in recent months mainly as a result of export restrictions by key rice exporters.

| |

2006/07 |

2007/08 |

2008/09 |

Change: 2008/09 over | | | |

estim. |

f'cast |

2007/08 | | |

million tonnes |

% | |

WORLD BALANCE | | | | | |

Production |

2 013.3 |

2 111.9 |

2 191.9 |

3.8 | |

Trade |

255.5 |

261.9 |

251.8 |

-3.9 | |

Total utilization |

2 064.8 |

2 127.2 |

2 176.0 |

2.3 | | Food | 994.0 | 1 006.6 | 1 002.1 | 1.5 | | Feed | 741.4 | 756.8 | 760.3 | 0.5 | | Other uses | 329.3 | 363.8 | 393.5 | 8.2 | |

Ending stocks |

427.2 |

408.8 |

421.3 |

3.1 | | | | |

SUPPLY AND DEMAND INDICATORS | | | Per caput food consumption: | | | |

| | World (kg/year) | 152.3 | 152.4 | 152.2 | -0.1 | | LIFDC (kg/year) | 157.0 | 157.1 | 157.1 | 0.0 | | World stock-to-use ratio % | 20.1 | 18.8 | 19.5 | | | Major exporters' stock-to-disappearance ratio % | 14.5 | 12.6 | 14.0 | | | | | | | | | |

2006 |

2007 |

2008 |

Change:

Jan-Apr 2008 | | | | | |

over

Jan-Apr 2007 | |

FAO Cereal Price Index | | | | % | | (1998-2000=100) | 123 | 170 | 271* | 83 |

* Jan-Apr 2008

|

June 2008

June 2008