November 2008 November 2008 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

MARKET SUMMARIES

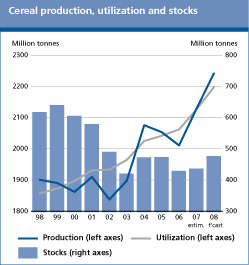

World cereal production is expected to hit a new record in 2008 as high prices boosted plantings and weather conditions were generally favourable. World cereal production is forecast to be large enough to meet the anticipated utilization and also allow for some replenishment of the much depleted global reserves. This prospect has already led to a sharp drop in international prices of most cereals from their peaks during the first half of 2008. However, the pace and the extent of the price declines, particularly in recent weeks were also influenced by the crisis in global financial markets and falling crude oil prices. These developments have added much uncertainty as to the future of price levels and raised the worrying possibility that plantings for the next season may be negatively affected. Farmers already burdened by the high cost of inputs may be less willing to expand or even keep up with production next year. Although by no means a certainty, such a scenario could well materialize and calls for caution when interpreting this seasons ongoing recovery in supplies. It is important to recall that the world harvested a record cereal crop also in 2007 and yet international prices soared and many countries faced severe food crises. The underlying factor behind the price surge in 2007/08 was the reduction in overall supplies in several exporting countries that had harvested smaller crops, while others restricted exports for fear of food shortages. If prices were to remain depressed in 2008/09 and plantings for next year are affected, a similar, if not more pronounced, price surge may be witnessed in 2009/10, unleashing even more severe food crises than those experienced in the current season.

World cereal market at a glance 1

* Jan-Sept 2008

1 Rice in milled equivalent

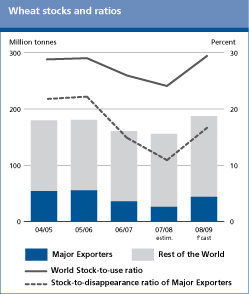

In sharp contrast to the previous season, the 2008/09 marketing season is marked with ample export supplies, a significant recovery in world inventories and falling international prices. World wheat production is forecast to hit a new record following larger crops in Europe, North America and Oceania. Brighter global supply prospects in exporting countries and lower international prices are likely to boost international trade in 2008/09 to an all time high. Demand is likely be underpinned by strong growth in feed wheat utilization.

World wheat market at a glance

* Jan-Oct 2008

Derived from IGC Wheat Index

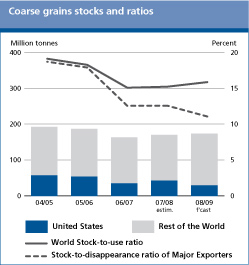

World production in 2008 is forecast to increase more than enough to meet the expected utilization, paving the way for a small recovery in inventories. World trade in 2008/09 is forecast to contract, after peaking to a record volume in 2007/08. The bulk of the reduction in trade would result from a scaling down of maize and sorghum imports, mostly because of large supplies of alternative substitutes for feed, such as feed wheat. Another emerging feature is the sharp decline in international prices, reflecting not only the reduction in demand but also the steep fall in crude oil prices and developments in financial markets.

World coarse grain market at a glance

* Jan-Oct 2008

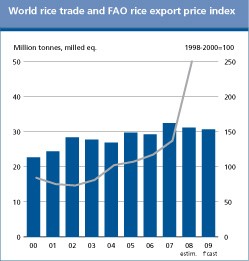

International rice prices have weakened since May, depressed by the arrival of new crops and by prospects for a new paddy production record in 2008. The price drop has been relatively contained, being less pronounced than the falls witnessed in wheat and maize prices. While rice quotations still remain substantially above one year ago, the situation may not persist, especially if those countries that still impose restrictions on exports lift them in the next few months. This, together with a stronger United States Dollar and the expected negative impacts of the financial crisis on import demand may accelerate the price slide in the coming months. Although less expensive rice on world markets should have boosted import demand in 2009, the uncertainty arising from the financial crisis has marred expectations for trade next year. Given new difficulties that traders may face in accessing credit for importing, the volume of rice trade is now anticipated to contract in 2009. The expansion in production and decline in world prices should ease the situation that faced consumers earlier this year and sustain an increase in average per caput consumption in 2009. The increased output should also allow for a rise in global rice inventories to their highest level since 2004.

World rice market at a glance

Note: Refer to table 4 for further explanations regarding definitions and coverage.

* Jan-Oct 2008

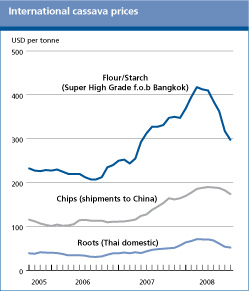

Global cassava production is set to reach an all-time high in 2008, driven by endeavours to sustain food security in the wake of high and protracted cereal prices and also to expand supply to meet the needs of the ethanol sector where cassava forms energy feedstock. The world market for cassava products could undergo a considerable contraction by the end of the year, as the recovery in global grain supplies has eroded the price advantage that cassava previously maintained over grain substitutes. Falling crude oil prices could also thwart an anticipated expansion in international demand for cassava in energy production. After reaching record levels, world prices of cassava products have fallen rapidly in recent months, principally on the back of faltering demand in major import destinations. The near term outlook appears bleak. Cassava product prices will need to fall considerably further to enable them to become competitive with grains. Falling world oil prices will also require cassava prices to decline or to be subsidized by governments for it to remain a viable alternative feedstock in energy production.

World cassava market at a glance

* Source: Thai Tapioca Trade Association

Market fundamentals in the oilseed complex are anticipated to remain relatively tight during the 2008/09 season. Although global oilcrop production is anticipated to rise, supply growth will be constrained by very low opening stocks. Demand for oils/fats is forecast to expand further, also thanks to biofuel production, while growth in meal consumption could be constrained by ample availability of feedgrains and subdued feed demand by the livestock sector. Under current forecasts, the global 2008/09 stock-to-use ratio for both meals and oils/fats is set to recover only in part, which suggests that the recent decline in oilseed, oil and meal prices may come to an end and even rebound later in the season. The course of prices remains strongly contingent upon the development of oilcrops in South America. Other sources of market uncertainty lie in the evolution of energy prices, potential adjustments in national biofuel policies and the possibility of a general economic recession, on the trail of the current financial crisis. With regard to trade, the 2008/09 season is expected to stand out for a slowdown in oilseed, oil and meal transactions.

World oilseeds and products markets at a glance

Source: FAO

Note: Refer to footnote 2 in the text of the market assessment for further explanations regarding definitions and coverage. 1 Includes oils and fats of vegetable and animal origin. 2 Production plus opening stocks. 3 Residual of the balance. 4 Trade data refer to exports based on a common October/September marketing season. 5 All meal figures are expressed in protein equivalent; meals include all meals and cakes derived from oilcrops as well as fish meal. * Jan-Oct 2008

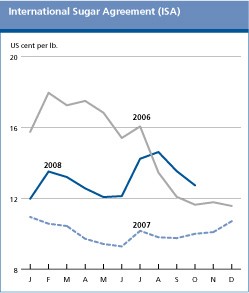

World sugar production is forecast to decline in 2008/09 from the record level in 2007/08, largely driven by a sharp decrease in India, the European Union, and Pakistan. In general, the contraction of production would be the result of reduced plantings, as many producers switched to alternative crops such as maize and soybeans, led by expectations of better returns. By contrast, world consumption is foreseen to increase at a sustained rate, propelled by strong demand by the developing countries. As a result, consumption is expected to outstrip production in 2008/09, which should lead to a reduction in the large global inventories that have been hanging over the market since 2005/06. World trade is forecast to expand in 2008/09, reflecting greater imports, notably by the European Union, where a shift in policies has curbed domestic supplies. The prospect of a tighter market could provide some support to prices later in the season, although recent currency exchange rates movements, developments in the oil price market and global financial turmoil may all work to prevent a sustained price recovery in 2008/09. Meanwhile, international sugar prices have been very volatile and falling since August, even though on average they have strengthened substantially compared with the depressed levels in 2007.

World production and consumption of sugar

* Jan-October 2008

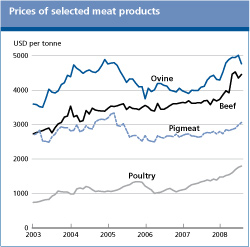

Global meat output is expected to stagnate in 2008, largely reflecting a contraction in China, where the sector was hit by animal diseases, harsh weather and natural disasters. Production may resume growth in 2009, buoyed by continuous strong demand in Asian developing countries and an expected decline in feed costs. All of the production increase is expected to arise in the developing countries, particularly in Asia, with Chinas production recovering. South America is also expected to contribute to the global meat production expansion, following European Unions recognition of Brazil major beef producing states as free of Foot-and-Mouth Disease (FMD). Prices of meat rose throughout 2008 until they peaked in August, but have shown signs of weakness in September. This was reflected in the FAO International Price Index of Meat Products, which fell from 146 points in August to 140 points in September. However, prices remain far higher than last year. For 2009, expanding demand in the developing countries is likely to sustain a small increase in global meat consumption. Part of the increased demand will be met through imports, especially of lower valued meat products. As a result, global trade in meat products is anticipated to increase by close to 3 percent in 2009.

World meat markets at a glance

* Jan-Sept 2008

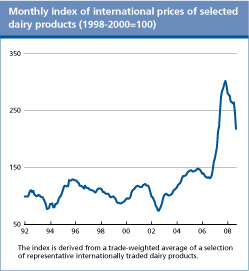

The price spike in international dairy markets, which, as measured by the FAO Dairy Price Index, peaked in November 2007, has ended. Over the first half of 2008, dairy product prices, particularly those with high protein content, have declined significantly and, in the context of high production costs, profitability has turned negative, particularly in feed-grain intensive dairy sectors. Increased supplies, weaker international demand and an appreciating United States Dollar may depress milk product prices further in the next six months, with export quotations nearing, or falling below European Union intervention support levels. Global milk production is expected to expand by 2.2 percent in 2008 and by a further 2.5 percent in 2009, reflecting continued growth in Asia and, especially, in South America. The recent melamine contamination incident in China is affecting markets, particularly in Asia and, for the first time in a decade, China may record a single digit growth rate in milk production in 2008. Dairy product trade is set to grow modestly this year, as export supplies increase, particularly for cheese and whole milk powder.

World dairy markets at a glance

* Jan-Sept 2008

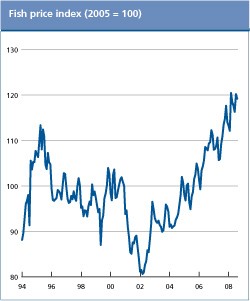

Global fish production is forecast to increase by only 1 percent in 2008, sustained by firm growth in aquaculture. By contrast, a contraction is anticipated in the capture fish sector, which may be depressed by high fuel prices, but also by the precarious state of stock resources, which has reached critical levels for many species. Fish consumption as food is set to increase in 2008, although consumers are expected to shift towards lower priced products. A fall in fishmeal production may constrain the utilization of fish-derived products in animal feed. Trade in fish products has held up fairly well so far in 2008, except for fishmeal, which may be traded in smaller volumes. As a result, overall trade in fish may contract by about 1 percent in 2008. However, import demand has been weakening in all major markets and prices for most products are reported falling in 2008, although given the extreme fragmentation of world fisheries market, a few prices have strengthened, in particular those from capture fisheries such as groundfish and yellowfin tuna.

World fish market at a glance

1 Production figures for 2006 and 2007 have been changed to reflect a downward revision in Chinas production estimates

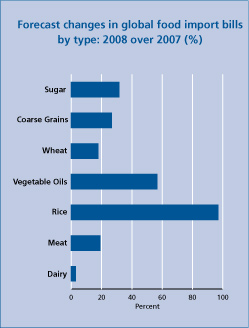

Falling food prices and freight costs fail to dent a USD 1 trillion bill in 2008 As 2008 draws to a close, the global cost of imported foodstuffs in 2008 is increasingly likely to break the USD 1 trillion barrier. The prediction comes in spite of sharp falls in freight rates and pervasive declines in international prices of foodstuffs that began mid year and accelerated thereafter. At USD 1 019 billion, the total food import bill facing the world would be some 23 percent higher than in 2007 and 64 percent the year before that. Of the estimated USD 200 billion or so global increase from 2007, vegetable oils could account for over one-third of the rise and coarse grain based foodstuffs for about a quarter. In fact, with the exception of sugar, expenditures on imported food by commodity group are all estimated to reach unprecedented high levels. International quotations, which even in the face of recent declines, remain much higher than last year constitute the main driver of record import bills in 2008. Freight charges have also been a factor, despite the near collapse in quotations in recent months. Hitherto, freight costs had been soaring, reaching unparalleled levels in mid 2008, adding on average roughly 10 percent to import expenditures since last year. The third variable in the import equation volume - has held remarkably firm in the wake of such high unit costs. The global market for wheat, vegetable oils, meat and dairy products all should experience record traded volumes in 2008, while world trade in rice and coarse grains could all but register the highest levels, bar 2007. Such resilience bears testimony to the importance of trade to assure food consumption around the world. However, the global picture masks significant difficulties that vulnerable countries are likely to endure. Record increase in food import bills of the worlds poorest countries Among economic groups, developing countries look set to bear the brunt of escalated food import costs. The burden of purchasing food on the international market place for the most economically vulnerable groups, LDCs and LIFDCs, is set to soar by around a third each from last year. This would stand as the largest year-to-year increase on record. Bills in sub-Saharan Africa could rise in slightly less proportion, but again, the annual rise would constitute a record for the region. The sheer encumbrance facing some of the worlds poorest countries in importing food can be contrasted against that of richer nations, whose food import bills are likely to rise by only 18 percent from 2007. Rising food import bills do not necessarily result in more imported food. Numerous LDCs and LIFDCs are expected to curb procurement of basic foodstuffs from international markets, a response that does not always reflect improved domestic supply prospects. The world will look towards 2009 for respite given the outlook for further declines in international prices and freight costs. But the prospect of lower food import expenditures for many countries, especially the poorest, could be undermined by the crisis in global financial markets, as they may find it harder to secure finance for their imports. Forecast import bills of total food and major foodstuffs (USD million)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |