November 2008 November 2008 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

RICE

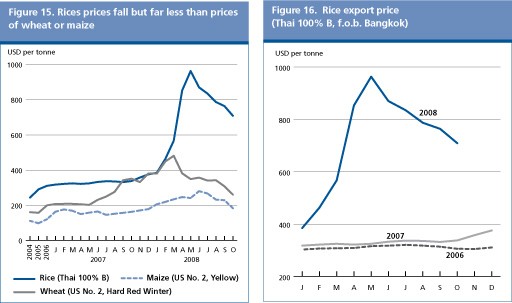

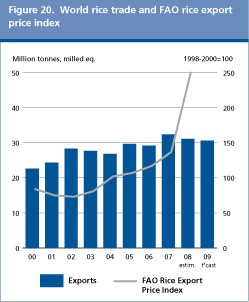

World rice prices under strong downward pressure The tightness that dominated the international rice market in the first half of 2008 has been easing since June, when new rice supplies became available from the secondary 2007 crops. The turnaround manifested in a steady tendency for world rice prices to fall from their nominal peaks in May, pressuring the FAO all rice price index (1998-2000=100) downwards to 253 by October 2008, 21 percent below the May 2008 high. The strengthening of the United States Dollar, which gained on average 10 percent against major currencies between mid-June and mid-October also contributed to the dip in prices. So far, however, international rice quotations have held much better than those of wheat or maize and are still more than 78 percent above their value in October 2007. The slide has been limited so far by policies in place in several exporting countries, in particular export restraints in Egypt and India and government domestic procurement in Thailand. It is noteworthy, however, that the steady decline in prices is leading governments to shift their focus from consumers to producers, in sharp contrast with actions taken in the first half of the year, when domestic food inflation was at the centre of their attention. As a result, several of them are actively intervening to sustain farm prices.

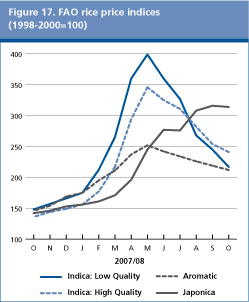

Among the various rice types and qualities, those which have endured the largest declines have been the lower and higher qualities of Indica rice, which retreated by 46 percent and 30 percent respectively from May to October this year. Weaker import demand also depressed quotations of aromatic rice varieties by 16 percent over the same period. By contrast, the unavailability on the international market of Australian and Egyptian round rice varieties lent further support to Japonica rice prices, which have gained 28 percent since May. Despite the recent general price dive, rice remains far more expensive on world markets than it was one year ago. Compared with October 2007, prices are 77 percent higher for Higher Quality Indica, 47 percent for Lower Quality Indica, 45 percent for fragrant rice and as much as 121 percent higher in the case of Japonica rice.

Under current rice supply and demand prospects, world rice prices could decrease further, especially within the context of falling prices of other cereals There is also much concern about the possible negative impacts of the world-wide financial crisis on rice import demand on trade.

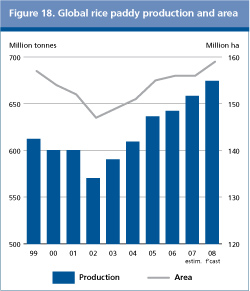

Global paddy Production heading towards a new height in 2008 The 2008 paddy season is approaching the critical year-end period, when major rice producing countries harvest their main crops. With the progressing of the season, prospects have greatly improved from the early assessment made in June and global paddy production is now set to reach 674 million tonnes (equivalent to 450 million tonnes of milled rice), 16 million tonnes or 2.4 percent above the excellent performance of 2007. Favourable growing conditions and improved economic incentives, which have encouraged farmers to expand plantings, lie largely behind the expectations of strong gains. It is important to note, however, that the full 2008 paddy season will only be concluded when the 2008 secondary crops are gathered in the northern hemisphere, around May next year. Given the current tendency for world prices to weaken and the difficulty to secure finance for production, processing and trade, there is much uncertainty as to how much land will be seeded with rice over the coming months. However, based on current expectations, production is forecast to expand in virtually all regions, although developed countries as a group may incur a fourth consecutive contraction. Globally, the area under rice is forecast to rise by 1.5 percent to 158.6 million hectares, and yields by close to 1 percent to 4.3 tonnes of paddy per hectare.

Asian countries are set to drive production up this season, as they are expected to reap 611 million tonnes of paddy (408 million tonnes of milled rice), about 13 million tonnes more than in 2007. Large absolute gains are anticipated in all the leading producing countries, such as Bangladesh, Mainland China, India, Indonesia andViet Nam, but also in Cambodia, Pakistan, the Philippines, Sri Lanka and Thailand. A recovery is expected to take place in the Chinese Province of Taiwan, the Democratic People’s Republic of Korea and in the Republic of Korea, affected last season by excessive precipitation and flooding problems. On the other hand, production in Myanmar may be curbed by more than 2 million tonnes following the destruction and disruption of agricultural activities caused by the landfall of cyclone Nargis in May 2008. Smaller crops are also expected in Afghanistan, Iraq and the Islamic Republic of Iran, which have all endured persistent drought problems. Production may also fall in Japan, under the government policy to cut excess supply. With favourable growing conditions prevailing so far in Africa, production in the region is forecast to expand by 7 percent to a record of 24.5 million tonnes, driven by progress in Egypt, Madagascar, Mali and Nigeria. However, the increases are expected to be widespread across the region, a sign that producers have responded positively to the attractive market conditions and to government incentives, which have mainly taken the form of fertilizer subsidies. Indeed, various endeavours to sustain rice production in the region have been launched at the national and international levels, including an Emergency Rice Initiative for Africa, in June 2008. Production in Latin America and the Caribbean (LAC) may stage a remarkable increase of 7 percent, much of which concentrated in Argentina, Brazil, Colombiaand Uruguay, a reflection of favourable weather conditions and high prices. On the other hand, the various hurricanes that have battered Central America and the Caribbean since August are likely to depress output in Cuba, the Dominican Republic and Haiti. In the rest of the world, although hurricanes also hit some rice growing areas in the United States, the USDA outlook still points to a 3 percent gain this season, but prospects by the Rice Federation are less optimistic. In theRussian Federation, high prices are expected to boost production, while a decline is foreseen in both Australiaand the European Union.

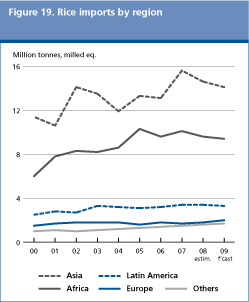

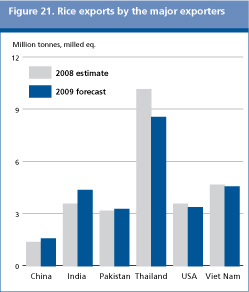

Trade in rice contracts in 2008 as export restraints reduces availabilities FAO’s forecast of global rice trade in 2008 has been raised to 31.0 million tonnes, after several exporting countries eased somewhat the restrictions on exports they had imposed earlier this year. At that level, trade in rice would be 4 percent lower than the 32.3 million tonnes now estimated to have been traded in 2007, but still the second highest level on record. High world prices and difficulty to secure supplies were much behind the expected retrenchment of rice imports, especially by Asian and African countries. In Asia, much lower purchases are expected to be made this year by Indonesia, which harvested a bumper crop this season, and by Nepal, Saudi Arabia, the United Arab Emirates and Yemen, while larger imports are anticipated in Bangladesh, Iraq, the Democratic People’s Republic of Korea, Malaysia and the Philippines. High world prices are set to depress total shipments to African countries, in particular, Guinea, Senegal and South Africa. Having used an export ban to keep domestic inflation in check, the Government of Egypt, which imported around 100 000 tonnes in 2007, has also largely withdrew from the import side of the market this year. By contrast, the suspension of the the over 100 percent tariff in Nigeria is anticipated to boost deliveries to the country. Imports to countries in LAC are unlikely to change much overall, with some declines expected in Colombia, Mexico and Nicaragua compensated by increases in Bolivia, Ecuador, Haiti and Panama. By contrast, Australia, the European Union and the United States are all expected to purchase more. Much of the anticipated drop in world exports in 2008 largely reflects the restrictive export policies that have been implemented by numerous countries in the course of the year. While most of them have lifted those curbs, Egypt still maintains a ban, while India’s restraints on non-basmati rice exports have only be relaxed for a number of government-to-government transactions. As a result, shipments from both countries are expected to decline substantially. Some contraction is also anticipated in China and Guyana. Only part of the shortfalls is foreseen to be offset by the other exporting countries. Thailand, in particular is now set to ship over 10 million tonnes, matching the 2004 record, but Cambodia, Pakistanand the United States are also anticipated to boost external sales this year. Small increases in exports are expected for Argentina, Brazil and Viet Nam.

Prospects for a recovery of rice trade in 2009 marred by the global liquidity crunch Although very preliminary, FAO’s forecast of global rice trade in 2009, at 30.4 million tonnes points to a 1.6 percent contraction from 2008, equivalent to some 500 000 tonnes. The anticipated weakening of world prices should allow for the recovery in the volume of trade in 2009, but amidst bleaker economic growth prospects arising from the global financial crisis, the beneficial price effects on rice import demand are now anticipated to be diminished. This would be a result of falling household incomes, higher risks and costs in trading on the international market place plus growing difficulties for governments and importers to obtain credit and foreign exchange necessary to finance their rice purchases. Thus, unlike in 2008, when exporter policies were largely responsible for an expected fall in rice trade, the reason for the expected contraction next year may well lie on the importer side.

Imports by African countries are expected to be particularly affected next year by the economic downturn. The importation of rice by the region is principally under the control of the private sector, which could well be more exposed to the risks of a global tightening of liquidity than state trading enterprises. As a result, many African countries are expected to cut their imports compared with 2008 even under the prospect of falling international prices. The restoration of import duties in Nigeria could also depress the inflow of rice to the region in 2009. Shipments to Asian countries may also be reduced in 2009, much on account of Bangladesh, Malaysia and the Philippines, which may import less after having purchased large supplies over the current year, either domestically or abroad, to rebuild their rice reserves. By contrast, the Islamic Republic of Iran, Iraq and Nepal are expected to step up their purchases, in light of relatively poor paddy crops in 2008 and rising domestic requirements in 2009. Imports by Saudi Arabia, the United Arab Emirates and Yemen could also rebound, as access to their traditional supply sources (mainly India) is likely to be restored. Deliveries to countries in LAC could fall slightly, on account of smaller purchases by purchases by Brazil and to a lesser extent by Haiti and Jamaica. By contrast, rice inflows to the European Union and the United States are forecast to rise, assisted by an expected return to more normal world prices levels. Much of the contraction in world exports in 2009 is expected to stem from reduced deliveries by Thailand, where the pledging programme could sustain prices in the country well above those of its competitors. Faltering world import demand and fiercer competition could also depress shipments from Argentina, Brazil, Cambodia, the United States and Viet Nam. By contrast, the anticipated removal of export restrictions would help Egypt and India boost international sales, although they may remain short of their 2007 levels. Ecuador, Guyana, Myanmar, Pakistan and Venezuela could also be in a position to raise rice deliveries to foreign markets. In the current context of financial difficulties, those exporting countries able to extend credit to buyers might be better off than the others, which may foster an intensification of government-to-government contracts.

Per Caput rice consumption set to rise again in 2009 Although rice prices in the world market have been falling in recent months, the decline has not always translated to lower domestic prices in importing countries, where they remain, in many cases, well above last year’s level. Nevertheless, an improved supply situation, following abundant 2008 crops, is expected to drive down domestic prices further in 2009 in many producing countries, bringing about improved prospects for consumption. Indeed, world rice utilization is forecast to increase by almost 2 percent next year to 444 million tonnes (in milled rice equivalent). About 86 percent of the total, or 384 million tonnes, is foreseen to be utilized as food, 1.8 percent more than in 2008. As a result, average annual rice per caput food consumption is set to rise by 0.3 kg to 57 kg g 2009. Among the regions, per caput rice consumption is forecast to increase in Asia, where consumers will continue to benefit from a number of targeted distribution programmes and retail price ceilings. By contrast, it may well fall in Africa and in LAC, partly on account of falling imports next year. Annual per caput rice consumption among developed countries is forecast to remain in the order of 12.4 kg in 2009.

Table 4. World rice market at a glance

* Jan-Oct 2008

1 Calendar year exports (second year shown) 2 Major exporters include India, Pakistan, Thailand, the United States of America and Viet Nam More detailed information on the rice market is available in the FAO Rice Market Monitor which can be accessed at: http://www.fao.org/es/esc/en/15/70/highlight_71.html

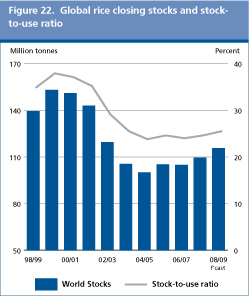

Good crops to boost world rice inventories in 2009 If confirmed, the buoyant production prospects for crops in 2008 should help boost the size of world rice inventories carried over into the new 2009 marketing seasons by 6 million tonnes, to 115.4 million tonnes, the highest level since 2002. All of the build-up is likely to be concentrated in the developing countries, while developed countries may face a contraction in inventories for the third consecutive year. From a trade status perspective, exporting countries would be mostly behind the global increase, with aggregate stocks in those countries expected to end 6 percent, or 5.8 million tonnes, above their opening levels. In China, Egypt, India, Pakistan and Viet Nam, such a build-up was greatly facilitated by the imposition of export restrictions in the course of 2008. Thailand is also foreseen to start the 2009 marketing year with much larger inventories, a consequence of government domestic purchases under the rice pledging programme. Among exporters, however, Myanmar is set to face a sizeable contraction in reserves, due to the large supply withdrawal needed to compensate for the hurricane Nargis-related losses in 2008. Reserves are also expected to grow in some of the most significant importing countries, in particular Bangladesh, Indonesia, Malaysia and the Philippines, where governments have been active in raising stocks to improve food security, an objective much revived by the soaring price episode in the first half of 2008. The increase in global inventories in 2009 would help raise the world stocks-to-use ratio from 24.6 in 2008 to 25.5 in 2009, the highest level since 2004.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |