|

|

MEAT AND MEAT PRODUCTS

PRICES

|

|

Prices strength showed signs of abating in September 2008

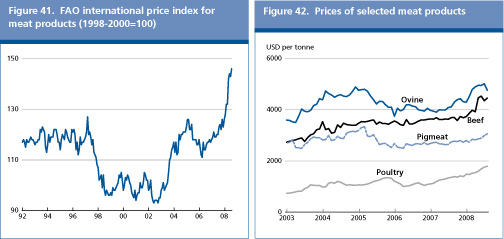

The FAO International Price Index of Meat Products has risen steadily from January to August 2008, when it stood 18 percent above its August 2007 level, reflecting a combination of firm demand and globally stagnant supplies. However, in September, prices started to show signs of weakening, amidst large supplies from increasing animal slaughtering and a faltering demand, particularly in developed countries. The September decline in prices is expected to continue over the coming months.

World meat prices have generally followed an upward trend between January and August 2008, as rising feed costs and firm consumer demand pushed the product prices upwards. The rise was particularly marked in the case of poultry meat and, to a smaller extent, ovine, bovine and pigmeat. Based on their indices, poultry meat prices have risen by 21 percent since January, followed by bovine, ovine meat and pigmeat, which have gained 19 percent, 11 percent and 9 percent respectively, over the same period.

Price prospects in the coming months point downwards. On the one hand, the sharp fall in cereal and meal prices are likely to translate in falling feed costs for livestock producers, particularly favouring the intensive poultry and pigmeat production systems. On the other, prospects for a general economic slowdown may have strong depressing effects on consumer meat demand and favour a shift of consumers towards poultry, which remains the cheapest source of meat protein. In the short term, the economic slowdown and cheaper feedstuffs could well result in an accelerating fall in meat prices.

|

|

2007

|

2008

estim.

|

2009

f’cast

|

Change: 2009 over 2008

|

|

|

million tonnes

|

%

|

|

WORLD BALANCE

|

|

|

|

|

|

Production

|

278.5

|

277.8

|

280.7

|

1.0

|

|

Bovine meat

|

66.4

|

65.1

|

65.4

|

0.4

|

|

Poultry meat

|

89.0

|

92.3

|

94.6

|

2.5

|

|

Pigmeat

|

103.6

|

100.8

|

101.0

|

0.2

|

|

Ovine meat

|

14.0

|

14.1

|

14.2

|

0.5

|

|

Trade

|

22.8

|

23.9

|

24.5

|

2.5

|

|

Bovine meat

|

7.0

|

6.7

|

7.0

|

4.3

|

|

Poultry

|

9.6

|

10.3

|

10.6

|

2.3

|

|

Pigmeat

|

5.1

|

5.7

|

5.8

|

1.5

|

|

Ovine meat

|

0.9

|

0.8

|

0.8

|

-1.7

|

|

|

|

|

SUPPLY AND DEMAND INDICATORS

|

|

|

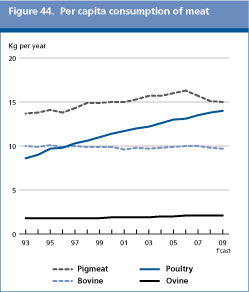

Per caput food consumption:

|

|

|

|

|

|

World

|

kg/year

|

42.1

|

41.6

|

41.6

|

-0.1

|

|

Developed

|

kg/year

|

82.3

|

82.3

|

82.0

|

-0.3

|

|

Developing

|

kg/year

|

31.2

|

30.6

|

30.8

|

0.5

|

|

|

|

2006

|

2007

|

2008

|

Change:

Jan-Sept 2008

|

|

|

|

|

|

|

over

Jan-Sept 2007

|

|

FAO Meat Price Index

|

|

|

|

|

%

|

|

(1998-2000=100)

|

|

114

|

120

|

137*

|

15

|

* Jan-Sept 2008

BOVINE MEAT

|

|

Bovine meat output to remain close to last year’s level, sustained by output gains in developing countries

Global bovine meat production in 2009 is forecast around 65.4milliontonnes, a slight recovery from 2008. The developing countries are expected to record a 1percent increase in production, offsetting a likely reduction in the developed countries. Production is expected to rise in Africa and Central America, reflecting larger slaughter numbers, often associated with a shift of grazing land into crop cultivated areas. In North America, output is foreseen to decrease somewhat in the UnitedStates and drop sharply in Canada where cattle numbers have been cut significantly as herd liquidation there began in early 2008. Among countries in Latin America and the Caribbean, Mexico’s bovine meat production may increase by 1percent in 2009, reflecting larger opening cattle inventories, and by 2percent in Brazil, sustained by a strong domestic market and improved export prospects; the European Union recently recognized some major beef producing Brazilian states as free of FMD and lifted the import ban that had been in place since 2005. A decline of 1percent is anticipated for Argentinean beef output, where cattle stocks have been downsized, along with a conversion of pastures into croplands. In Asia, slow growth in beef production is expected to continue, largely to meet the needs of an expanding population. Throughout 2008, production in China was impacted by natural disasters and animal disease outbreaks which left cattle producers reluctant to expand their herds. Barring any recurrence of such problems in 2009, production may rebound somewhat in the country, although not sufficiently to ensure full recovery to 2007 levels. Little change in production is currently forecast in the rest of the region. In Europe, high beef and dairy prices in the European Union have helped maintain cattle herds, which is expected to keep production in 2009 close to 2008 level. A decrease in bovine meat output of 1 and 3percent respectively is anticipated in Australiaand New Zealand, as producers retain cows and heifers to rebuild herds.

Trade in bovine meat is forecast to expand by 4percent to 7million tonnes in 2009. The rise is predominately due to the repeal of the European Union’s beef import ban on regions of Brazil, which is expected to foster increased deliveries to member countries. Chilean and Russian Federation beef imports are also set to increase, as domestic demand remains strong while the local industry does not appear in a position to expand production in the short term. With the current economic slowdown in Western economies, consumers are expected to alter their meat consumption patterns towards less expensive products. Therefore, Canada, Mexico and the United States may step up their purchases from abroad, particularly of low-valued beef cut from Australia and NewZealand. Little change in imports is currently anticipated for the other major beef meat destinations.

On the export side, shipments from the United States are expected to increase in 2009, although the recent currency appreciation may limit the expansion.Sales from Argentina are forecast to decline for the third consecutive year, reflecting the depressing effects of the tax on beef exports in place since 2007. Uruguay’s exports look set to continue to benefit from Argentina’s beef export restrictions and expand by 7percent in 2009. However, this is still subject to much uncertainty, as the unconfirmed resurgence of FMD in the country’s herds may hamper such prospects. Beef exports from Canada and Mexico are likely to be affected by new labelling requirements in the United States, their major beef market, applicable as of September 2008.The implications of the Country of Origins Labelling (COOL) requirements in the United States remain unclear, especially as meat processors may resort to multiple country labels to avoid the additional expense of segregating livestock.

PIGMEAT

|

|

Restructuring of the pigmeat sector should result in tight supplies in 2009

Global pigmeat production in 2009 is forecast to increase marginally above the 2008 level, to 101million tonnes, as much of the gains expected in Asia may be offset by a contraction in North America. In Asia, a modest expansion is expected in China, despite natural disasters and disease problems that have affected the sector in 2007 and 2008. Output is also anticipated to expand in the Republic of Korea, the Philippines and Viet Nam in response to heightened domestic demand. In many other countries, including Japan, high feed costs in much of 2008 have triggered a downsizing in the breeding herd, which is to limit the potential for expansion in 2009. In Latin America and the Caribbean, production in Brazil, is set to expand by more than 3percent, as an anticipated bumper harvest of feed crops could drive pigmeat production costs lower in 2009. Moreover, the World Organisation for Animal Health (OIE) recently declared the key, highly vertically integrated, pig producing states of Brazil free of FMD. This new status is expected to boost pigmeat demand both domestically and for export, stimulating an increase in production. Large feed availability could also boost pigmeat production in Argentina and Chile. In Europe, the Russian Federation may experience a 7percent growth in 2009, reflecting government support and policies aimed at boosting quality and domestic production to lessen dependency on imports. Reduced pig inventories in the European Union are behind a stagnating production outlook. By contrast, Ukraine may undergo a sharp contraction, following the industry response to more expensive feeds. Falling returns in North America, which triggered a downsizing of pig herds, may also result in falling output especially in Canada, but also in the United States.

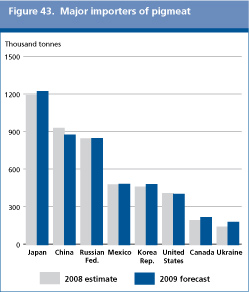

The world trade of pigmeat is estimated to remain in the order of 5.8million tonnes in 2009. Imports by Ukraineare expected to rise by 28percent compared with 2008, to compensate for a decline in domestic supplies. Larger purchases are also expected to be made by Japan, to meet growing domestic demand and offset a reduction in domestic production, and by the Republic of Korea. Deliveries to this country are likely to be facilitated by the recent Korean-Chile Free Trade Agreement (FTA), which has led to a reduction of the Republic of Korea’s import duties on Chilean products. Pigmeat imports by Canada, most of which originate from the United States, are set to rise by 13percent. Pigmeat deliveries to the RussianFederation, which are still subject to quota restrictions,are expected to remain stable. China, which is anticipated to be a major importer in 2008, may cut its purchases in 2009, as production starts recovering. They would, however, remain high, at around 450000 tonnes.

Brazilian trade negotiations with China, Japan, the Republic of Korea and the Philippines coupled with strong demand in those countries for pigmeat should hep Brazil boost pigmeat exports. The UnitedStates’ exports may also increase, sustained by strong import demand from Japan and Mexico. By contrast, exports from Canada are now anticipated to decline by 3percent, depressed by falling import demand from the UnitedStates. The European Union pork sector has been restructuring in 2008, which this should result in both lower supply and lower exports in 2009.

POULTRY MEAT

|

|

Poultry meat to gain further market share in 2009

Global poultry meat production in 2009 is projected to rise to 94.6million tonnes, 3percent higher than in 2008. Growth is expected in virtually all regions, except for North America. Poultry production in the UnitedStates is forecast to decrease by 1percent, in response to poor export prospects in 2009. By contrast, large production gains are anticipated in all the other major producing countries, i.e.Argentina, Brazil, Canada, China, Colombia, India, Indonesia, the Islamic Republic of Iran, Malaysia, Mexico, Russian Federation, Thailand and Turkey. Despite the resurgence of avian influenza (AI) in parts of the European Union, India and the Republic of Korea, the poultry production outlook in 2009 remains positive in those countries. The expected rise in Viet Nam’s import tariffs on frozen chicken should protect local farmers and boost the sector in 2009.

Competitive prices with respect to other meats and consumer preference for white meat still favour poultry meat. The cost efficiency of poultry can be largely attributed to the relative ability of the birds to convert feed into meat. This implies that high feed prices tends to raise poultry meat unit costs and prices by a smaller extent than is the case of pigmeat or beef from cattle raised in intensive production systems.

Trade in poultry meat for 2009 is forecast to rise by 2percent to 10.6million tonnes. Much of the import growth is expected to be driven by China, including the Hong Kong, SAR, where consumers are substituting broiler meat for higher-priced pigmeat. Increases are also expected in Japan, the Republic of Korea and the United Arab Emirates, to meet growing domestic demand. Saudi Arabia is anticipated to record a 6percent increase, following a recent cut of import tariffs for frozen poultry, aimed at controlling food inflation. Rising demand for leg quarters and mechanically separated chicken by the processing industry is also set to raise imports by Mexico. Deliveries to the European Union, which has become a net poultry importer since 2007, may rise slightly in 2009. By contrast, they may decline in the Russian Federation and in Ukraine. In the latter, the contraction may be as high as 27percent, reflecting a steady expansion in domestic poultry production.

As for poultry meat exports, expectations of falling imports by the RussianFederation and strong competition from Brazilian exports in the markets of China and Japan are dampening the United States’export prospects. Overseas sales from Brazil are now anticipated to grow by more then 4percent, to almost 3.8million tonnes, given competitive pricing. Despite rising production costs, the Thailand broiler industry anticipates that exports of chicken meat will continue to grow by approximately 5percent in 2009.

SHEEP AND GOAT MEAT

|

|

China behind a small increase in global ovine production in 2009

Global ovine meat production is forecast to rise slightly to 14.2million tonnes in 2009, reflecting mainly a moderate expansion in China. Except for Asia, all the other regions may only record marginal increases in production next year. Little change is expected in North American output, in line with stable demand. After two years of very high lamb slaughter numbers in Australia, due to poor pasture conditions, fewer lambs will be available for production in 2009. High grain prices also contributed to the decline in the size of the sheep flock, as mixed enterprise operators shifted land from pastures to crops. The size of New Zealand’s sheep flock has fallen substantially in the past few years, but the country has managed to maintain or even increase sheepmeat production, by increasing the focus of the industry on meat rather than wool production. Next year, however, the decline in numbers is likely to result in a small contraction of output. The EuropeanUnion’s production could decline somewhat in 2009, as a result of the decoupling of annual premiums for ewe numbers in major producing countries. In Africa and the MiddleEast, a few countries were also reported to be reducing the size of their flocks in response to higher crop prices, resulting in temporary increases in production in 2008, which are unlikely to be sustained in 2009. This was the case in Jordan, after the Government decided to cut feed subsidies to farmers in 2008.

World trade of sheep and goat meat in 2009 is expected to hover around 830000 - 850 000 tonnes. Overall, Australian sheep meat exports may decline by 7percent over 2008 due to weaker demand in key export markets, in particular the United States. Shipments from NewZealand may also decline somewhat. Among the major ovine meat importers, purchases by the UnitedStates are forecast to be depressed by poor overall consumer demand. Imports by the European Union are expected to stagnate. The European Union, nevertheless, remains the most important destination of trade in ovine meat.

|

November 2008

November 2008