November 2008 November 2008 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

OILSEEDS, OILS AND MEALS2

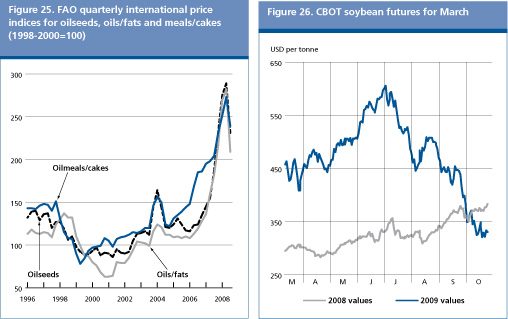

The latest price decline is not likely to continue and may be followed by firmer prices The unprecedented rally in oilseed and oilseed product prices that started in 2006 came to a halt in June 2008, when the FAO price indices reached historic highs of 295, 292 and 279 points for oilseeds, oils/fats and meals/cakes respectively, implying percentage increases of up to 150 from 2006 levels. Prices surged because supplies were insufficient to satisfy expanding demand, thus leading to a sharp reduction in inventories. Eventually, in July 2008 prices started tumbling and, by October, FAOs price indices had fallen back to the levels recorded in the summer of 2007. The drop was particularly pronounced for oils/fats and oilseeds. The general price fall was triggered by poor demand for oilseeds and products as well as by excellent production prospects for the new 2008/09 season. In the case of oils, the recent downturn in energy prices also contributed to the fall in prices. Developments on futures markets confirm these market sentiments: for instance, in the second half of October 2008, the CBOT March contract for soybeans was traded at around USD 330 per tonne, i.e. about 10 percent less than in the corresponding period of last year, and as much as USD 270 below the peak recorded in July 2008. Also, with the unfolding of the financial crisis, fears of global economic recession seem to be contributing to the continued slide in futures prices.

FAOs first supply and demand forecast for 2008/09 (October/September) suggests that prices in the oilseed complex should stabilize and possibly strengthen slightly, thus excluding a return to the low levels prevailing prior to the 2007/08 rally. Market fundamentals are anticipated to remain relatively tight, especially in the case of oilseeds and meals. Even if production is poised to rise, supply growth should be constrained by low opening stocks and an only partial recovery is expected in stock-to-use ratios. Other contributing factors are that farmers world wide are confronted with a substantial rise in costs of production, and continued strong competition between arable crops for land, as demand for non-food uses expands further.

Prices have been particularly volatile in the last season and could remain so in 2008/09, in light of the many uncertainties the market faces. In particular, current estimates for South Americas oilseed crops are very tentative, as the final outturn will depend on how weather conditions develop. Furthermore, growth in global oil and meal demand will be influenced by several external factors, notably the course of energy prices, possible changes in national biofuel policies, adjustments in the livestock sector and developments in the cereal market with direct effects on oilseed prices. If it materializes, the global economic slowdown could also have negative repercussions on the demand for oilseed products.

Global oilseed production poised to resume growth After last seasons exceptional decline, global oilseed production is forecast to expand strongly in 2008/09. FAOs output estimate of 431 million tonnes implies a 7 percent rise from last season and marks a new historic record. Record outturns are expected for all major oilcrops except cottonseed. The rise in global output will be mainly on account of soybeans (up 17.5 million tonnes), while the largest percentage year-on-year increase is expected for rapeseed and sunflowerseed (growing at about 12 percent). In general, farmers have responded to above average oilseed prices and prospects of continued demand growth by raising plantings. But oilcrop yields may also be boosted as weather conditions are better than last season in several regions and because farmers are raising fertilizer applications. Table 8. World production of major oilseeds

Source: FAO

Note: The split years bring together northern hemisphere annual crops harvested in the latter part of the first year shown, with southern hemisphere annual crops harvested in the early part of the second year shown. For tree crops, which are produced throughout the year, calendar year production for the second year shown is used.

In the northern hemisphere, harvesting of 2008/09 crops is nearing completion. In the United States, after loosing 14 percent to grains last season, the soybean area has more than recovered. However, adverse weather conditions in the early part of the crop year made yields fall to the lowest level in five years. As a result, although 11 percent up from the poor 2007/08 season, total output could remain below average. Also in China, soybean, as well as rapeseed, productions are showing healthy growth without, however, reaching the previous height. By contrast, estimates for India show a record soybean output and average rape and mustard seed production. The two other big rapeseed producers, the European Union and Canada, both harvested record crops owing to good yields, with Canada enjoying a particularly strong year-on-year rise. Meanwhile, rapeseed production in the Ukraine has again doubled, allowing the country to become the worlds fifth largest rapeseed producer in just a few years. Ukraine, the European Union and the Russian Federation also report record sunflowerseed crops, which should more than offset last years weather related decline. In the southern hemisphere, 2008/09 soybean plantings have only just started in South America. A slow down in area expansion from 5 percent last season to 3 percent this season is likely. This mainly reflects the situation in Brazil, where farmers are affected by reduced access to credit, higher production costs and prospects for lower profit margins. Soybean plantings in Brazil could be virtually unchanged from last season and thus remain below the recent record level, as opposed to Argentina where plantings could climb to a new record. The average regional yield level may drop (for the second consecutive year), due to less fertilizer use and because low rainfall has led to a depletion of soil moisture in key growing areas, especially in Argentina. Overall, a record soybean output is still possible, although growth would be below the regional trend for the second consecutive season. Sunflower production in Argentina is expected to decrease, while rapeseed production in Australia should finally climb back to normal levels. Table 9. World oilseeds and products markets at a glance

Source: FAO

Note: Refer to footnote 2 in the text for further explanations regarding definitions and coverage. 1 Includes oils and fats of vegetable and animal origin. 2 Production plus opening stocks. 3 Residual of the balance. 4 Trade data refer to exports based on a common October/September marketing season. 5 All meal figures are expressed in protein equivalent; meals include all meals and cakes derived from oilcrops as well as fish meal.

Moderate expansion expected in world oil/fat supplies FAOs first 2008/09 crop forecast translates into an increase of global oils/fats production of 5 percent, recovering from last seasons poor growth and closer to trend. Unlike in recent years, production may rise faster in developed than in developing countries. Among developing countries, total output is anticipated to rise in the two main oils/fats consuming nations, China and India. Although all major oils are likely to set new records, individual growth rates should differ: a strong slowdown is expected for palm oil (with a year-on-year growth of less than 3 percent as opposed to 8 percent on average), as palms in Asia are anticipated to enter the down-phase of the two-year yield cycle. By contrast, world soybean oil output could grow by an about average rate of 7 percent and sunflower and rapeseed oil by around 12 percent. Global supplies of oils/fats (i.e. 2007/08 ending stocks plus 2008/09 production) are estimated to rise about 3 percent, one percent more than last season but still considerably less than the growth observed in preceding years. Low opening stocks explain why supply is expected to expand less than production. The supply slowdown applies in particular to soybean oil, whereas palm, rapeseed and sunflower oils should fare much better. Countries affected by relatively low total supplies include the following major producers: the United States, the European Union, Argentina and Brazil. Global oil/fat consumption should grow, also thanks to biofuel Global oils/fats consumption is estimated to expand by 5.6 million tonnes or close to 4 percent in 2008/09. While this implies an acceleration compared with last seasons depressed level, growth would remain below trend. The recent decline in international prices should stimulate demand, but the response by domestic markets could be weaker than expected due to incomplete and slow price transmission. Furthermore, global economic recession could dampen demand growth later in the season. In some countries, the need to replenish stocks may also constrain consumption growth. As to individual oils, with a 27 percent share in total consumption, palm oil is expected to further consolidate its predominant position in the global utilization. With regard to major consuming countries, consumption is expected to grow by around 4 percent in China, India and the United States, while in the European Union the rate could be lower. Food uses may account for no more than half the expansion in global consumption, with the other half directed to non-food uses, notably biofuel. Private sources expect demand for biofuel production to expand by about 20 percent in 2008/09, slightly less than last season and in line with the gradual slowdown observed during the last few years. The key players will be soyoil in North and South America and rapeseed oil in Europe, followed by palm oil and eventually copra oil in Asia. Demand growth should be driven mainly by higher national blending requirements, for instance in Brazil and several European Union countries. For the European Union, the worlds leading producer and consumer of biodiesel, some further growth in demand is expected. The bioenergy sectors share in total vegetable oil consumption is estimated at 25 percent, which includes the absorption of 60-70 percent of the European Unions rapeseed oil output. Recent policy shifts could lead to a reduction in future targets for biofuel use from first-generation feedstock (e.g. vegetable oils), which could curtail the expansion of demand in future years. In 2008/09, usage looks also set to rise in the United States and Brazil, with the share of biofuel use in total vegetable oil consumption estimated to climb to 17 and 20 percent respectively. In Argentina, where a mainly export oriented industry has developed, biodiesel production is expected to account for about half of domestic oil consumption. Overall, these demand forecasts are still very tentative, given the large influence of the fossil fuel market on biofuel production. The relation between mineral and vegetable oil prices bears directly on the profitability of biodiesel production. For example, when prices for both vegetable oils and mineral oil started falling last July, the relative movement of prices has encouraged vegetable oil-based biofuel production.

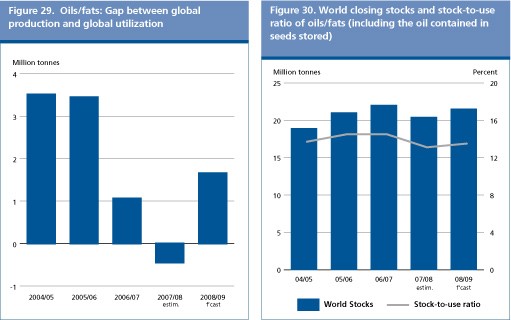

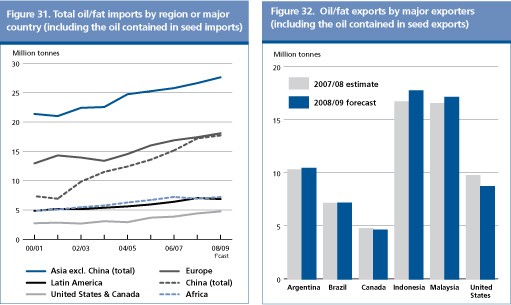

World oil/fat inventories are forecast to recover After falling short of consumption last season, in 2008/09, global oils/fats production is anticipated to exceed global demand, a situation that should allow a replenishment of inventories during the current season. The increase in vegetable oil stocks (measured as oil inventories, per se, plus the oil contained in stored seeds) is estimated at 6 percent, which implies a partial recovery from last seasons below average inventories. However, the rebuilding will not apply to all markets: while an increase of stocks is anticipated for rape, palm and sunflower oil, inventories are likely to drop for the second consecutive season in the case of soy oil. An accumulation of stocks is likely in Canada and the European Union (mainly rapeseeds and their oil) and in Indonesia (palm oil), while further reductions in inventories are expected in the United States (soybeans and their oil). Overall, the anticipated changes in global stocks and consumption could give rise to a modest recovery in the stock-to-use ratio, which, however, would not return to the level observed prior to last seasons drop. Such forecasts suggests that, rather than continuing on their recent downward trend, international prices for oils/fats could stabilize and perhaps even strengthen slightly in the course of this season. Moderate growth predicted in global trade of oils/fats At 83 million tonnes, world trade in oils/fats (which comprises the oil contained in traded seeds) is forecast to expand further in 2008/09, although at a below average rate of 3 percent. Over half of the anticipated expansion should be on account of higher palm oil shipments, in particular by Indonesia. Total palm oil trade should rise to 33.7 million tonnes, lifting the oils market share beyond 40 percent. Together, Indonesia and Malaysia are forecast to export 1.4 million tonnes or 5 percent more than last season. Global rapeseed and sunflower oil trade should climb even faster, with total shipments exceeding 6 million and 5 million tonnes respectively (including the oil equivalent of traded rape and sunflower seeds). The Ukraine should account for most of the rapeseed increase. Thanks to competitive pricing, the country is likely to raise its market share at the expense of Canada, who could face a cut in exports for the first time in eight years. The Ukraine should also keep its position of lead sunflower oil supplier, though record sun oil shipments are also expected from Argentina and the Russian Federation. As opposed to palm, rape and sunflower oils, global trade in soybean oil should fall, an event recorded only once in the last ten years. The anticipated 1 million tonnes (or 4 percent) decline in shipments would be mainly on account of the United States, whose exports are set to fall to a 3-year low of 6 million tonnes (of soy oil, per se, plus the oil contained in soybean shipments). Behind the reduction in export availabilities are the countrys below average soybean harvest, a lower than normal oil content in this years crop, the need to reconstitute stocks and increased demand from biofuel producers. Some of these same factors could also cause a slow down in exports from Brazil and Argentina.

Regarding oils/fats imports, Asia continues to be at the centre of attention as it accounts for over half of the worlds total. Led by China, Asias aggregate imports are forecast to expand by 1.5 million tonnes. While record purchases are expected in most of Asia, import expansion in China should slow down to 3 percent thanks to a resumption of oil production growth based on domestic sources. In India, where a moderate rise in domestic oil production is expected, imports are set to expand by 8 percent. In the European Union, an import rise of 0.5 million tonnes should be required to satisfy internal demand. In the United States, a net exporter of oils/fats, imports should continue to grow as the food industry further raises its use of vegetable oils other than soybean oil, in an effort to reduce the presence of trans fatty acids in food products. Africas import demand should rise as international prices return to more affordable levels and many developing countries are expected to continue preferring cheaper palm oil.

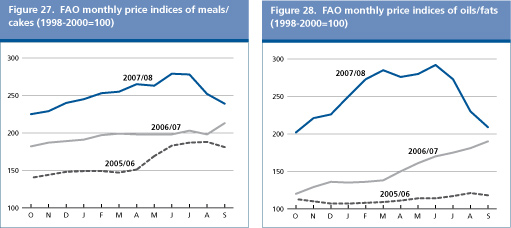

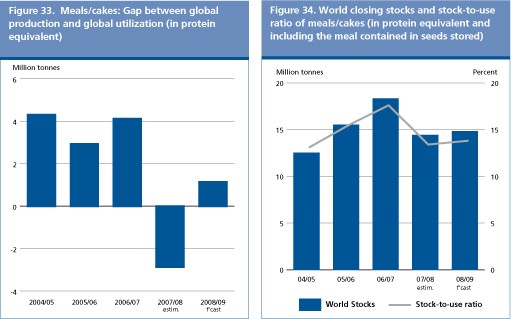

Rise in world meal/cake supplies limited by low opening stocks The anticipated expansion in global oilseed production, which applies in particular to soybeans, should translate into an above average rise in world meal output in 2008/09. After last seasons unprecedented drop, global output is estimated to expand by over 16 million tonnes or 7 percent. Growth rates for individual meals will span from about 11 percent for rape and sunflowerseed, to 7 percent for soybean and -3 percent for cottonseed. New records may be set in all main producing countries, with the exception of the United States and China. In the United States, where soybean output fell sharply last season, an only partial recovery in production is likely. By contrast, South Americas soymeal output should exceed last seasons record, although year-on-year growth could be low compared with recent years. As to global meal supplies (i.e. 2007/08 ending stocks plus 2008/09 production), growth should be limited to 3 percent, due to the sharply reduced opening stocks. Although faring better than last season, global supplies are expected to grow less than in previous years. Growth in global meal/cake consumption to remain below average In 2008/09, global meal consumption is forecast to grow by 2.8 million tonnes (on a protein equivalent weight basis) or almost 3 percent, same as last year, but less than average. While record high prices have triggered the past slow down in demand, this season, growth could be constrained by improved availability and attractive prices of feed grains. Relatively low livestock numbers in some countries (including the United States and the EU) and a general reduction in feeding profitability should add to the demand pressure. The weak growth in total meal supplies and the need to replenish inventories could also affect consumption. In Asia, meal consumption is anticipated to expand further, especially in China. But, in the European Union, consumption may rise by only one percent and, in the United States, demand is expected to recover only partially from last years drop. While in Asia and the United States growth continues to be driven by soymeal, in the European Union, rape and sunflowerseed meal should be the main drivers.

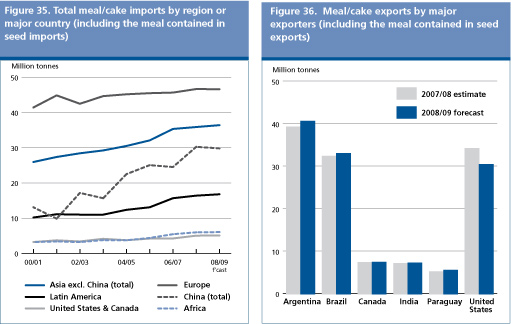

Only minor improvement expected in the meal/cake stock-to-use ratio After last seasons exceptional decline in global meal output and the resulting steep drop in stocks, in 2008/09, meal inventories are estimated to recover by no more than 3 percent (measured in protein equivalent weight and comprising the meal equivalent contained in stored seeds). Behind the low replenishment rate is the moderate rise in meal production vis-à-vis consumption. Meal output is forecast to exceed consumption by 1.1 million tonnes or one percent only, compared with rates of 3-5 percent in recent years. Also the comparison of global supplies with global consumption confirms that meal markets would likely remain tight in 2008/09. This situation applies in particular to the soymeal market, where, in spite of the anticipated 7 percent rise in output, global inventories may remain virtually unchanged. At the country level, the small stock increase expected in the United States and China could well be offset by inventory cuts in the European Union and Brazil. Overall, the anticipated consumption and stock changes translate into a minor improvement in the global stock-to-use ratio. Considering that the ratio may remain well below average, the recent decrease in international oilseed and oilmeal prices may come to an end, allowing prices to stabilize or even strengthen slightly. Expansion in world meals/cakes trade may come to a halt After four consecutive seasons of healthy growth, global trade in meals/cakes (including the meal equivalent contained in oilseeds traded) is forecast to remain virtually unchanged from last season. Increased transactions in rape, sunflower and palmkernel meal should be offset by an unusual drop in soymeal trade (including meal from beans), mainly on account of sharply reduced shipments from the United States. In 2007/08, United States exports grew in spite of a poor harvest thanks to a steep draw down in inventories. This season, however, a below average crop, firm domestic consumption and the need to replenish stocks are anticipated to force down United States soymeal exports (including meal from beans) by more than 10 percent. Also in Brazil export availabilities may be constrained by rising domestic demand. Argentina, by contrast, should be in the position to step up its exports: soymeal shipments alone could climb to a record 29 million tonnes, which would correspond to over half of global exports. Paraguay and India are affirming themselves as emerging suppliers of soy-based meals, while the Ukraine is becoming an important source for rape and sunseed meal, partly taking over market shares from other countries such as Canada.

With respect to meal imports (including the meal equivalent contained in oilseeds traded), shipments to the European Union and China, which together account for over half of global import demand, are both poised to drop somewhat, thanks to a good outturn in domestic oilcrop production. Purchases by other Asian buyers, whose demand is largely satisfied via imports, should continue to rise, though less than last season, because of subdued growth in domestic demand. Interestingly, in Argentina, the worlds leading exporter of soybean meal, imports of soybeans are forecast to grow further, as the country is purchasing soybeans from neighbouring nations to boost even more its meal shipments. 2. Almost the entire volume of oilcrops harvested worldwide is crushed in order to obtain oils and fats for human nutrition or industrial purposes and cakes and meals used as feed ingredients. Therefore, rather than referring to oilseeds, the analysis of the market situation is mainly undertaken in terms of oils/fats and cakes/meals. Hence, production data for oils (cakes) derived from oilseeds refer to the oil (cake) equivalent of the current production of the relevant oilseeds, and do not reflect the outcome of actual oilseed crushing nor take into account changes in oilseed stocks. Furthermore, the data on trade in and stocks of oils (cakes) refer to the sum of trade in and stocks of oils and cakes plus the oil (cake) equivalent of oilseed trade and stocks. 3. For details on prices and corresponding indices, see appendix Table A-24. 4. This section refers to oils from all origins, which, in addition to products derived from the oil crops discussed under the section on oilseeds, include palm oil, marine oils as well as animal fats. 5. This section refers to meals from all origins, which, in addition to products derived from the oil crops discussed under the section on oilseeds, include fish meal as well as meals of animal origin. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |