|

|

WHEAT

PRICES

|

|

International prices rose in recent weeks

|

|

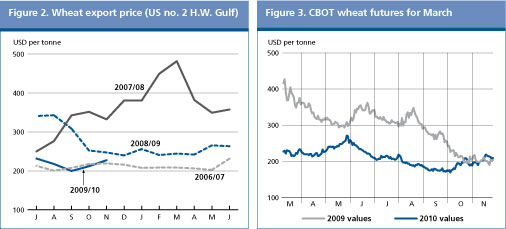

This year's solid prospects for world production and large exportable supplies against the backdrop of a sharp reduction in world import demand, acted to push international wheat prices down in the early months of the season. However, wheat prices began rising in October and by late November they stood at some 20 percent above their September values. The recent surge in wheat prices was mainly driven by developments in other markets, especially maize and rice, but also outside factors such as exchange rates (a weak United States Dollar) and changes in financial markets. In November, the price of United States' wheat (No.2 Hard Red Winter, f.o.b. Gulf) averaged USD 228 per tonne, up 14 percent from September. However, this price is still 50 percent down from March 2008, the month when prices peaked to an all time high.

| |

2007/08 |

2008/09 |

2009/10 |

Change: 2009/10 over | | | |

estim. |

f'cast |

2008/09 | | |

million tonnes |

% | |

WORLD BALANCE | | | | | |

Production |

625.5 |

681.4 |

678.6 |

-0.4 | |

Trade1/ |

112.1 |

139.1 |

117.0 |

-15.9 | |

Total utilization |

644.7 |

647.6 |

665.3 |

2.7 | | Food | 447.8 | 455.6 | 462.9 | 1.6 | | Feed | 122.6 | 119.9 | 125.3 | 4.5 | | Other uses | 74.3 | 72.1 | 77.0 | 6.9 | |

Ending stocks |

143.3 |

172.3 |

183.5 |

6.5 | | | | |

SUPPLY AND DEMAND INDICATORS | | | Per caput food consumption: | | | | | | World (kg/year) | 67.1 | 67.5 | 67.7 | 0.4 | | LIFDC (kg/year) | 57.2 | 57.8 | 58.3 | 0.8 | | World stock-to-use ratio % | 22.1 | 25.9 | 27.9 | |

| Major exporters' stock-to-disappearance ratio % 2/ |

11.8 | 17.5 | 20.3 | | | | | | | | | |

2007 |

2008 |

2009 |

Change:

Jan-Nov 2009 | | | | | |

over

Jan-Nov 2008 | |

Wheat Price Index * | | | | % | | (2002-2004=100) | 179 | 235 | 154** | -36 |

* Derived from International Grains Council (IGC) Wheat Index

** January-November 2009

1/Trade data refer to exports based on a common July/June marketing season

2/ Major exporters include Argentina, Australia, Canada, EU and the United States

Wheat futures have also strengthened in recent weeks. The increase was in part driven by the weak United States Dollar as the ICE Futures U.S. Dollar Index, a leading benchmark for the international value of the United States Dollar, dipped to a 15-month low in November. In addition, small supplies in Argentina, a major exporter, and delayed winter wheat plantings in the United States, mostly because of the late harvesting of maize as a result of excessive wet conditions, also pushed up prices. By late November, wheat futures for March 2010 delivery on the Chicago Board of Trade (CBOT) were quoted around USD 210 per tonne, up 20 percent from September and close to the values quoted for the same period last year.

PRODUCTION

|

|

Wheat output in 2009 remains close to last year's record high

|

|

FAO's latest forecast for world wheat output in 2009 now stands at 679 million tonnes, substantially up from earlier expectations and almost equalling the bumper crop gathered last year. Of the wheat crops already harvested, latest estimates in Asia, now point to a significant (6 percent) increase in production following generally above average yields. In North Africa, harvests also turned out better than predicted and the region's crop is now estimated at double last year's reduced level. In North America, the 2009 wheat crop estimate in the United States rose as the season progressed, but despite the realization of above-average yields, the final output is nevertheless 11 percent short of last year's exceptional crop. In Europe, better than expected crops in the Russian Federation and Ukraine contributed to an increase in the continent's 2009 wheat output estimate but again, aggregate output would still fall well short of last year's bumper level. In the southern hemisphere, the major 2009 wheat crops are scheduled to be harvested between now and the end of the year. In South America, production is expected to fall a by 4 percent from last year's already poor level, largely as a consequence of the prolonged drought that has affected Argentina since May. By contrast the outlook remains favourable in Brazil. In Oceania, prospects for the wheat crop in Australia remain favourable and the second largest crop since the 2005 record is anticipated.

|

Country* |

2008 estim. |

2009 f'cast |

Change: 2009 over 2008 | | |

million tonnes |

percent | | European Union | 150.4 | 137.1 | -8.8 | | China (Mainland) | 112.5 | 115.0 | 2.2 | | India | 78.6 | 80.6 | 2.6 | | Russian Federation | 61.2 | 61.0 | -0.3 | | United States of America | 68.0 | 60.4 | -11.2 | | Canada | 28.6 | 24.6 | -14.1 | | Pakistan | 21.5 | 24.0 | 11.8 | | Ukraine | 24.2 | 20.5 | -15.4 | | Australia | 21.4 | 22.7 | 6.2 | | Turkey | 17.8 | 20.5 | 15.2 | | Kazakhstan | 16.0 | 17.0 | 6.3 | | Iran Islamic Rep. of | 9.8 | 13.0 | 32.7 | | Argentina | 8.3 | 7.5 | -9.6 | | Egypt | 8.0 | 8.8 | 10.3 | | Uzbekistan | 6.1 | 6.5 | 5.8 | | | | | | | Other countries | 49.1 | 59.4 | 21.0 | | | | | | |

World |

681.4 |

678.6 |

-0.4 |

* Countries listed according to their position in global production (average 2007-2009)

In many parts of the northern hemisphere, winter wheat crops for harvest in 2010 are already at the early stages of development or planting is underway. In the United States, as of mid-November, winter wheat sowing was reported to be almost complete. Although delays had been experienced in some parts due to adverse weather, 64 percent of the crop was rated in good to excellent condition, just marginally down from the same time last year. The final area sown, however, is expected to be down for the second year in succession, reflecting reduced producer price expectations compared with their outlook last year. Although no firm estimates are available yet, early indications suggest that the reduction could be in the region of 3 percent. Similarly, reduced wheat area in 2010 is also expected in the European Union, especially where farmers can switch easily to alternative crops such as oilseeds that could offer better returns. By contrast, among the major producers outside the European Union, especially in East Europe, wheat area is expected to increase in the Russian Federation and remain around last year's good level in Ukraine, as farmers are being encouraged by government support. In Asia, in the two largest wheat producing countries, China and India, the Governments have likewise initiated plans to encourage wheat production through increasing state minimum purchasing prices. Thus, wheat planting in China is thought to have equalled last year's satisfactory level, while in India, a larger area is expected.

TRADE

|

|

Sharp fall in global wheat trade in 2009/10

|

|

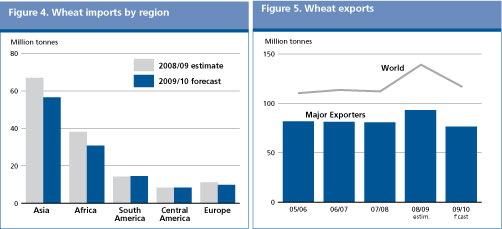

World wheat trade in 2009/10 (July/June) is forecast to reach 117 million tonnes, down by as much as 16 percent, or 22 million tonnes, from the estimated volume last year. The forecast is though some 3 million tonnes higher than FAO's first trade forecast published in June 2009. Relatively low international wheat prices during the early months (July-September) of the season boosted purchases by several countries, resulting in progressive upward revisions to forecasts for 2009/10 trade. Nonetheless, world wheat trade would still remain well below the previous season's record volume mostly because of reduced demand following bumper crops in North Africa and good harvests in the leading wheat importing countries of Asia.

Total wheat imports by Asia are expected to reach 55 million tonnes, down 16 percent, or 10 million tonnes, from the record high in 2008/09, but the second largest since 1992. Much of the decrease is expected to originate in the Islamic Republic of Iran where, as a result of a partial production recovery from last year's severe drought, deliveries in 2009/10 are forecast to fall by over 50 percent from the last season's record high. Wheat imports by Pakistan are also forecast to be more than halved as a result of a record crop this year and sharply lower imports are similarly anticipated for Bangladesh and Turkey. In India, wheat imports by the private sector could exceed slightly the previous season's small volume but, given this year's record production level and ample stocks, the Government recently announced that it was not planning to import wheat for the time being. By contrast, wheat imports by Saudi Arabia are forecast to increase sharply for the second consecutive season. Higher imports are in line with the Government's decision to gradually eliminate wheat cultivation by 2016 in order to conserve scarce water supplies. Following a gradual return to a more comfortable supply situation, some countries in the region are expected to relax their trade restrictions imposed since 2007/08 in response to shortages and high domestic prices. For instance, Pakistan has removed a 35 percent export duty on wheat products while China lowered export taxes on wheat (to 3 percent) and wheat flour (to 8 percent).

.

In Africa, wheat imports by Morocco could fall by a half from last year because of a record harvest. Above average crops are also likely to lower wheat inflows to Algeria, Egypt and Tunisia. Wheat imports by most countries in Latin America and the Caribbean are forecast to be similar to the previous season with slightly higher imports by a few countries, including Chile, Peru and Venezuela. In Brazil, the region's largest buyer, imports are forecast to remain unchanged but the Government has restricted import licences for wheat flour imports from Argentina. This is mainly to support the domestic milling industry in the south of Brazil, which is being affected by cheaper flour imports from Argentina. In Europe, aggregate transactions are forecast down from the previous season mostly as a result of a reduction in wheat purchases by the European Union, as large carryovers from the previous season have boosted domestic supplies.

In view of the anticipated sharp decline in world import demand in 2009/10, shipments from most exporting countries are forecast to decline. The most significant reduction is forecast for Argentina where supplies are extremely tight due to the country's drought-reduced harvest. Exports from the European Union are also expected to decline sharply, not only because of lower demand in the traditional importers, but also due to the strong Euro and increased competition from other exporters. By mid-November, cumulative wheat exports since the start of the marketing year from the European Union reached 6.6 million tonnes, 2 million tonnes less than during the same period last year. While smaller exports are also anticipated from Canada and the United States, shipments from Australia could increase, driven by large supplies following two consecutive seasons of good harvests and strong demand from nearby countries; namely Indonesia, Malaysia, Thailand and Viet Nam. Elsewhere, wheat exports from Ukraine are forecast to decline sharply owing to reduced production while sales from the Russian Federation may fall slightly below the previous season's record level. Exports from Kazakhstan are forecast to increase, helped by the recent decision of the Government to subsidize shipments to Baltic and Black Sea ports in order to improve export competitiveness.

UTILIZATION

|

|

World wheat utilization in 2009/10 to increase at a faster pace than anticipated earlier

|

|

World wheat utilization in 2009/10 is forecast to reach 665 million tonnes, 10 million tonnes higher than FAO's first forecast published in June and almost 3 percent above the estimated utilization level in 2008/09. At this level, total wheat utilization would also exceed the ten-year average by roughly 2 percent. With world wheat production in 2009 approaching last year's record (contrary to earlier expectations) and large carryovers from the previous season, world wheat supplies have increased. This is expected to contribute to faster growth in wheat utilization than in the previous two seasons, when supplies were tight and prices much higher.

Global food consumption of wheat is forecast to reach 463 million tonnes, up 1.6 percent from the previous season. At this pace, world per caput consumption of wheat is forecast to remain stable at around 68 kg. In the developing countries, total wheat used for food is forecast to reach 328 million tonnes. At this level, per caput intake would show a slight increase, from 59.5 kg in 2008/09 to 60.0 kg in 2009/10.

World feed use of wheat is forecast to reach 125 million tonnes, up 4.5 percent from 2008/09. This compares with a 2 percent contraction in the previous season. The anticipated increase would mostly reflect a sharp recovery in feed usage of wheat in the Russian Federation. In the European Union, the world's largest user of wheat for animal feed, wheat utilization by the livestock sector is forecast to remain unchanged at the previous season's level at around 56 million tonnes, reflecting weak demand and large supplies of alternative feed grains, in particular triticale, rye and barley.

The other uses of wheat, which include seed, industrial usage and post harvest losses, are expected to total around 77 million tonnes, up 7 percent from the previous season. Some of the increase would reflect higher wastage, largely driven by bumper harvests in many countries while the industrial use of wheat is also seen to expand, boosted by stronger demand from the starch industry as well as the ethanol sector, the latter primarily in Canada and the European Union.

STOCKS

|

|

World wheat inventories to increase for the second consecutive season

|

|

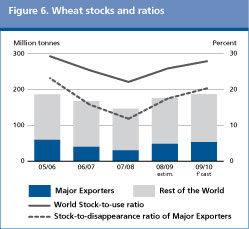

World wheat stocks by the close of the crop seasons ending in 2010 are forecast to reach 183.5 million tonnes, 6.5 percent, or 11 million tonnes, higher than their opening level, but down 4 million tonnes from the FAO forecast at the start of the season. The reduction since the previous forecast, published in the June report mostly reflects upward revisions to utilization numbers, made in response to lower prices.

Although world wheat production is expected to register a small decline in 2009 from the record in 2008, it is foreseen to exceed total wheat utilization anticipated in 2009/10. For this reason, stocks are forecast to return to more normal levels, and rise by 28 percent from the estimated low of 143 million tonnes in 2007/08 (the smallest since the early 1980s). Based on the latest forecasts for stocks and utilization, the world wheat stock-to-use ratio is also expected to increase, to nearly 28 percent, 2 percentage points higher than in the 2008/09 season and close to the five-year average (2002/03-2007/08). To put the recovery into perspective, this ratio dipped to 22 percent in 2007/08, reflecting the very tight supply and demand balance in that season.

Total wheat stocks held by the major exporters are forecast to reach 52 million tonnes, up 5 million tonnes from their opening level and the highest since 2006. The largest increase is expected in the United States where, despite a fall in production, ending season wheat inventories are likely to increase because of an expected drop in exports and a slight reduction in the domestic feed utilization. Stocks in the European Union are set to decline slightly despite a sharp drop in production and an increase in feed and ethanol utilization. The prospect of significantly less exports than in the previous season is the main reason that wheat stocks in the European Union could remain large. On aggregate, therefore, the ratio of stocks held by the major exporters to their total disappearance (i.e. domestic utilization plus exports) is currently forecast to increase to 20.3 percent, up 3 percentage points from the previous season and well above the critically low ratio of just under 12 percent in the high-price 2007/08 season.

Among other countries, near-record exports and a slight contraction in output could result in lower ending stocks (to 6.5 million tonnes) in the Russian Federation. But in China, where the world's largest inventories of wheat are to be found, ending stocks are forecast to increase to roughly 55 million tonnes given this year's record production. In India, another leading stock holder harvesting a record crop this year, inventories are forecast to decline slightly, to 17 million tonnes. Since the beginning of the current season to date, the Government of India under its Open Market Sale Scheme, has been releasing wheat from its strategic reserves, to the tune of nearly 4 million tonnes, in order to keep domestic food prices in check.

|

December 2009

December 2009