December 2009 December 2009 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

RICE

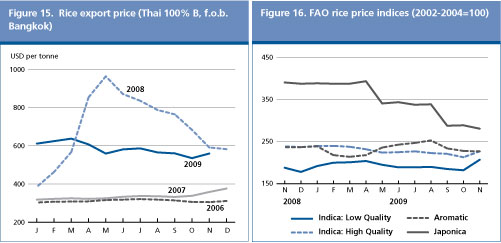

After several months of slow but steady declines, international rice prices started rebounding in November 2009, coinciding with several announcements by the Philippines that it would bid for around 2 million tonnes of rice imports in various tranches. The market was further stirred by rumours that the Government of India was approaching the authorities of major exporting countries to secure several million tonnes of rice. Although the prospect of India entering the global market to buy large volumes has yet to be confirmed, the news was sufficient to lift world prices in a period usually associated with abundant supplies and falling quotations. The price strength was particularly evident for lower quality Indica, the type the Philippines is buying, which pulled the index for this category upwards by 14 percent between October and November. As an example, Indica with 25 percent brokens, fob Viet Nam, was quoted USD 433 per tonne in November, up from USD 360 per tonne in October. Although more contained, increases were also witnessed for similar quality rice in Pakistan and Thailand. Some of the price strength was transmitted to the higher quality Indica rice, the index of which gained 7 percent in November, with the benchmark Thai white rice 100 percent B rising by USD 24 per tonne to USD 559 per tonne. On the other hand, Japonica and aromatic rice varieties were little affected.

Despite the recovery, world rice prices in November were some 12 percent lower than one year ago. Indeed, over the January-November period, the FAO All Rice Price Index fell back by 15 percent, driven in particular by lower quotations for Indica, which lost ground on average by 35 and 24 percent for low quality and high quality types respectively. Aromatic rice prices were also 8 percent weaker, but quotations of Japonica rice averaged 12 percent more than last year.

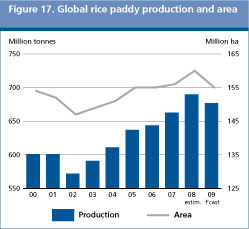

In the past few months not only was the pattern of the southwest monsoon, which determines much of the season's paddy output in several of the major producing countries, erratic, but a series of natural disasters, from earthquakes and landslides to hurricanes, also impaired rice crops across several regions. As a result, the global paddy production outlook has worsened substantially since the release of the June issue of Food Outlook, and now stands at 675 million tonnes (451 million tonnes, milled basis), 13 million tonnes, or 1.9 percent less than in 2008. Despite the contraction, production in 2009 would still stand out as the second highest after the record 2008 season. Furthermore, should rice prices peak up in the coming months, plantings of the secondary crops may well expand beyond current expectations, as witnessed in 2008, which would boost global production in 2009 further.

Much of the world production decline is expected to be concentrated in Asia, where output may fall from 624 million tonnes in 2008 to 609 million tonnes in 2009. India was particularly hit by the irregularity of monsoon rains beginning with drought or below average rainfall, followed by torrential rains and floods, bringing about a sharp reduction to the country's main Kharif crop. Although the area under the 2009 secondary Rabi crop, now at the planting stage, is likely to be raised, India is expected to harvest 128 million tonnes of paddy (85 million tonnes, milled basis) over the full 2009 season, 21 million tonnes, or 14 percent, less paddy than in 2008. Several other countries in the region also faced severe production shocks in the past few months. In some cases the losses are expected to be compensated through larger 2009 secondary crops, now at the planting stage. On balance, total rice production is expected to fall below last season's level in Bangladesh, the Chinese Province of Taiwan, Iraq, Japan, Nepal, Pakistan, the Philippines and Sri Lanka. By contrast, the outlook for 2009 production is positive in Afghanistan, Cambodia, mainland China, the Democratic Republic of Korea, Indonesia, the Islamic Republic of Iran, Lao People's Democratic Republic, Myanmar, the Republic of Korea, Thailand and Viet Nam, generally driven by favourable returns on rice compared with other crops, which have fostered an expansion of plantings. Weather conditions in Africa have been less favourable this season than in 2008, which, together with a cut of the rice area in Egypt, may bring production in the region down by 3 percent to 24.6 million tonnes. Extensive drought problems are estimated to have depressed production in eastern Africa, especially in the United Republic of Tanzania. However, the outlook for production is positive in western Africa , where many governments have maintained the subsidies on seeds and fertilizers introduced in 2008. As a result, gains in production are forecast across the subregion, in particular in Ghana, Guinea, Mali, Nigeria and Senegal. In Southern Africa, Madagascar, Mozambique and Zambia have harvested bumper crops. Prospects are buoyant in the other continents. In Latin America and the Caribbean, production in 2009 is estimated to reach 27.4 million tonnes, almost 4 percent more than last year. In Central America and the Caribbean, the hurricane period in the Northern Atlantic Ocean, which normally ends on 30 November, was relatively benign, as only El Salvador and Nicaragua were reported to have suffered some limited rice losses from the passage of hurricane Ida in early November. However, within the subregion, Mexico alone is foreseen to experience a decline in output this season, reflecting widespread drought in recent months and heavy rainfall subsequently. In South America, with the exception of Guyana, Uruguay and Venezuela, all countries are estimated to harvest larger crops in 2009, with especially strong gains recorded by Argentina, Bolivia, Brazil, Colombia and Peru. However, in the wake of a recurring El Niño, the outlook for regional production in 2010 has worsened. Indeed, with the planting of the new crops underway, a prevailing drought and well below average water reserves are constraining the area sown to rice in Argentina, Brazil and Uruguay, which may bring about a decline in production next season. In North America, the most recent forecast from the United States pointed to a 7 percent increase in output, sustained by an expansion of medium grain rice. In Europe, prospects are excellent for the European Union and the Russian Federation, which are both expected to harvest their largest crops in the decade so far. In Oceania , production also rose in Australia, although limited water availability restrained it to a fraction of what it was at the beginning of the decade. The country's outlook for 2010 remains subdued as winter rainfall in key growing regions was again below normal.

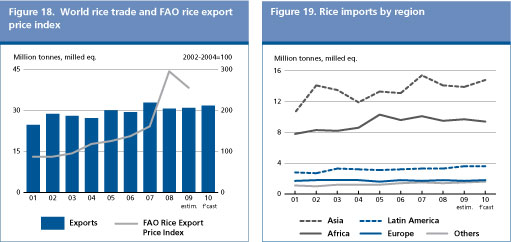

The current forecast for international rice trade in the calendar year 2010, at 31.2 million tonnes, points to a 2.7 percent, or 800 000 tonnes, increase from the 2009 estimate and much higher than forecast last June. The revision reflects larger import requirements by those countries that faced important crop losses in recent months. If confirmed, trade next year would be the second largest after 2007.

Much of the expected growth is expected to be driven by larger imports by Asian countries, which are foreseen to reach 14.8 million tonnes on aggregate, almost 7 percent more than last year. Part of the increase would stem from increased purchases by Near East Asian countries, in particular Iraq, Saudi Arabia and the United Arab Emirates, while rice flows into the Islamic Republic of Iran may be depressed by large domestic availabilities and a recent increase in the basmati rice tariff. Among countries in the Far East, imports by Bangladesh, Nepal and especially the Philippines are forecast to rise to offset recent losses from natural disasters. In the case of the Philippines, they are currently forecast to reach 2.3 million tonnes, up 28 percent from 2009 with over 2 million tonnes already being tendered by the National Food Authority in 2009 for delivery in 2010. Imports by India, are expected to be in the order of 100 000 tonnes only, as high international prices compared with domestic prices and the fact that the Government can draw from its large rice and wheat stocks to compensate for the 2009 rice production shortfall, limit the chances of greater imports. On the other hand, good prospects for crops this season may result in a 3 percent reduction of imports by countries in Africa , especially Guinea, Mali, Mozambique and Senegal. In Latin America and the Caribbean , rice imports may rise slightly, sustained by Brazil and Mexico, where the smaller crops along with strong currencies are likely to result in greater rice deliveries , while those destined for Colombia, Cuba and Peru are expected to fall. Rice purchases by the European Union are forecast to rise by 100 000 tonnes to 1.3 million tonnes in 2010, which would turn the region into the third largest destination of rice trade, after the Philippines and Nigeria and on a par with Saudi Arabia.

The increase in import demand is anticipated to be met by a surge of exports from Thailand but also China mainland, Myanmar and the Republic of Korea, which are all estimated to hold abundant supplies. By contrast, exports are predicted to fall to 2 million tonnes in India, where the Government is likely to maintain its tight restrictions on external sales, allowing only Basmati rice shipments. Exports from Brazil, Cambodia, Egypt, Pakistan and Uruguay are also foreseen to decline compared with 2009, as all those countries are anticipated to face tight market conditions next year. Shipments from the United States are also forecast to be smaller.

Total rice utilization, including food, feed and other uses, is anticipated to reach some 454 million tonnes in 2010, 8 million tonnes more than consumed in 2009. Virtually all of the increase is expected in food consumption, which is forecast to absorb 389 million tonnes next year compared with 383 million tonnes in 2009. The increase, however, would be barely sufficient to meet the needs of the world's growing population and would keep average per caput intake unchanged at around 57.3 kg. Table 6. World rice market at a glance

1 Calendar year exports (second year shown).

2Major exporters include India, Pakistan, Thailand, the United States of America and Viet Nam.

More detailed information on the rice market is available in the FAO Rice Market Monitor which can be accessed at: http://www.fao.org/es/esc/en/15/70/highlight_71.html

* Jan-Nov 2009.

Among different economic groups, per caput rice consumption is also anticipated to remain stable in developing and developed countries at around 68 and 13 kg per year, respectively. The sustained level of world demand for rice confirms the little responsiveness of rice consumption to changes in prices or incomes. Indeed, retail or wholesale prices in many countries have remained stubbornly high, a situation that has been made worse by rising unemployment even in those countries where the economic recovery is underway. However, these factors are having weaker implications for rice than for more expensive food items such as livestock products. To some extent, the widening of subsidized food distribution, to benefit larger segments of the population in countries such as Bangladesh, India, Indonesia, the Philippines or Venezuela, will likely contribute to the sustaining of rice consumption across the world.

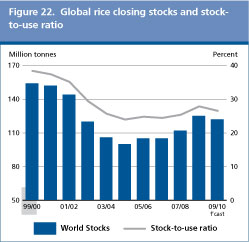

Under current prospects, world production in 2009 would fall short of global rice utilization in 2010 by around 3 million tonnes, which would need to be met by world reserves. As a result, rice carryover stocks at the close of the marketing seasons ending in 2010 are anticipated to shrink from 124 million tonnes in 2009 to 121 million tonnes this year, still high if compared with the 110 million tonnes held on average between 2002 and 2009.

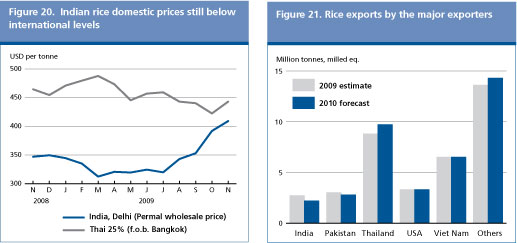

A sizeable part of the contraction this year will be on account of India, which is expected to draw more than 9 million tonnes from its reserves to fill the gap between production and consumption. As a result, the country may carry over as much as 12 million tonnes at the end of its season on 30 September 2010, down from 21 million tonnes a year earlier, but not much different from the volumes held between 2003 and 2007. Other countries are anticipated to reduce the size of their inventories, in particular Bangladesh, Egypt, Myanmar, the Philippines and Viet Nam. By contrast, good crops in 2009 are expected to boost stocks in China mainland, Colombia, Indonesia, Mali, the Republic of Korea and the United States. Likewise, large imports would enable Brazil, the European Union, Saudi Arabia, and the United Arab Emirates to increase the size of their rice reserves.

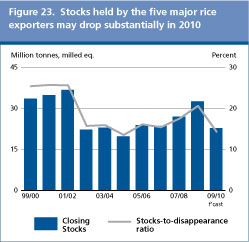

At the forecast level of 121 million tonnes, the world stocks-to-use ratio would be around 27 percent, slightly below the level last year but still adequate enough to provide a good degree of food security at the global level. However, because much of the stock decline is anticipated to affect several of the five major exporting countries (India, Pakistan, Thailand, Viet Nam and the United States), the stocks-to-disappearance ratio for this group may significantly deteriorate, from 21 percent in 2009 to 14 percent in 2010, the lowest witnessed since 2005. Accordingly, a much smaller ratio would signal a tightening of world market conditions in the course of 2010.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |