COARSE GRAINS

PRICES

|

|

International prices remain firm

|

|

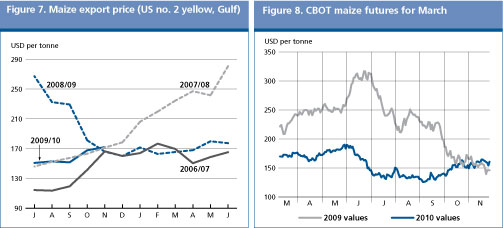

International prices have remained generally firm since the start of the current marketing season and underwent considerable strengthening in recent weeks. Following a short-lived dip in July, prices began to move up slowly, driven by early signs that world production in 2009 would be smaller than in 2008, giving rise to a supply and demand balance sheet for major coarse grains that would be tighter than last season. Delays in harvesting in the United States, caused by excessive wet conditions, added to upward price pressure but the economic slowdown and weaker demand prospects, particularly for feed, restrained the price rise to some extent. The increase in international prices has become more pronounced since October, helped by the slide in the United States Dollar and a rally in oil prices. In November, the US maize price (No. 2 Yellow, Gulf) averaged USD 172 per tonne, representing a gain of 13 percent from September, although still down 40 percent from the peak in June 2008.

Prices in the futures market have also shown renewed strength in recent weeks. The strong increase in soybean prices and the expectation of larger demand from the ethanol sector should oil prices rise faster in the coming months were also supportive. By late November, the March 2010 maize contract at the Chicago Board of Trade (CBOT) stood around USD 160 per tonne, up USD 28 per tonne, or 20 percent, above the September average but 5 percent below the corresponding period last year.

| |

2007/08 |

2008/09 |

2009/10 |

Change: 2009/10 over | | | |

estim. |

f'cast |

2008/09 | | |

million tonnes |

% | |

WORLD BALANCE | | | | | |

Production |

1 082.4 |

1 143.1 |

1 108.7 |

-3.0 | |

Trade 1/ |

130.8 |

113.7 |

112.0 |

-1.5 | |

Total utilization |

1 075.3 |

1 095.7 |

1 109.0 |

1.2 | | Food | 187.6 | 192.5 | 192.7 | 0.1 | | Feed | 634.6 | 629.1 | 631.5 | 0.4 | | Other uses | 253.1 | 274.2 | 284.8 | 3.9 | |

Ending stocks |

172.6 |

208.9 |

205.2 |

-1.8 | | | | |

SUPPLY AND DEMAND INDICATORS | | | Per caput food consumption: | | | | | | World (kg/year) | 28.1 | 28.5 | 28.2 | -1.1 | | LIFDC (kg/year) | 28.9 | 29.4 | 29.0 | -1.6 | | World stock-to-use ratio % | 15.8 | 18.8 | 18.2 | |

| Major exporters' stock-to-disappearanceratio % 2/ |

12.0 | 14.4 | 13.8 | | | | | | | | | |

2007 |

2008 |

2009 |

Change:

Jan-Nov 2009 | | | | | |

over

Jan-Nov 2008 | |

FAO Coarse Grains Price Index | | | | % | | (2002-2004=100) | 154 | 211 | 157* | -27 |

* January-November 2009

1/ Trade data refer to exports based on a common July/June marketing season

2/ Major exporters include Argentina, Australia, Canada, EU and the United States

PRODUCTION

|

|

Coarse grains output down from last year's record but still a satisfactory crop

|

|

FAO's latest forecast for world production of coarse grains in 2009 has been revised upwards in recent months and now stands at 1 109 million tonnes. Although down by 3 percent from last year's record, this would still be the second largest crop in history. The upward revision is virtually all attributed to improved yield prospects for the maize crop in the United States where generally favourable weather lasted throughout the growing season and this year's crop is now forecast well above last year's level and close to the 2007 record. Elsewhere, among the most significant producers of maize, the latest information confirms mostly smaller maize harvests in 2009, with the exception of the southern African region where, on aggregate, another good harvest was gathered earlier this year. With improved prospects for the United States' maize crop, world maize production in 2009 is now forecast at almost 805 million tonnes, only 1.7 percent down from 2008.

Regarding barley, the second most important coarse grain, the latest forecast points to a 4.5 percent decrease in global production in 2009, to some 146 million tonnes. Significant decreases in North America and Europe have more than offset gains in the other main barley producing nations, particularly in the Near East and North Africa. The forecast of world sorghum output in 2009 is put at 60 million tonnes, 8.5 percent down from the previous year's bumper crop, largely on account of a significant reduction in production in the United States after two consecutive good years.

|

Country* |

2008 estim. |

2009 f'cast |

Change: 2009 over 2008 | | |

million tonnes |

percent | | United States of America | 326.5 | 346.6 | 6.2 | | China (Mainland) | 175.9 | 167.2 | -4.9 | | European Union | 163.2 | 153.0 | -6.3 | | Brazil | 61.6 | 53.7 | -12.9 | | India | 39.1 | 34.8 | -11.2 | | Russian Federation | 41.7 | 31.7 | -24.0 | | Mexico | 31.9 | 30.1 | -5.7 | | Canada | 27.4 | 22.5 | -17.9 | | Nigeria | 26.0 | 26.0 | 0.0 | | Argentina | 27.0 | 16.7 | -38.1 | | Ukraine | 24.4 | 21.6 | -11.6 | | Indonesia | 16.3 | 17.0 | 4.4 | | Ethiopia | 12.7 | 11.2 | -11.9 | | Australia | 12.8 | 12.5 | -2.2 | | South Africa | 13.7 | 12.8 | -6.3 | | | | | | | Other countries | 142.8 | 151.3 | 5.9 | | | | | | |

World |

1 143.1 |

1 108.7 |

-3.0 |

* Countries listed according to their position in global production (average 2007-2009)

TRADE

|

|

World trade in coarse grains to decline slightly in 2009/10

|

|

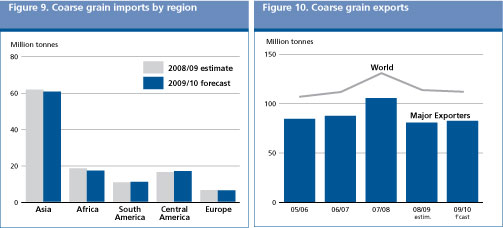

World trade in coarse grains in 2009/10 (July/June) is forecast to reach 112 million tonnes, down slightly from the estimated trade volume in 2008/09 but well below the record level of nearly 131 million tonnes in 2007/08. Most of the anticipated decline is expected in barley and to a lesser extent in sorghum while trade in maize is forecast to increase. World maize trade is expected to approach 86 million tonnes, up around 2 percent from the previous season but 16 percent below the 2007/08 all-time high. Higher maize imports are forecast for Canada and several countries in Latin America and the Caribbean. Trade in barley is forecast to reach 18 million tonnes, down 11 percent from last season's exceptional level, mostly on account of larger production in a number of leading importing countries in North Africa and Asia. Trade in sorghum is forecast to fall to 5.5 million tonnes, down 8 percent from the previous season and as much as 45 percent less than the record volume traded in 2007/08. Fewer transactions in sorghum principally reflect reduced demand for feed in the major destinations of the European Union, Japan and Mexico. For other coarse grains, trade is forecast to be smaller for oats at around 2 million tonnes, but steady for rye and millet, at 440 000 tonnes and 205 000 tonnes, respectively.

On a regional basis, imports of coarse grains by Africa are forecast to decline most, mainly because of bumper crops in several countries in the north of the continent: Morocco, in particular, where barley production was at a record. In sub-Saharan Africa, smaller imports by many countries, including Botswana, Mozambique, Zambia and Zimbabwe, are forecast to more than offset increases by countries in the eastern subregion that have been affected by drought. In Asia, total imports are forecast down only slightly from the record in 2007/08 and that, mainly by the Syrian Arab Republic following a recovery in domestic barley production; in the Islamic Republic of Iran due to a slight increase in production of barley and maize; and in the Philippines, following a record maize crop this year. In Latin America and the Caribbean, Mexico is seen to import more maize because of lower production and strong demand. Higher maize imports are also forecast for Chile, Colombia and Peru, which, combined more than offset declining imports by Brazil, which has emerged as a major maize exporter, and Venezuela on account of a bumper domestic maize production.

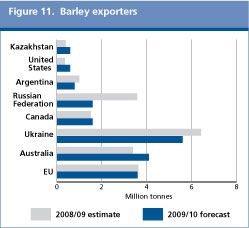

Given the current trade prospects for 2009/10, export supplies are ample enough to meet world import demand for all coarse grains. Among the major exporters only shipments from the United States are forecast to increase significantly, by over 7 million tonnes, while sales from Argentina could drop sharply because of supply shortfalls as a result of a 40 percent dip in domestic production. In Argentina, while export restrictions on maize have been eliminated recently, the Government will grant export permits in 2009/10 only in exchange for a commitment from exporters to guarantee 8 million tonnes of maize for the domestic market. Export sales by Australia, Canada and the European Union are likely to remain steady but much lower barley exports are anticipated from the Russia Federation, while shipments of maize from Ukraine are also expected to decline because of reduced production. In Brazil, where this year's maize output fell below last year's record, exports are still expected to be larger than the volume of the previous season due to adequate domestic supplies and slow sales from Argentina. Among the minor exporters, Malawi is expected to sell some 200 000 tonnes of maize to neighbouring countries following a record domestic harvest this year supported by the Government's lifting of a ban on exports in September. A bumper maize crop in Zambia also resulted in the removal of its maize export ban which is expected to lead to at least 260 000 tonnes of exports.

UTILIZATION

|

|

Slower growth in total utilization as feed use stagnates

|

|

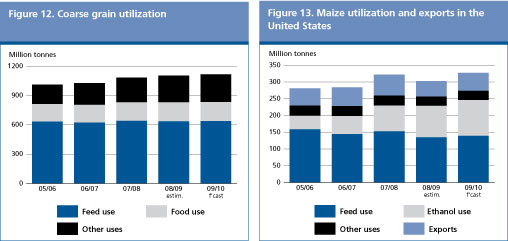

World utilization of coarse grains in 2009/10 is forecast to increase by 1.2 percent from the previous season. This compares with almost 2 percent growth in 2008/09 and well over a 5 percent expansion in 2007/08. The deceleration in total utilization of coarse grains mainly stems from weaker demand from the livestock sector along with a slower increase in the use of grains for the production of ethanol.

Total feed utilization of coarse grains in 2008/09 is forecast to reach 632 million tonnes, up by less than one percent from the previous season. Such tepid growth reflects the impact of economic problems in the United States and several other industrial countries which have dampened the demand for meat and other animal products, and therefore, the overall demand for feed. Large supplies of feed wheat as well as non-grain alternatives including Dried Distiller Grains (DDG), a by-product of maize-based ethanol manufacturing, are also considered important factors bearing down on feed usage of coarse grains in 2009/10. In fact, feed utilization of coarse grains in the developed countries is forecast to remain very much subdued from the previous season's reduced level while among developing countries, the small anticipated increase in this season's feed usage is likely to be driven mostly by Asia and, primarily China.

World food consumption of coarse grains is forecast to remain unchanged from the previous season, at around 193 million tonnes. This forecast is slightly higher than was anticipated at the start of the season but with improvements in production prospects, consumption estimates have also been revised up. At the current forecast levels, global food consumption of coarse grains on a per caput basis is expected to average around 28 kg, similar to the previous season, with generally steady levels of consumption regionwide.

Among the other usage categories, industrial applications of coarse grains, maize in particular, is likely to again demonstrate a brisk growth. The increase will be largely driven by continued strong demand from the fuel ethanol sector, most of which in the United States, where almost 107 million tonnes of maize is expected to be procured for processing into ethanol, up 14 percent from 2008/09. This growth, although robust, is slower than has been experienced in recent years.

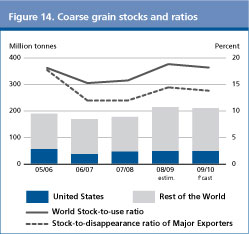

STOCKS

|

|

World stocks decline but less than anticipated

|

|

On the basis of the latest forecasts for production and utilization, global inventories of coarse grains for crop years ending in 2010 are forecast to reach 205 million tonnes, down 1.8 percent from their opening but still the second largest level since 2001. The forecast for the season's ending stocks has been raised by 3 million tonnes since the previous report in June mostly because of upward adjustments to forecasts for maize production in the United States. World maize stocks are likely to decline by around 2 million tonnes, to 158 million tonnes. Sorghum inventories could also fall slightly, to just under 6 million tonnes, but stocks of barley are seen to increase marginally, to 31 million tonnes.

For major exporters, ending stocks are forecast to reach 78 million tonnes, down 2 million tonnes from their relatively high opening levels. While carryovers in the United States are likely to remain unchanged, at around 47 million tonnes, some reductions are anticipated in Canada (for barley and maize) and in the European Union (maize). At the current forecast level, the ratio of major exporters' stocks to their total disappearance (i.e. domestic utilization plus exports), could decline slightly from the previous season's level, to around 14 percent, but should exceed the low level registered in 2007/08 by almost 2 percentage points.

The small reduction in total coarse grains' inventories in major exporting countries is partly offset by increases in North Africa and in several Asian countries, reflecting strong production in 2009. Maize inventories are forecast to increase in Africa, mostly in South Africa, and in Asia, mainly in China and Indonesia, but to decline in Latin America and the Caribbean, primarily in Brazil. Barley inventories are expected to end the season higher in Algeria and Morocco while in the Russian Federation and Ukraine they are heading for a decline.

|

December 2009

December 2009